- Healthcare

- Direct-to-Consumer (DTC) Testing Market

Direct-to-Consumer (DTC) Testing Market Size, Share, and Growth Forecast 2026 - 2033

Direct-to-Consumer (DTC) Testing Market by Category-1 (Genetic Testing, Diagnostic & Disease-Oriented Testing, Microbiome Testing, Rapid Self-Tests, Others), by Category-2 (Retail Pharmacies & Drugstores, Supermarkets / Hypermarkets, Direct Online Sales), by Regional Analysis, 2026-2033

Direct-to-Consumer (DTC) Testing Market Size and Trend Analysis

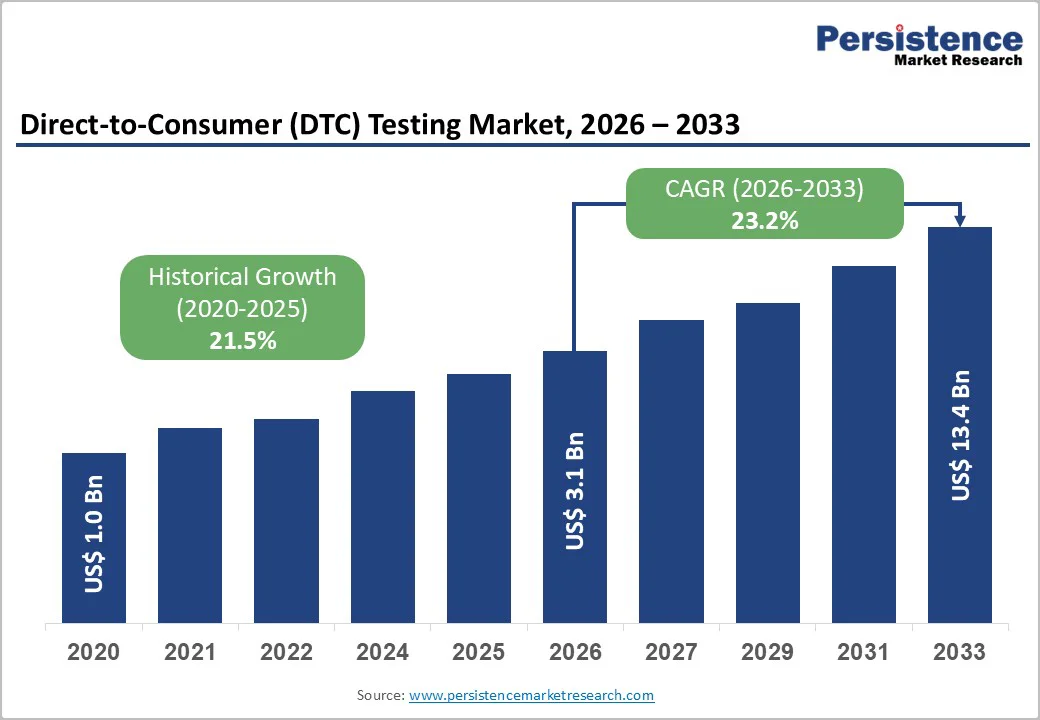

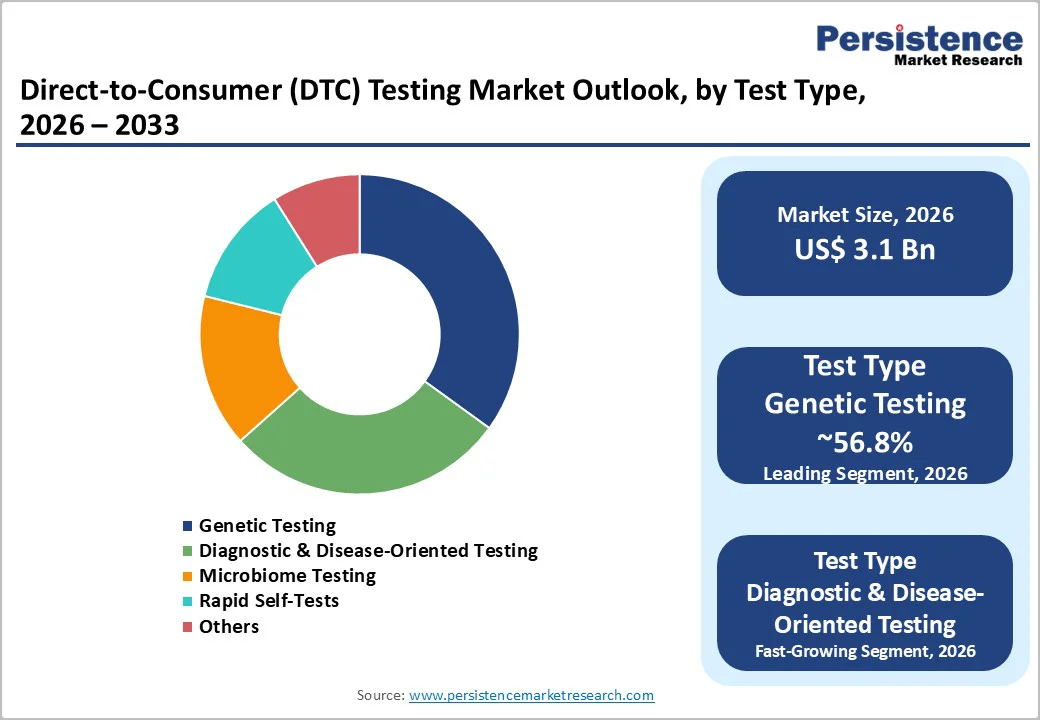

The global Direct-to-Consumer (DTC) Testing Market size is likely to be valued at US$ 3.1 Billion in 2026 and is expected to reach US$ 13.4 Billion by 2033, growing at a CAGR of 23.2% during the forecast period from 2026 and 2033.

The market is primarily driven by the increasing consumer prioritization of preventive healthcare and the growing demand for personalized medical insights. Technological advancements, particularly in Next-Generation Sequencing (NGS) and digital health platforms, have significantly reduced the cost of genetic and diagnostic testing, making these services more accessible to the mass market. Furthermore, the proliferation of digital pharmacy integrations and the convenience of at-home sample collection are shifting consumer behavior away from traditional clinical settings toward decentralized, user-initiated testing models.

Key Market Highlights

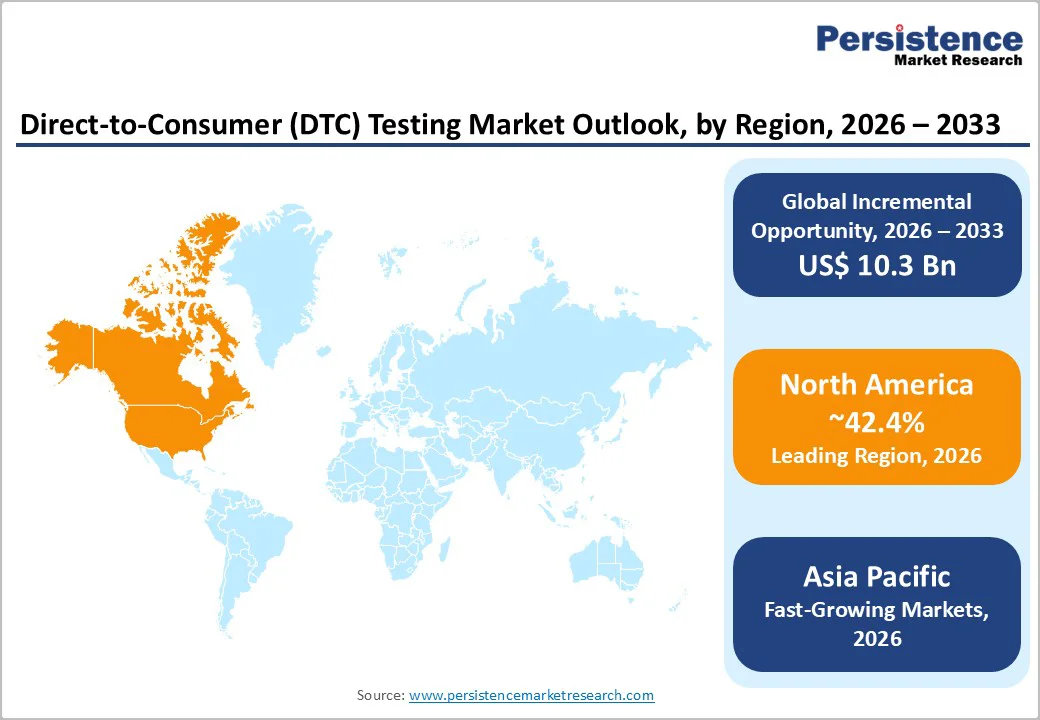

- Leading Region: North America commands the largest market share at 42.4%, supported by high consumer adoption, favorable reimbursement trends, and the presence of major industry players’ headquarters.

- Fastest Growing Region: Asia Pacific is projected to witness the highest growth, capturing 36.1% of global revenue, driven by rising disposable incomes, aging populations, and large untapped consumer bases in China and India.

- Dominant Segment: Genetic Testing remains the top revenue-generating segment, holding 56.8% of total revenue, fueled by continued interest in ancestry tracing and hereditary health screening.

- Fastest Growing Segment: Diagnostic & Disease-Oriented Testing is accelerating rapidly as consumers increasingly rely on at-home kits for managing chronic conditions and infectious diseases.

- Key Market Opportunity: Integration of Pharmacogenomics into DTC platforms represents a substantial untapped opportunity to personalize medication management and reduce adverse drug reactions.

| Key Insights | Details |

|---|---|

|

Direct-to-Consumer (DTC) Testing Market Size (2026E) |

US$ 3.1 Billion |

|

Market Value Forecast (2033F) |

US$ 13.4 Billion |

|

Projected Growth CAGR (2026-2033) |

23.2% |

|

Historical Market Growth (2020-2025) |

21.5% |

Market Dynamics

Market Growth Drivers

Rising Consumer Interest in Proactive and Personalized Healthcare Driving DTC Testing Adoption

The growing focus on preventive healthcare and personalized medicine is a major factor propelling the direct-to-consumer testing market. Consumers increasingly seek early detection of health risks, such as genetic predispositions to cancer, cardiovascular diseases, or lifestyle-related conditions like diabetes, without needing immediate physician intervention. This trend is amplified by the “quantified self” movement, where individuals track biomarker data to optimize fitness, nutrition, and overall wellness.

By offering convenient, private, and actionable health insights, DTC testing empowers consumers to make informed lifestyle changes and take charge of their health proactively. The ability to monitor personal health metrics independently enhances awareness, encourages preventive measures, and drives the adoption of both genetic and diagnostic screening solutions across diverse populations.

Technological Innovation and Integration with Digital Health Platforms as a Growth Catalyst

Technological advancements are significantly expanding the DTC testing market. Reduced costs of genomic sequencing, coupled with artificial intelligence–driven interpretation of complex biomarker data, allow companies to provide user-friendly, actionable health insights that were previously difficult for consumers to understand. These innovations transform complex medical information into clear guidance for lifestyle, wellness, and early intervention decisions.

Seamless integration with telehealth platforms strengthens the overall value of DTC testing. Positive results can instantly trigger virtual consultations, guidance, or prescription services, creating a complete care pathway. This combination of AI, digital health integration, and connectivity enhances accessibility, convenience, and reliability, making DTC testing a more comprehensive and widely adopted health management solution.

Market Restraints

Data Privacy Concerns and Cybersecurity Risks Limiting Market Growth

The rapid expansion of the DTC testing market is tempered by growing consumer apprehension about the security of sensitive genetic and health data. High-profile cybersecurity incidents, including data breaches affecting millions of users at major companies like 23andMe, have eroded public trust. Consumers are increasingly concerned that their immutable genetic information could be accessed by unauthorized parties, insurers, or employers, raising fears of discrimination or exploitation.

These privacy and security risks create substantial psychological barriers for potential customers. Many individuals hesitate to share biological samples or personal data with private entities, limiting the adoption of genetic and diagnostic testing solutions. Maintaining robust cybersecurity measures and transparent privacy policies is essential for companies to build consumer confidence and sustain market growth.

Regulatory Uncertainty and Compliance Challenges Impeding DTC Testing Expansion

The DTC testing market faces a complex and dynamic regulatory environment, which presents significant challenges for industry participants. While select tests have received FDA authorization, many Laboratories Developed Tests (LDTs) remain subject to shifting oversight policies, including ongoing legal debates regarding the FDA’s regulatory authority over these medical devices.

Furthermore, inconsistent regulations across regions such as stringent GDPR compliance requirements in Europe versus evolving FDA guidelines in the United States force companies to navigate a patchwork of standards. This regulatory uncertainty can delay product launches, increase operational costs, and complicate strategic planning, ultimately restraining the market’s overall growth potential and investment attractiveness.

Market Opportunities

Expansion into Pharmacogenomics and Chronic Disease Management as a Strategic Opportunity

DTC testing companies have a substantial opportunity to expand beyond ancestry and general wellness into medically actionable areas such as pharmacogenomics (PGx) and chronic disease monitoring. PGx testing evaluates how an individual’s genetic makeup influences drug response, helping reduce trial-and-error prescribing for conditions like depression, cardiovascular disease, and chronic pain.

By partnering with healthcare systems and health plans, DTC providers can offer personalized medication management tools that improve outcomes and reduce healthcare costs. This integration of PGx and chronic disease monitoring into clinical workflows not only creates recurring revenue streams but also positions DTC testing as an essential component of mainstream, precision-focused healthcare delivery.

Integration of Microbiome and Nutritional Testing to Capture Holistic Wellness Demand

The growing field of microbiome science offers high-growth potential for DTC companies seeking market diversification. Increasing research connects gut health to immunity, mental wellness, and chronic inflammation, driving consumer demand for tests that provide personalized dietary and lifestyle recommendations based on microbiome profiles.

Companies that translate complex microbiome data into clear, actionable nutritional guidance or supplement plans can capture a dedicated segment of the wellness market. This movement toward “food as medicine,” supported by verified biological insights, aligns with consumer preferences for evidence-based, holistic health solutions, enhancing engagement and brand loyalty while expanding DTC testing’s reach beyond conventional wellness applications.

Category-wise Insights

Test Type Analysis

The Genetic Testing segment currently dominates the DTC testing market, capturing approximately 56.8% of total revenue. This leadership is driven by the enduring popularity of ancestry and health risk assessments and the strong brand presence of major players such as 23andMe and AncestryDNA. The normalized process of mailing saliva samples for DNA analysis and receiving detailed genetic insights has made this segment the primary revenue contributor in the market.

Meanwhile, the Diagnostic & Disease-Oriented Testing segment is experiencing rapid growth. Post-pandemic normalization of at-home self-testing for infectious diseases like COVID-19 and STIs, along with monitoring chronic biomarkers such as HbA1c and cholesterol, is driving adoption. Consumers increasingly prioritize immediate, actionable health information, making this segment the fastest-growing area within the DTC testing ecosystem.

Distribution Channel Analysis

Direct Online Sales lead the DTC testing market, capturing approximately 65% of total market share. The channel’s dominance stems from the convenience of e-commerce platforms, which allow consumers to order tests discreetly, submit samples easily, and access results through secure portals. This model bypasses geographical limitations and provides access to specialized tests that may not be available in local retail outlets.

The Retail Pharmacies & Drugstores channel is emerging as a key growth avenue. Major pharmacy chains are increasingly stocking diagnostic and wellness kits to target impulse buyers and consumers seeking immediate access. The accessibility of these physical retail channels complements online sales, driving broader adoption and supporting market expansion.

Regional Insights

North America Direct-to-Consumer (DTC) Testing Market Trends

North America, led by the United States, dominates the global DTC testing market, capturing 42.4% of total revenue. The region benefits from a highly developed healthcare infrastructure, high consumer disposable income, and the presence of leading companies such as 23andMe, Everlywell, and Quest Diagnostics. FDA-established pathways for certain genetic health risk reports further support market leadership.

Integration of DTC testing into employee wellness programs and health insurance plans is accelerating adoption. Consumers increasingly value the convenience, privacy, and actionable insights offered by DTC services, while ongoing innovation in genetic and diagnostic testing reinforces North America’s position as the largest and most mature regional market globally.

Europe Direct-to-Consumer (DTC) Testing Market Trends

Europe presents a fragmented DTC testing landscape with stringent regulatory oversight and strict data protection laws, including GDPR, which governs genetic data processing. These requirements have slowed adoption of US-based services while encouraging local companies to offer privacy-focused solutions. Countries like the United Kingdom show relatively higher openness to DTC testing, whereas Germany and France often restrict genetic testing to prescriptions.

Despite regulatory hurdles, Europe is projected to grow at a CAGR of 25.2%. Rising consumer demand for lifestyle, nutrigenomics, and wellness-focused tests drives this growth, as companies innovate products that navigate strict compliance while providing actionable insights, gradually expanding market adoption across key European nations.

Asia Pacific Direct-to-Consumer (DTC) Testing Market Trends

The Asia Pacific region is emerging as the fastest-growing DTC testing market, capturing 36.1% of global revenue. Growth is fueled by a rapidly expanding middle class, aging populations in Japan and China, and rising health awareness. Local startups are providing genetic tests tailored to Asian populations, addressing gaps left by Western-centric databases. Government initiatives promoting precision medicine, particularly in China, indirectly support market expansion.

Markets like India and South Korea are witnessing growth in affordable diagnostic screening kits due to rising chronic disease prevalence and limited primary care access. Increasing consumer preference for preventive health solutions, combined with technological innovation and telehealth integration, positions Asia Pacific as a high-potential growth region within the global DTC testing market.

Competitive Landscape

The global DTC testing market is moderately consolidated, with the genetic segment dominated by a few leading players, while the diagnostic segment remains highly fragmented with numerous specialized providers. Market leaders are shifting from one-off test sales to subscription-based care models, enhancing customer retention and expanding revenue streams. Strategic acquisitions and vertical integration are being leveraged to strengthen service offerings and operational efficiency.

Emerging business models increasingly focus on B2B2C strategies, partnering with employers and health plans to distribute tests as part of corporate wellness benefits. The adoption of “test-to-treat” solutions, integrating telehealth and pharmacy services, is becoming a key differentiator in the competitive landscape.

Key Market Developments

- In October 2025, Everlywell unveiled "Eva," a next-generation AI-powered health platform designed to interpret complex biomarker data and provide personalized care plans, signaling a major shift toward AI-enhanced diagnostics.

- In June 2025, LetsGetChecked finalized its acquisition of digital pharmacy Truepill, effectively combining at-home diagnostics with medication delivery to create a seamless end-to-end healthcare service for consumers.

- In September 2024, 23andMe agreed to pay US$ 30 million to settle a class-action lawsuit regarding a 2023 data breach that exposed the information of nearly 7 million users, highlighting the critical importance of cybersecurity in the sector.

Companies Covered in Direct-to-Consumer (DTC) Testing Market

- 23andMe, Inc.

- AncestryDNA

- MyHeritage Ltd.

- Color Genomics, Inc.

- Everlywell, Inc.

- Invitae Corporation

- Helix OpCo LLC

- LetsGetChecked Ltd.

- Vitagene, Inc.

- Nebula Genomics

- Fulgent Genetics

- Dante Labs

- CircleDNA

- EasyDNA

- Quest Diagnostics Incorporated

Frequently Asked Questions

The global market is forecast to reach a valuation of US$ 13.4 Billion by 2033, expanding significantly from its 2026 valuation of US$ 3.1 Billion.

Key drivers include the rising consumer demand for preventive healthcare, advancements in genomic technology lowering costs, and the increasing convenience of digital health platforms.

The Genetic Testing segment holds the largest market share, holding 56.8%, driven by the widespread popularity of ancestry services and genetic health risk assessments.

North America is expected to remain the dominant region at 42.4%, supported by advanced healthcare infrastructure, major market players, and high consumer awareness.

The integration of Pharmacogenomics and personalized nutritional testing (microbiome analysis) offers significant growth potential by providing medically actionable insights.

Major companies include 23andMe, Inc., AncestryDNA, Everlywell, Inc., LetsGetChecked Ltd., and Quest Diagnostics Incorporated.