- Industrial Goods & Service

- Fastening Power Tools Market

Fastening Power Tools Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Fastening Power Tools Market By Product Type (Cordless Drills, Nail Guns, Others), Technology (Manual, Electric, Pneumatic, Hydraulic, Hybrid), Application (Automotive, Aerospace & Defense, Construction, Electricals & Electronics, Others), and Regional Analysis for 2025 - 2032

Fastening Power Tools Market Share and Trends Analysis

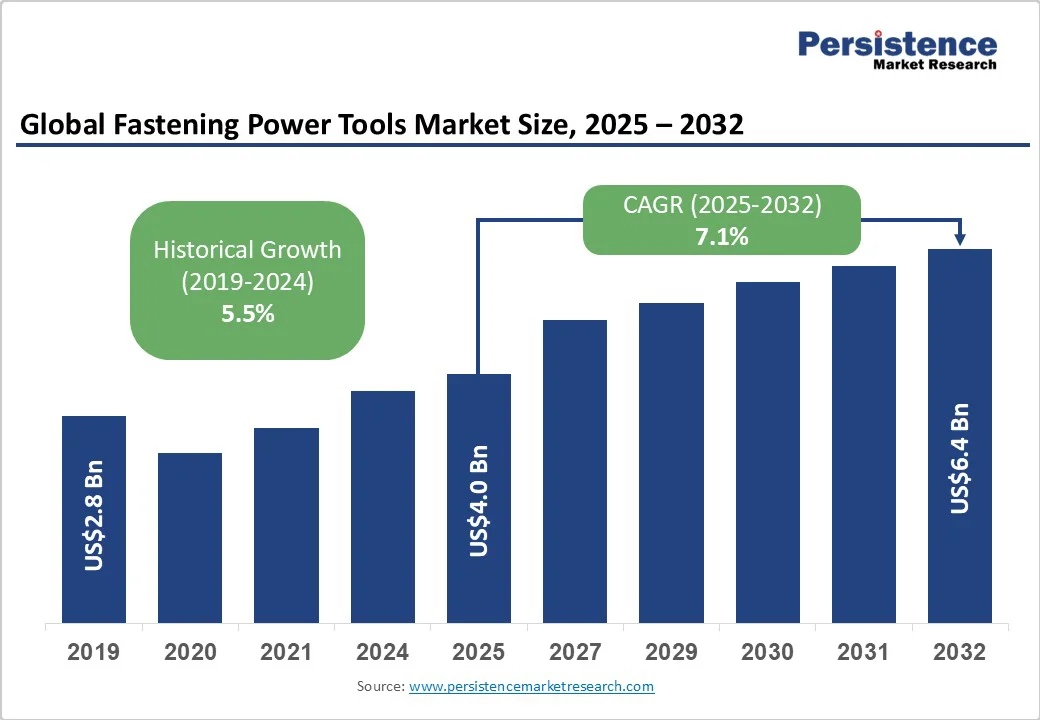

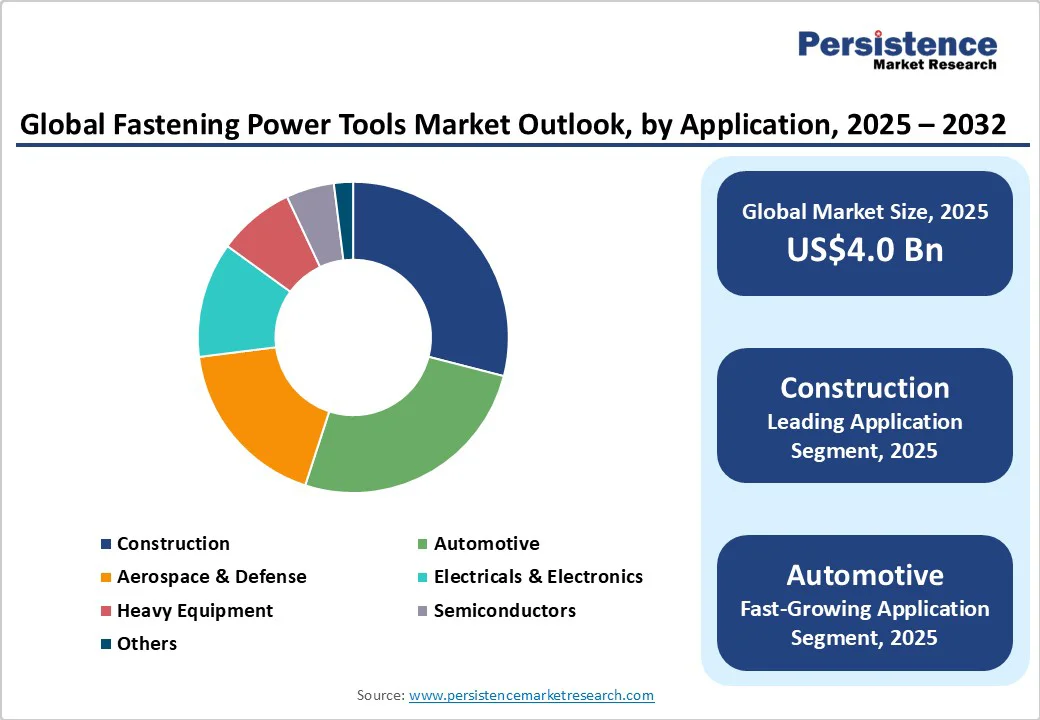

The global fastening power tools market size is likely to be valued at US$4.0 Billion in 2025 and is estimated to reach US$6.4 Billion by 2032, growing at a CAGR of 7.1% during the forecast period 2025-2032, driven by robust expansion in construction and automotive manufacturing sectors, with global infrastructure investments and vehicle production modernization creating sustained demand for efficient assembly solutions.

Technological advances in lithium-ion batteries and AI-powered smart tools are transforming the industry by boosting productivity, extending runtime, and enabling predictive maintenance. The move toward cordless and electric systems is replacing pneumatic tools, while Industry 4.0 and smart factories drive demand for IoT-enabled fastening tools with torque control and automated assembly.

Key Industry Highlights

- Leading & Fastest-growing Product Type: Cordless drills will retain leadership at 38.0% value share in 2025, while electric screwdrivers will post the fastest growth, advancing at a forecast CAGR of 9.2% by 2032.

- Leading & Fastest-growing Technology: Pneumatic tools command technology segment dominance at 35.0% in 2025, but cordless electric tools will expand fastest at 10.4% CAGR through 2032.

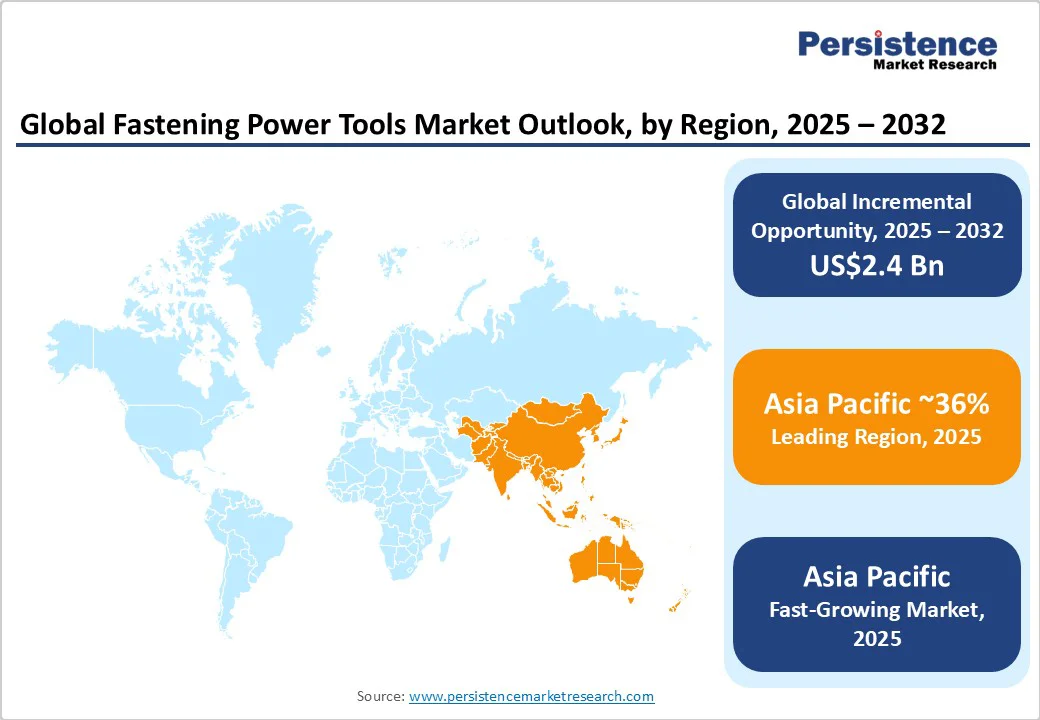

- Dominant Region & Fastest-growing Region: Asia Pacific is set to retain a 36.0% market share in 2025, also emerging as the fastest-growing regional market at 8.2% CAGR.

- Leading Application Type: The construction sector holds a 29.0% share in global applications, with the automotive segment advancing at 8.3% CAGR from 2025 to 2032.

- Key strategic developments: Large investments in battery R&D, partnerships for torque-controlled tool launches, and geographic expansion moves among leading firms.

- April 2025: Hillman Group unveiled the next generation of its Power Pro® fasteners, featuring a dual thread design that enables 30.0% faster engagement into wood, significantly reducing installation time while maintaining strong holding power.

| Key Insights | Details |

|---|---|

|

Fastening Power Tools Market Size (2025E) |

US$4.0 Bn |

|

Market Value Forecast (2032F) |

US$6.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Macroeconomic Expansion in Construction and Industrial Manufacturing

The rapid expansion of the construction and automotive sectors is significantly boosting demand for fastening power tools. Investments in infrastructure and vehicle manufacturing are key drivers, with the U.S. construction industry contributing over US$1.36 Trillion to GDP in 2022 and China reporting over 7% annual growth in infrastructure investment. Power tools that offer fast assembly, precision, and ergonomic advantages are increasingly preferred for improving productivity and meeting safety standards such as OSHA and the EU Machinery Directive. As electric and pneumatic tools become standard on job sites and assembly lines, this market growth is expected to accelerate through 2032, especially in Asia Pacific.

Technological Innovations in Battery Systems, Automation, and Smart Integration

Industry leaders are advancing battery tech, AI automation, and modular tool platforms. Lithium-ion batteries now offer longer runtime, faster recharging, and lower maintenance than legacy systems. The IEA forecasts a 15.0% CAGR in global lithium-ion battery capacity through 2030, fueling cordless tool adoption. AI-powered fastening tools enhance predictive maintenance and minimize downtime, aligning with ISO 13849. Innovations such as brushless motors, IoT-enabled management, and real-time torque monitoring are transforming workflows. According to the European Federation for Welding, these advancements boost project efficiency by 20.0%–25.0%, driving widespread adoption across industrial settings.

Barrier Analysis - Raw Material Price Volatility and Supply Chain Disruptions

Volatility in alloy, lithium, and semiconductor prices, spiking up to 24.0% per the London Metal Exchange, has heightened cost uncertainty. Global supply chains, still vulnerable to geopolitical tensions and post-pandemic disruptions, are compounding pressure on OEMs, leading to margin compression and higher customer prices. According to the 2025 Global Manufacturing & Supply Chain Survey, 18.0% of respondents cite raw material instability as a key obstacle to capital investment and product development.

Regulatory and Competitive Barriers in Import-Heavy Regions

Stringent import duties, evolving safety regulations, and rising certification costs in Latin America, the Middle East, and parts of Asia are limiting foreign manufacturers access. In Europe, stricter CEN standards on noise, vibration, and energy efficiency require costly product reengineering, delaying market entry. The WTO reports that global compliance costs have risen 6.8% annually. Intensifying competition from local players, particularly in Asia Pacific and Eastern Europe, is prompting global brands to reassess supply chain and innovation strategies.

Opportunity analysis - Emergence of Smart Factories and Manufacturing Automation

The transition to Industry 4.0 and smart factories is presenting significant growth opportunities for fastening power tool providers. Automated assembly lines and predictive maintenance protocols are enabling manufacturers to reduce labor costs by 30.0%–40.0% while enhancing quality control. Governments, including Germany’s Federal Ministry for Economic Affairs and Energy, are incentivizing digitalization through grants and tax credits, accelerating tool upgrades and spurring capital investment.

Industrial Development in Emerging Markets

Rapid industrialization, rising consumer incomes, improving business environments, and government-led infrastructure programs in the major economies of India, China, Vietnam, and Brazil are boosting market access. The India Brand Equity Foundation projects domestic power tool consumption to grow at an 8.0% CAGR through 2032, with fasteners being integral to new construction and automotive investments. Power tool manufacturers are targeting local partnerships, distribution agreements, and price-sensitive segments to capitalize on unmet demand in both consumer and industrial verticals. By 2032, emerging markets are forecasted to collectively account for 35.0% of global fastening power tool revenues, up from 29.0% in 2025.

Category-wise Analysis

Product Type Insights

Cordless drills are slated to continue as the dominant product type, capturing approximately 38.0% of the market value in 2025. Their popularity is primarily driven by enhanced mobility and operational efficiency, which are critical on large construction sites and expansive assembly operations. Advances in lithium-ion battery technology are central to this growth, enabling longer run times, faster charging, and supporting multi-shift work environments with minimized downtime. The ergonomic designs incorporated in recent models improve user comfort and reduce fatigue, encouraging adoption among professionals.

Meanwhile, electric screwdrivers are emerging as the fastest-growing segment, with a projected CAGR nearing 9.2% through 2032. Growth is fueled by expanding consumer electronics manufacturing and the demand for precise torque control in automated assembly lines, where these tools offer superior accuracy and repeatability. Manufacturers are enhancing these tools with wireless capabilities and safety-compliant features to meet rigorous industrial standards while maximizing productivity.

Technology Insights

Pneumatic fastening tools are projected to retain a 35.0% market share in 2025, driven by their dominance in automotive, metal fabrication, and heavy equipment manufacturing. Valued for high torque, reliability, and rapid cycle times, they excel in demanding, high-volume production environments. Their simple mechanical design ensures lower upfront costs and easy maintenance, making them a preferred choice across traditional manufacturing sectors requiring consistent, high-power output.

The electric and cordless segment is set to grow at a rapid CAGR of 10.4% from 2025 to 2032, fueled by advances in lithium-ion batteries, modular designs, and smart factory integration. These tools now rival pneumatic systems in performance while offering greater mobility and eliminating air supply dependency. AI-enabled sensors and brushless motors enhance safety, efficiency, and predictive maintenance. As Industry 4.0 adoption accelerates, electric and cordless tools are becoming the preferred choice across key manufacturing sectors.

Application Insights

The construction sector remains the largest application market for fastening power tools, holding an estimated 29.0% revenue share in 2025. This strong position is attributable to accelerating urbanization, significant investments in large-scale infrastructure projects, and widespread renovation activities around the world. Growing urban populations and government initiatives to upgrade transportation, commercial, and residential infrastructure sectors continuously fuel demand for fastening tools that offer reliability, efficiency, and ease of use on construction sites. Moreover, the increasing adoption of cordless, battery-powered fastening tools with ergonomic designs supports improved worker productivity and safety, reinforcing the sector's market dominance.

In contrast, the automotive sector stands out as the fastest-growing application segment, expected to expand at a robust CAGR of 8.3% from 2025 to 2032. This rapid growth is propelled by several key trends, including the sharp rise in electric vehicle (EV) production worldwide, which demands precise and consistent fastening to meet stringent safety and quality standards. Additionally, rising automation and digitalization in automotive manufacturing drive the adoption of torque-controlled and automated fastening solutions that enhance throughput and reduce assembly errors. Aggressive automotive production targets in rapidly industrializing countries such as China and India, as well as established markets in Europe, ensure sustained demand for advanced fastening technologies that support complex vehicle assembly lines.

Regional Market Insights

Asia Pacific Fastening Power Tools Market Trends

Asia Pacific is anticipated to occupy the top position in the market with an estimated share of 36.0% in 2025. China, Japan, and India will be the growth engines of the regional market, enabling it to expand at the highest CAGR through 2032. China’s rapid infrastructure investment and dominance in electronics and automotive manufacturing have generated unprecedented demand for power tools in the region, while India’s Make in India strategy and rising construction activity are propelling market growth. Meanwhile, Japan’s mature industrial sector and efficiency emphasis underpin adoption rates for advanced fastening solutions.

Regional regulatory regimes are increasingly supportive, with streamlined standards for imports and certification, accelerated by ASEAN’s harmonization initiatives. Competitive differentiation arises from low-cost manufacturing, high-volume exports, and widespread adoption of smart production paradigms. Investment flows are targeting industrial automation, domestic assembly facilities, and expansion of distribution networks across emerging urban centers.

North America Fastening Power Tools Market Trends

North America is expected to capture around 31.0% of the share in 2025, with the U.S. contributing approximately 60.0% of the regional share. Leading U.S.-based firms such as Stanley Black & Decker, Milwaukee, and Emerson Electric are fueling market gains through investments in battery R&D, product integration, and strategic distributor partnerships.

The regulatory environment, governed by OSHA workplace safety standards and supportive EPA regulations for energy-efficient equipment, continues to favor innovation and penetration. High consumer adoption of DIY tools, robust construction growth, and demand for precision automation in automotive and aerospace underpin market expansion. Investment trends are centered on financing innovation, mergers, and cultivating local technical talent.

Europe Fastening Power Tools Market Trends

Europe is set to command a significant 28.0% share of the fastening power tools market in 2025, with Germany, the U.K., France, and Spain representing the top-performing countries. The regional market growth is supported by regulatory harmonization under the European Machinery Directive and amplified investments in sustainable manufacturing.

Germany’s sophisticated automotive and mechanical engineering ecosystem is a key growth driver, while France and the U.K. are emphasizing fastener safety, material innovation, and production efficiency. Local firms are targeting smart fastening technologies and forging partnerships for R&D. Regulatory changes, especially related to energy efficiency, recycling compliance, and workplace ergonomics, are elevating product standards and facilitating cross-border trade. Investment activity includes acquisitions aimed at consolidating supply chains and enhancing technological capabilities.

Competitive Landscape

The global fastening power tools market features a moderately consolidated landscape, with the top five players, Stanley Black & Decker, Robert Bosch GmbH, Makita Corporation, Hilti Corporation, and Techtronic Industries, controlling nearly 50.0% of global revenue in 2025. The industry is structured around branded product differentiation and channel expansion, with high concentrations in North America and Europe. Market fragmentation is notable within localized and price-sensitive segments, but consolidation is intensifying through cross-border mergers and alliances. Leading players are distinguished by their breadth of product portfolios, strong regional presence, and emphasis on patent-protected innovations, particularly in lithium-ion and sensor-integrated technologies.

Key Industrial Developments:

- In September 2025, Informa Markets hosted the 23rd edition of India’s largest Hand Tools, Power Tools & Fasteners Expo (HTF) at the Bombay Exhibition Centre, Mumbai. The three-day B2B event featured 300+ exhibitors and served as a key sourcing platform for tools, fasteners, and manufacturing tech across automotive, construction, and engineering sectors. Co-located shows included the Cutting & Welding Expo, Used Machinery Expo, and Machine Tools Expo, creating a comprehensive industrial trade hub.

- In September 2025, Panasonic launched the Accupulse 4+ cordless torque tool, featuring industry-first Snug Torque Detection Level technology to prevent over- or under-tightening in mixed joint conditions. It also includes intelligent buffering for offline batch tracking and data syncing, boosting productivity. With cordless, one-handed operation, a non-contact transducer for precision, and a simplified software interface, the tool enhances both operator safety and setup efficiency.

- In March 2025, Bosch Limited launched a new range of hand tools for professionals, artisans, and home users, along with its I-Series industrial tools designed for automotive and heavy engineering sectors. The hand tools include over 100 ergonomically designed products with high-voltage safety certification up to 1,000V. The I-Series industrial tools offer torque presetting, NFC-based HMI locks to prevent unauthorized changes, and a fivefold increase in tool life, eliminating the need for two-step tightening.

Companies Covered in Fastening Power Tools Market

- Stanley Black & Decker, Inc.

- Robert Bosch GmbH

- Makita Corporation

- Hilti Corporation

- Techtronic Industries Co. Ltd.

- Emerson Electric Co.

- Atlas Copco AB

- Snap-on Incorporated

- Ingersoll Rand, Inc.

- Hitachi Koki Co., Ltd.

- Apex Tool Group, LLC

- Panasonic Corporation

- Kyocera Corporation

- Ridgid Tool Company

- Metabo Power Tools GmbH

Frequently Asked Questions

The fastening power tools market is projected to reach US$4.0 Billion in 2025.

Robust expansion in the construction and automotive manufacturing sectors, coupled with global infrastructure investments and vehicle production modernization, is driving the market.

The fastening power tools market is poised to witness a CAGR of 7.1% from 2025 to 2032.

Innovations in lithium-ion battery systems and AI-integrated smart tools, the accelerating shift toward cordless and electric platforms, and growing adoption of Industry 4.0 and smart factory systems are key market opportunities.

Stanley Black & Decker, Inc., Robert Bosch GmbH, and Makita Corporation are some of the key players in the fastening power tools market.