- Pharmaceuticals

- Global Drug Induced Cardiotoxicity Market

Global Drug Induced Cardiotoxicity Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Drug Induced Cardiotoxicity Market by Drug Class{Tyrosine Kinase Inhibitors (TKIs), Antibiotics, Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)}, Type (Chemotherapy-Induced Cardiotoxicity, Antipsychotic Drug-Induced Cardiotoxicity), Detection (Biomarkers, Imaging Techniques), End User (Hospitals, Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis from 2026 to 2033

Drug Induced Cardiotoxicity Market Size and Trends Analysis

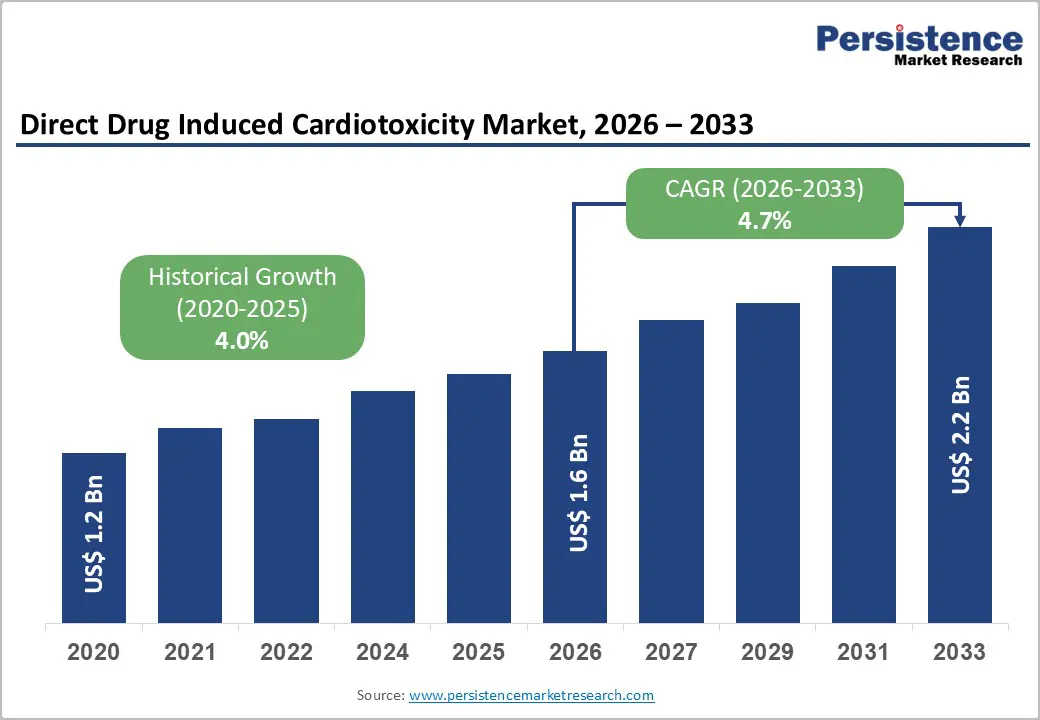

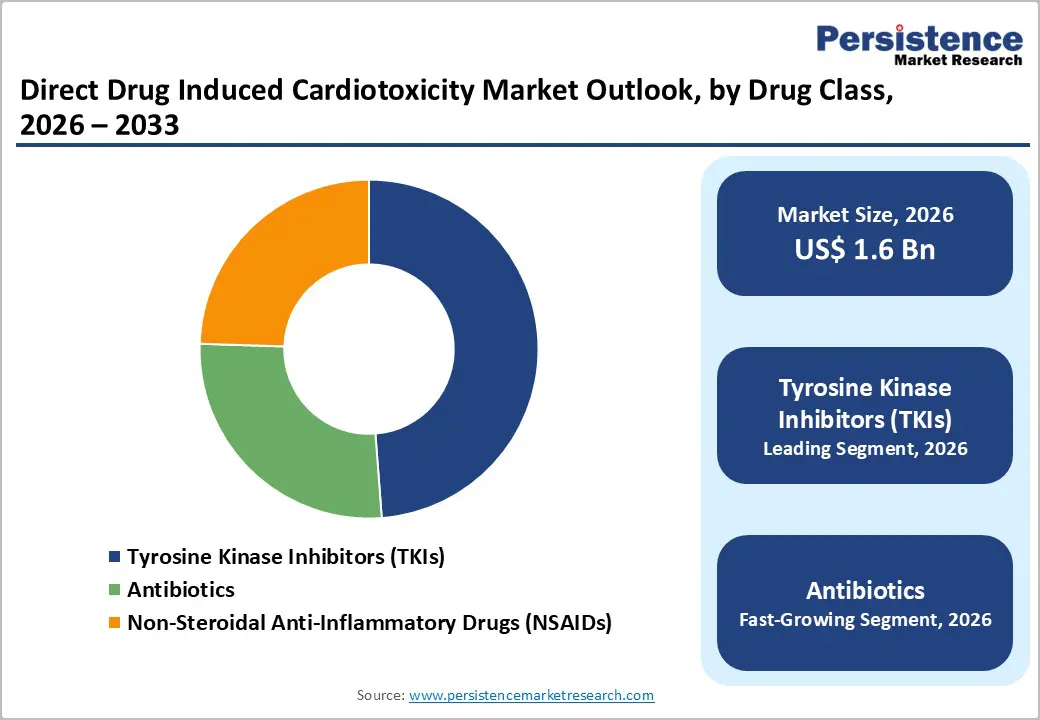

The global Drug Induced Cardiotoxicity Market is estimated to grow from US$ 1.6 Bn in 2026 to US$ 2.2 Bn by 2033. The market is projected to record a CAGR of 4.7% during the forecast period from 2026 to 2033.

The Drug Induced Cardiotoxicity Market is growing steadily, driven by rising use of cardiotoxic drugs, increasing oncology treatments, and greater emphasis on early cardiac risk detection. North America leads due to advanced healthcare infrastructure and strong regulatory focus, while Asia-Pacific is growing rapidly with expanding healthcare access, increasing cancer prevalence, and improved adoption of cardiac monitoring technologies.

Key Industry Highlights

- Dominant Segment: Chemotherapy-induced cardiotoxicity dominates the market with 71.0% share in 2025, driven by widespread use of anthracyclines, TKIs, and targeted cancer therapies that require intensive cardiac monitoring. High reliance on biomarkers and advanced imaging for early detection and risk stratification supports strong adoption across oncology and cardiology settings.

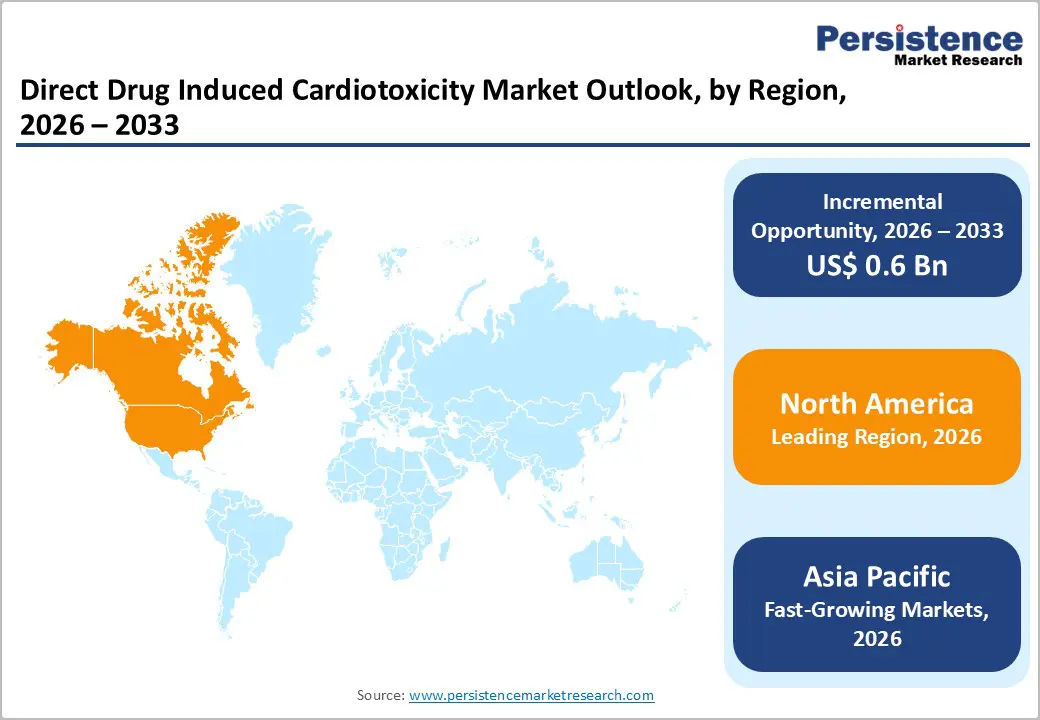

- Dominant Region: North America holds the largest market share with 41.7%, supported by advanced healthcare infrastructure, high oncology drug utilization, strong regulatory oversight, and widespread adoption of cardiac monitoring technologies. Asia-Pacific is the fastest-growing region, driven by rising cancer prevalence, expanding access to oncology care, and improving availability of diagnostic and imaging solutions.

- Market Drivers: Growth is fueled by increasing use of cardiotoxic drugs, rising cancer incidence, greater awareness of treatment-related cardiac risks, integration of cardio-oncology practices, and growing adoption of biomarkers and imaging for early cardiotoxicity detection.

- Market Opportunity: Key opportunities include development of novel cardiac biomarkers, AI-enabled risk prediction tools, advanced imaging technologies, integration with digital health platforms, expansion in emerging markets, and closer collaboration between oncology, cardiology, and pharmaceutical companies.

| Global Market Attributes | Key Insights |

|---|---|

| Global Drug Induced Cardiotoxicity Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Dynamics

Driver – Rising Use of Cardiotoxic Drugs

The rising use of cardiotoxic drugs, particularly in oncology, is a primary driver of the Drug Induced Cardiotoxicity Market. Chemotherapy agents such as anthracyclines remain foundational in treatment regimens for common cancers including breast cancer, lymphoma, and leukemia, with global cancer incidence estimated at 20 million new cases in 2022 according to IARC data. Cardiovascular adverse effects are significant: pooled data indicate chemotherapy related cardiac dysfunction occurs at a rate of 63.2 per 1000 person years among cancer patients, with higher incidence in older adults and those with breast cancer. This prevalence underscores the clinical and economic impetus for improved cardiotoxicity detection and monitoring solutions.

The expanding use of targeted therapies such as tyrosine kinase inhibitors further elevates cardiotoxicity concerns. Meta analyses show that patients receiving targeted agents have a significantly increased risk of cardiotoxic events, with anti VEGFR TKIs demonstrating higher relative risk compared with other agents in some studies. Additionally, studies report substantial rates of cardiotoxicity manifesting as cardiac dysfunction including left ventricular impairment and arrhythmias associated with common oncology treatments. These clinical patterns reflect broader trends in therapeutic adoption and reinforce the need for rigorous cardiotoxicity assessment, contributing to sustained market growth for monitoring and diagnostic tools.

Restraints – High Cost of Advanced Diagnostics

One key restraint on the Drug Induced Cardiotoxicity Market is the high cost of advanced diagnostic tools required for early detection of cardiac injury. State of the art imaging modalities such as cardiac magnetic resonance imaging (cMRI) can cost hospitals about $3.2 million per machine, with ongoing maintenance and staff training adding further financial burden. Advanced biomarker testing platforms, including high sensitivity assays, involve specialized instrumentation and expensive reagents that can run $25–$75 per test, and smaller facilities may incur millions in total equipment ownership costs over five years. These high capital and operational expenses hinder widespread adoption in many clinical settings and resource limited regions.

The economic barrier of advanced diagnostics also affects patient access and institutional investment. In the United States, cardiac imaging and related diagnostics contribute substantially to healthcare spending, with cardiovascular imaging accounting for a significant portion of the more than $100 billion spent annually on imaging services. Price variation across hospitals for standard cardiac tests like echocardiography demonstrates how high and inconsistent costs (e.g., commercial prices several times Medicare rates) can influence utilization decisions. High out of pocket costs and limited reimbursement coverage for complex diagnostic procedures further discourage both providers and patients, particularly in low income settings, suppressing broader market penetration of advanced cardiotoxicity monitoring solutions.

Opportunity – Development of Novel and Predictive Biomarkers

The development of novel and predictive biomarkers presents a significant opportunity in the Drug Induced Cardiotoxicity Market by enabling earlier and more precise detection of cardiac injury from drug therapies. Traditional measures such as left ventricular ejection fraction (LVEF) detect damage after functional decline, but emerging biomarker panels including high sensitivity cardiac troponins (cTnI and cTnT) and circulating microRNAs show promise in identifying subclinical cardiotoxicity before overt dysfunction. In studies with over 5,000 cancer patients, troponin assays demonstrated diagnostic sensitivity of approximately 69% and specificity of 87% for detecting treatment related left ventricular dysfunction, indicating robust predictive potential when combined with clinical surveillance.

In addition to established markers, research highlights emerging molecular biomarkers such as miR 34a, miR 29a, and miR 499 that correlate with cardiomyocyte injury and may signal cardiotoxicity earlier than conventional imaging. One cohort study found upregulation of these markers in patients receiving anthracycline chemotherapy that correlated with elevated high sensitivity troponins, pointing to their utility in early risk stratification. While clinical adoption requires further validation, this evolving biomarker landscape could reduce reliance on costly imaging, enable personalized monitoring, and expand the scope of cardiotoxicity surveillance across drug classes.

Category-wise Analysis

By Drug Class, Tyrosine Kinase Inhibitors (TKIs) Dominates the Drug Induced Cardiotoxicity Market

Molecular Testing dominates with 61.2% share of the global market in 2025, because they are widely prescribed across many common cancers and carry a well documented risk of cardiovascular adverse events. TKIs such as imatinib, sunitinib, and sorafenib have transformed treatment of chronic myeloid leukemia, renal cell carcinoma, and other tumors, contributing to rising usage: in the United States alone, there were more than 1.9 million new cancer cases in 2022, many of which are treated with targeted agents. Clinical data indicate that TKI therapy is associated with significant cardiotoxicity; for example, one meta analysis reported that VEGFR targeting TKIs increased the risk of cardiac dysfunction by ~4.7 fold compared with controls. This high incidence and broad therapeutic adoption drive demand for cardiotoxicity monitoring and diagnostics.

By Type, Chemotherapy-Induced Cardiotoxicity dominates due to widespread use, high cardiac risk, and strong monitoring demand globally

Chemotherapy induced cardiotoxicity dominates the Drug Induced Cardiotoxicity Market because conventional anticancer drugs are widely used and carry substantial cardiac risk, creating high demand for monitoring and early detection. Chemotherapy agents such as anthracyclines are commonly linked to cardiotoxicity, with systematic analyses reporting cardiotoxic events in about 8–9% of treated cancer patients, and higher risks at increased cumulative doses. Heart failure or left ventricular dysfunction occurs in up to 48% of patients receiving anthracyclines at high cumulative dosing, and asymptomatic cardiac changes are frequently detected through sensitive measures like strain imaging and biomarkers. This prevalence underscores routine surveillance needs, particularly in oncology care, driving adoption of cardiotoxicity diagnostics and supporting market dominance for chemotherapy related cardiotoxicity.

Regional Insights

North America Drug Induced Cardiotoxicity Market Trends

North America dominates the Drug Induced Cardiotoxicity Market with 41.7% share in 2025, due to its advanced healthcare infrastructure, widespread access to oncology and cardiology care, and strong regulatory focus on drug safety. The region has a high prevalence of cancer, with the CDC reporting over 1.9 million new cancer cases in 2022 in the U.S., many treated with cardiotoxic therapies like anthracyclines and TKIs. Availability of state-of-the-art diagnostics, such as echocardiography, cardiac MRI, and high-sensitivity biomarkers, allows early detection and management of cardiotoxicity. In addition, strong governmental programs like the FDA’s pharmacovigilance initiatives and widespread clinical awareness ensure rigorous monitoring of drug-induced cardiac adverse events, supporting adoption of cardiotoxicity assessment across hospitals and clinics.

Europe Drug Induced Cardiotoxicity Market Trends

Europe is an important region in the Drug Induced Cardiotoxicity Market because of its comprehensive healthcare systems, strong regulatory frameworks, and high burden of chronic diseases requiring cardiotoxic therapies. The European Cancer Information System reported over 2.7 million new cancer diagnoses in the EU in 2020, many treated with anthracyclines, targeted agents, and other drugs with cardiac risk, driving demand for cardiotoxicity monitoring. European health authorities emphasize proactive safety surveillance, exemplified by regular updates to the European Medicines Agency’s pharmacovigilance guidelines for cardiac adverse events. Additionally, widespread availability of advanced diagnostics including cardiac imaging and biomarker assays supported through universal or highly subsidized healthcare ensures broad access. This combination of high disease prevalence, regulatory emphasis on safety, and accessible diagnostic infrastructure underpins Europe’s leadership in cardiotoxicity assessment.

Asia-Pacific Drug Induced Cardiotoxicity Market Trends

Asia Pacific is the fastest growing region in the Drug Induced Cardiotoxicity Market due to rapidly expanding healthcare infrastructure, rising cancer incidence, and increasing access to advanced diagnostics. The World Health Organization’s GLOBOCAN estimates show Asia accounting for over half of global new cancer cases, driven by populations in China and India, which in turn increases the use of cardiotoxic therapies requiring monitoring. Improvements in healthcare expenditure such as India’s projected health spending growth and China’s continued investment in cancer treatment facilities enhance availability of imaging and biomarker testing. Broader insurance coverage and governmental initiatives to strengthen oncology and cardiovascular care further accelerate adoption of cardiotoxicity detection, making the region the fastest growing globally.

Market Competitive Landscape

Leading applications in the Drug Induced Cardiotoxicity Market focus on early detection, risk assessment, and timely intervention. Advanced diagnostics, including biomarkers and imaging, enable precise identification of cardiac injury, guide treatment decisions, and support patient monitoring. High adoption in hospitals, oncology centers, and cardiology clinics drives market growth and increases acceptance of advanced cardiotoxicity testing globally.

Key Industry Developments:

- In September 2025, Novartis completed its acquisition of Tourmaline Bio, integrating the clinical stage biopharmaceutical company into its cardiovascular pipeline. The deal, valued at approximately $1.4 billion in cash, was finalized with Tourmaline becoming an indirect wholly owned subsidiary of Novartis after a tender offer at $48 per share was accepted by shareholders.

- In June 2025, Novartis entered a four year strategic collaboration with ProFound Therapeutics to discover and develop novel therapeutics targeting cardiovascular disease. Under the agreement, ProFound received $25 million in upfront and near term milestone payments, with potential downstream milestone payments of up to $750 million per selected target, along with tiered royalties.

Companies Covered in Global Drug Induced Cardiotoxicity Market

- Novartis AG

- Pfizer Inc

- Siemens Healthineers

- GE Healthcare

- Amgen Inc

- Bristol Myers Squibb

- Others

Frequently Asked Questions

The global Drug Induced Cardiotoxicity Market is projected to be valued at US$ 1.6 Bn in 2026.

Rising cardiotoxic drug use, increasing cancer prevalence, advanced diagnostics, and regulatory emphasis drive market growth.

The global Drug Induced Cardiotoxicity Market is poised to witness a CAGR of 4.7% between 2026 and 2033.

Development of predictive biomarkers, AI-enabled tools, digital monitoring, emerging markets, and pharma–diagnostic collaborations offer opportunities.

Novartis AG, Pfizer Inc, Siemens Healthineers, GE Healthcare, Amgen Inc.