- Industrial Goods & Service

- Direct to Packaging Printer Market

Direct to Packaging Printer Market Size, Share, and Growth Forecast, 2025 - 2032

Direct to Packaging Printer Market By Printer Type (Single-Pass Printers, Multi-Pass Printers), Technology (Inkjet Printing, UV Printing, Others), Packaging Type (Rigid Packaging, Others), End-user Industry (Food & Beverage, Others), and Regional Analysis for 2025 - 2032

Direct to Packaging Printer Market Share and Trends Analysis

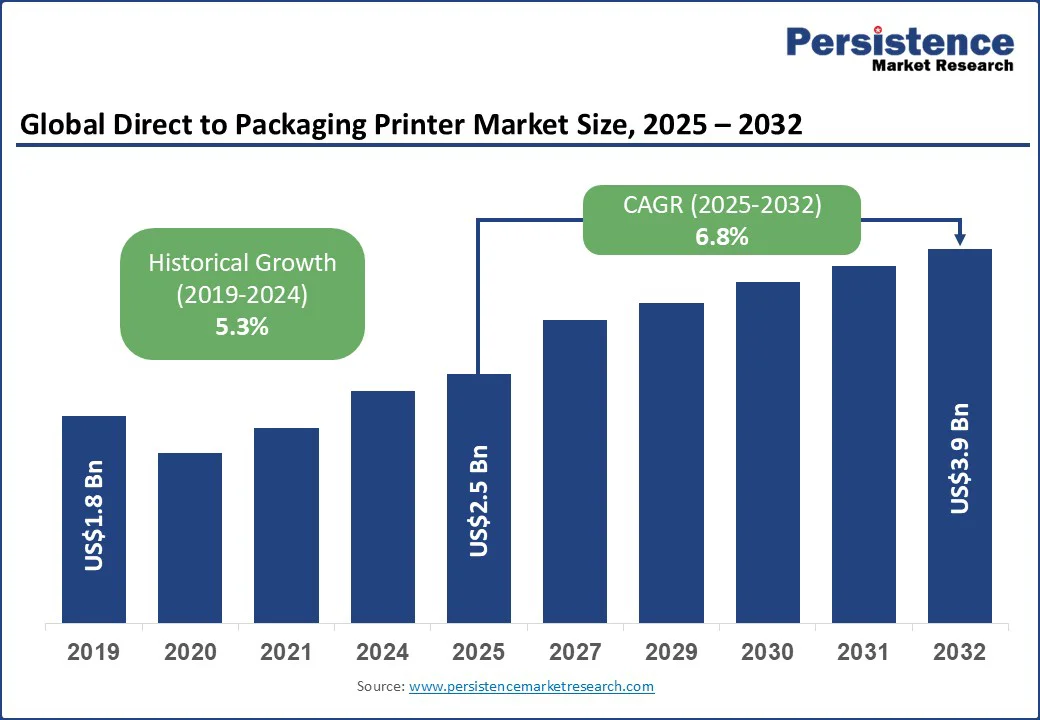

The global direct to packaging printer market size is projected to rise from US$2.5 Bn in 2025 to US$3.9 Bn by 2032. It is anticipated to witness a CAGR of 6.8% during the forecast period from 2025 to 2032.

The market expansion is driven by the rising adoption of digital printing technologies, enabling high-quality, customizable printing across flexible, semi-rigid, and rigid packaging.

Innovations in UV, toner-based, and inkjet printing systems enhance production efficiency, allowing short-run, on-demand printing that meet evolving consumer and e-commerce requirements. Direct-to-packaging printing enables brands to achieve precise, high-resolution graphics directly on packaging materials, allowing for traceability, smart codes, and interactive features. Growing e-commerce, subscription-based retail, and short-run campaigns fuel the need for versatile packaging solutions.

E-commerce trends are reshaping packaging demand, with online retail expected to reach US$5.5 Tn by 2027, driving higher requirements for digital print solutions. Companies are increasingly deploying high-speed printers capable of printing on diverse substrates, such as corrugated boards, films, and flexible packaging, to meet fast delivery cycles. Innovations by key players such as Mehta Hitech, Mutoh, and AstroNova highlight the market’s shift toward scalable, efficient, and sustainable digital printing solutions, enabling precision, productivity, and on-demand customization.

Key Industry Highlights

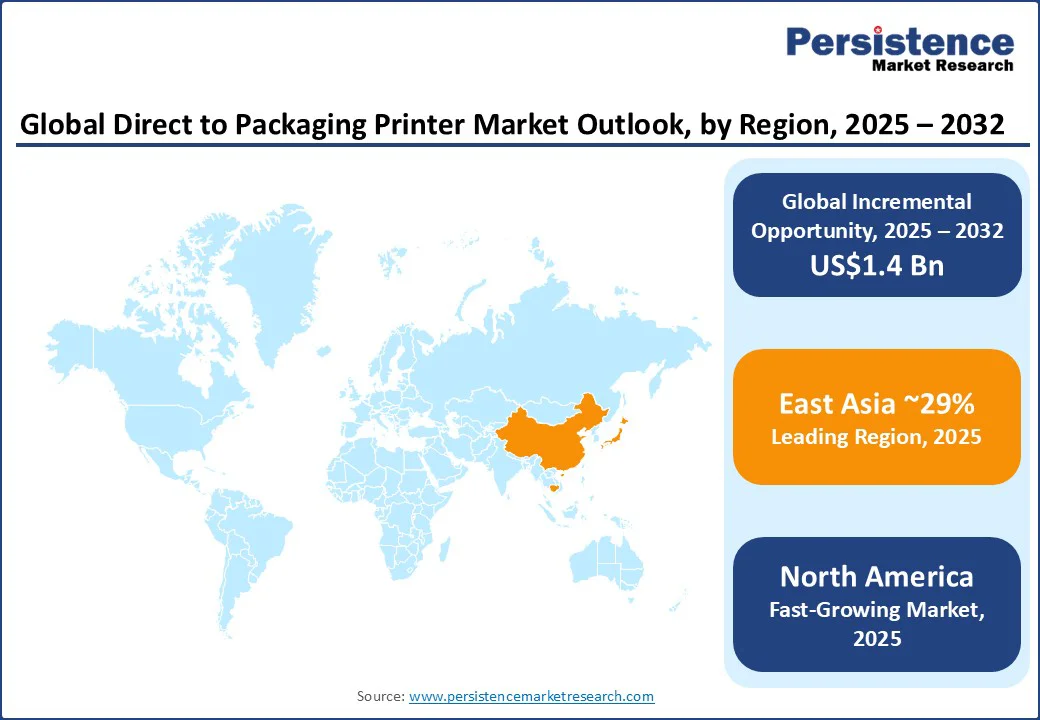

- Leading Region: East Asia is projected to hold approximately 29%, fueled by e-commerce growth, technological adoption, and logistics demand.

- Fastest-growing Region: North America is expected to hold a significant share of around 24% and is also projected to be the fastest-growing region, supported by a dynamic manufacturing base, a strong food and beverage industry, and rapid growth in e-commerce packaging applications.

- Dominant Technology Type: Inkjet printing is anticipated to lead with approximately 53.4% market share, supported by high-speed, cost-efficient, and versatile applications.

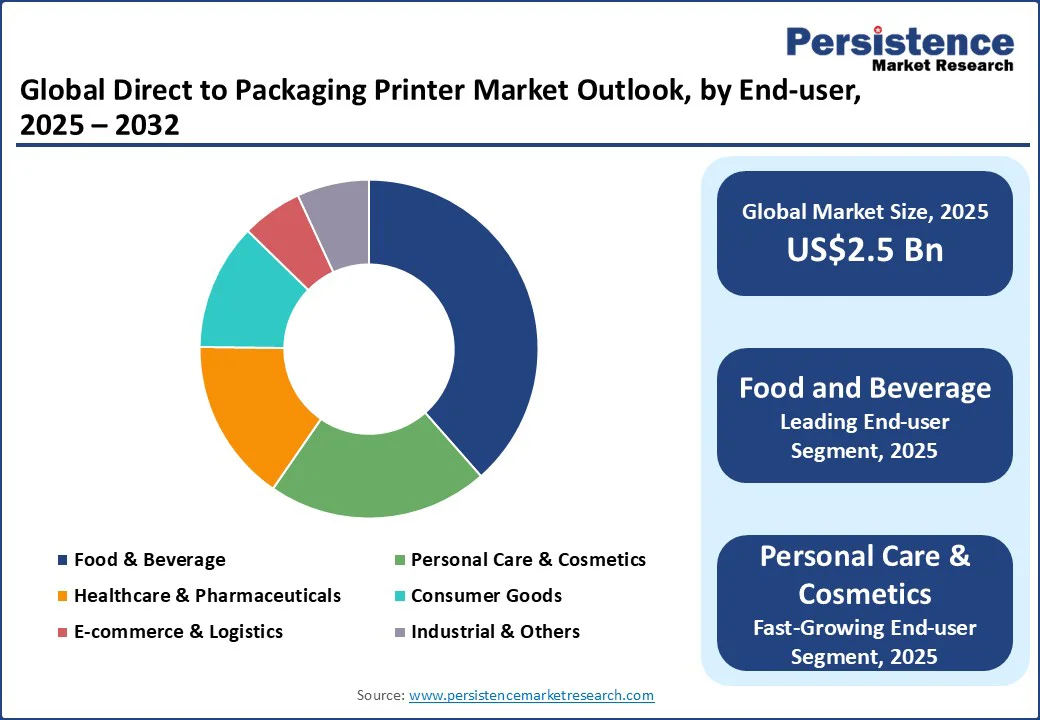

- Leading End-user: Food & beverage is anticipated to dominate with approximately 38.5% market share, while the personal care and cosmetics segment holds about 21.1%, driving premium packaging adoption.

- Innovations: Sustainability and eco-friendly printing with water-based inks and recyclable substrates are shaping the future of packaging production.

|

Global Market Attribute |

Details |

|

Market Size (2024A) |

US$2.3 Bn |

|

Estimated Market Size (2025E) |

US$2.5 Bn |

|

Projected Market Value (2032F) |

US$3.9 Bn |

|

Value CAGR (2025 to 2032) |

6.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Dynamics

Driver - Enhanced Customization Capabilities Across Flexible and Semi-Rigid Packaging

The consumer demand for personalized, on-demand, and short-run packaging solutions is driving the direct to packaging printer market growth of enhanced customization capabilities across flexible and semi-rigid packaging. Brands now focus on delivering differentiated packaging experiences that strengthen consumer engagement, while maintaining production efficiency and cost-effectiveness. Customization in flexible films, pouches, and semi-rigid boxes is becoming a critical factor for manufacturers aiming to meet evolving market expectations.

Technological advancements such as high-resolution UV direct-to-packaging printing, AI-driven positioning, and real-time variable data printing enable precise, short-run printing with vibrant CMYK color output. Developments such as AstroNova’s QuickLabel QL-425 and QL-435 systems provide compact digital inkjet solutions capable of handling medium to high-volume flexible packaging production while offering low total cost of ownership and industry-leading print quality. These innovations enable brands to create limited-edition releases, personalized seasonal packaging, and luxury rigid box designs, improving product visibility and consumer recall.

Innovations in ink chemistry also enhance customization across flexible packaging substrates. Linx Printing Technologies’ new plastic-film inks for OPP, BOPP, HDPE, and LDPE films improve adhesion, durability, and code readability on thin, flexible materials. PFAS-free and CMR-free eco-friendly formulations support sustainable production goals while enabling secure, traceable, and brand-compliant packaging. The ability to incorporate raised textures, spot gloss finishes, and anti-counterfeit features further strengthens packaging differentiation and aligns with regulatory compliance requirements.

Restraint - High Operational and Maintenance Costs for Advanced Printing Technologies

High operational and maintenance costs pose a significant challenge for the adoption of advanced direct-to-packaging printing technologies. Digital presses with UV curing units, precision inkjet heads, automated modules, and water-based or eco-friendly inks require a consistent power supply, routine servicing, and specialized consumables.

Rising industrial electricity rates in regions such as the U.S. and Europe, coupled with the need for continuous uptime, drive production expenses for converters and print service providers. Even innovative technologies such as single-pass digital presses or high-speed roll-to-roll systems, while increasing efficiency, cannot fully offset the high operational expenditures, particularly for smaller and mid-sized packaging businesses.

Maintenance demands further strain budgets, as skilled operators and technicians must manage complex digital systems, perform frequent technical inspections, and comply with environmental and safety regulations, including air emission controls and solvent recovery mandates. Advanced automation and AI-assisted positioning technologies improve productivity and precision, but they also require higher initial setup, calibration, and upkeep costs.

Opportunity - Expansion of Direct to Packaging Printing in E-Commerce and Logistics

The expansion of direct-to-packaging printing in e-commerce and logistics creates a significant growth opportunity as businesses increasingly demand sustainable, customizable, and on-demand packaging solutions. The surge in online shopping and fast-moving logistics requires systems that enhance operational efficiency while supporting brand differentiation. Digital printing technologies now enable zero-inventory workflows, high-speed production, and variable data printing, allowing companies to respond to dynamic order volumes without compromising sustainability or quality.

Technological advancements are also driving this shift. High-speed single-pass systems now achieve efficiency gains of over 300%, while supporting full-color CMYK printing across diverse substrates, eliminating the need for traditional platemaking. Integration of water-based inks and eco-conscious feed mechanisms reduces environmental impact and aligns with global ESG trends. Industry 4.0-ready solutions offer automated feeding, high-resolution output up to 1200 dpi, and flexible substrate handling, enabling businesses to produce short-run, customized packaging economically.

Trend - Emphasis on Sustainability and Eco-Friendly Printing

The shift toward sustainability and eco-friendly printing has emerged as a powerful trend in the direct to packaging printer market. Companies are prioritizing technologies that reduce environmental impact while maintaining high-quality outputs on a variety of substrates such as corrugated cardboard, paper bags, padded envelopes, and recyclable films. Advanced digital printing solutions now enable energy-efficient operations, waste minimization, and versatile medium-volume production, supporting brands in meeting both consumer expectations and regulatory requirements for environmentally responsible packaging.

Innovations such as single-pass printing, water-based UV inks, and LCA-enabled evaluation tools are driving measurable reductions in carbon footprint. Studies indicate that modern digital printing can lower global warming potential by nearly 50% compared to conventional analog methods, owing to plate-free printing, lower energy consumption, and just-in-time production capabilities.

Integration with recyclable films and eco-friendly substrates allows consistent performance in food and luxury packaging applications while maintaining operational efficiency. Intelligent print engines, automation, and cost-effective medium-volume production further strengthen the environmental and economic benefits of sustainable packaging printing.

Category-wise Analysis

Technology Insights

Inkjet printing is anticipated to lead the technology segment by holding a market share of approximately 53.4%, driven by packaging producers adopting high-speed and cost-efficient solutions for corrugated and labeling applications. EFI’s single-pass inkjet system achieves box production every few seconds while improving sustainability and reducing waste.

Agfa’s robotic automation with the Onset X3 HS boosts 24/7 productivity, and Roland DG’s flatbed inkjet printers expand direct-to-object applications, supporting versatile substrates from plastics to wood. Compact solutions from AstroNova also strengthen flexibility for small businesses and specialty packaging.

UV printing is expected to gain strong momentum with advances that combine cost efficiency, premium quality, and customization. Roland’s DGXPRESS printers address demand in growth markets, while its TrueVIS MG Series enables multilayer output that creates dimensional finishes for packaging prototypes.

Giftec’s breakthrough leather UV technology supports luxury and gift packaging by delivering wear-resistant, high-resolution effects with embossing and hot stamping. These innovations make UV printing a vital driver for brands seeking differentiated and value-added packaging.

End-user Insights

The food and beverage industry is expected to lead with a market share of approximately 38.5% in the direct to packaging printer market, driven by its scale and continuous innovation in packaging. Europe’s food and drink sector alone generates €1.2 Tn (US$1.29 Tn) in turnover, employing 4.7 million people, while the U.S. contributes over US$534 Bn to GDP with 3.5 million jobs.

Rising demand for sustainable packaging, combined with strong growth in beverage manufacturing and pet food, pushes producers to adopt efficient printing technologies that deliver cost savings, speed, and eco-friendly outcomes.

The personal care and cosmetics industry is likely to capture a significant market share of about 21.1%, fueled by premiumization, sustainability, and rising global demand. The sector is projected to generate US$646.2 Bn in revenue in 2024, with the U.S. contributing US$100 Bn and India emerging as a high-growth hub at US$31.5 Bn.

Shifting consumer preferences toward organic and plant-based products, alongside the surge of online channels contributing nearly 20% of global sales, create a growing need for customizable and high-quality packaging solutions that strengthen brand identity.

Regional Insights

East Asia Direct to Packaging Printer Market Trends

East Asia is projected to hold a substantial share of approximately 29% in the global direct-to-packaging printer landscape, led by China, Japan, and South Korea, driven by strong e-commerce growth and rising consumer demand. China’s online retail reached US$2.29 Tn in 2020 and is projected to hit US$3.56 Tn by 2024, supported by over 710 million digital buyers, creating high demand for short-run, personalized, and logistics-ready packaging solutions.

Japan and South Korea are accelerating technological innovation, with companies such as Mutoh introducing XpertJet 461UF and 661UF UV LED printers for small-lot production, packaging prototyping, and premium personalization. Advanced automation, high-resolution UV inks, and compact print engines enable medium-volume production with durable, eco-resilient finishes across diverse substrates for healthcare, cosmetics, and consumer goods packaging.

Cross-border e-commerce and global exports further strengthen the region, with South Korea’s healthcare and cosmetics exports reaching US$14.6 Bn and China’s retail sales hitting US$651 Bn in June 2025. Consumer-driven personalization, international branding needs, and smart packaging trends are driving the adoption of versatile, automated direct-to-packaging printer solutions, creating long-term opportunities for high-quality, short-run packaging across multiple end-use industries.

North America Direct to Packaging Printer Market Trends

North America is anticipated to holds a significant share of around 24% in the direct to packaging printer market, supported by a dynamic manufacturing base, a strong food and beverage industry, and rapid growth in e-commerce packaging applications.

The U.S. food and beverage sector contributed more than US$534.3 Bn to GDP in 2023, sustaining nearly 3.5 million jobs and recording a 10% employment growth over the last five years. Beverage manufacturing alone added over 63,000 new jobs, led by breweries and emerging categories such as pet food, underscoring the strong demand for customized and short-run packaging solutions. This demand aligns with the region’s need for flexible digital printing technologies that deliver high-quality, low-volume production across multiple substrates.

Technological advancements in direct-to-packaging printers, including high-performance inkjet and UV-based systems, enable medium-volume production with durable, eco-resilient finishes on corrugated boards, paper bags, and recyclable films. Automated print engines, water-based inks, and in-house UV varnishing reduce material waste and energy use while supporting high-mix prototyping across food, pharmaceutical, and hospitality packaging.

E-commerce growth further strengthens the region, with U.S. online retail sales reaching US$304 Bn in Q2 2025 and a logistics sector valued at US$2.3 Tn. Consumer-driven personalization, faster turnaround, and sustainable production practices are driving the adoption of versatile, automated digital printing technologies, creating long-term opportunities for high-quality, medium-volume packaging across multiple end-use industries.

Competitive Landscape

The global direct to packaging printer market is moderately fragmented, with global and regional players competing through technological advancements, sustainability-driven innovations, and customized solutions.

The market shows characteristics of a competitive oligopoly, where a few large companies dominate high-speed and industrial-scale packaging printing, while several emerging players focus on niche applications such as short-run, personalized, and eco-friendly packaging.

Manufacturers are primarily focusing on integrating digital single-pass and multi-pass technologies, water-based and UV ink systems, and automation to enhance production efficiency, sustainability, and customization. The trend indicates a strong shift toward eco-friendly substrates, on-demand printing, and Industry 4.0-ready solutions, which are shaping the future of direct-to-packaging printing.

In terms of future outlook, the market is expected to consolidate further as larger companies expand portfolios through strategic partnerships, acquisitions, and joint ventures, while smaller innovators cater to specialized needs such as direct-to-object printing, premium packaging, and smart packaging applications.

The growing importance of sustainability, variable data printing, and compliance-ready coding will drive long-term adoption across food & beverage, e-commerce, and healthcare packaging. Leading players such as EFI, Mutoh, Agfa-Gevaert, and AstroNova are currently setting benchmarks in terms of speed, scalability, and digital transformation, while regional entrants focus on disruptive, cost-efficient, and sustainable solutions to capture emerging demand.

Key Industry Developments

- In April 2025, Giftec launched a Single Pass packaging printer offering 300%+ higher efficiency with CMYK support on multiple substrates. Using HP printheads and eco-friendly water-based inks, it enables zero-inventory, variable data, and smart packaging, ideal for e-commerce, F&B, and logistics.

- In May 2025, AstroNova launched the VP-800 direct-to-package printer for medium-volume, eco-friendly printing on corrugated boxes, paper bags, envelopes, and wood. Featuring MTEX digital tech, it offers high-resolution output, automation, and reduced costs, ideal for short-run, sustainable packaging needs.

Companies Covered in Direct to Packaging Printer Market

- AstroNova, Inc.

- Labelgraff

- Mutoh Holdings Co., Ltd.

- OKI Electric Industry Co., Ltd.

- MTuTech (MeiTu Digital Industry Co., Ltd.)

- Roland DG Corporation

- Konica Minolta, Inc.

- Electronics For Imaging, Inc. (EFI)

- Mehta Hitech Industries Limited

- Linx Printing Technologies

- Shenzhen Giftec Technology Co., Ltd.

- Paul Leibinger GmbH & Co. KG

- Agfa-Gevaert Group

Frequently Asked Questions

The direct to packaging printer market is projected to be valued at US$2.5 Bn in 2025.

Inkjet Printing is expected to hold a 53.4% market share in 2025, driven by rising demand for high-quality, customizable, and efficient direct-to-packaging solutions.

The market is poised to witness a CAGR of 6.8% from 2025 to 2032.

Direct to packaging printer market growth is driven by enhanced customization for flexible packaging and high-quality printing for premium rigid packaging in personal care and cosmetics.

Opportunities include expanding direct-to-packaging printing in e-commerce and logistics, Short-run custom packaging, and integration of digital codes and smart features, which also offer growth potential.

Key players in the direct to packaging printer market include AstroNova, Inc., Labelgraff, Mutoh Holdings Co., Ltd., OKI Electric Industry Co., Ltd., MTuTech, Ltd., Roland DG Corporation, Konica Minolta, Inc., and Electronics For Imaging, Inc. (EFI).