- Agrochemicals

- Europe Organic Fertilizer Market

Europe Organic Fertilizer Market Size, Share, and Growth Forecast 2026 - 2033

Europe Organic Fertilizer Market by Source (Animal-Based, Plant-Based, Mineral-Based), by Crop Type (Cereals and Grains, Fruits and Vegetables, Oilseeds and Pulses, Turf and Ornamentals, Miscellaneous), Form (Granules, Powder, Liquid), End-user (Agriculture, Horticulture, Residential and Gardens), and Country Analysis, 2026 - 2033

Europe Organic Fertilizer Market Size and Trend Analysis

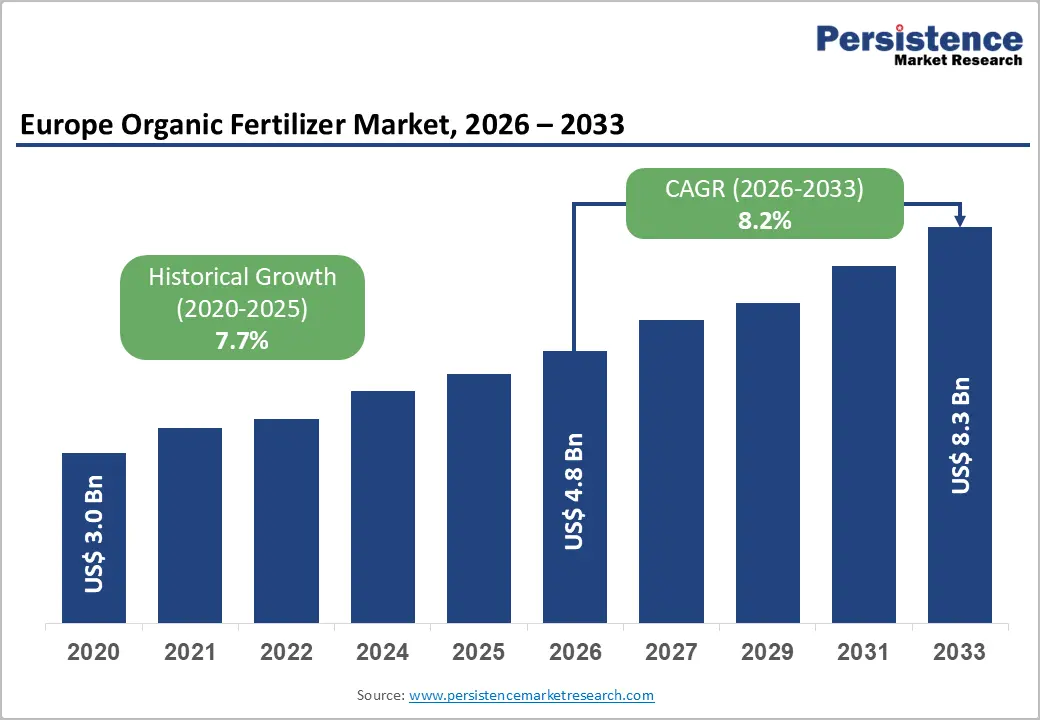

Europe organic fertilizer market size is expected to be valued at US$ 2.7 billion in 2026 and projected to reach US$ 4.2 billion by 2033, reaching a CAGR of 6.6% between 2026 and 2033.

The European Green Deal's Farm to Fork Strategy mandates that 25% of EU agricultural land shift to organic farming by 2030. Combined with the phased restriction of synthetic nitrogen fertilizers under the EU Nitrates Directive enforcement across member states, has fueled the demand for organic fertilizers in the region.

Consumer demand for certified organic food, with the EU organic food market growing at above 7% annually in recent years, creates a parallel commercial pull that directly compels farmers to adopt compliant organic fertilization programs, sustaining both volume and premium pricing dynamics across the forecast period.

Key Industry Highlights:

- Leading Country: Germany leads the region with approximately 21% revenue share in 2026, driven by the Federal Organic Farming Scheme, and stringent Fertilizer regulation nitrogen limits compelling organic fertilizer adoption in Nitrate Vulnerable Zones.

- Fastest Growing Country: BENELUX is the fastest-growing sub-region through 2033, propelled by the Netherlands' €10 billion+ annual greenhouse horticulture export sector, Belgium's intensive ornamental cultivation, and the EU FPR 2019/1009 circular economy fertilizer framework.

- Dominant Crop Type: Cereals and grains are dominant crop types with approximately 41% share in 2026, anchored by the EU's 55 million hectares of arable cereal cultivation, Farm to Fork organic transition mandates, and Nitrate Vulnerable Zone nitrogen management obligations compelling organic nitrogen substitution at scale.

- Fastest Growing Segment: Turf and ornamentals is the fast-growing application at a leading CAGR, driven by France's Loi Labbe synthetic fertilizer ban in public spaces, EU Sustainable Use of Pesticides Directive mandates, and urban greening programs.

DRO Analysis

Drivers - EU Farm to Fork Strategy and Organic Farming Targets Compelling Organic Fertilizer Adoption

The European Commission's Farm to Fork Strategy, a cornerstone of the European Green Deal, has institutionalized organic fertilizer demand through its binding target of converting 25% of EU agricultural land to organic farming by 2030, up from approximately 9.9% in 2020. As of 2022, the EU had approximately 16.4 million hectares under certified organic production, requiring transition farmers to replace conventional synthetic nitrogen with certified organic alternatives.

The EU Regulation 2018/848 on organic production mandates that organic farmers use exclusively permitted substances, a list that explicitly favors animal manure, composted plant materials, and mineral-origin organic fertilizers over synthetic inputs. Germany's Federal Organic Farming Scheme targets 30% organic agricultural area by 2030 while France's Ambition Bio 2027 plan allocates EUR 350 million to organic transition support, both programs structurally compelling organic fertilizer procurement at national scale.

Declining Soil Health and Nitrate Pollution Driving Shift from Synthetic to Organic Inputs

Documented soil degradation across European agricultural land, driven by decades of synthetic fertilizer over-application, is compelling agronomists, regulatory bodies, and farmers to transition toward organic fertilization as both an environmental obligation and a soil restoration strategy. The European Environment Agency (EEA) has documented that approximately 60-70% of European soils are in poor health, with nitrate leaching into groundwater exceeding EU Nitrates Directive (91/676/EEC) limits across vulnerable zones in Germany, Belgium, the Netherlands, and northern France.

EU has designated 62% of its agricultural area as Nitrate Vulnerable Zones (NVZs), where synthetic nitrogen application is strictly regulated. This regulatory framework is directly compelling farmers in high-fertility grain-producing regions, including the Rhine-Westphalia and Paris Basin agricultural corridors, to supplement or replace synthetic nitrogen programs with organic fertilizer products certified under EU Regulation 2019/1009.

Restraints - Higher Per-Hectare Cost of Organic Fertilizers Relative to Synthetic Alternatives

Despite long-term soil health benefits, organic fertilizers command a significant per-hectare cost premium over synthetic equivalents that constrain adoption among price-sensitive conventional farmers, particularly in cost-compressed commodity grain production. Organic fertilizer products typically deliver lower nutrient concentration per kilogram, requiring 3-5 times greater application volumes than synthetic alternatives to achieve equivalent nitrogen delivery, resulting in higher logistics, spreading, and labor costs per unit of nutrient applied.

For conventional farmers operating on thin margins in the EU cereals sector, where average farm gate wheat prices fluctuated between €180-260/tons in 2023-2024, the cost premium of organic fertilization programs creates a direct and measurable economic barrier to voluntary adoption beyond regulatory mandate areas.

Nutrient Release Variability and Application Precision Challenges in Organic Fertilizers

Unlike synthetic fertilizers with precisely defined NPK formulations, organic fertilizers exhibit inherent variability in nutrient content and unpredictable mineralization timing that complicates precision agriculture applications and integrated crop management planning. The nitrogen mineralization rate of organic fertilizers is temperature and moisture dependent, making accurate soil nitrogen supply prediction, a cornerstone of EU Nitrates Directive planning, substantially more complex than synthetic nitrogen management.

This variability creates agronomic uncertainty for farmers pursuing optimal yield-to-input ratios, particularly in high-value horticultural crops where over- or under-nutrition has direct consequences for product quality and marketability under GlobalG.A.P. and EU organic certification schemes.

Opportunities - Turf, Ornamentals, and Urban Horticulture as the Fastest-Growing Organic Fertilizer Application Segment

The Turf and Ornamentals are fast-growing applications at a projected CAGR of 7% in the forecast period. This represents a high-margin, volume-growing opportunity for organic fertilizer manufacturers operating in Europe's intensifying green spaces, professional turf management, and urban horticulture markets.

European municipalities are mandating pesticide and synthetic fertilizer elimination from public green spaces under the Sustainable Use of Pesticides Directive (SUD) revision, with France having banned synthetic fertilizers from public parks since 2020 under Loi Labbe, creating a mandatory organic-only procurement framework for municipal turf and ornamental management.

Germany's urban greening programs, the Netherlands' City Deal Climate adaptation, and Belgium's biodiversity-linked green infrastructure mandates are collectively generating institutionalized demand for organic turf fertilizers from specialist brands including COMPO Group, ICL, and Plantin S.A.R.L.

Circular Economy Compliant Organic Fertilizers from Industrial Byproducts and Biowaste Streams

The EU Fertilising Products Regulation (FPR) 2019/1009, which creates a harmonized single-market framework for recycled and organic fertilizers, has opened a transformational commercial opportunity for manufacturers developing certified organic fertilizer products derived from biowaste, sewage sludge digestates, compost, and industrial organic bystreams.

The Regulation's Component Material Categories (CMCs) explicitly enable struvite (phosphate recovery from wastewater), compost, digestate, and processed animal proteins to be marketed as CE-marked fertilizers across all EU member states, a framework that removes country-by-country approval barriers that previously fragmented the European recycled nutrient market.

ILSA S.P.A., which specializes in enzymatically hydrolyzed animal-derived organic nitrogen sources, and Fertikal N.V., operating in recycled nutrient streams in the Benelux, are positioned to benefit as the FPR creates a level regulatory playing field for circular economy-sourced organic fertilizer products across Europe's €30+ billion agricultural inputs market.

Category-wise Analysis

Source Insights

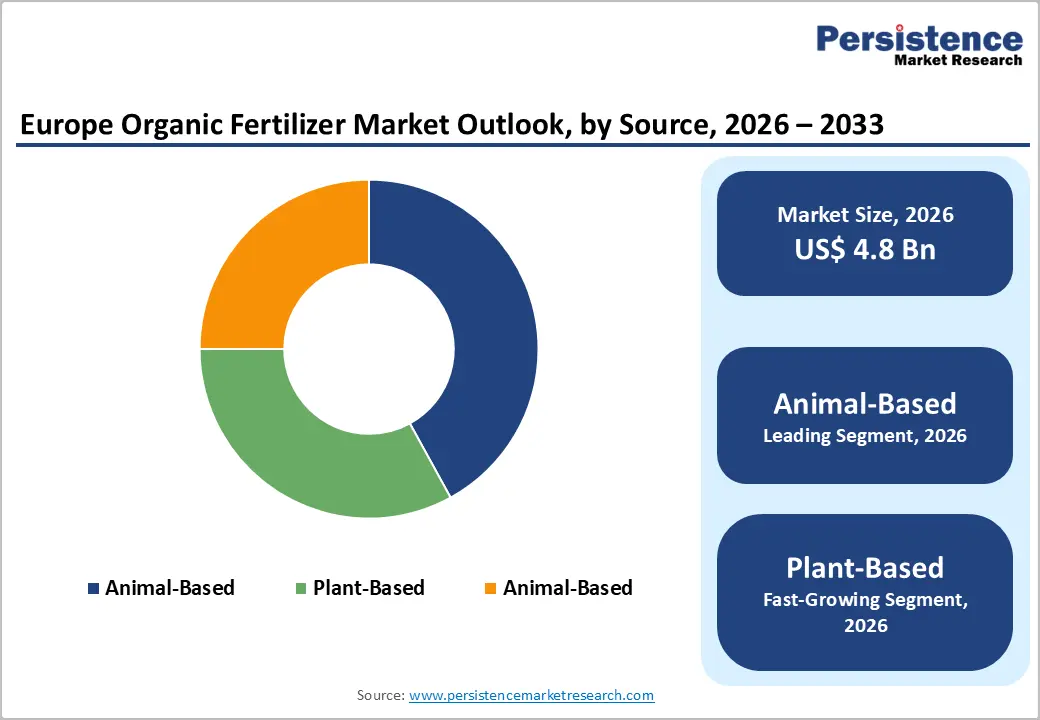

The animal-based source is leading and likely to command approximately 46% share in 2026. Animal-based organic fertilizers, encompassing composted manure, bone meal, blood meal, feather meal, fish emulsion, and enzymatically hydrolyzed animal proteins, as they deliver the broadest nutrient spectrum, including nitrogen, phosphorus, potassium, and essential micronutrients, in forms that align with EU Organic Regulation 2018/848 permitted substance lists.

The sheer scale of European livestock production, with the EU housing approximately 150 million cattle, pigs, and poultry units generating hundreds of millions of tons of organic matter annually, provides an abundant, locally sourced raw material base for animal-based fertilizer production at cost-competitive price points. IFFCO's manure-based product lines and ILSA S.P.A.'s hydrolyzed protein fertilizer platform both draw on this extensive European livestock input chain.

Crop Type Insights

The cereals and grains are the leading crop types, accounting for approximately 41% of the total share in 2026. Cereals, including wheat, barley, oats, rye, and maize, represent Europe's highest-area crop category by cultivated hectarage, with Eurostat reporting approximately 55 million hectares under cereals cultivation in the EU-27 as of 2023. The combination of arable area scale, transition of farmer obligations under the Farm to Fork organic farming target, and Nitrate Vulnerable Zone nitrogen management requirements collectively ensures cereals remain the highest-volume organic fertilizer application category.

Bulk granular and pelleted organic nitrogen products applied during spring establishment are the dominant product format for cereal organic fertilization, positioning granule-form animal-based and plant-based organic products as the primary revenue format within this leading segment.

Form Insights

Granules are likely to represent approximately 52% of the total share in 2026. Granulated organic fertilizers offer handling, storage, and application advantages that liquid and powder alternatives cannot replicate at a commercial scale, including free-flowing properties compatible with standard fertilizer spreader equipment, reduced dust generation during handling, controlled release characteristics through granule coating technology, and precise application uniformity across large arable fields.

For professional farmers applying organic fertilizers across hundreds of hectares in the cereal and oilseed sectors, granular form compatibility with existing broadcast spreading and precision placement equipment is a non-negotiable operational requirement. Yara's organic granular range, Coromandel International's granulated compost products, and COMPO Group's pelletized organic lawn and garden fertilizers all reflect the granule format's dominance across professional and consumer-facing market segments.

End-user Insights

Agriculture holds a huge prominence in Europe and accounts for 68% of total revenue share in 2026, reflecting the foundational role of large-scale arable, mixed, and permanent crop farming in driving organic fertilizer volume procurement. Professional agricultural operations, including EU-certified organic farms, transition farms, and conventional farms in Nitrate Vulnerable Zones, generate the highest per-user procurement volumes, typically sourcing organic fertilizers under annual supply agreements or cooperative purchasing frameworks.

France's over 60,000 certified organic farms and Germany's approximately 36,000 organic holdings represent the primary professional agriculture demand base driving this segment's dominance. The Horticulture end-use segment is the fastest-growing category, driven by the expansion of protected cultivation, high-value vegetable production, and the professional floriculture and ornamental sectors across the Netherlands, Germany, and Spain.

Country Analysis

Europe organic fertilizer market spans five primary countries: Germany, France, Italy, the U.K., and Spain, collectively representing the bulk of European organic agricultural production, regulatory-driven fertilizer demand, and distribution infrastructure. Germany leads with approximately 21% market share in 2026, while BENELUX is the fastest-growing sub-region through 2033, driven by circular economy fertilizer regulation and intensive horticulture expansion.

Germany Organic Fertilizer Market Trends and Insights

Germany's Organic Fertilizer market is valued at approximately US$ 0.56 Billion in 2026, anchored by the country's Federal Organic Farming Scheme targeting 30% organic agricultural area by 2030, approximately 36,000 certified organic farms, and one of Europe's most stringent Nitrate Vulnerable Zone enforcement regimes. Germany's Fertilizer regulation (Fertilizer Ordinance) imposes strict nitrogen application limits that directly drive organic fertilizer substitution in livestock-dense regions of Lower Saxony, Bavaria, and North Rhine-Westphalia.

U.K. Organic Fertilizer Market Trends and Insights

The U.K. organic fertilizer market is valued at approximately US$ 380 million in 2026, sustained by the Sustainable Farming Incentive (SFI) scheme under the ELMS (Environmental Land Management Scheme) which financially incentivizes soil organic matter improvement, a direct driver of organic fertilizer adoption. The U.K.'s approximately 9,000 certified organic farms managed by Organic Farmers & Growers (OF&G) and Soil Association Certification represent the primary professional organic fertilizer demand base.

France Organic Fertilizer Market Trends and Insights

France's Organic Fertilizer market is valued at approximately US$ 510 million in 2026, driven by the country's Ambition Bio 2027 program allocating EUR 350 million to organic transition support and the Loi Labbe banning synthetic fertilizers in public spaces since 2020. France has over 60,000 certified organic farms, and the Paris Basin, Europe's most productive cereal-growing region, is increasingly adopting organic and low-synthetic nitrogen management programs under NVZ compliance frameworks.

Italy Organic Fertilizer Market Trends and Insights

Italy's Organic Fertilizer market is valued at approximately US$ 430 million in 2026, reflecting the country's position as the EU's largest certified organic country by farm count, with over 80,000 organic farms. Italy's Mediterranean climate, supporting high-value organic fruit, vegetable, and olive production, with organic viticulture and horticulture commanding premium market prices, sustains consistent demand for specialty liquid and granular organic fertilizers from ILSA S.P.A. and international suppliers.

BENELUX Organic Fertilizer Market Trends and Insights

The BENELUX sub-region, comprising Belgium, the Netherlands, and Luxembourg, is the fastest-growing organic fertilizer market within Europe, estimated at approximately US$ 0.27 Billion in 2026. The Netherlands' globally leading greenhouse horticulture sector, producing over €10 billion in horticultural exports annually, and Belgium's intensive vegetable and ornamental cultivation are driving premium liquid and granular organic fertilizer demand. Fertikal N.V. and Plantin S.A.R.L. are key regional players serving the BENELUX specialty horticultural segment.

Competitive Landscape

The Europe Organic Fertilizer market exhibits a moderately fragmented competitive structure, with a mix of global agricultural inputs conglomerates, Yara, ICL, The Scotts Company, competing alongside European specialist organic manufacturers including COMPO Group, ILSA S.P.A., Fertikal N.V., and Plantin S.A.R.L. Key competitive differentiators are EU FPR 2019/1009 CE-marking capability, EU Organic Regulation 2018/848 permitted substance compliance, and application-specific formulation expertise for professional agriculture versus consumer garden segments.

A defining strategic trend is investment in biostimulant-organic fertilizer hybrid products that combine nutrient delivery with plant growth-promoting microorganism activity, creating premium positioning beyond pure nutrient commodity competition. Regional distribution network depth and proximity to large livestock-producing raw material sources are significant structural competitive advantages.

Key Developments

- In March 2025, Yara International launched a certified organic granular nitrogen product line under its YaraNatural brand, targeting transition farmers in Germany and France seeking drop-in organic nitrogen substitutes for conventional ammonium nitrate with equivalent spreading equipment compatibility.

- In November 2024, ICL Group expanded its Agroblen controlled-release organic fertilizer portfolio for European professional horticulture markets, launching new formulations certified under EU Regulation 2018/848 and EU FPR 2019/1009, targeting Netherlands and Belgium greenhouse operators.

- In June 2024, ILSA S.P.A. received expanded EU CE-mark approval under FPR 2019/1009 for its enzymatically hydrolyzed animal protein fertilizer range, enabling single-market distribution across all EU member states without country-specific regulatory approvals, significantly expanding its European addressable market.

Europe Organic Fertilizer Market - Key Insights

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 1.9 Billion |

| Current Market Value (2026) | US$ 2.7 Billion |

| Projected Market Value (2033) | US$ 4.2 Billion |

| CAGR (2026 - 2033) | 6.6% |

| Leading Country | Germany, 21% market share (2026) |

| Dominant Category-1 (Source) | Animal-Based, 46% market share (2026) |

| Top-ranking Category-2 (Crop Type) | Cereals and Grains, 41% market share (2026) |

| Incremental Opportunity (2026 - 2033) | US$ 1.5 Billion |

Companies Covered in Europe Organic Fertilizer Market

- IFFCO

- Yara International ASA

- The Scotts Company LLC

- COMPO Group

- Multiplex Group of Companies

- Sustane Natural Fertilizer Inc.

- ICL Group

- Coromandel International Limited

- T. Stanes and Company Limited

- TerraLink Horticulture Inc.

- ILSA S.P.A.

- Fertikal N.V.

- PUR VER

- Uniflor Poland Sp. z o.o.

- Plantin S.A.R.L.

- Humintech GmbH

- Bioiberica S.A.U.

- EuroChem Group AG

Frequently Asked Questions

The Europe Organic Fertilizer market is valued at US$ 2.7 billion in 2026, up from US$ 1.9 billion in 2020 at a historical CAGR of 4.3%. It is projected to reach US$ 4.2 billion by 2033 at a CAGR of 6.6%, representing an incremental opportunity of approximately US$ 1.5 Billion.

The two primary drivers are the EU Farm to Fork Strategy's binding target of 25% of EU agricultural land under organic farming by 2030, compelling certified organic and transition farmers to replace synthetic inputs with EU-permitted organic fertilizers, and the EU Nitrates Directive's designation of 62% of EU agricultural area as Nitrate Vulnerable Zones.

Germany leads with approximately 21% revenue share in 2026, valued at approximately US$ 2.6 billion, driven by the Federal Organic Farming Scheme's 30% organic area target by 2030.

The EU Fertilizing Products Regulation (FPR) 2019/1009 CE-marking framework for circular economy fertilizers from biowaste, struvite, and hydrolyzed protein streams represents the most structurally transformative opportunity, removing country-by-country approval barriers that previously fragmented the European recycled nutrient market.

The market is led by Yara International (YaraNatural certified organic range), ICL Group (Agroblen controlled-release organic platform), COMPO Group (professional and consumer organic fertilizers), ILSA S.P.A. (enzymatically hydrolyzed animal protein fertilizers certified under EU FPR and Organic Regulation), and Fertikal N.V. (BENELUX-based recycled nutrient organic fertilizers).