- Specialty & Fine Chemicals

- Detergent Alcohol Market

Detergent Alcohol Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Detergent Alcohol Market by Source (Natural, Synthetic), Application (Laundry, Dishwashing, Lubricant Additives, Personal Care & Cosmetics, Industrial Cleaners, Other), and Regional Analysis for 2025-2032

Detergent Alcohol Market Size and Trend Analysis

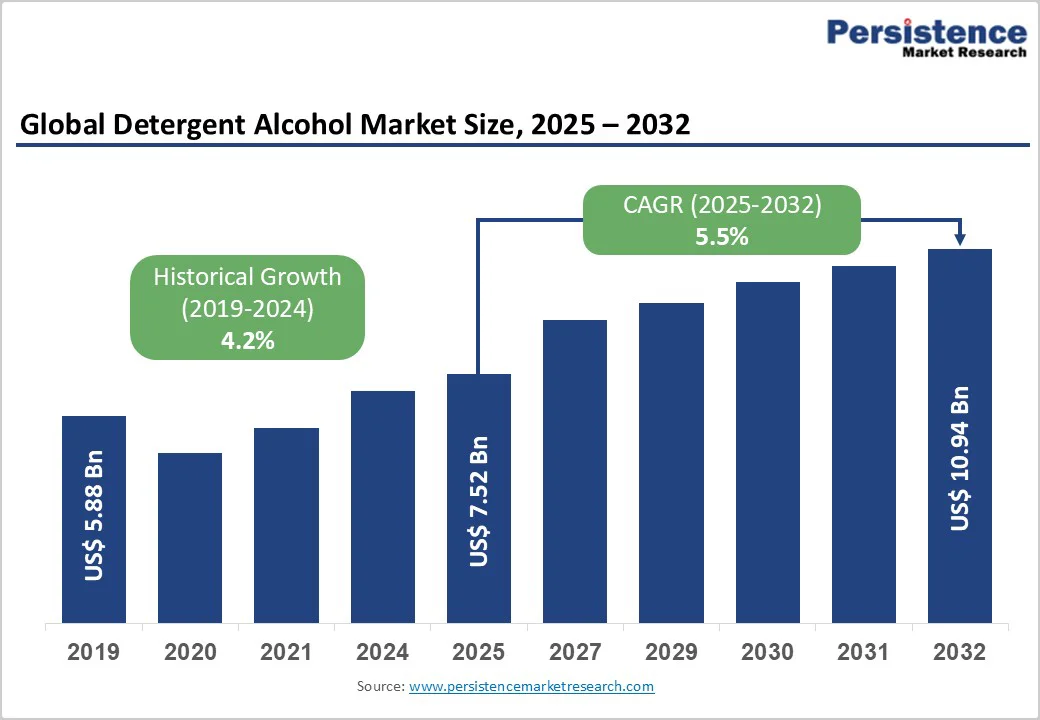

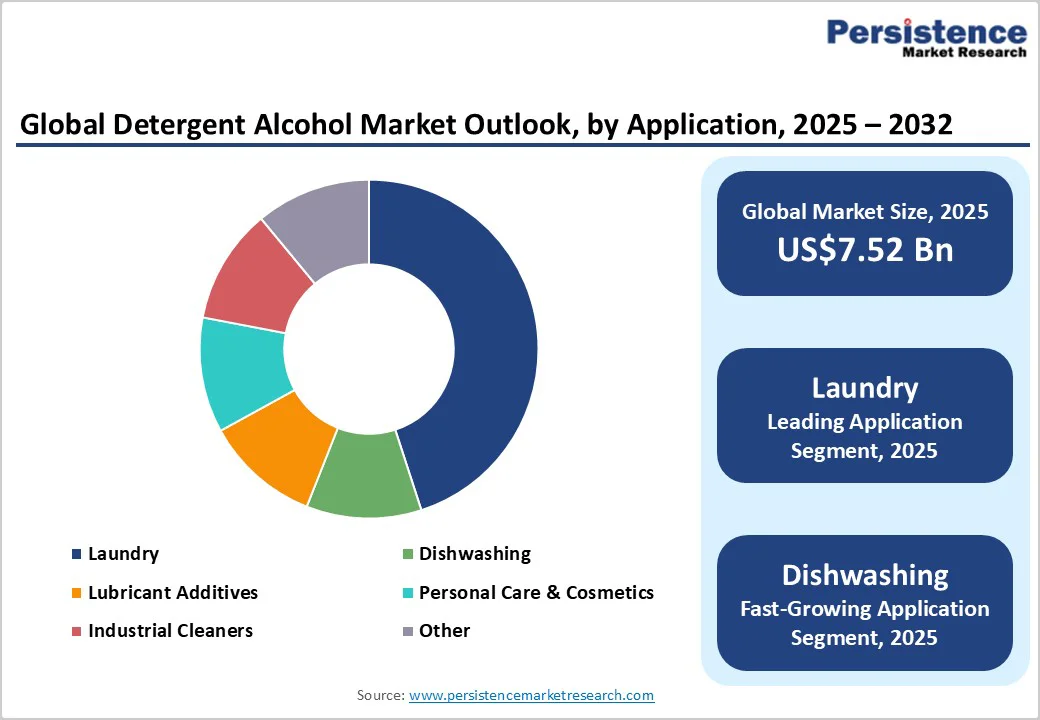

The global detergent alcohol market size is valued at US$7.5 billion in 2025 and is projected to reach US$10.9 billion, growing at a CAGR of 5.5% between 2025 and 2032. The market expansion is fundamentally driven by escalating demand for cleaning and hygiene products in both household and industrial sectors, coupled with a decisive shift toward environmentally sustainable formulations. Rising consumer awareness regarding the environmental impact of petrochemical-based products, combined with stringent regulatory frameworks in developed nations, has catalyzed the adoption of bio-based detergent alcohols derived from renewable feedstocks such as palm oil, coconut oil, and tallow.

Key Market Highlights:

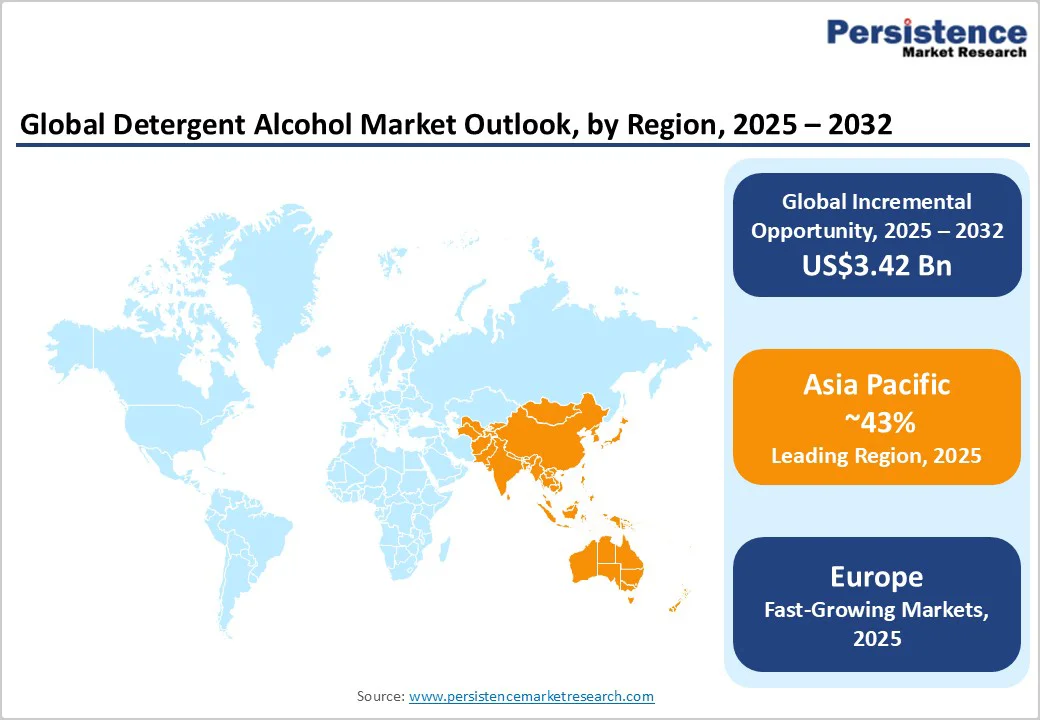

- Regional Leader: Asia Pacific commands the Detergent Alcohol Market leadership, with 43% of the market share, due to manufacturing hubs and high consumption in laundry segments, driving regional dominance.

- Fastest Growing Region: Europe emerges as the fastest-growing region, propelled by stringent eco-regulations and bio-based innovations.

- Leading Segment: The synthetic source segment prevails, capturing 70% share with cost-effective scalability for industrial uses.

- Fastest Growing Region: Laundry application grows quickest, fueled by hygiene trends and a high demand surge in households.

- Growth Opportunities: Bio-based technological advancements offer key opportunities, enabling 30% cost reductions in sustainable formulations.

| Report Attribute | Details |

|---|---|

|

Detergent Alcohol Market Size (2025E) |

US$7.5 Bn |

|

Market Value Forecast (2032F) |

US$10.9 Bn |

|

Projected Growth CAGR (2025-2032) |

5.5% |

|

Historical Market Growth (2019-2024) |

4.2% |

Market Dynamics

Drivers -

Rising Demand for Sustainable Cleaning Products

The shift toward eco-friendly cleaning solutions is a major growth driver for the Detergent Alcohol Market, propelled by increasing consumer preference for biodegradable and natural ingredients. European Union regulations under Regulation (EC) No. 648/2004 mandate comprehensive biodegradability testing for surfactants used in detergents, compelling manufacturers to reformulate products using renewable fatty alcohols. In November 2024, BASF announced a transformational collaboration with Acies Bio to develop methanol-based fermentation technology for producing fatty alcohols from captured CO?, marking a significant advancement in sustainable surfactant manufacturing.

As such, regulations emphasize sustainability, and companies adopting these practices gain a competitive edge, fostering market expansion through innovation and consumer trust. The integration with related sectors, such as the Natural and Organic Personal Care Market, further accelerates this driver by aligning with broader wellness trends.

Restraints -

Volatility in Raw Material Prices

Detergent alcohol production faces persistent challenges from fluctuating prices of natural feedstocks, including palm oil, coconut oil, and tallow, which are susceptible to weather conditions, agricultural practices, and global supply-demand dynamics. In April 2025, two major fatty alcohol plants in Selangor, Malaysia, Edenor Technology's 80,000 tonne/year facility and KLK OLEO's 300,000 tonne/year plant, experienced unplanned outages due to a gas pipeline fire that disrupted natural gas supply to 192 plants across the region. Such infrastructure vulnerabilities create supply constraints that ripple through global surfactant supply chains, affecting price stability and availability.

The palm oil prices, a primary input, rose by 12% in 2022 due to supply chain disruptions in major producers like Indonesia, leading to higher detergent alcohol costs and reduced affordability in price-sensitive markets. The raw material price instability directly impacts manufacturing costs, forcing producers to either absorb margin pressures or transfer costs to downstream customers, potentially constraining market expansion in price-sensitive segments.

Stringent Environmental Regulations

Regulatory hurdles, including bans on non-biodegradable surfactants, limit market growth by complicating compliance for synthetic detergent alcohols. The EPA in the U.S. and EU REACH frameworks have imposed stricter limits since 2020, resulting in a 15% increase in compliance costs for producers, delaying product launches and innovation. These rules favor bio-based options but burden traditional manufacturers, transitioning slowly, particularly in regions with fragmented enforcement.

The European Union's Detergent Regulation (EC) No. 648/2004 establishes comprehensive rules for placing detergents and surfactants on the market, requiring two-tier biodegradability testing regimes covering anionic, non-ionic, cationic, and amphoteric surfactants. Products containing surfactants that fail to meet specified biodegradability thresholds cannot be marketed in the EU, necessitating significant research and development investments in reformulation. The Intertek testing protocols for compliance involve extensive laboratory assessments of ultimate biodegradability, toxicity assessments, and environmental impact evaluations, substantially increasing time-to-market and development costs.

Opportunities -

Advancements in Bio-Based Technologies

The development of advanced bio-based detergent alcohols presents a prime opportunity, targeting the fastest-growing personal care and bio-lubricants market segments. Innovations in fermentation and enzymatic processes from renewable feedstocks like algae and waste oils could reduce production costs by 30% by 2030, meeting rising demand for sustainable lubricants and cleaners.

With global sustainability policies, such as the UN Sustainable Development Goals, supporting green chemistry, companies investing here can capture premium pricing in eco-conscious markets. Emery Oleochemicals expanded its 100% certified biobased portfolio in October 2024 by introducing four pelargonic acid products certified under the USDA BioPreferred® Program, targeting applications in lubricant base stocks, metalworking fluids, and corrosion inhibitors.

Emerging Markets in Asia-Pacific

Rapid industrialization in the Asia-Pacific offers substantial opportunities, especially in the laundry and industrial cleaners segments, driven by manufacturing booms in China and India. Government initiatives like India's Make in India campaign have spurred a 7% annual growth in chemical production since 2022, creating demand for cost-effective detergent alcohols in exports. With urbanization rates projected at 50% by 2030, household applications will expand, allowing firms to localize production and reduce import dependencies.

This region's advantages in feedstock availability further enable scalable bio-alcohol development, promising significant market penetration. Per capita detergent consumption in India remains at approximately 2.7 kg per year, significantly below the Philippines and Malaysia at 3.7 kg and the U.S. at nearly 10 kg, indicating substantial growth potential.

Category-wise Insights

Source Analysis

The synthetic segment leads the Source category in the Detergent Alcohol Market with a 70% market share, attributed to its cost-effectiveness and scalability in large-scale production. Synthetic fatty alcohols are primarily manufactured through petrochemical routes using isopropanol and ethanol as feedstocks, offering advantages in terms of supply chain reliability and production economics. Major facilities in South Africa, Europe, and Asia have established large-scale synthetic alcohol production infrastructure, enabling manufacturers to meet high-volume demand from industrial cleaning and detergent sectors. This dominance persists in industrial settings, where performance uniformity is critical, though a gradual shift toward naturals is emerging.

The natural source segment is experiencing accelerated growth momentum fueled by sustainability imperatives and regulatory pressures favoring bio-based ingredients. Natural detergent alcohols derived from oils, fats, and waxes offer superior biodegradability profiles and lower carbon footprints. KLK OLEO, recognized as one of the world's largest natural fatty alcohol producers, manufactures PALMEROL Fatty Alcohols with a 100% vegetable oil base from renewable resources, specifically targeting household detergent applications.

Application Analysis

In the application category, the laundry segment dominates with a 45% share, driven by its essential role in surfactant production for everyday cleaning. Detergent alcohols function as critical precursors in surfactant synthesis, delivering essential emulsifying, foaming, and degreasing properties that define cleaning performance in laundry formulations, with global consumption rising 11% post-2020 hygiene pushes.

The segment's dominance is reinforced by structural shifts toward high-efficiency liquid detergents, particularly in developed markets of North America and Europe, where automatic washing machine penetration exceeds 70% of households. Rapid urbanization across emerging economies has exponentially increased washing machine penetration and per capita consumption of laundry detergents, particularly liquid formulations. The segment's integration with the dishwashing additives market highlights its broad influence on cleaning formulations.

Regional Insights

North America Detergent Alcohol Market Trends

North America exhibits robust trends in the Detergent Alcohol Market, led by the U.S.'s innovation ecosystem and stringent regulatory framework. In the United States, approximately half of the states have enacted phosphate restriction legislation, with certain states, including Massachusetts, Oregon, and Washington, implementing bans on detergents containing more than 0.5% phosphate.

Innovation hubs in the region foster advancements, such as bio-alcohol patents filed by U.S. firms, enhancing efficiency in personal care applications. Procter & Gamble, headquartered in Cincinnati, Ohio, has committed to achieving net-zero greenhouse gas emissions across its supply chain by 2040, actively developing sulfate-free surfactant compositions using C12/C14 and C16/C18 alkyl chains in liquid dishwashing agents and detergents. This positions North America as a leader in quality-driven growth, balancing compliance with high-performance needs.

Europe Detergent Alcohol Market Trends

Europe represents the fastest-growing regional market, driven primarily by stringent environmental regulations and aggressive development of bio-based detergent alcohol production technologies. The European Union's Detergent Regulation (EC) No. 648/2004 imposes comprehensive biodegradability requirements for surfactants, creating regulatory pull for natural fatty alcohols that demonstrate superior environmental profiles compared to petrochemical alternatives. Germany, the U.K., France, and Spain lead regional demand, with established manufacturing infrastructure and strong consumer preference for certified sustainable products.

European companies are investing substantially in fermentation-based production routes for fatty alcohols from renewable methanol. In November 2024, BASF's Care Chemicals division partnered with Acies Bio, a leading European biotechnology company, to develop transformational fermentation technology utilizing captured CO? as a carbon source for fatty alcohol production. This collaboration aims to produce key surfactant building blocks for home-care and personal-care products through more sustainable pathways, with initial rollout planned in Europe before expansion into broader personal care applications.

Asia Pacific Detergent Alcohol Trends

Asia Pacific holds the largest market share at approximately 43%, representing the most dynamic growth region driven by China, Japan, India, and ASEAN nations' manufacturing advantages and burgeoning consumer markets. China's domestic detergent alcohol production capacity, combined with its position as a global manufacturing center for cleaning and personal care products, establishes the nation as both a major consumption market and a significant production hub for regional distribution.

Government initiatives, including the Swachh Bharat Mission, have elevated sanitation awareness and accelerated penetration of commercial cleaning products across institutional and industrial sectors. Japan emphasizes high-tech bio-alcohols, while ASEAN benefits from palm oil abundance. These dynamics, including the Detergent Chemicals Market ties, position the Asia Pacific for sustained dominance.

Competitive Landscape

The global detergent alcohol market features a consolidated structure, with top players controlling over 60% of supply through vertical integration and R&D investments. Leading manufacturers pursue vertical integration strategies, controlling feedstock sourcing through sustainable palm oil and coconut oil supply chains to mitigate raw material price volatility. Strategic partnerships between chemical majors and biotechnology innovators characterize recent competitive dynamics, exemplified by BASF-Acies Bio collaboration for fermentation-based production routes. Companies differentiate through sustainability certifications, including RSPO (Roundtable on Sustainable Palm Oil) and USDA BioPreferred® designations, which command premium positioning in environmentally conscious markets.

Key Market Developments

- August 2025: Univar Solutions Inc. and BASF SE expanded their distribution partnership in North America, with Univar Solutions appointed as the exclusive distributor for select BASF specialty ingredients, including polyalcohols and related products, enhancing supply security and technical support capabilities for industrial customers.

- November 2024: Sasol Limited launched NACOL 18-98, a palm-free biobased stearyl alcohol solution derived from rapeseed oil, providing high-performance sustainable packaging applications while addressing environmental concerns associated with palm oil production.

- October 2024: Emery Oleochemicals expanded its 100% certified biobased portfolio by introducing four pelargonic acid products certified under the USDA BioPreferred® Program, targeting applications in lubricant base stocks, metalworking fluids, corrosion inhibitors, and industrial cleaning.

Top Companies in the Detergent Alcohol Market

Sasol Limited (South Africa) leads with strong petrochemical expertise, generating significant revenue from synthetic alcohols and investing heavily in green transitions, holding a mature portfolio in industrial applications.

Kao Corporation (Japan) excels in innovation, particularly natural sources for personal care, with influential R&D yielding biodegradable products and a robust Asian presence.

BASF SE (Germany) dominates through diversified offerings, leveraging global scale for both synthetic and bio-alcohols, emphasizing sustainability to strengthen market influence.

Companies Covered in Detergent Alcohol Market

- Sasol Limited

- Kao Corporation

- VVF Ltd.

- KLK Oleo

- Emery Oleochemicals

- Univar Solutions Inc.

- Kepong Berhad (KLK) Oleo

- Wilmar International Ltd

- Royal Dutch Shell plc

- BASF SE

- SABIC

- Godrej Industries

- Procter & Gamble

- Ecogreen Oleochemicals

Frequently Asked Questions

The market is valued at US$7.5 Bn in 2025 and expected to reach US$10.9 Bn by 2032, reflecting steady growth.

Hygiene awareness and urbanization drive demand in cleaning products, boosting alcohol usage in surfactants.

The synthetic segment leads with a 70% share, due to its scalability and cost advantages in production.

Asia Pacific leads, driven by manufacturing in China and India, capturing the largest consumption share.

Advancements in bio-based technologies offer potential, reducing costs and aligning with sustainability policies.

Major players include Sasol Limited, Kao Corporation, and BASF SE, leading through innovation and global supply.