- Renewable Energy

- Europe Biomass Pellets Market

Europe Biomass Pellets Market Size, Share, and Growth Forecast, 2025 - 2032

Europe Biomass Pellets Market by Product Type (Wood Pellets, Black Pellets, Forestry Pellets, Agricultural Pellets and Biomass Briquettes), by Source type (Agricultural Residue, Wood Sawdust, Wood Chips and Others), End-User (Residential, Industrial and Commercial), and Regional Analysis for 2025 - 2032

Europe Biomass Pellets Market Size and Trends Analysis

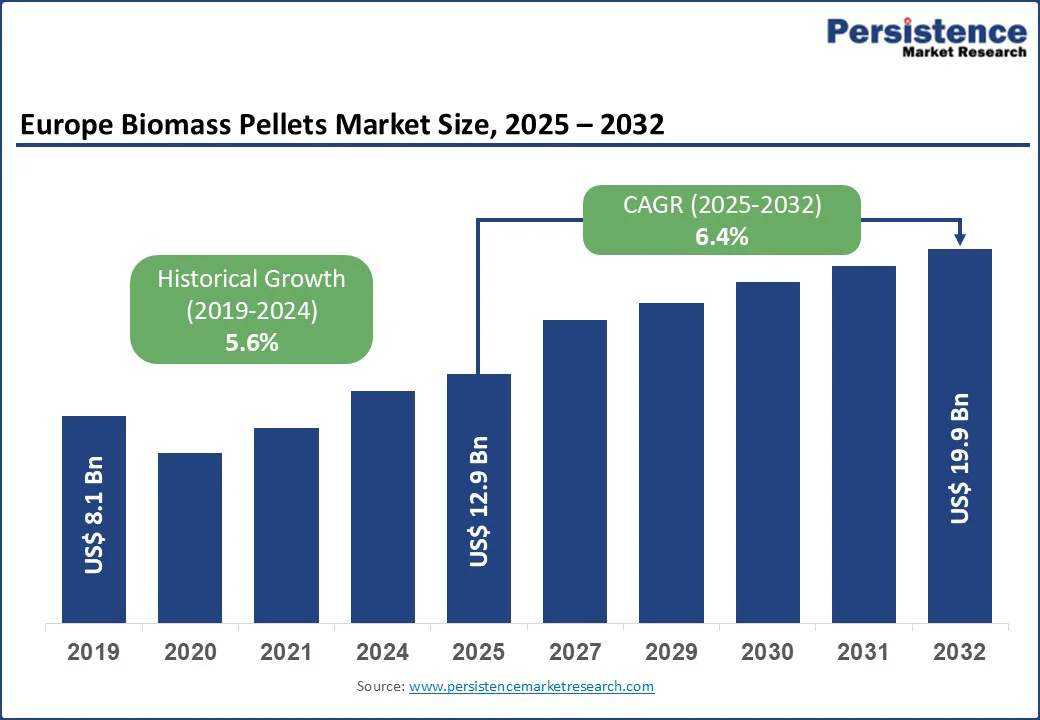

Europe biomass pellets market size is likely to value at US$ 12.9 Bn in 2025 and is expected to reach US$ 19.9 Bn by 2032 growing at a CAGR of 6.4% during the forecast period from 2025 to 2032.

Key Industry Highlights:

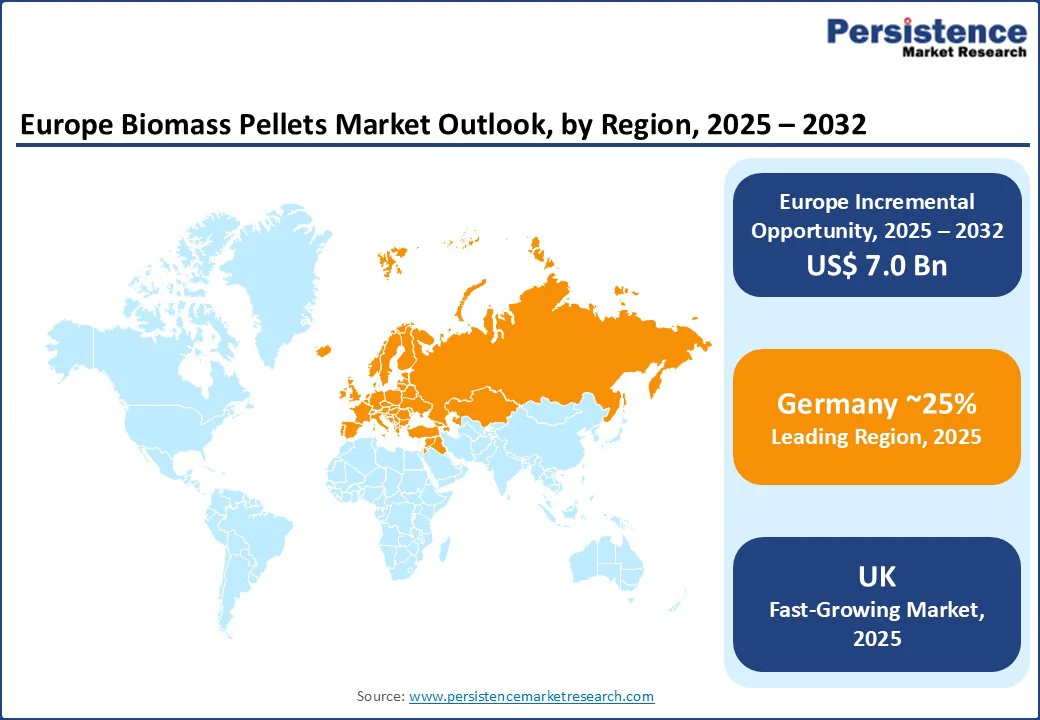

- Leading Country: Germany, accounting for over 25% market revenue share in 2025, driven by its strong renewable energy policies, advanced industrial base, and commitment to decarbonization. The country has invested heavily in biomass-based heating systems and industrial applications, supported by subsidies under its Renewable Energy Sources Act (EEG).

- Fastest-growing Country: UK, projected CAGR of 6.5% from 2025 to 2032. The UK plays a pivotal role in shaping the Europe Biomass Pellets Market, primarily due to its large-scale consumption for power generation and its strong policy framework supporting renewable energy.

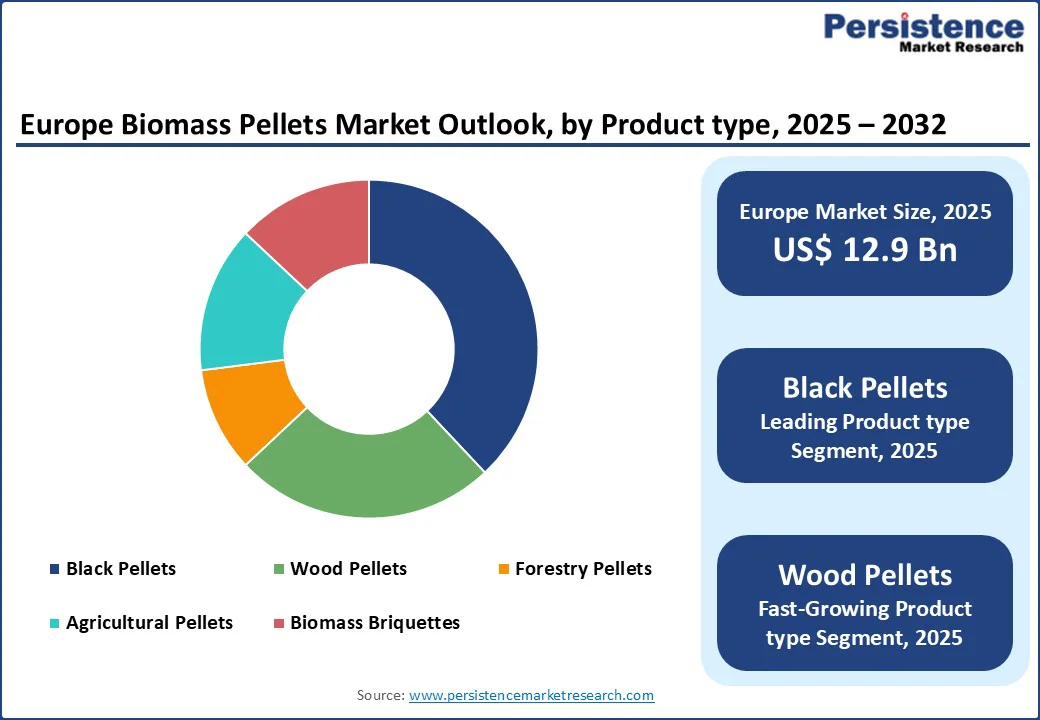

- Dominant Product Type: Black Pellets Gain Traction with Superior Energy Efficiency and Reduced Moisture Content and led the market with the largest revenue share of 36.3% in 2025.

- Source Insights: The main raw material for biomass pellet production is wood sawdust, sourced quite conveniently from areas close to sawmills, furniture factories, and wood-processing industries. Some of the most prolific producers of wood sawdust pellets are those countries that enjoy a well-developed forest sector.

- Import-Export Scenario: Europe is the largest consumer and importer of biomass pellets, with countries like the UK, Italy, Denmark, and the Netherlands heavily relying on imports, mainly from the U.S., Canada, and Russia. Meanwhile, nations like Latvia and Estonia are key exporters, driven by surplus production and strong EU renewable energy policies.

| Global Market Attribute | Key Insights |

|---|---|

| Biomass Pellets Market Size (2025E) | US$ 12.9 Bn |

| Market Value Forecast (2032F) | US$ 19.9 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.6% |

The emphasis on clean, efficient, and local energy alternatives has led to an entire overhaul of the market structure, while developments in pellet production, storage, and combustion efficiency further assisted these changes. The enhancement of supply chains, cross-border trade in pellets, and increasing use of agricultural residues for pellet manufacturing is supportive for the market growth.

Market Dynamics

Driver - Growing Demand for Renewable and Local Energy Sources Drives Adoption

Energy security concerns and the push for stable, local energy supplies stimulate the adoption of biomass pellets across Europe. The market capitalizes on the use of agricultural and forestry residues, aligning with circular economy principles and resource efficiency.

Biomass pellets offer a reliable, cost-effective solution for residential heating, industrial power production, and combined heat and power plants. The preference for clean, efficient, and locally sourced energy has attracted significant investment in pellet production and logistics. It continues to gain traction as consumers and industries seek alternatives to imported fossil fuels.

For instance, in July 2022, Enviva Inc. began construction of its Epes plant in Alabama, designed with a nameplate capacity of 1.1 million metric tons per year, the company’s largest wood pellet production facility, with full production expected by 2025.

Restraint - Regulatory Pressures and Supply Chain Instability Undermine Market Growth

Europe Biomass Pellets Market faces a major restraint stemming from a combination of regulatory complexity, sustainability compliance, and supply chain instability. Strict EU directives require detailed certification of feedstock sources, raising costs and posing barriers for smaller producers, while regulatory uncertainty hampers long-term investments.

At the same time, the market is vulnerable to supply chain disruptions caused by geopolitical tensions, trade restrictions, transportation cost fluctuations, and labor shortages. These issues drive price volatility, making it difficult for producers and consumers to plan effectively.

Additionally, public scrutiny regarding land use and biomass carbon neutrality further complicates approvals and market acceptance. Together, these factors create an environment of high operational risk and unpredictability, compelling stakeholders to adopt stronger compliance frameworks and diversify supply chains to ensure resilience and stability.

Opportunity - Industrial Decarbonization and Innovation Drive Biomass Pellet Opportunities

Europe Biomass Pellets Market possesses significant growth potential by combining its role in industrial decarbonization with opportunities from feedstock innovation and cross-border trade. Large-scale industries such as cement, steel, and chemicals are under pressure to cut emissions, creating demand for biomass pellets as a sustainable substitute for coal and natural gas. Simultaneously, expanding district heating networks across urban areas further boosts pellet consumption.

On the supply side, diversifying feedstock sources including agricultural residues, energy crops, and waste streams enhances sustainability while reducing reliance on limited resources. Technological advancements in pellet production improve efficiency and product quality, making them more competitive. Strengthened intra-European trade agreements and rising export opportunities for certified sustainable pellets position the market to play a central role in Europe’s renewable energy transition.

Category-wise Analysis

Product type Insights - Black Pellets Gain Traction with Superior Energy Efficiency and Reduced Moisture Content

In view of their higher energy density, lower water absorption, and reduced storage and transport costs, these advanced biomass fuels, known as black pellets are gaining acceptance. Major differences with traditional wood pellets are that black pellets can be co-fired with coal in power stations, producing far less carbon emissions on existing coal largely infrastructure.

With European nations closing down coal-based power stations, black pellets shine on the path to carbon-neutral energy transition. Scandinavian countries, Germany, and the Netherlands are the forerunners in the black pellet market, especially in industrial and utility-scale applications.

Source Insights - Wood Sawdust Remains the Leading Source Due to High Availability and Consistency

Back in Europe, the main raw material for biomass pellet production is wood sawdust, sourced quite conveniently from areas close to sawmills, furniture factories, and wood-processing industries. Some of the most prolific producers of wood sawdust pellets are those countries that enjoy a well-developed forest sector.

These include Sweden, Finland, and Austria, all supplying the domestic and the export markets. Residential heating applications, along with high-efficiency biomass boilers, increasingly demand sawdust-based pellets of high purity and low moisture. Regulations favoring sustainable forest management practices also provide a stable supply of certified wood sawdust to produce pellets.

For instance, Graanul Invest, a leading European producer, is expected to produce 2.2 million tons of wood pellets in 2024, reflecting its advanced manufacturing capacity and strong market presence.

Regional Insights and Trends

Germany Leads in the Biomass Pellets Market

Germany holds a leading position in the Europe Biomass Pellets Market, driven by its strong renewable energy policies, advanced industrial base, and commitment to decarbonization. The country has invested heavily in biomass-based heating systems and industrial applications, supported by subsidies under its Renewable Energy Sources Act (EEG).

Growing demand from district heating networks and residential heating fuels market expansion. Key manufacturers such as German Pellets GmbH, ENplus-certified producers, and regional cooperatives are enhancing production capacities and adopting advanced pelletizing technologies for higher efficiency and sustainability.

Recent developments include innovations in feedstock diversification, integrating agricultural residues, and improving supply chain logistics to reduce costs. Additionally, Germany’s focus on meeting EU sustainability certification standards ensures global competitiveness, strengthening its role as both a major consumer and exporter within the European biomass pellet industry.

U.K. is a Key Market for in Europe’s Biomass Pellets

The U.K. plays a pivotal role in shaping the Europe Biomass Pellets Market, primarily due to its large-scale consumption for power generation and its strong policy framework supporting renewable energy. The country has transitioned from coal to biomass in major power plants, significantly boosting pellet imports.

The Renewable Heat Incentive (RHI) and ambitious net-zero carbon targets further strengthen biomass adoption in both industrial and residential heating applications. The UK is one of Europe’s largest importers of biomass pellets, sourcing primarily from North America and Europe, ensuring energy security and diversification.

Key manufacturers such as Drax Group have been at the forefront, investing in expanding pellet production capacity and developing carbon capture and storage (CCS) projects to enhance sustainability. Recent developments include Drax’s expansion of pellet plants in North America and partnerships to deliver negative emissions, consolidating the UK’s leadership in biomass energy transition.

Competitive Landscape

Europe biomass pellets market is much competitive and induces renewable energy initiatives, government incentives, and further demand for sustainable heating solutions. Due to their low carbon footprint and cost-effectiveness, biomass pellets are widely used in electricity production, residential heating, industrial applications, and combined heat and power (CHP) plants.

The current market condition is affected by the technological advancement in pellet production along with supply chain optimization. These would also lead to the less reliance on fossil fuels. Focus is given by key players to scale up production, secure raw material supply, and improve pellet quality for the more stringent EU sustainability criteria.

Key Industry Developments:

- In December 2024, Enviva announced its successful emergence from Chapter 11 bankruptcy protection, completing a major financial restructuring.

- In September 2024, Drax Group PLC and Karbon-X Corp launched a new partnership to facilitate transactions in carbon offsets, accelerating large-scale carbon removal and sustainable energy generation.

- In February 2023, Enviva announced a new partnership with the Girl Scouts of Greater Mississippi to support forest restoration and reforestation, including financial support for long-term forest management and tree planting initiatives.

Companies Covered in Europe Biomass Pellets Market

- Vyborgskaya Cellulose LLC

- Energex Wood Pellets

- Stora Enso Oyj

- Canfor Corporation

- PIVETEAUBOIS

- An Viet Phat Energy Co. Ltd.

- German Pellets GmbH

- ErndtebrückerEisenwerk GmbH & Co. KG

- HolzindustrieSchweighofer

- Biomass Secure Power Inc.

- Other Market Players

Frequently Asked Questions

Europe Biomass Pellets market is estimated to be valued at US$ 12.9 Bn in 2025.

The key demand driver for the Biomass Pellets Market is the global push for renewable energy and carbon emissions reduction, largely supported by government policies and incentives.

In 2025, Germany is expected to dominate with an exceeding 25% revenue share in the Europe Biomass Pellets market.

Among the product type, black pellets account for the highest preference, capturing beyond 36.3% revenue share in 2025, surpassing others.

The key players in Europe Biomass Pellets market are Vyborgskaya Cellulose LLC, Energex Wood Pellets, Stora Enso Oyj, Canfor Corporation and PIVETEAUBOIS.