- Chipsets & Processors

- Digital Signal Processor Market

Digital Signal Processor Market Size, Share, and Growth Forecast 2026 - 2033

Digital Signal Processor Market by Product Type (General Purpose DSP, Application-Specific DSP, DSP SoC), by Processing Type (Fixed-Point DSP, Floating-Point DSP), by Application (Consumer Electronics, Automotive, Telecom, Industrial, Aerospace & Defense, Healthcare, Computing & Data Centers, Others), and Regional Analysis, 2026 - 2033

Digital Signal Processor Market Size and Trend Analysis

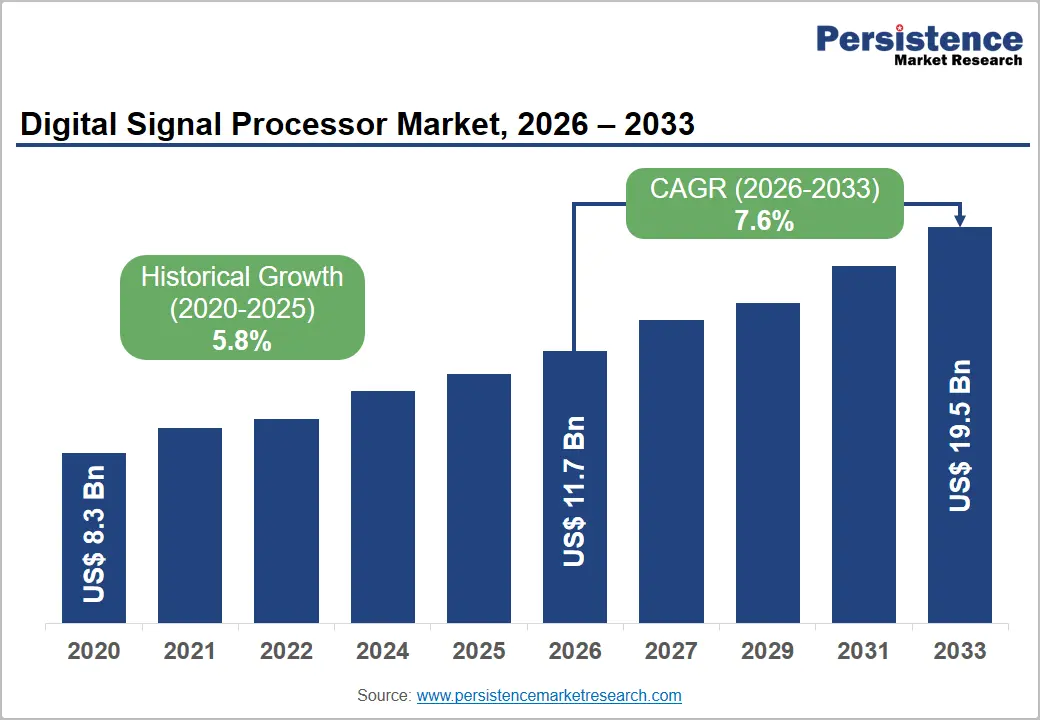

The global digital signal processor market is expected to be valued at US$ 11.7 billion in 2026 and is projected to reach US$ 19.5 billion, growing at a CAGR of 7.6% between 2026 and 2033.

The increasing deployment of AI-enabled edge computing applications, including always-on voice assistants, industrial automation systems, and advanced driver-assistance systems (ADAS), is transforming digital signal processors from conventional computing components into critical high-performance processing assets. Growing demand for real-time data processing, low-latency communication, and power-efficient computing across telecommunications, automotive, consumer electronics, and industrial sectors is further accelerating market expansion.

Key Industry Highlights:

- Leading Product Type: Application-Specific DSPs is dominant with nearly 43% share in 2026, valued at around US$ 5 Billion, driven by demand for highly optimized, low-latency, and power-efficient architectures in automotive ADAS, edge AI sensors, and intelligent audio systems.

- Leading Processing Type: Fixed-Point DSPs are likely to register over 55% share in 2026, valued at approximately US$ 6.43 Billion, driven by high-volume consumer electronics and telecom applications requiring cost-efficient and energy-optimized signal processing.

- Fast-Growing Processing Type: Floating-Point DSPs are expanding rapidly due to increasing adoption in aerospace, defence, scientific computing, and advanced communication systems requiring high numerical precision and algorithmic flexibility.

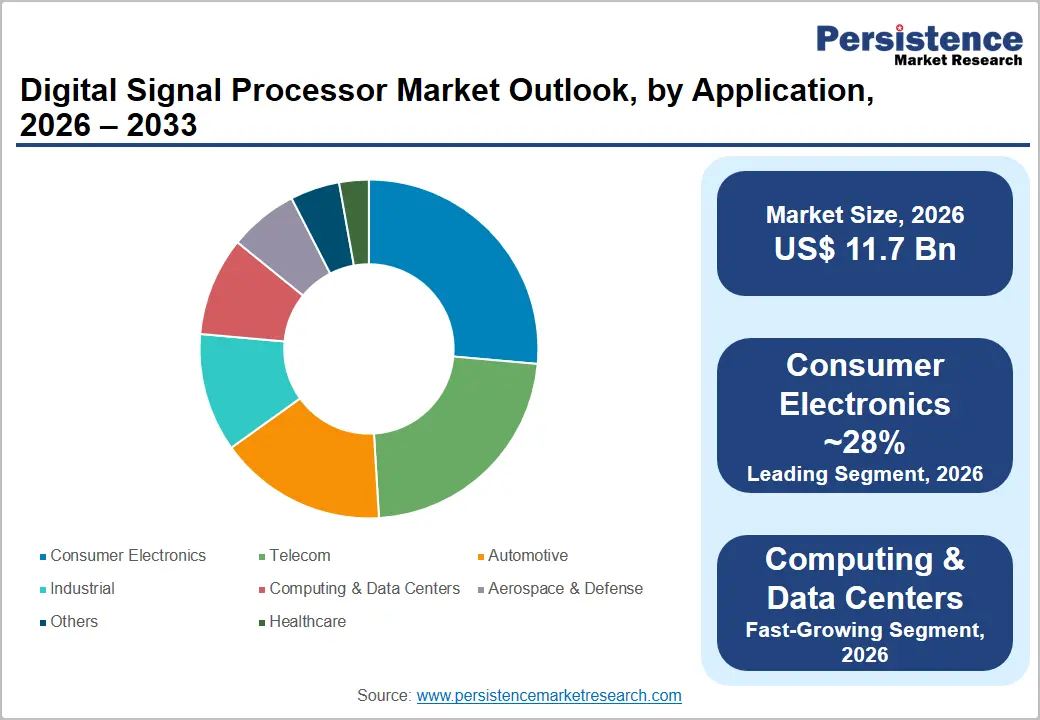

- Leading Application: Consumer electronics is likely to account for over 28% share in 2026, valued at around US$ 3.28 Billion, driven by computational photography, voice recognition, active noise cancellation, and immersive multimedia experiences.

- Fast-Growing Application: Computing & Data Centers is the fastest-growing segment, fuelled by hyperscale expansion, AI workloads, and transition to 400G/800G networking architectures requiring advanced DSP-enabled signal processing.

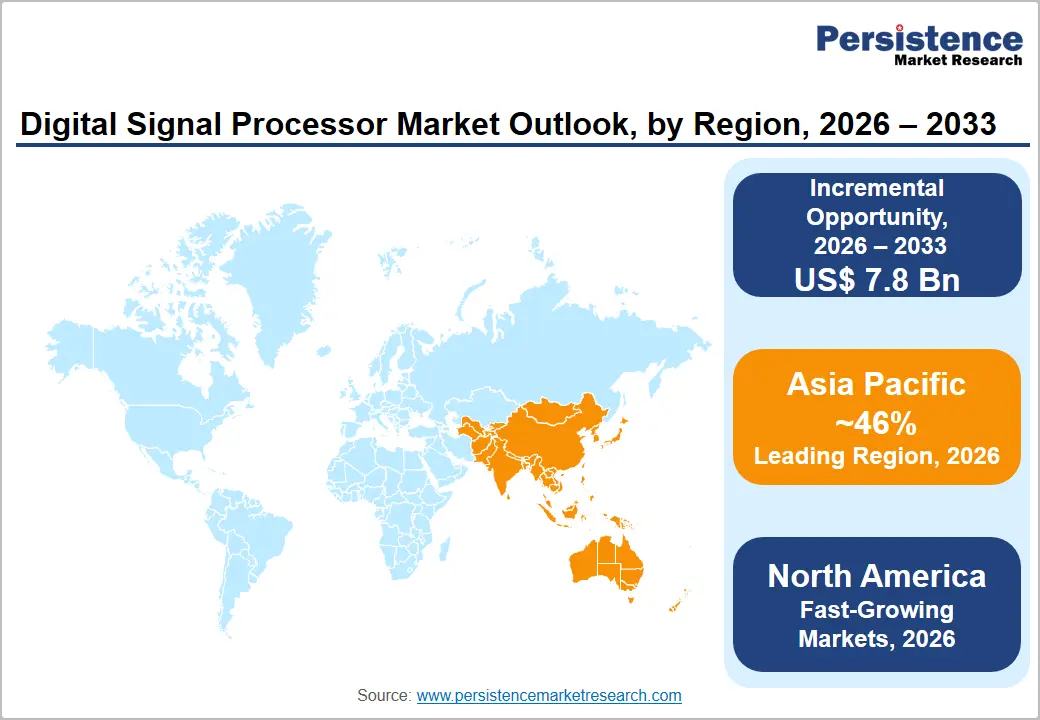

- Leading Region: Asia Pacific is dominant with 46% share in 2026, valued at US$ 5.38 billion, supported by large-scale electronics manufacturing, 5G rollout, and semiconductor localisation initiatives.

Market Dynamics

Drivers - Rise in 5G Infrastructure Deployment Driving Baseband DSP Procurement

The rapid deployment of 5G Radio Access Network (RAN) infrastructure is significantly increasing demand for high-performance digital signal processors capable of handling massive MIMO, beamforming, and real-time baseband processing workloads. According to the Ericsson, global 5G subscriptions are expected to exceed 6.4 billion by 2031, accelerating investments in advanced telecom network equipment.

Semiconductor companies such as Qualcomm Technologies are integrating AI-enabled DSP architectures into commercial 5G modem chipsets to improve spectral efficiency and network throughput. As telecom operators increasingly migrate toward standalone 5G architectures through 2026-2028, demand for next-generation DSP SoCs optimized for low-latency signal processing is expected to rise substantially.

Automotive ADAS and In-Cabin Signal Processing Mandates Accelerating Design Wins

Growing regulatory requirements for vehicle safety systems are accelerating the adoption of DSP-enabled automotive processors across radar, LiDAR, camera, and sensor-fusion applications. The European Union’s General Safety Regulation (EU) 2019/2144 mandated technologies such as autonomous emergency braking and lane-keeping assistance for new vehicle type approvals beginning in July 2024. Companies, including NXP Semiconductors, expanded their automotive processing portfolios to address increasing ADAS computational workloads.

Additionally, China’s evolving automotive safety standards under GB 7258 revisions are expected to further strengthen demand for high-performance automotive DSP solutions through 2027, particularly in connected and semi-autonomous vehicle platforms.

Restraints - Semiconductor Supply Chain Concentration and Geopolitical Export Controls Compressing Margins

The DSP industry remains heavily dependent on advanced semiconductor foundries such as Taiwan Semiconductor Manufacturing Company and Samsung Electronics for leading-edge manufacturing nodes below 7nm. This concentration exposes semiconductor vendors to supply-chain disruptions, wafer pricing volatility, and extended production lead times during geopolitical tensions or capacity shortages. Expanded export control measures introduced by the U.S. Bureau of Industry and Security increased licensing and compliance requirements for semiconductor design tools and advanced IP transfers involving certain Chinese entities. These restrictions are increasing operational complexity and slowing cross-border semiconductor collaboration activities.

High Non-Recurring Engineering Costs Constraining Custom Development

Developing application-specific DSP architectures at advanced semiconductor nodes requires substantial non-recurring engineering (NRE) investment covering chip design, verification, software integration, and mask production. According to a study, advanced-node chip development costs at 5nm can exceed US$ 500 million for highly complex designs. Such elevated development costs limit full-custom DSP innovation primarily to large semiconductor companies with extensive R&D budgets. Many mid-sized vendors increasingly rely on licensed DSP IP cores from companies such as Cadence Design Systems and Synopsys to reduce risk and accelerate product commercialization.

Opportunities - AI-at-the-Edge Deployment Creates a Greenfield DSP Upgrade Cycle

The rapid expansion of AI-at-the-edge applications is creating significant growth opportunities for DSP vendors focused on low-power inference acceleration and real-time signal processing. Industrial automation systems, smart cameras, IoT devices, and consumer electronics increasingly require localized AI computation to reduce latency and cloud dependency. In 2023, Analog Devices introduced enhanced SHARC+ DSP solutions targeting industrial edge AI workloads with improved MAC throughput and energy efficiency. As demand for battery-powered intelligent edge devices grows, DSP architectures capable of operating below 1W power consumption are expected to gain stronger adoption across embedded AI applications.

Healthcare Wearables and Implantable Devices Expanding DSP Demand

The growing adoption of wearable health monitoring systems, hearing aids, and implantable medical devices is increasing demand for ultra-low-power DSP technologies capable of processing ECG, EEG, and PPG biosignals in real time. Regulatory initiatives such as the U.S. FDA Safety and Landmark Advancements (FDASLA) Act of 2022 have streamlined approval pathways for several digital health and remote monitoring solutions, accelerating commercialization across the medical electronics industry. Healthcare OEMs are also increasingly emphasizing ISO 13485 compliance, long product lifecycles, and supply-chain traceability to satisfy EU Medical Device Regulation (MDR) requirements. DSP vendors offering medically certified, power-efficient, and highly reliable processing platforms are expected to benefit from expanding healthcare digitization trends.

Category-wise Analysis

Product Type Insights

Application-specific DSP commands nearly 43% of the global digital signal processor market in 2026, equivalent to US$ 5 Billion, due to industries requiring highly optimized processors tailored for dedicated workloads where latency, power efficiency, and reliability are critical. These processors reduce unnecessary compute overhead and improve real-time execution efficiency compared to general-purpose architectures. The growing adoption of advanced driver-assistance systems, edge AI sensors, and intelligent audio devices is further strengthening demand for application-specific DSP deployments.

DSP SoC is the fast-growing segment, supported by rising demand for compact, integrated semiconductor platforms capable of combining signal processing, connectivity, sensor control, and power management on a single chip. IoT devices, smart wearables, industrial sensors, and portable consumer electronics increasingly require low-cost and energy-efficient architectures that minimize board space and component count. Integrated DSP SoCs help manufacturers reduce bill-of-material costs while improving battery life and system reliability.

The expansion of NB-IoT, smart metering, asset tracking, and connected healthcare devices is accelerating the adoption of highly integrated DSP-based SoCs across large-scale deployments.

Processing Type Insights

Fixed-point DSP accounts for over 55% share in 2026, surpassing the value of US$ 6.43 billion, due to its strong suitability for high-volume, power-sensitive electronics and communication systems. Consumer devices rely heavily on fixed-point architectures because they deliver efficient signal processing with lower silicon complexity and reduced energy consumption. These DSPs are widely preferred in applications where predictable arithmetic precision and low manufacturing costs are more important than extreme computational flexibility. The growing shipment volumes of battery-powered electronics globally are sustaining long-term demand for cost-efficient fixed-point processing architectures.

Floating-Point DSP is the fastest-growing processing type, due to increasing demand for high-precision computation in advanced communications, aerospace, defense, scientific instrumentation, and imaging systems. It improves numerical accuracy, reduces signal distortion, and simplifies algorithm development for highly sophisticated workloads. Defense modernization programmes and investments in high-frequency communication infrastructure are further accelerating the adoption of floating-point processing platforms globally. As next-generation sensing and real-time analytics systems become more computationally intensive, industries are increasingly prioritising floating-point DSP capabilities despite their higher power and cost profiles.

Application Analysis

Consumer electronics are likely to register more than 28% share in 2026, reaching over US$3.28 billion. DSPs are essential for enabling computational photography, voice recognition, active noise cancellation, spatial audio, and augmented multimedia experiences without overloading central processors. The increasing consumer preference for AI-enhanced features and premium media performance is driving higher DSP integration per device generation. Manufacturers are also prioritising DSP adoption to improve battery efficiency while maintaining high-performance multimedia processing.

Computing & data centers is the fast-growing application segment, fuelled by hyperscale infrastructure expansion and the rising complexity of high-speed networking and AI workloads. Modern data centres increasingly require DSP-enabled accelerators for optical interconnect processing, network signal conditioning, workload optimization, and low-latency data transmission. The transition toward 400G and 800G networking architectures is significantly increasing DSP content within servers, switches, and optical modules to maintain signal integrity and bandwidth efficiency.

Cloud providers and AI infrastructure operators are also deploying DSP-supported accelerators to improve inference throughput and reduce processing bottlenecks in large-scale computing environments.

Regional Insights

North America Digital Signal Processor Market Trends and Insights

North America holds over 26.0% of the global digital signal processor market in 2026, reaching US$ 3.04 Billion, supported by the region’s strong concentration of fabless semiconductor companies, defence electronics contractors, and hyperscale cloud infrastructure providers that collectively sustain large-scale DSP deployment. Growing investments in AI-enabled edge computing, 5G infrastructure, aerospace electronics, and advanced radar systems are accelerating demand for high-performance and low-latency signal processing solutions across the region. The region is also witnessing rising integration of DSPs within AI accelerators, data centre networking equipment, and industrial automation systems, further expanding long-term market opportunities.

The U.S. digital signal processor market is expected to surpass the value of US$2.62 billion in 2026, driven by the presence of globally leading semiconductor innovators including Texas Instruments, Qualcomm, and Analog Devices, alongside one of the world’s largest defence electronics procurement ecosystems. Strong federal initiatives such as the Department of Defense Microelectronics Commons programme launched under the CHIPS and Science Act framework are accelerating investment into trusted domestic DSP manufacturing and advanced semiconductor R&D capabilities. This initiative is expected to reduce dependency on foreign semiconductor supply chains while supporting secure design-to-manufacturing integration for mission-critical signal processing hardware.

Europe Digital Signal Processor Market Trends and Insights

Europe digital signal processor market value is expected to reach over US$1.99 billion by 2026, supported by strong automotive electronics production, industrial automation upgrades, and rising defence modernization spending across NATO member states. The demand is being reinforced by advanced driver-assistance systems (ADAS), vehicle electrification, and 5G communication infrastructure requiring high-speed real-time signal processing capabilities. The European Chips Act is further accelerating semiconductor investments aimed at expanding Europe’s share in global semiconductor production by 2030, which is expected to strengthen local DSP manufacturing and reduce supply chain dependence on Asian suppliers.

Germany digital signal processor market value is expected to surpass US$ 460 million in 2026, driven by the country’s dominant automotive supply chain led by companies such as Continental AG, ZF Friedrichshafen, and HELLA, which integrate DSPs into radar, lidar, infotainment, and V2X communication systems. France growth is supported by avionics and defence electronics demand from Thales Group and semiconductor innovation activities led by STMicroelectronics. The United Kingdom captures over 16.0% share, with DSP procurement anchored by aerospace and defence programs from BAE Systems and Rolls-Royce, alongside expanding Open RAN and telecom infrastructure deployments by British network operators.

Italy’s Industry 4.0 incentives and participation in the European Defence Fund are supporting adoption of DSP-enabled motion-control, radar, and electronic warfare systems, particularly through programs associated with Leonardo S.p.A.. The Rest of Europe segment holds over 26.0% share, reaching US$ 520 million, supported by Nordic telecommunications equipment manufacturing, Dutch semiconductor equipment ecosystems, and expanding Eastern European defence electronics procurement.

Telecom leaders such as Ericsson and Nokia continue driving high-volume DSP demand for 5G baseband infrastructure, while increased NATO interoperability investments across the Baltic and Eastern European region are accelerating procurement of defence-grade DSP platforms.

Asia Pacific Digital Signal Processor Market Trends and Insights

Asia Pacific holds over 46.0% of the global digital signal processor market in 2026, reaching US$ 5.38 billion, while advancing at the fastest regional CAGR of 11.5% through the forecast period. The region’s dominance is structurally supported by its position as the manufacturing and export hub for more than three-fourths of global consumer electronics production, alongside accelerating semiconductor localisation initiatives across China, South Korea, Japan, and India. Rising deployment of 5G infrastructure, AI-enabled edge devices, automotive electronics, and industrial automation systems continues to reinforce long-term DSP demand across the Asia Pacific.

China Digital Signal Processor Market Trends

China holds over 45.0% of the Asia Pacific digital signal processor market in 2026, surpassing US$ 2.42 billion, supported by aggressive 5G infrastructure expansion and domestic semiconductor self-sufficiency initiatives under the Made in China 2025 framework. The country’s expanding base station ecosystem and state-backed semiconductor funding programmes are accelerating indigenous DSP development for telecom and AI workloads.

Japan Digital Signal Processor Market Insights

Japan's market value is expected to reach over US$ 860 million, driven by demand from automotive electronics, factory automation, and high-precision industrial equipment manufacturers, while continued investment in advanced semiconductor manufacturing strengthens domestic DSP innovation capabilities.

India Digital Signal Processor Market Trends

India digital signal processor market is expected to achieve a CAGR of 15.2%, propelled by rapid 5G rollout, expanding electronics manufacturing capacity, and increasing semiconductor assembly and testing investments. Government incentives and strategic collaborations with global semiconductor companies are gradually positioning India as an emerging DSP supply chain destination. Southeast Asia's growth is supported by semiconductor back-end manufacturing expansion in Malaysia, Vietnam, and Thailand as global companies diversify production beyond China.

Increasing telecom network modernization, coupled with rising consumer electronics assembly activity across the region, continues to generate sustained demand for DSP components in communication, computing, and industrial applications.

Competitive Landscape

The global digital signal processor market exhibits a moderately concentrated competitive structure, with a limited number of large semiconductor vendors accounting for a significant share of industry revenue. Companies are focusing on strengthening software development ecosystems, enhancing DSP compiler tool chains, and expanding co-design capabilities with OEM customers to improve performance efficiency and product integration. Also prioritizing heterogeneous system-on-chip architectures that combine CPU, GPU, AI accelerator, and DSP functionalities within a single platform, thereby reshaping traditional DSP market positioning.

Key Developments:

- In March 2026: Vokon, a China-based commercial audio amplifier manufacturer, will showcase its next-generation DSP-powered audio solutions at ISLE 2026. The company’s technology integrates digital signal processing to enhance real-time sound control, including features like noise reduction and audio optimization.

- In March 2026: Broadcom completed development of its 400G-per-lane PAM4 optical digital signal processor (DSP) targeting next-generation 1.6T and 3.2T data center interconnects, with mass production planned for 2027. The chip is designed for high-speed AI and hyperscale data center networking, enabling higher bandwidth and more efficient optical communications.

Companies Covered in Digital Signal Processor Market

- Texas Instruments

- Analog Devices

- Qualcomm Technologies

- NXP Semiconductors

- STMicroelectronics

- Infineon Technologies

- Intel Corporation

- AMD (Xilinx)

- Broadcom Inc.

- Renesas Electronics

- Microchip Technology

- MediaTek

- Marvell Technology

- Cadence Design Systems

- Others

Frequently Asked Questions

The global digital signal processor market is valued at US$ 11.7 Billion in 2026 and is projected to reach US$ 19.5 Billion, growing at a CAGR of 7.6%, due to expanding 5G deployment, AI-enabled edge devices, and rising automotive electronics demand.

The market is primarily driven by increasing adoption of ADAS systems, rapid 5G infrastructure expansion, and rising data centre traffic requiring high-speed signal processing

Application-Specific DSP holds the largest market share at 43.0% due to its superior efficiency in automotive radar, medical devices, and hearing instruments. Long qualification cycles and high design complexity further strengthen supplier retention in this segment.

Asia Pacific dominates the market with an over 46.0% revenue share in 2026, supported by strong electronics manufacturing and rapid 5G infrastructure deployment in China, Japan, South Korea, and India. Government semiconductor initiatives are further boosting regional growth.

Major opportunities are emerging in healthcare wearables, implantable medical devices, and ultra-low-power biosignal monitoring applications. Increasing regulatory support and demand for energy-efficient processing solutions are expected to create strong long-term growth potential.

The leading companies include Texas Instruments, Analog Devices, Qualcomm Technologies, NXP Semiconductors, STMicroelectronics, Infineon Technologies, Intel Corporation among others.