- Specialty & Fine Chemicals

- Dimer Fatty Acids Market

Dimer Fatty Acids Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Dimer Fatty Acids Market by Product Type (Standard, Distilled, Distilled & Hydrogenated), Application (Reactive Polyamides, Non-Reactive Polyamides, Lubricant Additives, Surfactants & Plasticizers, Oilfield Chemicals, Other), Industry (Construction, Oil & Gas, Cosmetics, Other), and Regional Analysis for 2025 - 2032

Dimer Fatty Acids Market Size and Trend Analysis

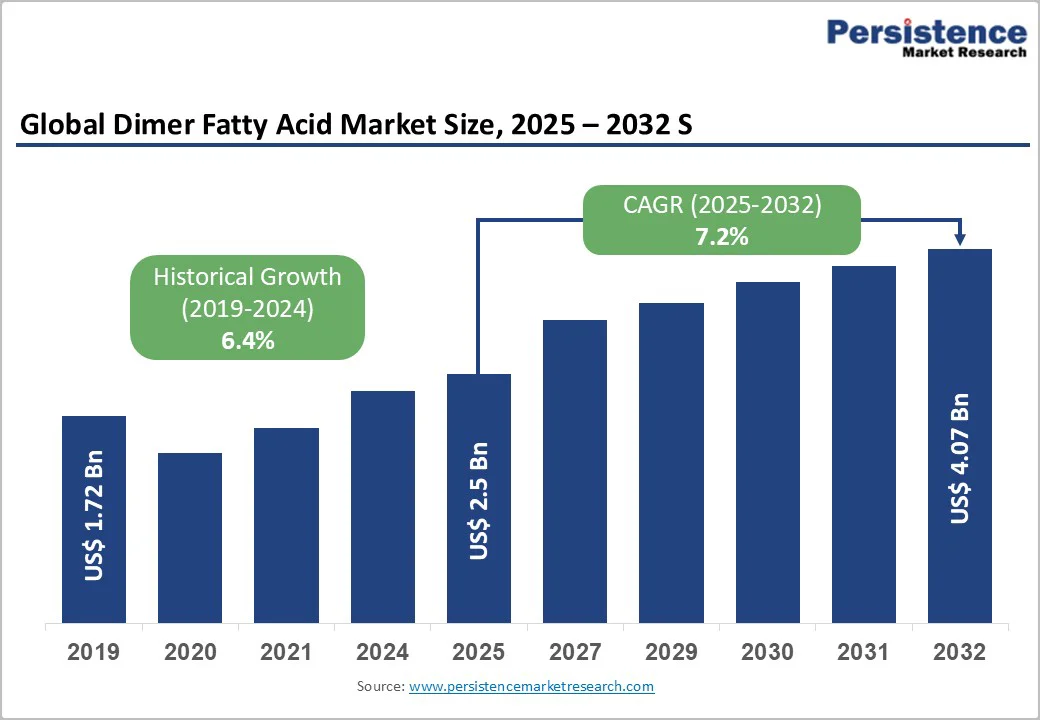

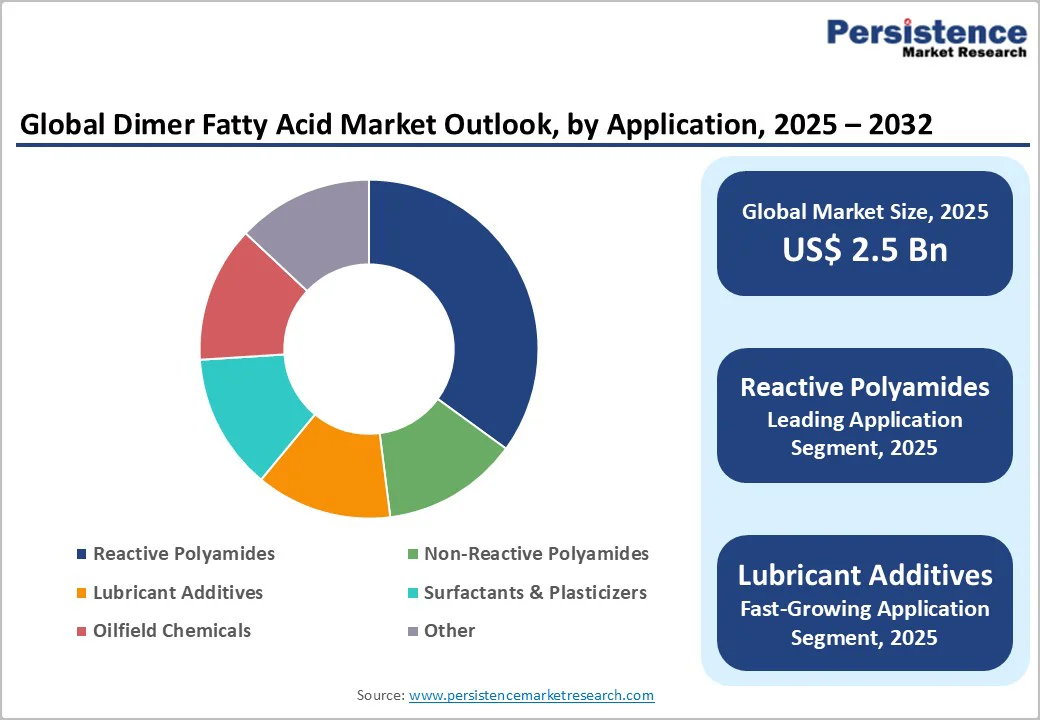

The global dimer fatty acids market size is valued at US$2.5 billion in 2025 and is projected to reach US$4.1 billion, growing at a CAGR of 7.2% between 2025 and 2032.

This robust growth trajectory is primarily driven by the growing demand for bio-based polyamide adhesives in construction and automotive sectors, where superior heat resistance and flexibility are critical performance requirements.

The market's expansion is further propelled by increasing adoption of sustainable chemical alternatives amid stringent environmental regulations across North America and Europe, coupled with rising consumption of specialty oilfield chemicals in emerging hydrocarbon exploration activities.

Key Market Highlights

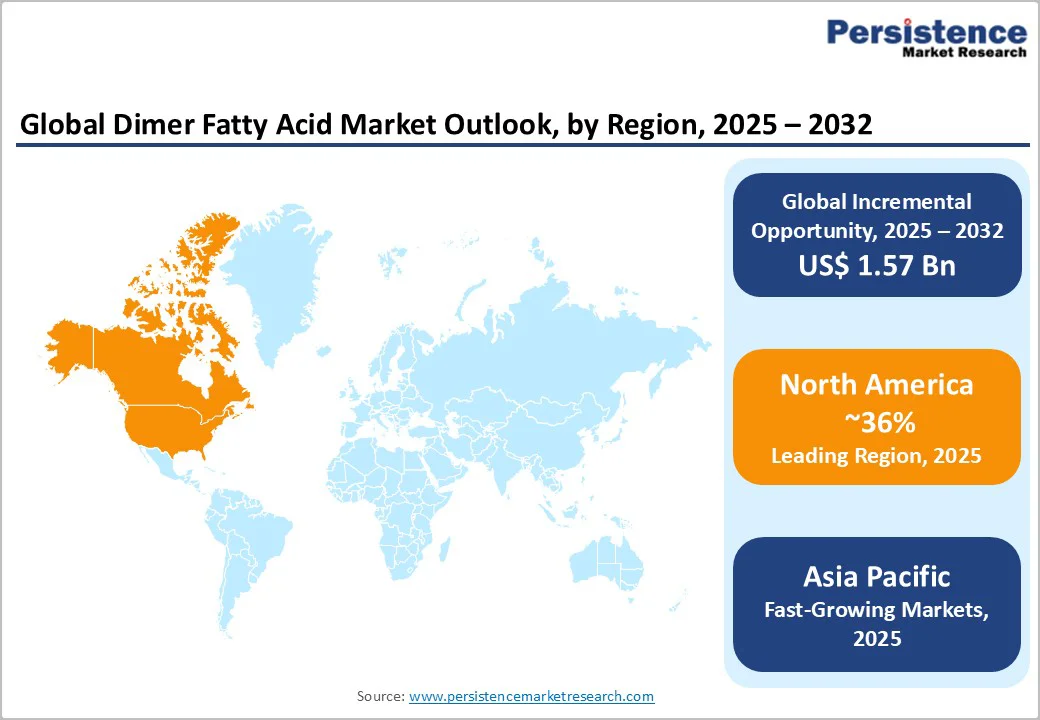

- Regional Leader: North America dominates the dimer fatty acids market, with 36% of the market share, due to strong U.S. oilfield demand and regulatory support for bio-based chemicals, ensuring steady growth through innovation ecosystems.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, propelled by China's manufacturing scale and India's infrastructure boom, offering untapped potential in adhesives and cosmetics.

- Leading Segment: Reactive polyamides stand as the dominant application segment, with 35% share, leveraging dimer acids for superior adhesion in industrial coatings and sealants worldwide.

- Fastest Growing Segment: Distilled product type is the fastest-growing segment, driven by purity demands in high-end polyamides and lubricants for sustainable applications.

- Growth Opportunities: Expansion in bio-lubricants presents a key opportunity, aligning with global sustainability trends and regulatory incentives for renewable industrial fluids.

| Key Insights | Details |

|---|---|

| Dimer Fatty Acids Market Size (2025E) | US$2.5 Bn |

| Market Value Forecast (2032F) | US$4.1 Bn |

| Projected Growth CAGR (2025 - 2032) | 7.2% |

| Historical Market Growth (2019 - 2024) | 6.4% |

Market Dynamics

Driver - Rising Demand in the Oil and Gas Sector

The escalating exploration and production activities in the oil and gas industry significantly propel the dimer fatty acids market forward. According to data from the Petroleum Planning and Analysis Cell, crude oil processing in India reached 21.6 million metric tons in April 2024, marking a 0.8% increase from the previous year, reflecting heightened global energy demands.

This surge directly correlates with increased usage of dimer fatty acids in hydraulic fracturing and well drilling, where their hydrophobic properties improve fluid performance and reduce operational costs.

Dimer acids serve as critical components in oilfield chemicals, including corrosion inhibitors, demulsifiers, and surfactants, which are essential for enhancing extraction efficiency and protecting equipment.

Imidazoline compounds synthesized from dimer fatty acids with alkyl chain lengths ranging from C16 to C22 demonstrate superior corrosion protection efficacy compared to conventional monomeric inhibitors when applied in molar ratios of 1:2 to 1:4 with dialkylene triamines.

Shift Toward Sustainable Bio-Based Materials

The global transition to renewable and eco-friendly materials is a key driver for the dimer fatty acids market, particularly as industries seek alternatives to synthetic chemicals. The European Union's Circular Economy Action Plan and USDA BioPreferred Program in North America have institutionalized preferential procurement of bio-based construction materials, creating regulatory tailwinds that amplify market penetration.

Research published by the National Institutes of Health demonstrates that dimer acids synthesized from plant oil fatty esters achieve bio-based content exceeding 90%, positioning them as sustainable alternatives to petroleum-derived monomers in adhesive formulations.

A 2020 United States Department of Agriculture report highlights the rapid expansion of bio-based chemicals, including fatty acids, due to lower carbon footprints compared to petroleum derivatives.

This shift is evident in applications like adhesives and coatings, where dimer acids provide superior flexibility and adhesion without compromising sustainability. With rising consumer preferences for green products, manufacturers are investing in bio-refinery integrations, which not only meet regulatory standards but also open new avenues in the Specialty Chemicals Market.

Restraints - Volatility in Raw Material Prices

Fluctuations in prices of raw materials like vegetable oils and tall oil pose a significant restraint to the dimer fatty acids market growth. These inputs, sourced from agricultural and forestry byproducts, are susceptible to supply chain disruptions caused by weather events and geopolitical tensions.

The palm oil prices rose by 30% in 2022 due to export restrictions from major producers like Indonesia, increasing manufacturing costs, and squeezing profit margins for fatty acid producers. This volatility affects production stability and discourages investment in capacity expansion. By 2025, average fatty acid prices reached USD 2,415 per metric ton in the U.S. and USD 4,315 per metric ton in Germany, highlighting regional supply-demand imbalances.

This volatility increases production costs for manufacturers, squeezing profit margins and deterring investments in capacity expansion. Consequently, end-users in cost-sensitive sectors such as oilfield chemicals may opt for cheaper synthetic alternatives, hampering the market's momentum despite its bio-based advantages.

Stringent Environmental Regulations

Stringent environmental regulations in key regions like Europe and North America act as a barrier for the dimer fatty acids market by imposing high compliance costs on production processes. Regulations such as the European Union's REACH framework require extensive testing for emissions and waste management, particularly for chemical dimerization involving acids and catalysts.

Regulatory concerns about the environmental impact of certain dimer acids have led to restrictions, especially in the European Union. The EU Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, limits hazardous substances and creates market uncertainty.

Compliance with these standards can elevate operational expenses by up to 15-20%, leading to delays in product approvals and market entry. While aimed at reducing pollution, these rules limit scalability for smaller producers and slow innovation in applications like cosmetics, where biodegradability must be balanced against regulatory hurdles.

Opportunity - Expansion in Bio-Lubricants and Green Formulations

The burgeoning demand for bio-lubricants presents a substantial opportunity for dimer fatty acids market participants, driven by the global push for sustainable industrial fluids.

Dimer acids' unique properties, such as high viscosity index and oxidative stability, make them ideal for formulating lubricants used in automotive and machinery sectors, replacing petroleum-based options. The Bio Lubricants Market is witnessing robust growth, with projections indicating a compound annual increase fueled by regulatory incentives like the U.S. Farm Bill promoting renewable feedstocks.

Companies can capitalize by developing hydrogenated variants tailored for high-performance applications, targeting emerging markets in Asia where industrialization is accelerating.

Croda International Plc's acquisition of Solus Biotech in February 2023, a transaction focused on biotechnology-derived beauty actives, signals strategic industry positioning to leverage oleochemical platforms including dimer acids for premium cosmetic applications. Such opportunities not only diversify revenue streams but also aligns with circular economy principles, promising significant returns through partnerships with OEMs and eco-conscious brands.

Growth in Cosmetics and Personal Care Innovations

Innovations in the cosmetics industry offer promising opportunities for dimer fatty acids, particularly as formulators seek natural emollients and thickeners for clean beauty products. With rising consumer awareness of synthetic-free formulations, dimer acids derived from renewable sources provide skin-compatible benefits like moisture retention and non-comedogenic properties.

The cosmetic ingredients market is expanding rapidly, supported by statistics from the Personal Care Products Council showing a 5.8% annual rise in demand for bio-based actives post-2023. Developments such as their use in anti-aging creams and hair care, where they enhance product stability without irritation, are gaining traction.

Market players can leverage this by investing in R&D for distilled grades, targeting high-growth regions like Europe with its stringent EU Cosmetics Regulation. This segment's potential is further bolstered by e-commerce trends, enabling global reach and fostering collaborations with beauty giants for sustainable product lines.

Category-wise Analysis

Product Type Insights

The distilled segment leads the product type category in the dimer fatty acids market, holding approximately 42% market share. This dominance stems from its high purity and versatility, making it suitable for premium applications like polyamide resins and coatings, where low monomer content ensures better performance and color stability.

The distillation processes yield acids with reduced impurities, aligning with quality demands in pharmaceuticals and cosmetics. The distilled and hydrogenated grades achieve purity levels exceeding 95% dimer content measured by gel permeation chromatography (GPC) area percentage, with rosin acid content reduced to 1-10% through fractional distillation.

This leadership is further justified by its eco-friendly profile, reducing oxidative degradation in end-products compared to standard variants.

Applications Insights

Reactive polyamides represent the leading application segment in the dimer fatty acids market, commanding about 35% share due to their critical role in high-performance adhesives and coatings. These polyamides, formed by reacting dimer acids with diamines, offer exceptional flexibility, adhesion, and corrosion resistance, essential for industries like marine and automotive.

Reactive polyamides are extensively utilized in the construction industry, coatings, flooring systems, and aerospace adhesives, benefiting from superior mechanical properties and chemical resistance, differentiating them from competing formulations.

Their bio-based origin supports sustainability goals, justifying dominance as they withstand harsh environments while meeting low-VOC standards. This segment's prevalence is evidenced by increasing adoption in construction sealants, where durability translates to cost savings over time.

Industry Analysis

The Construction sector maintains market leadership with approximately 45% share among end-use industries, propelled by escalating consumption of polyamide hot melt adhesives for building materials, structural bonding applications, and advanced sealing systems.

This sectoral dominance reflects construction industry requirements for adhesive solutions offering superior heat resistance up to 100°C+, rapid solidification characteristics, and reliable long-term performance across diverse environmental conditions.

The narrow melting range exhibited by dimer acid-based polyamide adhesives enables precise application control during construction processes, with materials maintaining structural integrity below melting points while achieving immediate liquefaction at marginally elevated temperatures.

The European Union's regulatory framework promoting sustainable building materials through the Circular Economy Action Plan, combined with green building certification programs globally, amplifies specification rates for bio-based adhesives derived from renewable feedstocks.

Regional Insights

North America Dimer Fatty Acids Market Trends

North America demonstrates market leadership, with 36% of the market share, driven by the dominance of the U.S. in bio-based chemical adoption, supported by the USDA BioPreferred Program that mandates federal agencies and contractors provide preferential consideration to biobased products meeting performance, availability, and cost requirements.

This regulatory framework has certified over 2,500 products across 100 different product categories as biobased, creating institutional demand mechanisms that systematically favor dimer fatty acid-derived materials in government procurement.

The advanced automotive and aerospace industries extensively utilize reactive polyamide resin-based high-performance adhesives and coatings, supporting sustained demand for dimer acid across multiple industrial sectors that require premium formulations. Infrastructure spending initiatives and concrete floor coating adoption in residential and industrial markets further reinforce regional demand drivers, sustaining market expansion.

Europe Dimer Fatty Acids Market Trends

Europe's dimer fatty acids market is characterized by strong performance in Germany, the U.K., France, and Spain, underpinned by harmonized regulations like REACH that prioritize sustainable chemicals.

The European Union's Fertilising Products Regulation (FPR) establishes comprehensive criteria for soil-biodegradable products, with CE marking requirements effective from November 20, 2024, for biodegradable mulch films and October 17, 2028, for coatings and water retention polymers.

Germany's chemical cluster in Ludwigshafen leads in polyamide innovations, driven by automotive sector demands for lightweight, durable components. Oleon NV's expansion initiative through the acquisition of a blending plant in Conroe, Texas , with US$ 50 million investment in December 2022, while geographically located in North America, reflects European oleochemical majors' global footprint expansion strategies.

Asia Pacific Dimer Fatty Acids Market Trends

Asia Pacific exhibits dynamic growth in the dimer fatty acids market, with China accounting for the largest revenue share, driven by massive production capacity, expanding construction sector, and strategic positioning as both domestic consumer and international exporter. China leads in both standard and distilled dimer acid manufacturing, benefiting from lower production costs, a robust industrial base, and government support for sustainable chemical production.

Japan's market is characterized by technological sophistication, with Harima Chemicals Group, Inc., headquartered in Kobe , specializing in pine-derived chemical products, including tall oil derivatives, resin chemicals, and electronic materials.

Harima's patent portfolio includes advanced dimerization methodologies employing clay catalysts, lithium salts, and controlled reaction temperatures between 230-245°C to selectively produce acyclic dimer acids from plant-derived fatty acids.

Competitive Landscape

The dimer fatty acids market exhibits a moderately consolidated structure, with a handful of global players controlling over 50% share through strategic expansions and R&D investments. Companies focus on vertical integration, securing raw material supplies from sustainable sources to mitigate price volatility.

Key differentiators include bio-based purity and customized formulations, while emerging models emphasize circular economy partnerships for recycling polyamides. This landscape encourages innovation in green processes, balancing competition with collaborative sustainability efforts.

Key Market Developments

- March 2025: Croda International Plc announced expansion of its dimer acid production facility in North America to increase capacity and meet growing demand for bio-based reactive polyamide resins from construction and automotive adhesive manufacturers seeking premium sustainable formulations.

- January 2024: Oleon NV completed capacity capacity-doubling project at Ertvelde production facility, enabling 14,125 tons of annual processing capacity for premium-quality dimer and isostearic acids to support the lubricants, coatings, and cosmetics sector expansion throughout European and global markets.

- August 2024: BASF SE advanced bio-based portfolio transformation initiatives, emphasizing renewable feedstock integration across specialty chemicals lineup while maintaining performance parity with traditional formulations, signaling broader industry sustainability commitment and competitive positioning.

Top Companies in Dimer Fatty Acids Market

- Croda International Plc (United Kingdom): As a leader in specialty chemicals, Croda excels with its robust portfolio of bio-based dimer acids for polyamides and cosmetics, generating significant revenue through global expansions like the 2024 Singapore facility upgrade. Its maturity in sustainable sourcing strengthens market influence, with strong R&D driving innovation in high-purity grades.

- Emery Oleochemicals Group (Malaysia): Emery dominates with over 60 years in natural fatty acids, offering EMERY® dimer products renowned for flexibility in adhesives and lubricants. Headquartered in Asia, its influence stems from large-scale production and biodegradability focus, capturing key shares in oilfield applications via technical expertise.

- BASF SE (Germany): BASF leads through diversified portfolios, integrating dimer acids into epoxy systems for construction. Its global reach and R&D investments, including 2023 tech upgrades, underscore portfolio strength, with revenue leadership in Europe from compliant, high-performance formulations.

Companies Covered in Dimer Fatty Acids Market

- Croda International Plc

- Oleon NV

- Emery Oleochemicals Group

- Florachem Corporation

- Aurorium

- Aturex Group

- Nissan Chemical America Corp.

- Harima Chemicals

- Jinan Tongfa Resin Co., Ltd.

- BASF SE

- Arizona Chemicals

- Techmen Chemicals

- KLK Oleo

- Wilmar International

Frequently Asked Questions

The global dimer fatty acids market is valued at US$1.9 Bn in 2025 and expected to reach US$2.7 Bn by 2032, reflecting steady growth in bio-based applications.

Key drivers include rising oil and gas exploration, demanding oilfield chemicals, and the shift to sustainable bio-based materials in adhesives and coatings, supported by global energy needs.

Reactive polyamides lead with about 35% share, due to their use in durable adhesives and epoxy systems for construction and automotive sectors.

North America leads, driven by U.S. oilfield activities and innovation in sustainable chemicals, capturing a significant global share.

Growth in bio-lubricants offers a prime opportunity, with dimer acids enabling eco-friendly formulations amid regulatory pushes for renewables.

Prominent players include Croda International Plc, Emery Oleochemicals Group, and BASF SE, leading through R&D and sustainable production expansions.