- Non-food Packaging

- Direct Thermal Linerless Labels Market

Direct Thermal Linerless Labels Market Size, Share, and Growth Forecast, 2026 - 2033

Direct Thermal Linerless Labels Market by Material Type (Paper, Plastic, Others), Application (Retail, Logistics & Transportation, Others), Printing Technology, and Regional Analysis for 2026 - 2033

Direct Thermal Linerless Labels Market Size and Trends Analysis

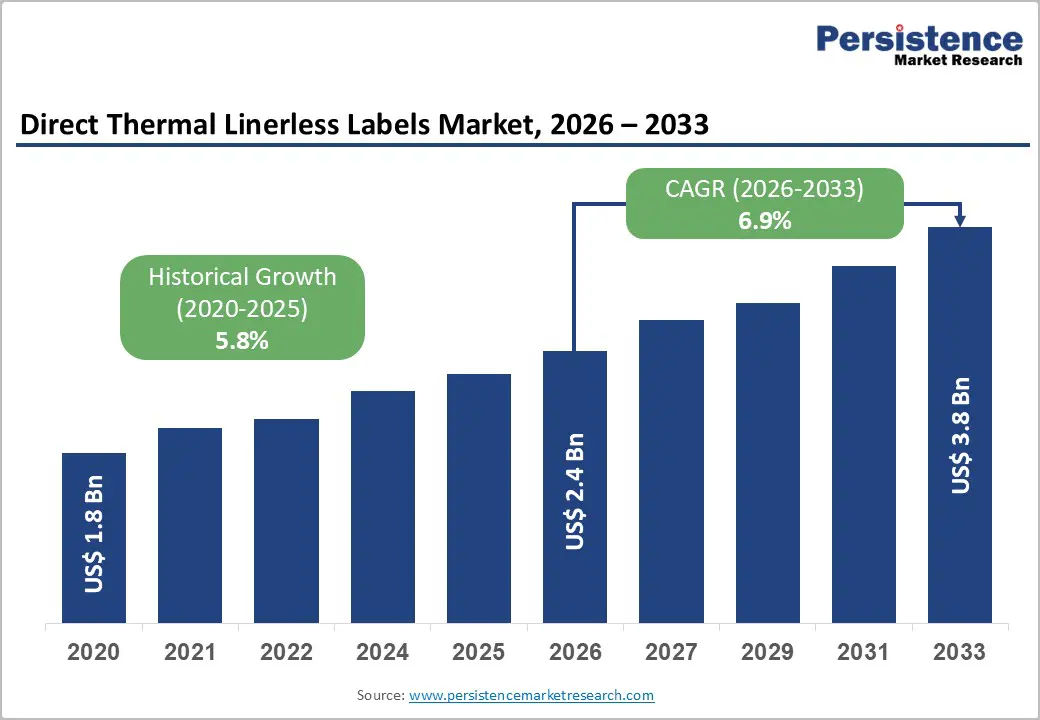

The global direct thermal linerless labels market size is likely to be valued at US$2.4 billion in 2026 and is expected to reach US$3.8 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033, driven by sustainability mandates that reduce backing-paper waste, rising e-commerce and retail labeling volumes, and expanded deployment of direct thermal printing systems that eliminate ribbon costs.

The market reflects a shift toward waste-efficient labeling formats that improve operational throughput while aligning with environmental compliance frameworks. Adoption is strongest in high-volume retail and logistics environments where measurable cost savings and waste reduction can be documented at scale.

Key Industry Highlights:

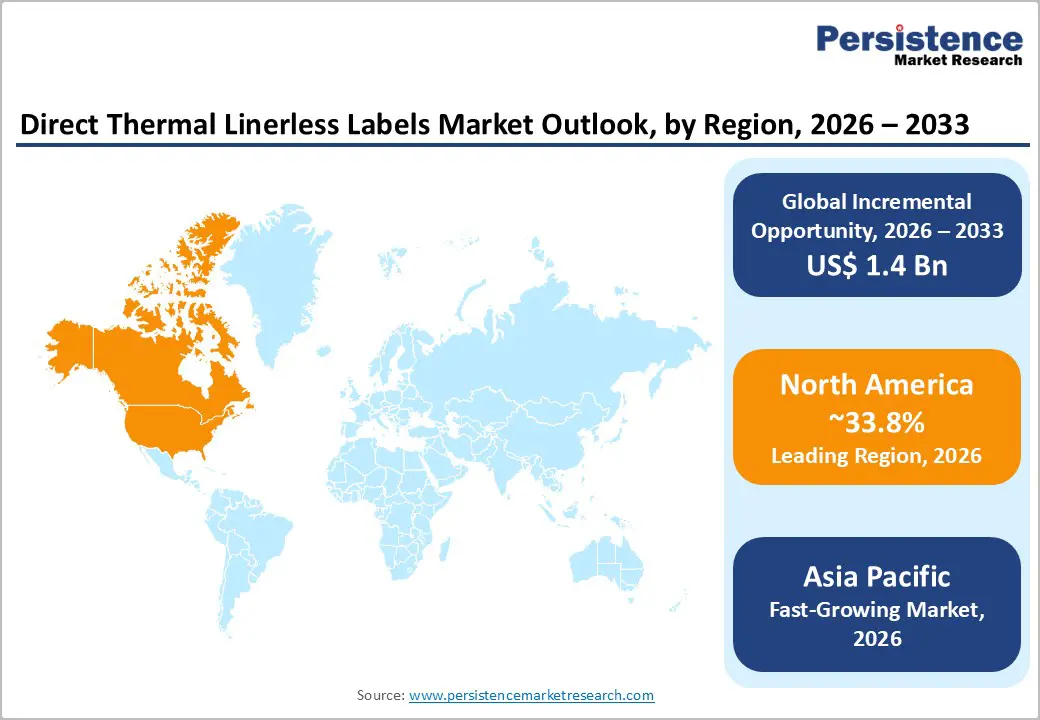

- Leading Region: North America is projected to lead the market, accounting for approximately 33.8% of market share, supported by advanced retail automation, high parcel shipment volumes, and strong corporate sustainability commitments.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, driven by the rapid expansion of organized retail and e-commerce networks, and is emerging as a major consumption and production hub with accelerating year-on-year adoption rates.

- Investment Plans: Converters and OEMs are investing in dedicated linerless coating and adhesive application lines, particularly in North America and Asia Pacific, while European players are expanding R&D in recyclable and food-safe thermal coatings to align with EPR frameworks.

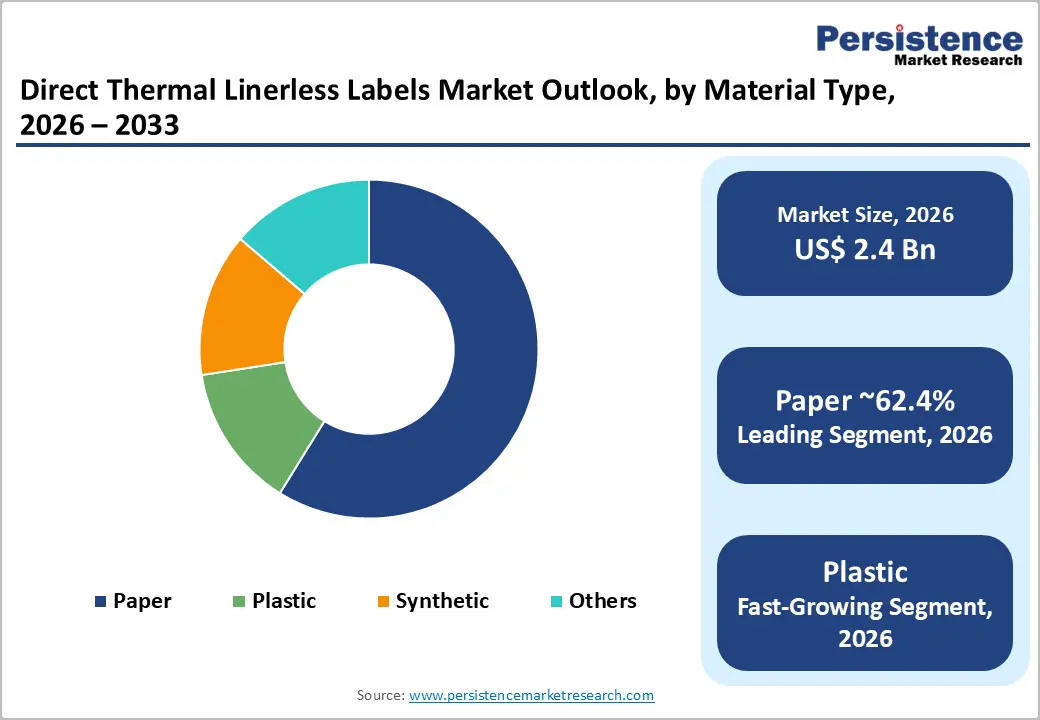

- Dominant Material Type: Paper is anticipated to hold approximately 62.4% of the market share, owing to cost-efficiency, recyclability, and strong suitability for short-life retail and food service applications.

- Leading Application: Retail represents the leading application segment with an anticipated market share of 29.7%, supported by recurring demand from supermarket shelf labeling, promotional pricing, and fresh food packaging systems.

| Key Insights | Details |

|---|---|

| Direct Thermal Linerless Labels Market Size (2026E) | US$2.4 Bn |

| Market Value Forecast (2033F) | US$3.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Regulatory Pressure Accelerating Linerless Adoption

Governments and major retailers are prioritizing packaging waste reduction and landfill diversion initiatives. Traditional pressure-sensitive labels generate liner waste that requires disposal or recycling infrastructure. Linerless formats eliminate this backing paper and can reduce total material consumption per roll by approximately 20-30%, depending on label configuration and application. This reduction directly supports extended producer responsibility (EPR) frameworks and corporate ESG reporting objectives. Large grocery chains and quick-service restaurant (QSR) operators increasingly track waste metrics at the store level, encouraging procurement of labeling systems that minimize disposal volume. The measurable waste reduction associated with linerless labels strengthens the business case for enterprise-level rollouts. As regulatory scrutiny on packaging waste intensifies, linerless solutions are positioned as a compliant and cost-efficient alternative.

Expansion of E-Commerce, Retail, and Food-to-Go Ecosystems

Rapid growth in parcel shipments and prepared food sales is increasing demand for on-demand labels that print quickly with minimal consumables. Direct thermal linerless labels eliminate ribbon requirements and reduce roll changes, improving operational uptime in point-of-sale, weigh-scale, and fulfillment line environments. High-volume retail and logistics operations benefit from greater roll length efficiency and simplified handling procedures. In e-commerce distribution centers, incremental reductions in roll replacement frequency translate into measurable labor savings. Grocery-to-go, click-and-collect, and QSR platforms further expand demand for durable, grease-resistant direct thermal linerless formats. As parcel and in-store labeling volumes grow, conversion to linerless systems enables scalability while controlling per-label cost.

Printer OEM and Materials Innovation

Printer manufacturers and material suppliers have introduced firmware updates, release coatings, and adhesive technologies specifically engineered for linerless applications. Innovations include phenol-free direct thermal topcoats, repositionable adhesives, and wide-web linerless constructions designed for larger format labels. Improved adhesive chemistry allows compatibility across diverse substrates, including corrugated packaging and food containers. Advancements in coating precision reduce printhead wear and improve image stability. These technical developments lower perceived switching risks for end users and expand the range of viable applications. As hardware compatibility improves and material performance stabilizes, linerless technology is transitioning from niche deployment to mainstream adoption across retail and logistics segments.

Barrier Analysis - Conversion and Retrofitting Costs

Transitioning to linerless labeling systems often requires capital investment in compatible printers, cutter mechanisms, and dispensing equipment. Operational adjustments and staff retraining may also be necessary. Payback periods typically range from 6 to 24 months, depending on print volumes, labor rates, and disposal costs. For small and mid-sized enterprises with lower labeling volumes, upfront capital expenditure can delay adoption. This structural cost barrier moderates penetration among smaller retailers and independent logistics providers.

Supply Chain and Raw Material Constraints

Linerless constructions require specialized release coatings and precision-engineered facestocks. Disruptions in specialty chemical supply or coating capacity can affect lead times and pricing stability. In tight supply conditions, margin pressure of approximately 2-6 percentage points may occur for converters without secure upstream agreements. Such volatility introduces procurement risk and may temporarily slow conversion programs among large retail accounts.

Opportunity Analysis - Emerging Market Penetration

Asia Pacific and parts of Latin America remain under-penetrated for linerless adoption despite rapid retail modernization and e-commerce growth. Expanding supermarket chains and QSR networks create scalable deployment opportunities. Lower manufacturing and labor costs in these regions improve unit economics for localized production. Establishing regional converting facilities reduces logistics expenses and improves service responsiveness. Early partnerships with national retail chains can secure long-term contracts and create high-volume recurring demand. First-move advantage in these developing markets offers significant incremental growth potential through 2033.

Vertical Integration and Managed Service Models

Bundling linerless materials with compatible hardware and managed consumables programs presents recurring revenue opportunities. Integrated service agreements that include equipment maintenance, automatic replenishment, and sustainability reporting create stronger customer retention. Retailers and logistics operators increasingly prefer performance-based contracts tied to uptime and waste reduction metrics. Offering subscription-based labeling solutions enables suppliers to differentiate beyond price competition. This vertical integration strategy strengthens supply relationships and stabilizes long-term revenue streams.

Category-wise Analysis

Material Type Insights

Paper-based facestocks are anticipated to account for approximately 62.4% of the market share in 2026, reflecting their strong cost-performance balance and sustainability alignment. Paper remains the material of choice for short-life labeling applications where durability requirements are limited but print clarity and thermal sensitivity are critical. Retail shelf-edge labels, promotional markdown stickers, and deli counter pricing labels widely rely on paper constructions due to their sharp imaging and efficient adhesive compatibility. Supermarket chains such as Walmart and Tesco deploy paper-based linerless labels for in-store weighing systems and fresh food packaging, where rapid turnover supports recurring volume demand. Quick-service restaurant operators, including McDonald's, utilize paper linerless labels for order tracking and takeaway packaging, reinforcing steady consumption patterns. Paper’s recyclability strengthens its competitive position, as it integrates seamlessly into established paper recovery streams. Procurement teams increasingly prioritize materials aligned with corporate ESG commitments, further solidifying paper’s dominance in mainstream linerless applications. Its cost advantage enables rapid enterprise-wide deployment, particularly in high-volume supermarket and QSR environments where label replacement cycles are frequent.

Plastic and synthetic facestocks are emerging as the fastest-growing material segment due to their superior durability and environmental resistance. These materials perform effectively in moisture-prone, refrigerated, or high-abrasion environments where traditional paper labels may degrade. Frozen food packaging, cold-chain logistics, chemical drums, and industrial identification tags increasingly require synthetic linerless constructions that maintain adhesion and legibility under stress. For example, logistics operators such as DHL and FedEx depend on durable labeling solutions capable of withstanding variable temperature exposure during transit. Similarly, temperature-controlled storage facilities operated by Americold rely on high-performance synthetic labels to preserve barcode readability and traceability compliance. Although synthetic materials carry higher upfront production costs, they deliver longer service life and reduced failure rates in demanding applications. Converters capable of producing coated polypropylene (PP) or polyethylene (PE) linerless constructions capture higher-margin opportunities within specialized verticals, strengthening profitability despite lower overall volume share relative to paper.

Application Insights

Retail is anticipated to account for approximately 29.7% of market share in 2026, making it the leading application segment. Shelf labeling, promotional pricing updates, in-store weighing systems, bakery packaging, and ready-to-eat meal identification generate consistent, recurring demand. Linerless formats are particularly attractive in retail settings due to reduced waste generation, improved roll efficiency (more labels per roll), and lower storage and transportation costs compared to linered alternatives.

Major grocery networks such as Carrefour and Kroger integrate linerless labeling into point-of-sale and fresh produce operations to streamline workflow efficiency. Adoption is further supported by self-service weighing systems and automated label printers supplied by manufacturers such as Bizerba. Enterprise-wide rollouts across national supermarket chains create predictable baseline consumption. While pricing pressure remains moderate due to supplier competition, securing multi-location retail contracts enables converters to achieve production scale efficiencies and stable, long-term revenue streams.

Logistics and transportation are projected to be the fastest-growing application segment. Expansion of e-commerce fulfillment networks and last-mile delivery infrastructure drives demand for durable, high-throughput labeling systems. Linerless labels reduce roll change frequency, minimize downtime in automated print-and-apply systems, and improve operational efficiency within distribution centers. Global parcel carriers such as UPS and Amazon operate high-volume fulfillment facilities where labeling speed and reliability are critical. Linerless solutions enhance sustainability credentials by eliminating release liner waste, aligning with corporate environmental targets. Growth in third-party logistics providers and cross-border shipping volumes further accelerates adoption. Suppliers offering high-adhesion formulations compatible with corrugated cartons and variable surface textures are well positioned to capture sustained volume expansion. As automation penetration increases across warehouses, linerless labels are expected to become integral to next-generation logistics workflows.

Regional Insights

North America Direct Thermal Linerless Labels Market Trends - Retail Automation and ESG-Driven Waste Reduction

North America is projected to account for approximately 33.8% of market share, positioning it as the regional leader in direct thermal linerless labels. The region benefits from advanced retail infrastructure, high e-commerce penetration, and well-established printing and converting ecosystems. Large-scale automation in packaging and labeling operations, growing e-commerce and logistics demand, and increasing corporate sustainability commitments are driving the transition from traditional linered labels to linerless label formats. Linerless labels reduce waste by eliminating backing liners, improve operational efficiency through fewer roll changes and faster application, and help companies meet environmental regulations and cost-efficiency goals across sectors such as retail, food & beverage, and logistics.

The U.S. represents the largest contributor, supported by national grocery chains such as Walmart and Kroger, both of which have expanded sustainability initiatives targeting packaging waste reduction. Walmart’s supplier sustainability scorecards, for instance, influence material selection decisions across private-label and fresh food operations, indirectly supporting linerless adoption where waste minimization is prioritized. The rapid expansion of e-commerce fulfillment networks led by Amazon and parcel carriers like UPS increases demand for high-efficiency labeling systems that reduce roll change frequency and operational downtime.

In Canada, grocery retailers such as Loblaw Companies Limited have publicly committed to reducing plastic waste and improving packaging recyclability, strengthening the case for linerless formats in fresh food labeling. From a regulatory standpoint, state-level waste reduction mandates in jurisdictions such as California reinforce procurement shifts toward waste-minimizing solutions. Hardware manufacturers, including Zebra Technologies and Honeywell, have expanded linerless-compatible printer portfolios, enabling smoother enterprise rollouts. Converters across the Midwest and Southeast U.S. are investing in dedicated silicone coating and adhesive application lines near retail distribution hubs, shortening lead times and supporting national deployment programs.

Europe Direct Thermal Linerless Labels Market Trends - EPR Compliance and Circular Economy Standardization

Europe remains a major market, underpinned by strong regulatory alignment with circular economy principles and packaging waste reduction mandates. The region’s emphasis on Extended Producer Responsibility (EPR) frameworks and harmonized recycling targets creates a structurally favorable environment for linerless label adoption. Retail automation across Western Europe further supports consistent volume demand. Germany serves as a technological hub, supported by engineering-led companies such as Bizerba, which supplies retail weighing and labeling systems widely deployed across European supermarkets. German grocery groups, including Edeka, integrate advanced print-and-apply systems within fresh food counters, strengthening baseline linerless consumption.

France and Spain benefit from cross-border converting alliances and centralized procurement structures across pan-European retail groups such as Carrefour. EU-wide directives, including the Packaging and Packaging Waste Directive revisions, incentivize waste reduction technologies by assigning financial responsibility to producers. This regulatory environment enhances the economic case for linerless systems that eliminate release liner waste. Investment focus across Europe centers on R&D in food-safe thermal coatings, recyclable release chemistries, and low-migration adhesives. Regional label producers are forming partnerships to standardize linerless specifications across multiple countries, enabling scalable rollouts while maintaining compliance with evolving EU food contact regulations.

Asia Pacific Direct Thermal Linerless Labels Market Trends - E-Commerce Fulfillment Expansion and Cost-Efficient Manufacturing Growth

Asia Pacific is expected to be the fastest-growing regional market, supported by rapid retail expansion, accelerating e-commerce penetration, and competitive manufacturing economics. Urbanization and organized retail development across emerging economies generate incremental demand for in-store labeling solutions, while established manufacturing hubs provide cost-efficient production capacity for export markets.

China leads regional volume growth. The expansion of fulfillment networks operated by Alibaba Group and JD.com drives large-scale adoption of high-speed labeling systems within automated warehouses. Growth in temperature-controlled logistics for fresh produce and pharmaceuticals further increases demand for durable linerless constructions. Domestic converter investments in coastal manufacturing zones enhance export competitiveness and reduce landed costs for global buyers. India represents a high-growth frontier market. Expansion of organized retail chains such as Reliance Retail and the rapid scale-up of e-commerce platforms, including Flipkart, contribute to rising label consumption. Government initiatives promoting manufacturing under “Make in India” policies encourage localized production of thermal papers and synthetic substrates, strengthening regional supply chains.

Technology transfer from North American and European OEMs into Asian production facilities supports quality standardization and cost optimization. Investments in localized coating lines and adhesive manufacturing reduce import dependence, enhance pricing competitiveness, and position Asia Pacific as both a high-growth consumption market and a strategic production hub for global linerless label supply.

Competitive Landscape

The global direct thermal linerless labels market is moderately concentrated, with global material suppliers and large converters holding significant shares. Regional players compete through customization, service responsiveness, and niche specialization. Competitive positioning depends on supply reliability, innovation in coatings and adhesives, and the ability to integrate hardware and consumables. Market leaders focus on product innovation, supply chain integration, managed services, and geographic expansion. Differentiation increasingly depends on sustainability reporting capabilities and technical compatibility with existing printer fleets.

Key Industry Developments:

- In April 2025, Avery Dennison announced that its direct thermal linerless label AD XeroLinr DT™ was successfully validated for compatibility with Star Micronics’ TSP100IV-UE SK printer, reinforcing its applicability in quick-service restaurant (QSR), takeaway, and delivery environments while advancing sustainable labeling performance.

Companies Covered in Direct Thermal Linerless Labels Market

- Avery Dennison Corporation

- UPM Raflatac

- 3M

- Zebra Technologies

- Mondi Group

- CCL Industries

- R.R. Donnelley & Sons Company

- SATO Holdings Corporation

- Toshiba Tec Corporation

- Bizerba

- ITW Thermal Films

- Hub Labels Inc.

- Ravenwood Packaging

- Coveris

- UPM Specialty Papers

- LINTEC Corporation

- Nippon Paper Industries

- Fuji Seal International

Frequently Asked Questions

The global direct thermal linerless labels market is projected to be valued at approximately US$2.4 billion in 2026.

By 2033, the direct thermal linerless labels market is expected to reach approximately US$3.8 billion.

Key trends include growing substitution of linerless labels with waste-free linerless formats, increasing investment in recyclable and food-safe thermal coatings, rising adoption in automated print-and-apply systems, and expansion of synthetic facestocks for cold-chain and industrial use.

Paper is the leading material segment, anticipated to account for approximately 62.4% of market share, owing to its cost efficiency, recyclability, and strong suitability for short-life retail and food service labeling applications.

Retail represents the leading application segment with an anticipated share of approximately 29.7%, supported by high recurring demand from supermarkets, grocery chains, and fresh food packaging systems.

The direct thermal linerless labels market is projected to grow at a CAGR of approximately 6.9% through 2033.

Major players include Avery Dennison Corporation, UPM Raflatac, 3M, Zebra Technologies, and Mondi Group.