- Retail

- Europe Amusement Parks Market

Europe Amusement Parks Market Size, Share, and Growth Forecast, 2026 – 2033

Europe Amusement Parks Market by Rides Type (Mechanical Rides, Water Rides), Age (Up to 18 Years, 19 to 35 Years, 36 to 50 Years, 51 to 65 Years, More Than 65 Years), Revenue Source (Tickets, Food and Beverage, Merchandise, Hotels and Resorts) for 2026 – 2033

Europe Amusement Parks Market Size and Trends Analysis

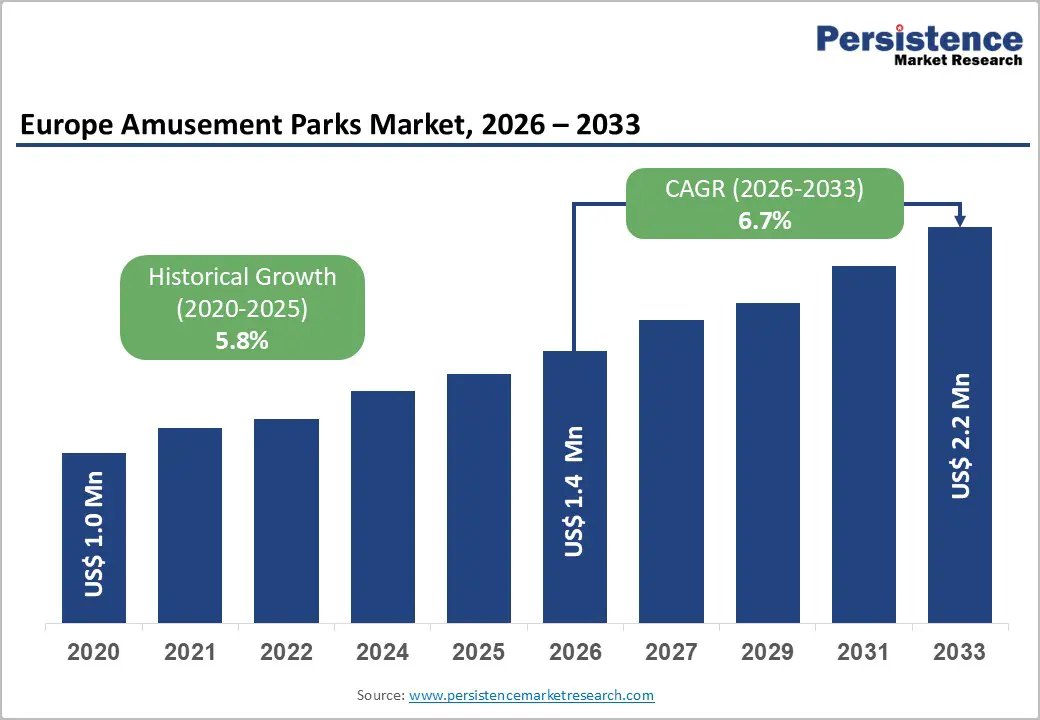

The Europe amusement parks market size is likely to be valued at US$1.4 billion in 2026 and is expected to reach US$2.2 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033, driven by resilient intra-European tourism, rising international arrivals, and sustained consumer demand for experience-based leisure. Major destination parks across France, Germany, Spain, and Italy continue to benefit from improved connectivity, government-backed tourism initiatives, and increasing household expenditure on recreation.

The market is strengthened by continuous capital investment in large-scale expansions, new themed lands, and ride upgrades aimed at driving repeat visitation and extending length of stay. Technological advancement and immersive storytelling remain central to market expansion. Parks are increasingly adopting IP-driven attractions, digital ticketing, mobile apps, and AI-enabled crowd and queue management systems to improve guest flow and enhance satisfaction. The shift toward integrated resort models, combining theme parks with hotels, water parks, and entertainment districts, has diversified revenue streams and reduced seasonality risks.

Key Industry Highlights:

- Leading Rides Type: Mechanical rides are anticipated to be the leading ride type, accounting for a revenue share of 48% in 2026, driven by their strong appeal as flagship attractions, continuous innovation in coaster design, and sustained demand from thrill-seeking visitors across major European amusement parks.

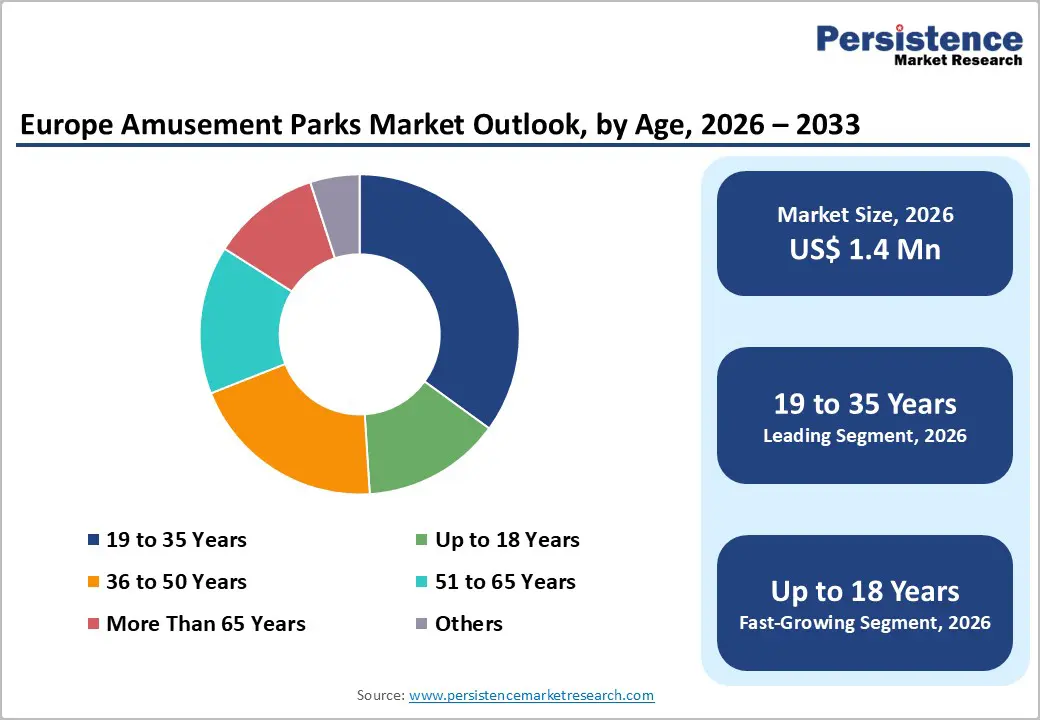

- Age Type: The 19 to 35 year group is projected to represent the leading age type in 2026, accounting for a revenue share of 42%, driven by strong spending on immersive, IP-based, and experience-centric attractions.

- Leading Revenue Source: Tickets are projected to represent the leading revenue source in 2026, accounting for 54% of the revenue share, supported by dynamic pricing strategies and high visitor footfall across major parks.

| Global Market Attributes | Key Insights |

|---|---|

| Europe Amusement Parks Market Size (2026E) | US$1.4 Bn |

| Market Value Forecast (2033F) | US$2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Integration of Intellectual Property and Immersive Storytelling

Renowned European parks increasingly leverage recognized IPs from movies, animation, and literature to create emotionally engaging environments that go beyond traditional rides. Attractions built around familiar characters and narratives enhance brand recall, encourage repeat visits, and justify premium pricing. Story-driven mechanical rides, themed zones, and live performances allow visitors to feel part of a larger narrative, aligning with Europe’s strong cultural appreciation for storytelling and heritage. This approach also increases dwell time within parks, increasing secondary spending on food, merchandise, and exclusive experiences. Competition intensifies across mature European markets, IP-led attractions help parks differentiate themselves and maintain relevance among digitally savvy audiences who seek immersive, shareable experiences rather than standalone thrills.

Immersive storytelling strengthens this driver by blending advanced technologies such as augmented reality, projection mapping, and interactive queue systems with physical attractions. European amusement parks are investing heavily in cohesive world-building, where architecture, sound design, and staff interactions reinforce the storyline across the visitor journey. This holistic experience appeals strongly to younger demographics and families, supporting cross-generational engagement. Localized adaptations of IPs help parks resonate with diverse European audiences while maintaining international appeal. The integration of IP also supports long-term revenue stability, as successful franchises enable periodic updates, seasonal events, and spin-off attractions without requiring entirely new concepts.

Seasonality and Weather Dependency Challenges

A large share of European amusement parks operates primarily during spring and summer, aligning with favorable weather and school holidays. Unpredictable conditions such as prolonged rainfall, heatwaves, or unseasonably cold temperatures can sharply reduce footfall, especially for parks with a high concentration of outdoor mechanical rides. Northern and Western European regions are particularly exposed to shorter peak seasons, limiting operating days and constraining annual revenue potential. This seasonality also creates uneven cash flows, making it challenging for operators to recover high capital investments in rides, safety systems, and themed infrastructure. Reliance on peak-season attendance increases sensitivity to tourism fluctuations, labor shortages, and transportation disruptions, amplifying financial risks for park operators.

Weather dependency complicates long-term planning and operational efficiency across the European amusement parks market. Parks must maintain full staffing, maintenance, and energy readiness despite variable daily attendance, leading to higher fixed costs relative to revenue during off-peak periods. Climate volatility driven by changing weather patterns adds uncertainty, with extreme events increasingly disrupting planned operations and visitor comfort. While investments in indoor attractions, covered queues, and weather-resistant rides are growing, such solutions require substantial upfront capital and long payback periods. Smaller and regional parks face greater difficulty adopting these mitigation strategies, widening the performance gap with large destination parks. Seasonality and weather exposure continue to restrain consistent growth, influencing pricing strategies, capacity utilization, and overall profitability across the European amusement parks industry.

Water Rides and Year-Round Facilities

The expansion of water rides and year-round facilities presents a strong growth opportunity for the Europe amusement parks market, helping operators overcome traditional seasonality constraints. Increasing investment in indoor and climate-controlled water attractions allows parks to extend operating calendars beyond peak summer months. Heated pools, enclosed slides, and hybrid water-ride concepts appeal to visitors during colder seasons, particularly in Northern and Central Europe. These attractions also align well with rising consumer interest in wellness-oriented leisure, as water-based experiences are associated with relaxation, family bonding, and health benefits. By integrating water rides within existing theme parks or as standalone indoor water parks, operators can attract diverse age groups and boost overall visitor volumes. This approach supports stable year-round footfall, improves asset utilization, and enhances revenue predictability across fluctuating tourism cycles.

Year-round facilities strengthen this opportunity by transforming amusement parks into multi-day, all-season destinations. European operators are increasingly combining water rides with hotels, resorts, and indoor entertainment zones to encourage longer stays and higher per-capita spending. Covered attractions, retractable roofs, and energy-efficient climate systems enable consistent operations regardless of weather conditions. These developments also support off-season events, school trips, and corporate bookings, reducing reliance on holiday-driven demand. Access to EU tourism and sustainability funding encourages investments in eco-friendly water systems and energy-efficient infrastructure. Consumer expectations shift toward immersive, flexible leisure experiences, and water rides and year-round facilities are positioned to play a critical role in driving long-term growth and resilience within the European amusement parks market.

Category-wise Analysis

Rides Type Insights

Mechanical rides are expected to lead the Europe amusement parks market, accounting for approximately 48% of revenue in 2026, driven by their role as flagship attractions that define park identity, continuous advancements in ride engineering and safety, and sustained demand for high-thrill, repeatable experiences among domestic and international visitors. Signature roller coasters, drop towers, and high-adrenaline attractions serve as flagship offerings that shape brand perception and visitor recall. European consumers, particularly repeat visitors and tourists, associate park value with iconic mechanical rides that deliver consistent excitement and technological sophistication. Continuous innovation in ride engineering, safety systems, and immersive theming has reinforced their dominance across both destination parks and regional attractions. For example, Europa-Park, where mechanically advanced roller coasters integrated with storytelling remain central to visitor demand and brand positioning.

Water rides are likely to represent the fastest-growing segment in 2026, supported by increasing investment in climate-controlled and hybrid water attractions. Parks are expanding indoor water rides and enclosed aquatic zones to overcome weather dependency and extend operating seasons, particularly in Northern and Central Europe. Water-based attractions appeal to a broader demographic range, combining thrill, relaxation, and wellness-oriented experiences within a single offering. The integration of spa-inspired environments, family pools, and interactive water play areas allows operators to diversify visitor profiles and increase dwell time. For example, PortAventura World has expanded water-focused zones to complement its traditional ride portfolio and attract visitors beyond peak summer months. These attractions also support higher per-visitor engagement by encouraging longer stays and bundled access across park facilities.

Age Type Insights

19 to 35 years is projected to lead the market, capturing around 42% of the revenue share in 2026, supported by strong preference for immersive, IP-themed attractions, higher discretionary spending on experiential leisure, and active engagement with social-media-driven entertainment offerings. European amusement parks increasingly design ride narratives, festivals, and seasonal events to resonate with millennial and young adult preferences, particularly those aligned with popular culture and digital engagement. This group also demonstrates higher discretionary spending on premium access, exclusive events, and themed food and beverage experiences. Their active social media presence boosts park visibility, indirectly enhancing marketing reach and brand equity. For instance, Disneyland Paris leverages IP-based attractions and event-focused experiences to draw young adult visitors looking for shareable, story-driven moments, whose spending habits drive robust ticket sales and ancillary revenue, reinforcing the park’s leading position in the Europe market.

The up-to-18 age group is expected to be the fastest-growing segment in 2026, driven by increasing parental emphasis on educational entertainment and family-focused leisure. Theme parks are creating child-centric zones that blend fun, learning, safety, and interactivity to meet evolving family expectations. Educational rides, role-play attractions, and guided group experiences attract schools and organized educational visits across Europe, while bundled family pricing and multi-attraction passes enhance affordability and perceived value. For example, Efteling focuses on storytelling, fantasy, and age-appropriate attractions that engage children and accompanying adults alike. The rising focus on curriculum-aligned recreational visits and structured learning experiences further boosts demand within this age group.

Revenue Source Insights

Tickets are expected to remain the leading revenue segment in the European amusement parks market, accounting for around 54% of revenue in 2026, due to their central role in visitor access and capacity management. European park operators are increasingly leveraging dynamic pricing, seasonal passes, and tiered entry options to optimize attendance and revenue per visitor. Online ticketing, advance bookings, and demand-based pricing have bolstered ticket revenue resilience even amid fluctuating tourism trends. Tickets also serve as the primary driver of secondary spending, boosting footfall across food, merchandise, and entertainment zones, for example, Parc Astérix, where diversified ticket structures support high seasonal attendance while maintaining operational efficiency. The dominance of ticket revenue underscores its essential role in sustaining park operations, funding ride investments, and supporting long-term infrastructure development.

Hotels and resorts are projected to be the fastest-growing segment in 2026, fueled by a shift toward destination-style, multi-day experiences. Integrated accommodations encourage longer stays, higher per-visitor spending, and greater engagement with park offerings. Themed hotels enhance immersion by extending storytelling beyond the park gates, strengthening emotional connections with visitors, reducing reliance on day visitors, and stabilizing revenue during off-peak periods. For instance, Gardaland Resort’s on-site hotels complement park attractions and promote extended family vacations. The expansion of park-linked hospitality reflects changing consumer preferences for convenience, bundled experiences, and immersive leisure travel. Supported by tourism development initiatives, hotels and resorts are emerging as a key growth pillar, enabling European amusement parks to enhance profitability, diversify revenue streams, and build year-round destination appeal.

Competitive Landscape

The Europe amusement parks market exhibits a moderately fragmented structure, driven by a mix of large multinational operators and strong regional players that balance international destination experiences with local cultural appeal. Competitive intensity remains substantial as established giants such as Merlin Entertainments and Disney leverage extensive portfolios and intellectual property to attract diverse visitor segments, while midsized firms focus on niche and regional strengths to maintain differentiation. The top five groups together control a significant portion of overall industry revenue, yet there is still space for emerging parks and boutique operators to carve out specialized positions, particularly with innovative theming and experiential offerings.

With key leaders including Merlin Entertainments, The Walt Disney Company’s Disneyland Paris, Parques Reunidos, and Compagnie des Alpes, the competitive landscape reflects a blend of reach and localized brand resonance. These players compete through diversified attraction portfolios, aggressive IP-driven theming, and resort-style expansions that enhance multi-day stays and drive ancillary revenue streams. Smaller operators and niche parks often emphasize unique cultural narratives, regional folklore, or targeted family experiences to differentiate from larger brands, while partnerships and strategic acquisitions intensify market positioning. Technology from virtual and augmented reality enhancements to AI-powered guest management systems has become another key battleground, enabling differentiated visitor experiences and operational efficiencies.

Key Industry Developments:

- In January 2026, Europa-Park announced the launch of Snorri 4D, a new family-oriented cinematic attraction set to debut at the start of the 2026 season. The experience will premiere at the park’s Magic Cinema 4D, marking the first time the popular Rulantica water park storyline is brought to the big screen. Developed by MACK Magic, the entertainment division of the Mack family, the project aims to extend the Rulantica intellectual property beyond water-based attractions and strengthen cross-park storytelling. Directed by Oscar-nominated filmmaker Thierry Marchand with an original score by Hendrik Schwarzer, Snorri 4D is produced entirely in-house by MACK Animation in Germany.

- In November 2025, Disneyland Paris announced that World of Frozen is scheduled to open on March 29, 2026, as part of the transformation of Walt Disney Studios Park into Disney Adventure World. This development represents one of the most significant expansions in the resort’s history and will substantially enhance the scale and immersive quality of its second park, reinforcing Disneyland Paris’s position as Europe’s leading tourist destination. The upcoming World of Frozen will fully immerse guests in the Kingdom of Arendelle, recreated at life-size scale and featuring a new family-friendly attraction, live daytime entertainment, character encounters with Anna and Elsa, themed dining, and retail experiences.

Companies Covered in Europe Amusement Parks Market

- Disneyland Park

- Europapark

- Efteling

- Tivoli Gardens

- PortAventura

- Gardaland

- Futuroscope

- Parc Asterix

- Grona Lund

- Walibi

Frequently Asked Questions

The Europe amusement parks market is projected to reach US$1.4 billion in 2026.

The Europe amusement parks market is driven by rising tourism, increasing demand for immersive IP-based experiences, and continuous investment in technologically advanced rides and year-round attractions.

The Europe amusement parks market is expected to grow at a CAGR of 6.7% from 2026 to 2033.

Key market opportunities in the Europe amusement parks market include the expansion of indoor and water-based attractions to enable year-round operations, the development of IP-driven immersive lands, and the growth of integrated resorts and themed accommodations to increase visitor stay duration and spending.

Disneyland Park, Europapark, Efteling, Tivoli Gardens, PortAventura, Gardaland, and Futuroscope are the leading players.