- Animal Feed & Additives

- Europe Calf Milk Replacer Market

Europe Calf Milk Replacer Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Europe Calf Milk Replacer Market by Product Type (Medicated, Non-medicated), by Form (Powder, Liquid), by Distribution Channel (Direct Sales/B2B, Retail/B2C), by End-use (Commercial Dairy Farms, Individual Farmers), and Country Analysis for 2025 - 2032

Europe Calf Milk Replacer Market Size and Trends

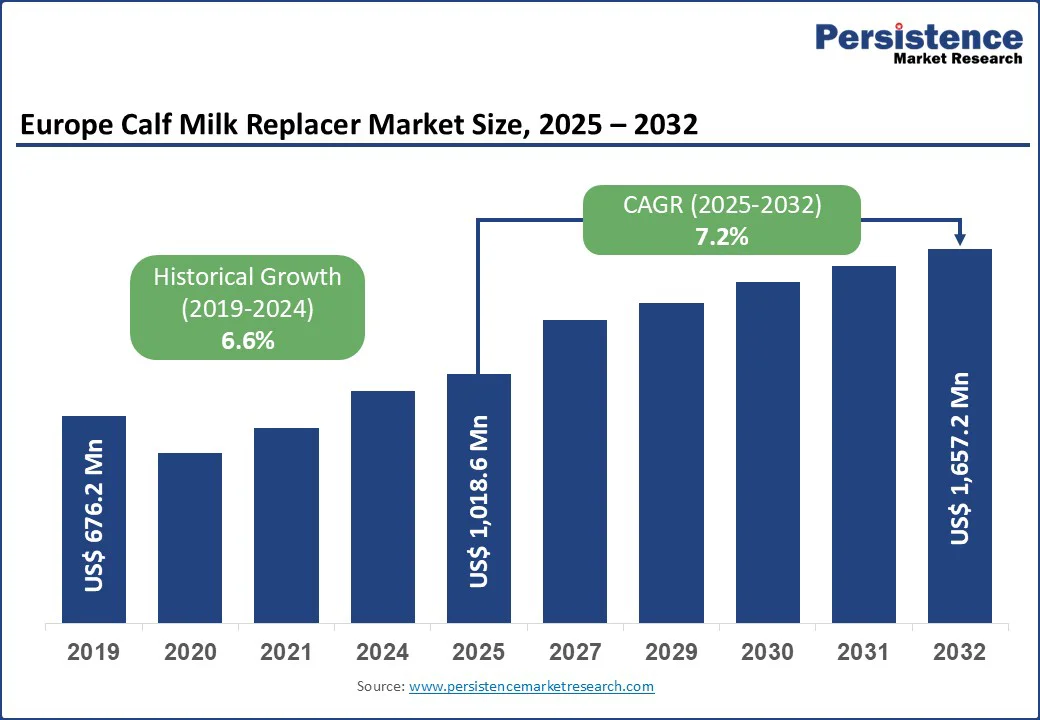

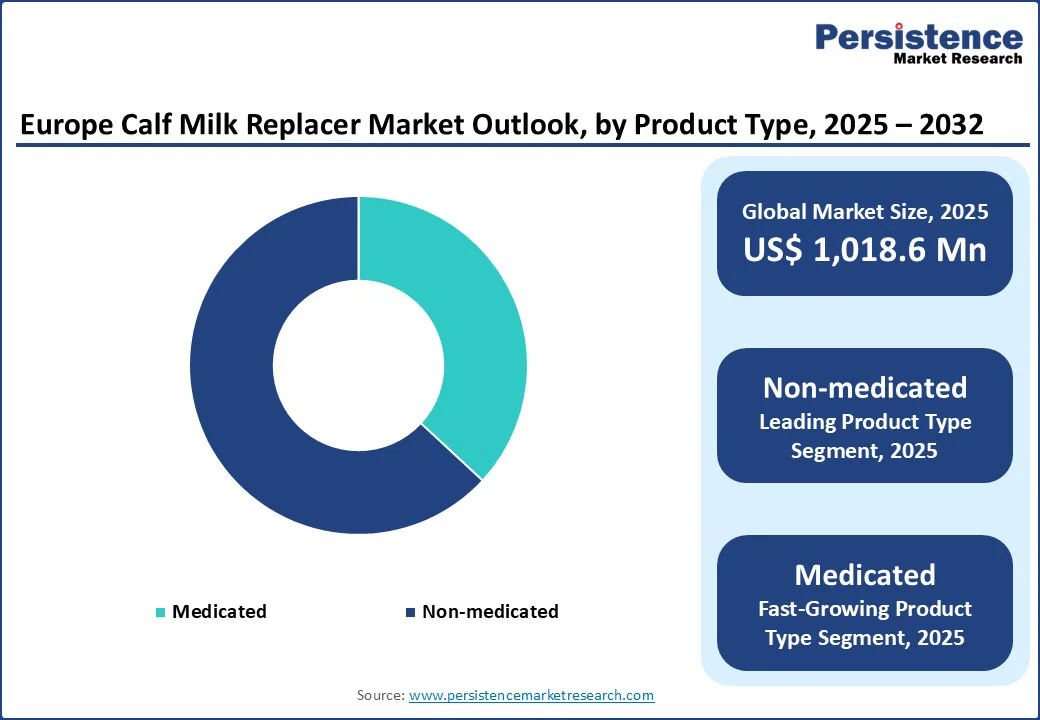

Europe calf milk replacer market size is likely to be valued at US$1,018.6 Mn in 2025. It is estimated to reach US$1,657.2 Mn in 2032, growing at a CAGR of 7.2% during the forecast period 2025-2032, driven by rising demand for unique calf nutrition solutions, expansion of intensive dairy farming, increased investment in fortified formulations, and ongoing regulatory push for animal welfare.

Key Industry Highlights

- Leading Product Type: Non-medicated calf milk replacers, with a nearly 63.1% share in 2025, driven by stringent EU antibiotic regulations and farmers' preference for natural growth solutions.

- Dominant Form: Powder recorded around 71.4% share in 2025, due to its long shelf life, ease of transport, and flexibility in mixing.

- Key Distribution Channel: Direct sales/B2B, approximately 66.3% share in 2025, as large dairy cooperatives and commercial farms prefer bulk purchases directly from manufacturers for cost efficiency.

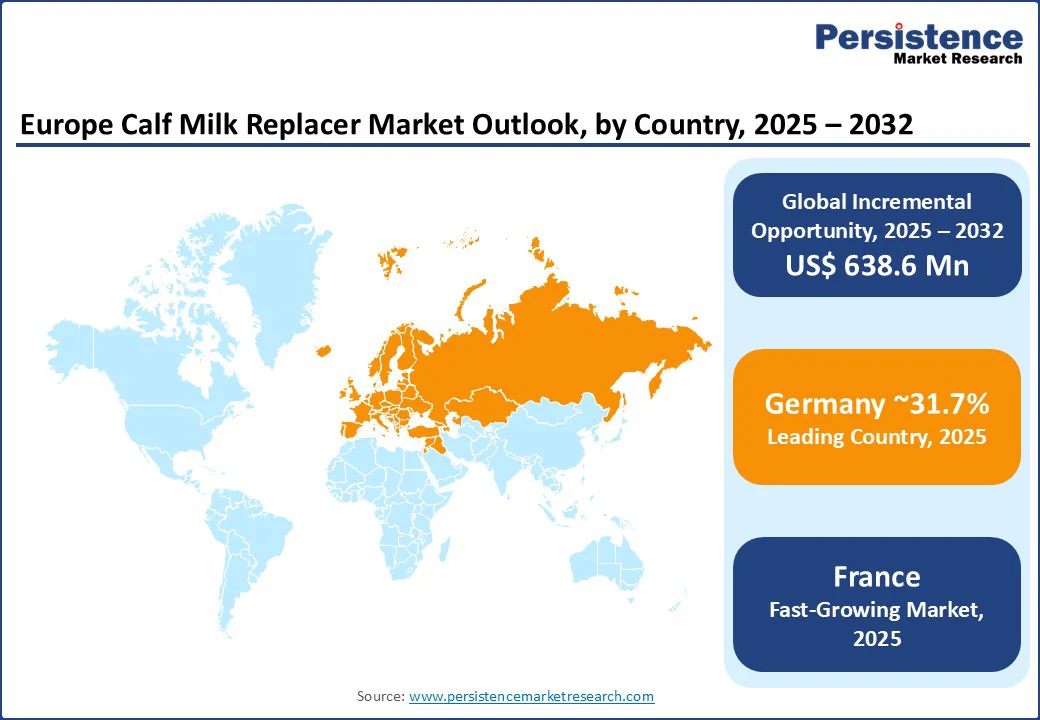

- Leading Country: Germany accounts for nearly a 31.7% share in 2025, owing to increasing dairy herd population, unique farming infrastructure, and active research investments.

- Fastest-growing Country: France is projected to hold approximately 25.8% share in 2025, driven by the expansion of organic dairy production and government support for sustainable farming practices.

- New Product: Trouw Nutrition recently introduced next-generation calf milks, namely, Milkivit ONE and Sprayfo Ultimo. These emphasize fatty-acid profiles that closely mimic cow milk and signal early gut/rumen development.

| Key Insights | Details |

|---|---|

|

Europe Calf Milk Replacer Market Size (2025E) |

US$ 1,018.6 Mn |

|

Market Value Forecast (2032F) |

US$ 1,657.2 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.6% |

Market Factors - Growth, Barriers and Opportunity Analysis

Expansion of Commercial Dairy Operations

Europe’s expanding dairy industry, which contributes over 30% of global milk output, accelerates the adoption of calf milk replacers aimed at boosting efficiency and improving herd health. Increasing herd sizes, ongoing shift toward intensive farming practices, and rising milk yield targets have made early calf nutrition a strategic investment for dairy businesses.

According to the European Parliamentary Research Service and Eurostat, dairy farms in Europe continue to consolidate operations for expansion and automation, thereby augmenting demand for precision nutritional solutions. Calf milk replacers also support consistent growth cycles and minimize mortality rates, directly improving farm profitability and operational resilience.

Developments in Formulation Technology

Breakthroughs in milk replacer formulations, such as the integration of probiotics, prebiotics, and essential amino acids, have transformed nutritional profiles, making powder-based replacers the industry standard. Leading manufacturers launched new powdered products, including Trouw Nutrition’s immunoglobulin-enriched solution, to meet the surging demand for high digestibility and immune support.

Research from industry associations and academic institutions confirms that improved formulations ensure optimal calf growth, digestive health, and disease resistance throughout weaning periods. Technological development improves product efficacy, widens adoption across farm profiles, and encourages regulatory acceptance of science-driven nutrition.

Progressive Regulatory Push Towards Animal Welfare

Strict European Union (EU) animal welfare directives, such as regulations mandating antibiotic stewardship and the promotion of non-GMO feed, fuel a widespread transition to non-medicated products. Regulatory agencies such as the European Food Safety Authority have established rigorous standards for calf nutrition and milk replacer composition.

They have successfully increased transparency and accelerated cross-border trade. Regulatory safeguards stimulate new product development while ensuring compliance and consumer trust, reducing risks of disease outbreaks and supporting sustainable farming.

Restraints - Persistent Cost and Price Sensitivity

Adoption of premium formulations is often challenged by cost barriers, especially in markets with low-margin dairy operations. Price pressures arise from raw material volatility, supply chain disruptions, and competitive discounting, affecting smallholders and independent farmers most severely. The market’s expansion is expected to be curtailed unless developments reduce production and sourcing costs or subsidies support broad adoption.

Regulatory and Supply Chain Complexity

High regulatory compliance costs for feed safety and documentation, as well as cross-border movement restrictions, complicate distribution channels and slow market penetration in a few regions. Supply chain interruptions, primarily related to disease outbreaks or import/export disruptions, pose systemic risks to consistent product availability and farm uptake. These factors increase the market’s vulnerability to unexpected shocks and require resilient logistics and risk management.

Opportunities - Rising Demand in Central and Eastern Europe

Emerging dairy markets across Central and Eastern Europe are increasingly investing in calf nutrition to bolster productivity and competitiveness. Modernization programs, EU-funded farm upgrades, and government-backed education campaigns also expand market size with an estimated opportunity of over US$200 Mn in new demand by 2032. Manufacturers are likely to capture this share by localizing production and engaging in partnerships with domestic farms.

The rising emphasis on sustainable farming practices is further creating fresh avenues for calf milk replacer manufacturers. Several domestic dairy cooperatives are encouraging low-carbon feed alternatives and animal welfare-focused nutrition strategies, prompting high adoption of specialized formulations. This shift not only complies with EU Green Deal objectives but also opens premium segments where producers can differentiate through quality assurance certifications.

Expansion of Retail and Specialty Distribution Channels

While direct sales/B2B channels dominate, specialty retail and online platforms are becoming important, delivering non-medicated and premium powder-based formulations to small-scale and hobbyist farms. Digitalization and logistics expansion are predicted to help build reach, transparency, and loyalty among new customer segments.

Collaborations with veterinary clinics, agri-cooperatives, and farm advisory services are poised to strengthen the retail and specialty channel ecosystem. These networks not only act as trusted points of purchase but also provide technical guidance. This makes it convenient for small farmers to adopt premium calf nutrition solutions. As consumer confidence in traceability and expert-backed recommendations rises, manufacturers that invest in such integrated distribution strategies are expected to gain a competitive advantage in Europe’s evolving market.

Development of Sustainable, Organic, and Non-GMO Products

Consumer preference and regulatory pressure for sustainable, organic, and non-GMO replacers present a premium European calf milk replacer market opportunity. Volac’s launch of sustainable non-GMO replacers and similar initiatives is estimated to represent 10 to 14% of new product revenues through 2032. Investing in green certifications and sustainable sourcing will likely unlock long-term competitive advantage and margin expansion.

Partnerships with organic dairy producers and certification bodies are anticipated to accelerate adoption across niche but fast-growing segments. As retailers and cooperatives increasingly prioritize eco-labeled products in their procurement policies, calf milk replacer brands that can demonstrate transparent sourcing, reduced carbon footprints, and compliance with strict EU sustainability standards will be well-positioned. This not only refines brand equity but also enables manufacturers to tap into export opportunities where organic and non-GMO credentials are a key differentiator.

Category-wise Analysis

Product Type Insights

Non-medicated products are anticipated to account for nearly 63.1% of the European calf milk replacer market share in 2025, reflecting consumer preference for formulations free of antibiotics and medicinals. Veterinary stewardship and evolving consumer demand for ‘clean label’ livestock products underpin the dominance of non-medicated replacers. Growth is further attributed to regulatory restrictions and farm modernization. Technological developments in immune-boosting ingredients further support segment expansion.

Medicated calf milk replacers are witnessing steady growth due to the rising focus on disease prevention and early-life health management among dairy farmers. Calves are highly vulnerable to digestive and respiratory infections. Hence, the inclusion of additives such as probiotics, coccidiostats, and vitamins in medicated replacers helps improve survival rates and herd productivity.

Form Insights

Powder-based replacers command approximately 71.4% of the market share in 2025, attributed to their cost-efficient storage, transportation, and customizable nutritional profiles. High demand for digestible, shelf-stable solutions across B2B and retail segments propels volume.

Liquid calf milk replacers are gaining impetus as farmers seek convenience and consistency in calf nutrition. These eliminate the requirement for mixing and measuring, ensuring uniform quality and reducing preparation time on farms.

Distribution Channel Insights

Direct sales/B2B channels represent about 66.3% of Europe calf milk replacer market share in 2025. This dominance is supported by contractual relationships with commercial dairy farms and processors. Integration in farm management systems and specialized nutrition consulting also strengthens channel primacy.

Retail/B2C channels (physical and online) are projected to expand at approximately 8.2% CAGR through 2032, as small-scale and independent farmers seek easy access to customized nutrition solutions through specialty platforms. In addition, the premiumization of calf nutrition through organic, non-GMO, and medicated formulations is spurring consumer interest in branded products that emphasize sustainability.

Country Insights

Germany Calf Milk Replacer Market Trends

Germany leads European calf milk replacer market, with an estimated share of 31.7% in 2025. The country boasts the highest per-farm productivity and value-added output, embracing novel herd management systems and cooperative distribution networks. Superior technological development, strategic merger and acquisition activity, and increased investment in research boost adoption.

The regulatory environment is highly compliant with EU feed directives, promoting non-medicated and sustainable product lines. The market is consolidated among leading firms such as Nutreco, De Heus, and Trouw Nutrition with deep partnerships spanning farm management, distribution, and technology. Private sequencing investments in research and development and manufacturing capacity have yielded 10+ key product launches since 2023, capitalizing on Germany’s unique ecosystem and skilled labor.

France Calf Milk Replacer Market Trends

In 2025, France is estimated to account for approximately 25.8% of share. Performance is characterized by sector harmonization, which is integrated with cross-border producers and buyers, pushing stable demand for non-medicated and powder-based formulations. Regulatory compliance with EU safety standards, widespread adoption of modern calf-rearing practices, and government-backed nutrition campaigns stimulate consumption and development.

France leads in terms of the adoption of sustainable and specialty products, propelled by manufacturer collaborations and academic partnerships to accelerate nutritional efficacy and traceability. Industry trends include multi-site expansions and targeted investments in green certifications, as well as organic product lines since 2024.

Netherlands Calf Milk Replacer Market Trends

The Netherlands serves as a growth and manufacturing hub, with an estimated market size of US$180 Mn in 2025. This growth is fueled by logistics efficiency and cutting-edge production technology in liquid and powder forms. Access to novel distribution channels and cost leadership strategies enable rapid expansion and competitive price points, benefiting regional and global exports.

The Netherlands is home to global innovators, including Nukamel and FrieslandCampina, leading contract manufacturers, and technology-backed distribution networks. Active investment in automation, precision nutrition, and process expansion since 2023 has further increased market yields by 9% annually, opening new export pathways.

Competitive Landscape

The Europe calf milk replacer market is classified as moderately consolidated, with the top five players controlling approximately 47% of the total share in 2025. Key players such as Alltech, Nutreco, De Heus, Trouw Nutrition, and Cargill dominate through product development, superior B2B relationships, and diversified portfolios. The presence of small-scale regional and specialty manufacturers creates a competitive environment, supporting differentiation and localized product lines.

Business Strategies

Dominant strategic elements revolve around sustained development, value-added product launch, vertical integration, and geographic expansion. Market leaders utilize data-driven nutrition, differentiate through proprietary formulas, and adopt direct and specialty distribution models.

Key Industry Developments

- In October 2024, Volac introduced skim-milk–rich calf replacer (50% skim). Its new high-skim formulation is aimed at farmers wanting dairy-protein-heavy replacers. It followed the company’s repositioning and product upgrade under the changed ownership landscape.

- In January 2024, Denkavit completed the acquisition of Volac’s milk-replacer business. Denkavit bought Volac’s milk-replacer operations to strengthen its U.K. and Italy position as well as create a focused calf-replacer business. This deal influenced product ownership and commercial footprints in Europe through 2024 and 2025.

Companies Covered in Europe Calf Milk Replacer Market

- Nutreco

- Trouw Nutrition

- De Heus

- Cargill

- Volac

- Alltech

- Nukamel

- FrieslandCampina

- Lactalis

- ADM Animal Nutrition

- Land O'Lakes

- Schils BV

- SCA Nutrition

- Provimi

- Bonanza Calf Nutrition

- Others

Frequently Asked Questions

Europe calf milk replacer market is projected to reach US$ 1,018.6 Mn in 2025.

Rising dairy farm productivity and increased regulatory pressure for animal welfare are the key market drivers.

The Europe calf milk replacer market is poised to witness a CAGR of 7.2% from 2025 to 2032.

Product range extensions for small-scale farms and development in sustainable sourcing are the key market opportunities.

Nutreco, Trouw Nutrition, and De Heus are a few key market players.