- Automation & Robotics

- Direct Energy Weapon Market

Direct Energy Weapon Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Direct Energy Weapon Market by Technology (High Energy Laser Technology, High Power Microwave Technology, Particle Beam Weapons, Acoustic Directed Energy Devices), Platform (Land-based, Airborne, Naval Combat Ships, Space Satellite based), Lethality (Lethal, Non-Lethal), by Regional Analysis, 2025-2032

Direct Energy Weapon Market Size and Trend Analysis

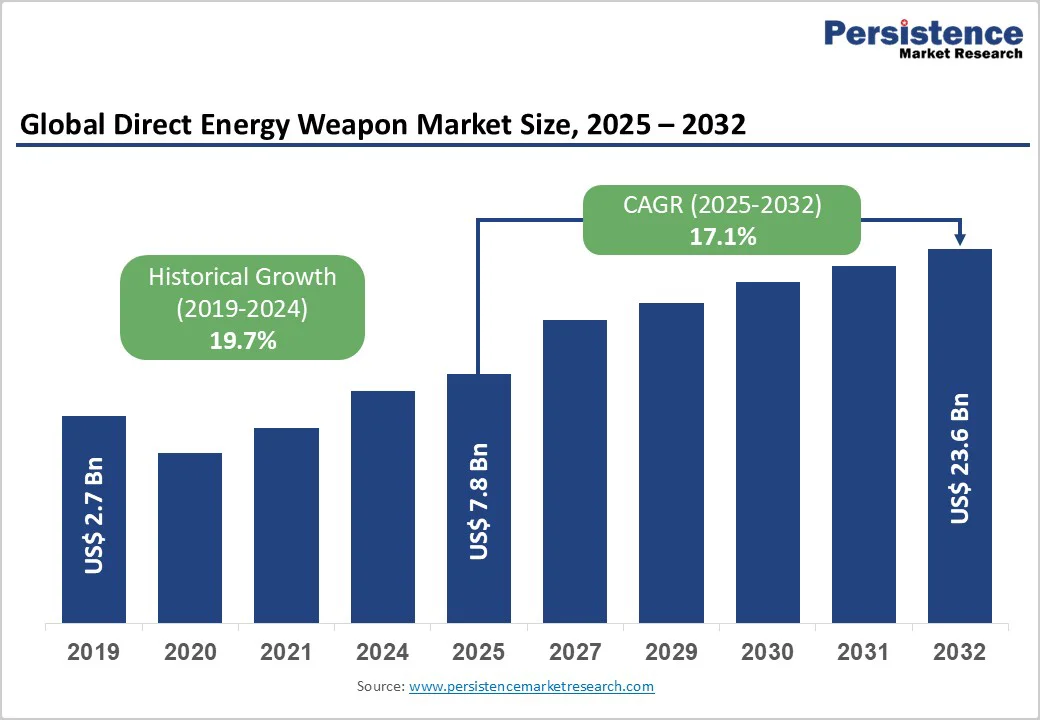

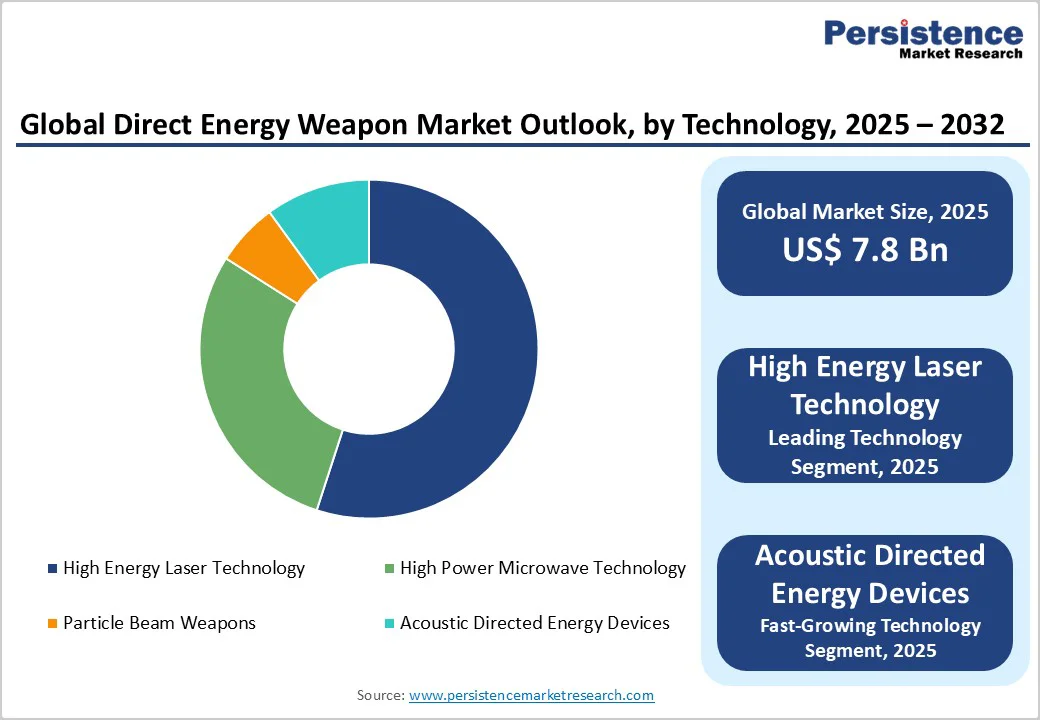

The global direct energy weapon market size is valued US$ 7.8 billion in 2025 and projected to reach US$ 23.6 billion, growing at a CAGR of 17.1% between 2025 and 2032.

The market expansion is primarily driven by escalating global security threats from unmanned aerial vehicles and drone swarm tactics, coupled with the urgent need for cost-effective defense solutions that offer unlimited magazine depth and near-instantaneous engagement capabilities.

Modern directed energy weapons provide significant operational advantages over conventional kinetic systems, including reduced cost per shot estimated at less than one dollar per engagement compared to thousands of dollars for missile interceptors, alongside precision targeting capabilities that minimize collateral damage in complex battlefield environments.

Key Market Highlights

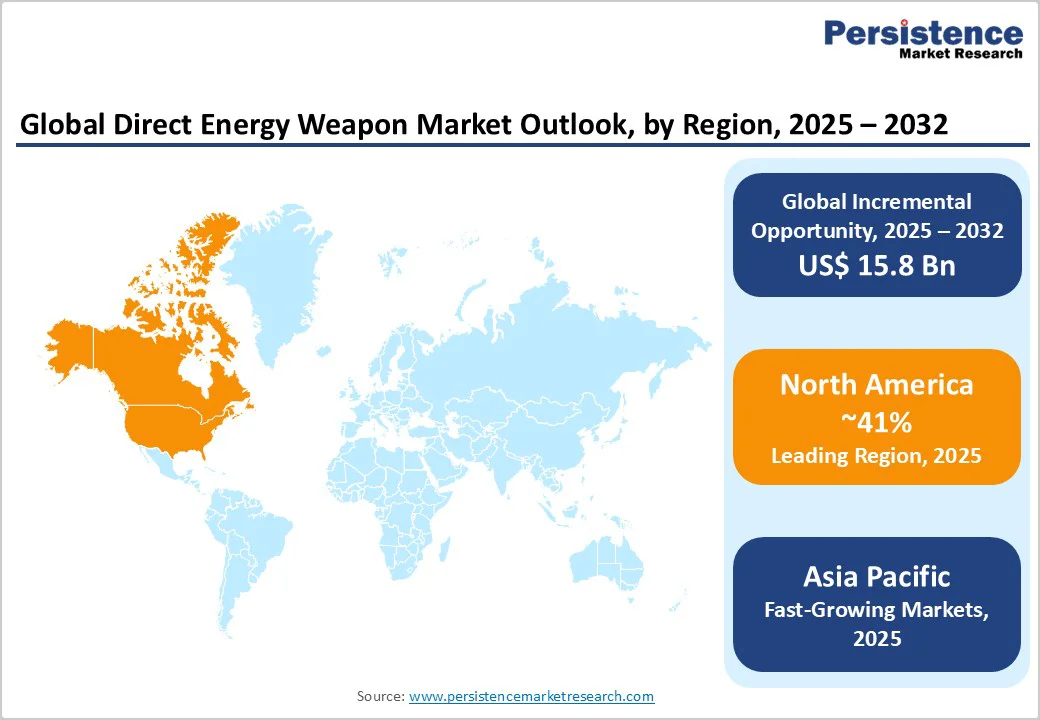

- Leading Region: North America dominates the direct energy weapon market with 41% share in 2025, driven by the United States’ massive investment in directed energy technologies and comprehensive military service programs.

- Emerging Region: Asia Pacific represents the fastest-growing regional market with 22% CAGR through 2032, propelled by China’s, India’s, and Japan’s substantial defense modernization budgets, intensifying regional security competitions, and strategic emphasis on directed energy capabilities for drone defense and maritime security missions.

- Dominant Segment: High energy laser technology commands 55% market share in 2025 as the dominant segment, reflecting successful operational deployments.

- Fastest Growing Segment: Space satellite-based platforms emerge as the fastest-growing segment with 31% CAGR through 2032, driven by strategic requirements for orbital missile defense capabilities, satellite protection missions, and elimination of atmospheric propagation constraints limiting ground-based laser weapon effectiveness.

- Key opportunity: Non-lethal acoustic directed energy devices present significant market opportunities with 24% CAGR growth potential through 2032, addressing escalating demand for crowd control capabilities, perimeter security applications, and law enforcement tools that minimize physical injury risks while maintaining operational effectiveness.

| Key Insights | Details |

|---|---|

| Direct Energy Weapon Market Size (2025E) | US$ 7.8 Bn |

| Market Value Forecast (2032F) | US$ 23.6 Bn |

| Projected Growth CAGR (2025-2032) | 17.1% |

| Historical Market Growth (2019-2024) | 19.7% |

Market Dynamics

Market Growth Drivers

Proliferation of Unmanned Aerial Systems and Counter-Drone Requirements

The exponential growth in commercial and military drone deployment has created an unprecedented security challenge that conventional air defense systems struggle to address economically. According to the U.S. Army’s operational assessments from combat zones, first-person-view drones currently account for 70-80% of battlefield casualties, surpassing traditional artillery impacts.

The U.S. Department of Defense allocates approximately US$1 billion annually toward directed energy weapon development specifically for counter-drone applications, reflecting the strategic priority of this capability. The military drone market continues expanding across Asia Pacific, Europe, and Middle East regions, with nations deploying increasingly sophisticated unmanned systems for reconnaissance and strike missions.

Advancement in Solid-State Laser and Fiber Laser Technologies

Technological breakthroughs in solid-state laser architectures and fiber laser systems have dramatically improved power output, beam quality, and operational reliability for military applications. The U.S. Navy successfully deployed Lockheed Martin’s HELIOS laser system with modular configurations ranging from 60 kW to 120 kW on Arleigh Burke-class destroyers, demonstrating sustained operational capability for drone defense and missile interception at ranges exceeding 6 miles.

The laser warning system market benefits from these advancements as detection and countermeasure technologies evolve alongside offensive capabilities. Contemporary fiber laser systems achieve unprecedented electrical-to-optical conversion efficiencies exceeding 30%, while adaptive optics technologies compensate for atmospheric disturbances, enabling effective engagement in diverse environmental conditions that previously limited directed energy weapon performance.

Market Restraints

Power Generation and Thermal Management Limitations

The operational deployment of high-energy laser systems confronts significant challenges related to power supply infrastructure and heat dissipation requirements. The U.S. Navy’s integration of directed energy weapons on Flight III Arleigh Burke-class destroyers revealed critical constraints, as the AN/SPY-6 radar system consumes substantial electrical capacity, leaving minimal reserve power for 60-150 kW laser weapons.

Ground-based and airborne platforms similarly struggle with the size, weight, and power requirements of laser systems, particularly for sustained engagement scenarios requiring multiple firings. Thermal management systems necessary for preventing component degradation add considerable weight and complexity, directly impacting platform mobility and operational endurance across land-based armored vehicles and unmanned aerial vehicles.

Atmospheric and Environmental Performance Degradation

Directed energy weapons experience significant performance reduction in adverse weather conditions including fog, rain, dust storms, and high humidity environments that scatter or absorb laser energy before reaching the intended target. High-power microwave systems, while less susceptible to atmospheric interference than lasers, face challenges related to electromagnetic spectrum congestion and potential interference with friendly communications and radar systems operating in similar frequency bands. The microwave transmission equipment market addresses some technical challenges, but fundamental physics limitations remain concerning beam propagation through dense atmospheric conditions.

Market Opportunities

Space-Based Directed Energy Weapon Systems Development

The strategic deployment of directed energy weapons on orbital platforms represents a transformative opportunity for global missile defense and satellite protection capabilities. The U.S. Space Force identifies space-based laser systems as critical countermeasures against adversarial anti-satellite weapons and debris threats, with ground-based directed energy weapons limited by atmospheric interference and range constraints.

China’s completion of its space station in 2022 incorporated directed energy technologies as part of comprehensive space domain awareness capabilities, accelerating international competition for orbital weapon systems.

Space satellite-based platforms eliminate atmospheric propagation challenges while achieving significantly closer proximity to targets, though they introduce complex thermal management requirements and vulnerability to adversarial counter-space operations.

As per Persistence Market Research analysis space-based directed energy systems will achieve the fastest segment growth at 31% CAGR through 2032, driven by increasing satellite constellation deployments and the strategic imperative to protect critical space infrastructure supporting communications, navigation, and intelligence gathering missions.

Non-Lethal Acoustic Directed Energy Applications for Crowd Control

Acoustic directed energy devices present substantial market expansion opportunities as governments and security forces seek effective non-lethal alternatives for crowd management and perimeter security applications. Long-range acoustic devices such as LRAD systems deliver focused sound beams exceeding 160 dB at one meter distance, creating painful auditory effects for crowd dispersal while maintaining communication capabilities at extended ranges beyond 500 meters.

The acoustic directed energy devices segment demonstrates exceptional growth potential with projected 24% CAGR through 2032, reflecting increasing procurement by law enforcement agencies, correctional facilities, and critical infrastructure protection teams.

The microwave absorbing materials market similarly benefits from acoustic system development as manufacturers seek to reduce unintended electromagnetic interference from high-power directed energy platforms operating in complex urban environments with dense civilian population concentrations and sensitive electronic infrastructure.

Category-wise Analysis

Technology Insights

High energy laser technology commands 55% market share in 2025, establishing itself as the dominant directed energy weapon technology through proven operational deployments and mature development programs across multiple military platforms. Solid-state laser systems developed by Lockheed Martin, Raytheon Technologies, and Northrop Grumman have successfully transitioned from research prototypes to combat-ready systems.

Contrary, Fiber laser architectures offer superior electrical efficiency, compact form factors, and enhanced thermal management compared to chemical laser predecessors, enabling integration on diverse platforms including naval combat ships, armored vehicles, and fixed installations.

High-energy laser dominance reflects decades of research investment, established supply chains for critical components including beam control systems and adaptive optics, and extensive operational doctrine development for integration with existing air defense networks and command structures.

Platform Insights

Naval combat ships represent the leading platform segment for directed energy weapon deployment, benefiting from substantial electrical power generation capacity and the strategic requirement to defend high-value maritime assets against evolving anti-ship missile threats.

The U.S. Navy has installed laser weapon systems on multiple vessel classes including the USS Ponce and Arleigh Burke-class destroyers, with the HELIOS system providing integrated capabilities for drone defense, missile interception, and sensor dazzling at ranges exceeding several nautical miles.

Naval platforms offer unique advantages including access to ship-generated electrical power eliminating logistical constraints of ammunition resupply, stable mounting platforms for precision beam control systems, and operational environments where atmospheric conditions generally favor laser propagation compared to dusty land environments.

The Europe unmanned aerial vehicle market influences naval directed energy requirements as maritime forces seek comprehensive counter-drone capabilities against reconnaissance and strike-configured unmanned systems.

Germany’s naval laser partnership and Italy’s MBDA-Leonardo naval laser project demonstrate international recognition of shipboard directed energy weapons as essential components of layered fleet air defense architectures protecting carrier strike groups and amphibious ready groups operating in contested littoral waters.

Lethality Insights

Lethal directed energy systems comprise the dominant market segment as military forces prioritize hard-kill capabilities for neutralizing aerial threats including drones, missiles, and manned aircraft through complete destruction of target flight controls, propulsion systems, or structural components.

High-energy laser weapons operating at power levels from 20 kW to 300 kW deliver sufficient energy density to ignite fuel systems, melt critical flight surfaces, or destroy guidance electronics, ensuring targets cannot continue mission execution or return to base for rearmament.

The U.S. Army’s Enduring-High Energy Laser program specifically requires “hard kill” capabilities against Group 1, 2, and 3 unmanned aerial systems, with solicitations seeking systems capable of preventing sustained flight through catastrophic damage rather than temporary disabling effects.

China’s LY-1 high-energy laser system showcased at defense exhibitions demonstrates lethal engagement capabilities against multiple target categories, with Pakistan exploring acquisition to counter India’s carrier strike groups and advanced drone capabilities.

Military doctrine emphasizes lethal directed energy systems for homeland defense, forward operating base protection, and naval fleet defense scenarios where temporary target disabling provides insufficient security assurance, driving continued investment in higher-power laser architectures and more efficient energy delivery mechanisms that guarantee target neutralization.

Regional Insights

North America Direct Energy Weapon Market Trends

North America maintains market leadership with 41% share in 2025, driven by the United States’ comprehensive directed energy weapon development programs spanning all military services and platform categories.

The U.S. Department of Defense invests approximately US$1 billion annually in directed energy technologies, with the U.S. Army advancing the Enduring-High Energy Laser program toward a first program of record by fiscal year 2026, following successful prototype deployments including the 50-kilowatt DE M-SHORAD system.

The United States benefits from a mature defense industrial base including Lockheed Martin, Raytheon Technologies, Northrop Grumman, L3Harris Technologies, and Boeing, which collectively possess decades of directed energy research experience and established supply chains for critical components including high-power laser diodes, beam control systems, and adaptive optics.

The U.S. Air Force also explores airborne laser platforms for missile defense and counter-drone missions. Congressional funding support remains robust with bipartisan recognition of directed energy weapons as force multipliers addressing drone proliferation, hypersonic missile threats, and contested electromagnetic spectrum challenges that conventional kinetic systems cannot effectively counter.

Europe Direct Energy Weapon Market Trends

Europe demonstrates accelerating directed energy weapon adoption driven by heightened security concerns following geopolitical tensions and NATO strategic initiatives emphasizing technological superiority in air defense capabilities.

In July 2024, the UK tested Raytheon UK’s laser weapon on a Wolfhound vehicle, successfully engaging targets beyond one kilometer, while the separate DragonFire program had earlier completed high-power firing trials without disclosed accuracy details. Germany advances its Laser Weapon Demonstrator program with successful ship-based trials reflecting strategic European defense autonomy objectives and cross-border industrial collaboration frameworks.

France advanced its directed energy efforts with the Syderal laser defense program, awarding development contracts to MBDA, Thales, Safran, and CILAS under the 2024-2030 military plan with deployment targeted for 2030.

Italy is pursuing naval laser systems through MBDA Italia and Leonardo, while Spain’s growing defense budgets support integration of directed energy technologies. EU collaboration frameworks and modular open architecture policies further enable shared development and procurement, giving smaller member states access to advanced laser capabilities.

Asia Pacific Direct Energy Weapon Market Trends

Asia Pacific is the fastest-growing region at a 22% CAGR through 2032, driven by rising security competition and major defense modernization programs in China, India, Japan, South Korea, and Australia. China leads regional advancements with its LY-1 high-energy laser system and broader directed energy infrastructure, supported by strong domestic production enabling rapid deployment and growing export traction across Africa, the Middle East, and Southeast Asia.

India’s DRDO is advancing high-energy laser and microwave weapons, developing systems with light-speed engagement capabilities suited for counter-UAV and border defense roles. Japan allocates significant funding to shipboard laser and hypersonic programs, while Australia focuses on high-power microwave weapons for drone-swarm defense. South Korea and several ASEAN nations are exploring laser and HPM technologies for missile, coastal, and critical-infrastructure protection, supported by competitive global suppliers.

Competitive Landscape

The global direct energy weapon market exhibits moderate consolidation with established defense prime contractors including Lockheed Martin, Raytheon Technologies, Northrop Grumman, BAE Systems, and Boeing commanding substantial market shares through decades of research investment and established relationships with military procurement agencies.

Market leaders pursue strategic differentiation through power scaling capabilities, with systems ranging from 20 kW tactical lasers to 300 kW fleet defense platforms, alongside vertical integration strategies encompassing beam generation, fire control systems, and platform integration capabilities.

Companies increasingly adopt modular open systems architecture enabling rapid technology insertion and cross-platform compatibility, while artificial intelligence and machine learning integration enhances autonomous target acquisition and engagement sequencing for drone swarm scenarios.

Strategic partnerships between traditional defense contractors and specialized photonics companies accelerate innovation cycles, with emerging players including Kratos Defense & Security Solutions and BlueHalo disrupting established market dynamics through agile development approaches and rapid prototype-to-production transitions.

Key Market Developments:

- April 2024: BlueHalo was awarded a four-year full-cycle support contract by the U.S. Army for its P-HEL high energy laser system, positioning BlueHalo as lead integrator from prototype to frontline operations.

- August 2025: The French DGA placed a contract with MBDA, Safran Electronics & Defence, Thales, and CILAS for the SYDERAL demonstrator (“Système Laser de Défense de Nouvelle Génération”), a high-power laser (several tens of kilowatts) to counter drones, rockets, mortar shells, and loitering munitions, with modular architecture and advanced beam-combining, tracking, and adaptive optics - aiming for evaluation and possible deployment by 2030.

Companies Covered in Direct Energy Weapon Market

- Lockheed Martin

- Raytheon Technologies

- Northrop Grumman

- BAE Systems

- The Boeing Company

- Leonardo SpA

- Thales Group

- L3Harris Technologies

- Rheinmetall AG

- Rafael Advanced Defense Systems

- Elbit Systems

- Kratos Defense & Security Solutions

- Textron Inc.

- MBDA

- Honeywell International

- BlueHalo

- Safran Electronics & Defense

- CILAS

- KBR (Kord Technologies)

- nLight

Frequently Asked Questions

The global direct energy weapon market is projected to reach US$ 23.6 Bn by 2032, growing from US$ 7.8 Bn in 2025 at a compound annual growth rate of 17.1% during the forecast period 2025-2032.

The market is primarily driven by the proliferation of unmanned aerial systems creating unprecedented counter-drone requirements, alongside technological advancements in solid-state laser and fiber laser systems.

High energy laser technology dominates the market with 55% share in 2025, driven by successful operational deployments.

North America leads the direct energy weapon market with 41% share in 2025, driven by the United States’ comprehensive development programs spanning all military services.

Space satellite-based directed energy systems represent significant opportunities with 31% CAGR growth through 2032.

Major market participants include Lockheed Martin, Raytheon Technologies, Northrop Grumman, BAE Systems, The Boeing Company, Leonardo SpA, Thales Group, etc.