- Aerospace & Defense

- Europe eVTOL Aircraft Market

Europe eVTOL Aircraft Market Size, Share, and Growth Forecast, 2026 - 2033

Europe eVTOL Aircraft Market by Lift Technology (Vectored Thrust, Multirotor, Lift Plus Cruise), Mode of Operation (Piloted, Autonomous, and Semi-Autonomous), Range (0-200 Km, and 200-500 Km), Maximum Take-off Weight (MTOW) (<250 Kg, 250-500 Kg, 500-1500 Kg, and >1500 Kg),Application (Commercial, Military, and Emergency Medical Service), Propulsion Type and Regional Analysis for 2026 - 2033

Europe eVTOL Aircraft Size and Trends Analysis

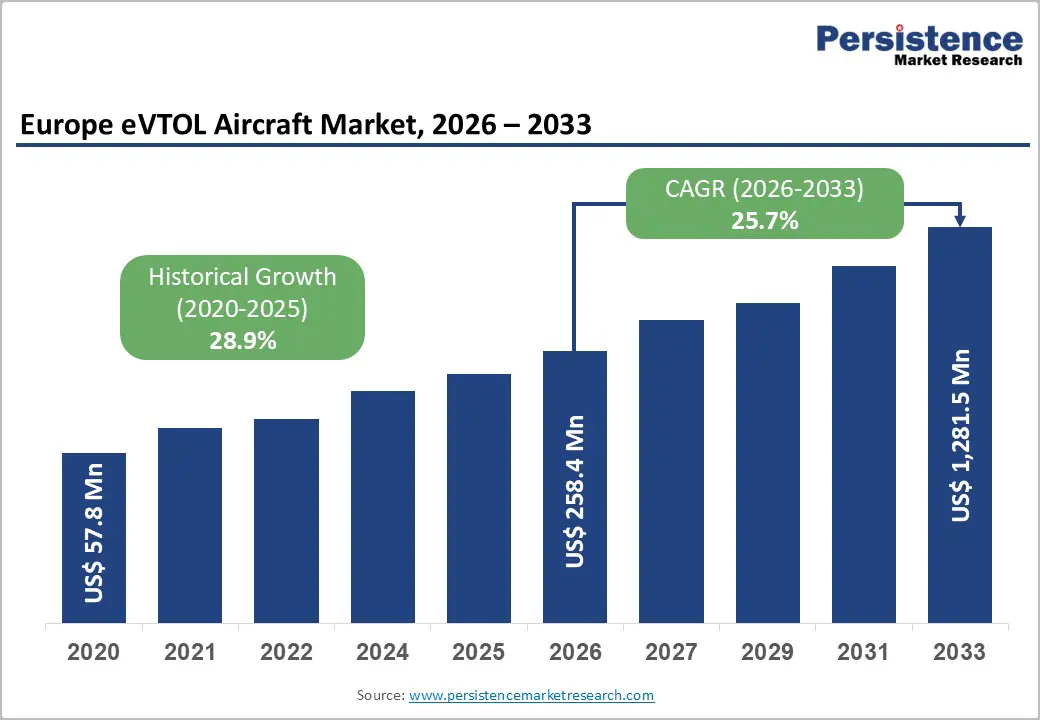

The Europe eVTOL aircraft market size is likely to be valued at US$ 258.4 million in 2026 and is projected to reach US$ 1,281.5 million by 2033, growing at a CAGR of 25.7% between 2026 and 2033. The market demonstrated strong historical momentum, recording a CAGR of 28.9% from 2020 to 2026, with the market valued at US$ 57.8 Million in 2020, reflecting a decade of accelerated technological investment and regulatory development. Primary growth factors include the formalisation of EASA's SC-VTOL certification framework for VTOL-capable aircraft, sustained public investment in sustainable transport infrastructure, and OEM-driven prototype milestones validating commercial readiness across air taxi, cargo, and emergency medical applications.

The European Commission's adoption of a secondary legislation package governing Air Operations, Flight Crew Licensing, and Air Traffic Management for VTOL platforms in April 2024 marked a decisive regulatory turning point, directly enabling accelerated certification and commercial service timelines.

Key Industry Highlights:

- Dominant Application: Commercial air taxi and cargo applications account for approximately 52% market share, supported by structured airport-to-city corridor strategies and national-level partnerships such as Archer Aviation’s deployment framework in Southeast Europe.

- Fastest Growing Application: EMS is the fastest expanding application, driven by institutional healthcare integration initiatives, including ADAC Luftrettung’s evaluation of up to 150 VoloCity aircraft and validated autonomous emergency response missions by EHang.

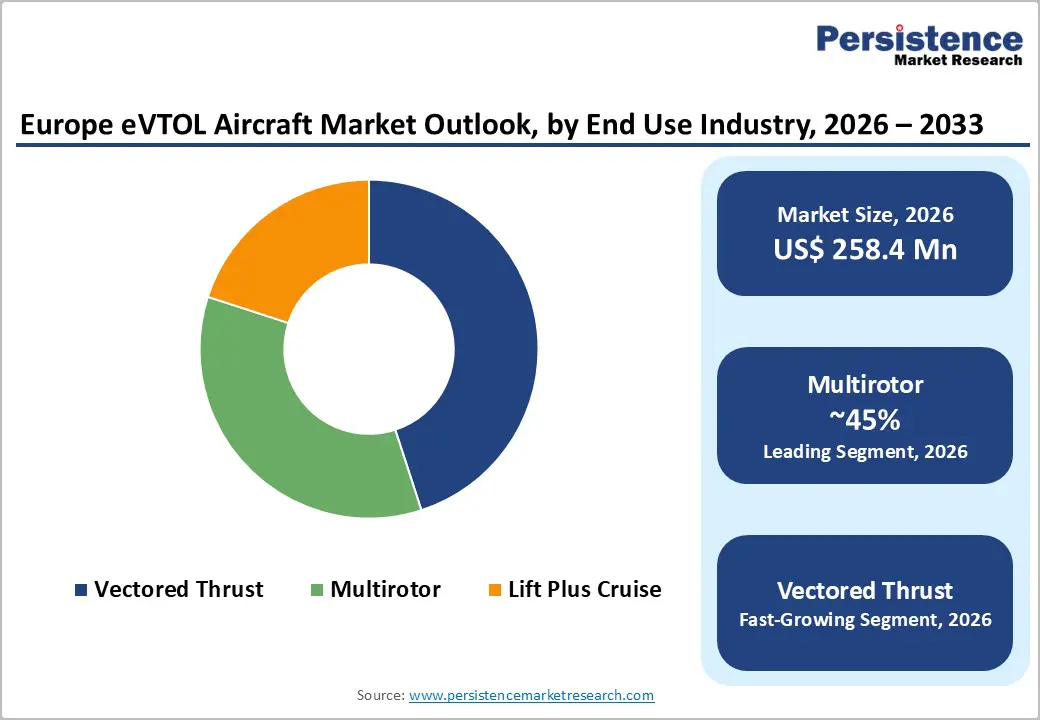

- Dominant Propulsion Type: Multirotor platforms hold nearly 44% market share, favored for short range urban missions due to mechanical simplicity, operational redundancy, and certification alignment under EASA SC VTOL standards.

- Fastest-growing Propulsion Type: Vectored thrust aircraft represent the fastest growing lift configuration, enabling higher cruise speeds and extended inter urban range, demonstrated by Vertical Aerospace’s wing borne flight validation of the VX4 platform.

- Regulatory Framework: EASA’s formalised Innovative Air Mobility regulatory architecture, with approximately 60% certification overlap with existing aviation standards, materially reduces timeline and compliance uncertainty.

| Key Insights | Details |

|---|---|

| eVTOL Aircraft Size (2026E) | US$ 258.4 Mn |

| Market Value Forecast (2033F) | US$ 1,281.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 25.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 28.9% |

Market Dynamics

Drivers - EASA Regulatory Advancement and the Formalisation of European IAM Frameworks

The European Union Aviation Safety Agency has established comprehensive regulatory architecture for Innovative Air Mobility, fundamentally strengthening the commercial viability of electric vertical take-off and landing eVTOL aircraft across Europe.

The European Commission adopted a secondary legislation package covering Air Operations, Flight Crew Licensing, and Air Traffic Management for VTOL-capable aircraft, creating a definitive legal foundation for commercial eVTOL services.

EASA’s SC VTOL Issue 2 framework actively governs certification campaigns, with MoC 4 to MoC 5 and SC VTOL Issue 3 completing a structured and transparent regulatory toolbox for electric vertical take-off and landing eVTOL aircraft approval. Volocopter has completed 75% of the required EASA audits for its VoloCity and holds both Design Organisation Approval and Production Organisation Approval, positioning it uniquely within Europe’s certification landscape. Vertical Aerospace further advanced regulatory progress through Europe’s first piloted wing-borne VX4 flight in open airspace, while approximately 60% of advanced air mobility certification requirements align with existing aviation standards, materially reducing regulatory risk and timeline uncertainty across the European eVTOL Aircraft Market.

Urban Congestion, Emission Reduction Mandates, and Demand for Sustainable Transport Corridors

European urban population density, combined with the European Green Deal's binding net-zero emissions agenda, has created structural, policy-driven demand for zero-emission vertical transport alternatives. The European Commission committed nearly €2.8 billion through the Connecting Europe Facility for 94 transport projects prioritising sustainable and connected mobility, reinforcing urban transport decarbonisation as a core policy objective.

The Commission allocated over €600 million to 70 projects deploying alternative-fuel infrastructure at airports and urban nodes, directly accelerating eVTOL ground readiness at key European hubs. Air freight and mail transport in the European Union reached 14.3 million tonnes in 2024, a 8.7% advance over 2023, with Frankfurt Main handling 2.0 million tonnes and Paris Charles de Gaulle handling 1.9 million tonnes, evidencing robust logistics demand that urban air mobility platforms are positioned to address.

The Europe eVTOL Aircraft Market benefits directly from this policy and infrastructure alignment, as vertiport development funding, airspace integration mandates, and emission reduction commitments converge to reinforce demand across commercial, cargo, and EMS deployment verticals.

Technological Maturation in Electric Propulsion, Battery Systems, and Prototype Validation Milestones

Rapid advancement in battery energy density, distributed electric propulsion architectures, and autonomous flight control has accelerated the European eVTOL Aircraft Market's transition from prototype validation to pre-commercial readiness. Conventional lithium-ion aviation batteries now achieve 200 to 300 Wh/kg energy density, with next-generation solid-state and sodium-ion battery chemistries under active development to extend range and payload capacity for longer-distance urban missions.

Vertical Aerospace completed Europe's first piloted wing-borne flight of an eVTOL in open airspace over Cotswold Airport in May 2025, approved by the UK CAA under the Flightpath 2030 strategy, representing a critical technology validation milestone. Munich-based ERC System completed the first public test flight of its heavy-lift Romeo eVTOL prototype at Erding military airfield in February 2026, a 2.7-tonne aircraft capable of piloted or unmanned operations with a six-seat capacity. EHang completed Europe's first multi-point-to-point urban emergency response flights with its pilotless EH216-S eVTOL in Zaragoza under the EU U-SAVE program in December 2025, setting a benchmark for autonomous eVTOL deployment. These milestones collectively confirm the technological pathway toward commercialisation across the Europe eVTOL Aircraft Market.

Restraint - High Capital Requirements and Financial Fragility Among European eVTOL OEMs

The Europe eVTOL Aircraft Market faces material financial sustainability challenges, as development costs for certification-grade aircraft run into hundreds of millions of euros with extended lead times before revenue generation. In Feb 2026, Lilium declared insolvency, laying off 1,000 employees, and Volocopter was acquired by China's Diamond Aircraft for €10 million, following billion-euro investment cycles that never reached commercial passenger operations.

These high-profile insolvencies signal caution for institutional investors, constraining the competitive pipeline of independent European OEMs and placing intellectual property and certification assets at risk of leaving the European ecosystem. Sustained access to capital remains a structural risk for the European eVTOL Aircraft Market.

Infrastructure Deficits in Vertiport Development and Urban Airspace Integration

Despite regulatory progress at the certification level, vertiport infrastructure, ground charging networks, and urban airspace integration systems required to support commercial eVTOL operations remain underdeveloped across European cities. EASA's guidance emphasises the availability of landing sites and energy management infrastructure as fundamental operational prerequisites, yet dedicated vertiport construction and municipal regulatory approvals have not kept pace with aircraft development timelines.

Coordination demands between aviation safety authorities, city planners, energy grid operators, and air traffic managers create multi-layered delays that extend the time to commercial service launch and reduce near-term deployment density across the Europe eVTOL Aircraft Market.

Opportunity - Emergency Medical Services Integration with National Healthcare and Aerial First-Response Networks

Emergency Medical Services represent one of the most strategically viable and high-value applications for electric vertical take-off and landing (eVTOL) aircraft in Europe, supported by the need for rapid patient transfer, time-critical organ and medical cargo delivery, and first response accessibility across dense urban and geographically complex regions. Healthcare systems are evaluating electric vertical take-off and landing platforms as complementary solutions to conventional helicopter fleets, particularly where lower operating costs, reduced noise levels, and zero emission performance strengthen operational efficiency.

Volocopter GmbH partnered with ADAC Luftrettung to integrate the VoloCity eVTOL into Germany’s emergency medical service framework, initiating research operations and evaluating broader fleet deployment for EMS missions. EHang successfully conducted Europe’s first multi-point-to-point urban emergency response flights in Zaragoza under the EU U-SAVE program, demonstrating the feasibility of pilotless aerial emergency services within regulated European airspace. ERC System developed the Romeo prototype specifically for emergency and hospital transport missions, targeting commercial deployment by 2031, while continued EMS-focused validation programs across Europe reinforce regulatory alignment and create a scalable procurement pathway for healthcare-integrated eVTOL adoption.

Cross-Border Operator Partnerships and Urban Air Mobility Network Scaling Across European Corridors

Strategic partnerships between eVTOL manufacturers, aviation service operators, and government authorities are shaping the commercial foundation for scalable urban air mobility networks across Europe. These collaborations support structured deployment along city-to-airport and inter-urban corridors, while aligning infrastructure development with regulatory compliance under the European Union Aviation Safety Agency (EASA). By formalising agreements early, stakeholders reduce commercialisation risk, enhance investor confidence, and accelerate public-sector validation of eVTOL services.

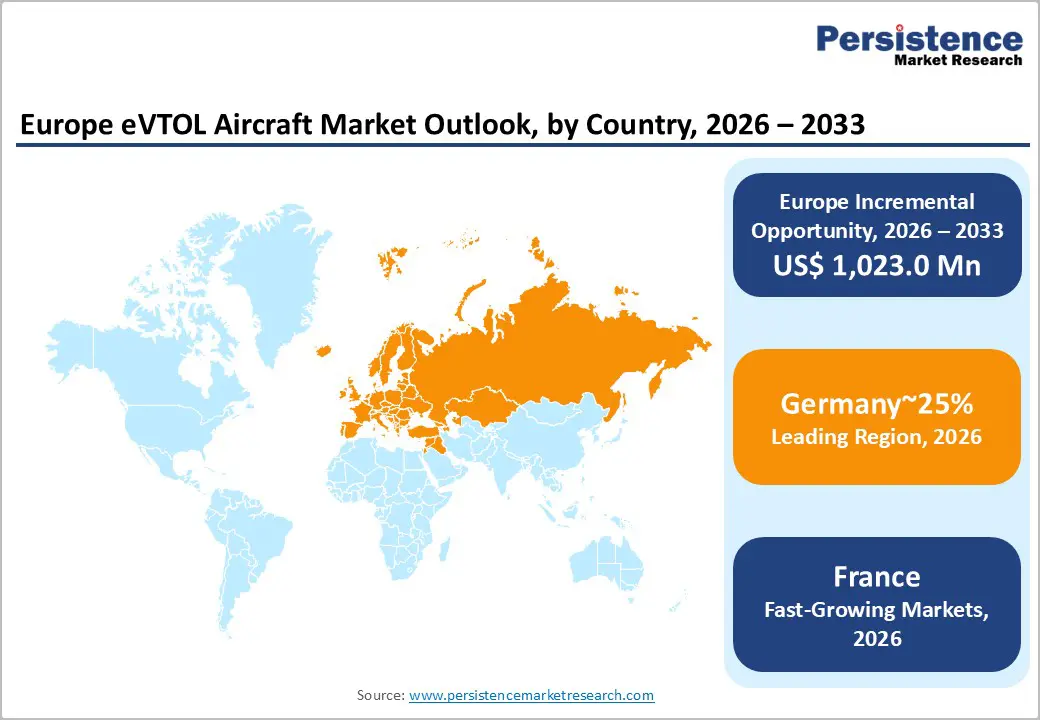

Volocopter GmbH partnered with Jet Systems Hélicoptères Services to deploy VoloCity operations in France, beginning in Paris and expanding to additional regional corridors through integrated fleet management and operational expertise. The Republic of Serbia selected Archer Aviation as its preferred partner for a national electric air taxi initiative, supporting infrastructure development and positioning Southeast Europe as an emerging urban air mobility hub. EHang established Europe’s first dedicated Urban Air Mobility Centre at Lleida-Alguaire International Airport, featuring a fully EASA-compliant vertiport to advance unmanned eVTOL integration. Collectively, these cross-border and institutional collaborations create a structured pathway for multi-city network expansion, strengthening the long-term scalability of the Europe eVTOL Aircraft Market.

Air Cargo and Logistics Demand as a Near-Term Commercial Deployment Foundation

European air cargo and logistics demand provides a practical near-term commercial pathway for electric vertical take-off and landing (eVTOL) aircraft cargo deployment, particularly across urban last-mile distribution, time-sensitive pharmaceutical shipments, and inter-hub freight connections. A cargo-first strategy allows manufacturers of electric vertical take-off and landing aircraft to generate early revenues while passenger certification advances through more complex regulatory processes. This phased deployment model reduces operational risk, enables real-world performance validation, and strengthens operator confidence prior to large-scale passenger service introduction.

Air freight and mail transport across the European Union reached 14.3 million tonnes, reflecting an 8.7% advance over the previous year, with intra-EU transport expanding by 9.1% and strong growth recorded in Hungary at 65.9% and Czechia at 43.7%. On a year-to-date basis, total cargo demand measured in cargo tonne kilometres advanced 3.1%, with international operations accounting for 87.3% share and growing 3.8%, indicating sustained reliance on cross-border freight connectivity.

Non-scheduled air freight services share advanced from 15% to approximately 20% over recent years, highlighting demand for flexible capacity solutions that align with eVTOL cargo capabilities. For the Europe eVTOL Aircraft Market, this logistics environment presents a commercially credible foundation to validate operational economics, strengthen supply chain integration, and support the transition toward broader certified passenger platforms.

Category-wise Analysis

Application Insights

The commercial segment holds the leading position in the Europe eVTOL Aircraft Market, accounting for approximately 52% of the total market in 2026, anchored by concentrated OEM investment in urban air taxi platforms and last-mile delivery drone services. The segment’s dominance reflects the scale of investor and government commitments to airport-to-city and interurban corridors as primary commercial use cases.

Vertical Aerospace’s Valo is designed for zero-emission airport-to-city services with a flexible six-passenger cabin, class-leading luggage capacity, and airliner-level certification targeted under EASA and UK CAA frameworks. The Republic of Serbia selected Archer Aviation as its preferred electric air taxi partner, holding an option to order up to 25 Midnight aircraft to support national air mobility deployment. This institutional backing underscores structured commercial adoption and reinforces the Commercial segment as the central growth engine within the Europe eVTOL Aircraft Market.

The Emergency Medical Service segment is the fastest-growing application within the European eVTOL Aircraft Market, reflecting operationally validated demand for rapid response aerial healthcare delivery across urban and semi-urban environments. ADAC Luftrettung agreed with Volocopter GmbH to evaluate up to 150 VoloCity aircraft for integration into Germany’s emergency medical service network, demonstrating structured institutional adoption.

Lift Technology Insights

The multirotor segment commands the leading position in the Europe eVTOL Aircraft Market, holding approximately 44% of total market share in 2026, attributed to its mechanical simplicity, operational redundancy, and well-suited design for short-range urban missions. Multirotor platforms offer inherent fail-safe capability through multiple independent rotors, simplifying certification under EASA's SC-VTOL framework and reducing pilot training requirements.

Volocopter's VoloCity, Europe's most advanced multirotor eVTOL, has completed 75% of EASA certification audits and holds both Design Organisation Approval and Production Organisation Approval, making it the benchmark platform for multirotor segment leadership.

The Vectored Thrust segment represents the fastest-growing lift technology within the European eVTOL Aircraft Market, driven by superior aerodynamic efficiency, extended range capability, and suitability for higher-speed airport-to-city and inter-urban transport missions. Vectored thrust aircraft employ tilting rotors or nacelles to transition between vertical lift and horizontal cruise flight, enabling range and speed profiles that substantially exceed multirotor configurations. Vertical Aerospace's VX4, which completed Europe's first piloted wing-borne eVTOL flight in open airspace over Cotswold Airport in May 2025, exemplifies the vectored thrust platform's technical maturity.

Competitive Landscape

Europe eVTOL aircraft market exhibits an emergent yet moderately consolidated competitive landscape, characterised by a mix of specialised European innovators and global aerospace incumbents advancing toward commercialisation.

Established European players such as Volocopter GmbH and Lilium GmbH lead with dedicated eVTOL platforms optimised for urban air mobility, leveraging deep aerospace engineering expertise and strong partnerships across cities and regulators. Airbus S.A.S., representing traditional aerospace leadership, brings scale, aviation certification experience, and broad industry influence, reinforcing the market’s credibility and investment appeal.

Strategic global entrants like EHang and Joby Aviation further intensify competition by introducing advanced autonomous and piloted eVTOL technologies, creating cross-regional technology transfer and benchmark standards. Although a handful of firms drive technological progress, barriers to entry remain high due to certification requirements, infrastructure needs, and capital intensity, resulting in a landscape that is moderately consolidated among a few technically and financially robust competitors. Collaboration with regulators such as EASA, combined with partnerships across OEMs, cities, and service operators, continues to shape competitive dynamics and differentiate leaders in Europe’s nascent eVTOL market.

Key Developments:

- In February 2026, ERC System completed the first public test flight of its heavy lift eVTOL prototype, Romeo, at Erding military airfield, Germany. The 2.7-tonne aircraft, capable of piloted or unmanned operations with a six-seat capacity, demonstrated its ability to lift substantial payloads, marking a significant step toward ERC’s plan to commercialise the eVTOL for emergency and hospital transport missions by 2031.

- In December 2025, Vertical Aerospace unveiled its new commercial eVTOL, Valo, in London, featuring a flexible six-passenger cabin, class-leading luggage capacity, and advanced aerodynamic design. Targeting EASA and UK CAA certification by 2028, Valo is engineered for zero-emission airport-to-city services, emergency medical, and cargo missions, marking a major step in Europe’s eVTOL commercialisation and the UK’s return to aircraft manufacturing leadership.

- On Feb,2025, Volocopter and Jet Systems Hélicoptères Services announced a partnership to launch VoloCity eVTOL operations in France, starting in Paris.The collaboration combines Volocopter’s eVTOL technology, pilot training, and fleet management with Jet Systems’ operational expertise.

Companies Covered in Europe eVTOL Aircraft Market

- Volocopter GmbH

- Lilium GmbH

- Airbus S.A.S.

- EHang

- Urban Aeronautics

- Joby Aviation

- Archer Aviation

- Beta Technologies

- Bell Textron

- Textron Inc.

- Eve Holdings

- Kitty Hawk

Frequently Asked Questions

Europe eVTOL Aircraft is projected to be valued at US$ 258.4 Mn in 2026.

The Commercial (Air taxi, Delivery drones) segment is expected to account for approximately 52% of the Europe eVTOL Aircraft by Application in 2026.

The market is expected to witness a CAGR of 25.7% from 2026 to 2033.

Europe eVTOL Aircraft Market growth is driven by EASA’s formalised Innovative Air Mobility regulatory framework, strong urban decarbonization and infrastructure funding under EU policy mandates, accelerating cargo and urban mobility demand, and rapid technological maturation in electric propulsion, battery systems, and validated flight-testing milestones across leading OEMs.

Key market opportunities in the Europe eVTOL Aircraft Market include Emergency Medical Services integration into national healthcare networks, cross-border operator partnerships enabling scalable urban air mobility corridors, and cargo first deployment strategies leveraging strong EU air freight demand to establish early commercial viability.

Key players in eVTOL Aircraft include Volocopter GmbH, Lilium GmbH, Airbus S.A.S., EHang, Joby Aviation, and Archer Aviation.