- Medical Devices

- Dental Lasers Market

Dental Lasers Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Dental Lasers Market by Product (Dental Surgical Lasers, and Dental Welding Lasers), by Application (Conservative Dentistry, Endodontic Treatment, Oral Surgery, Implantology, Tooth Whitening, and Others), End-user (Hospitals, Dental Clinics, Ambulatory Surgery Centers, and Academic and Research Institutions), and Regional Analysis from 2026 to 2033

Dental Lasers Market Share and Trends Analysis

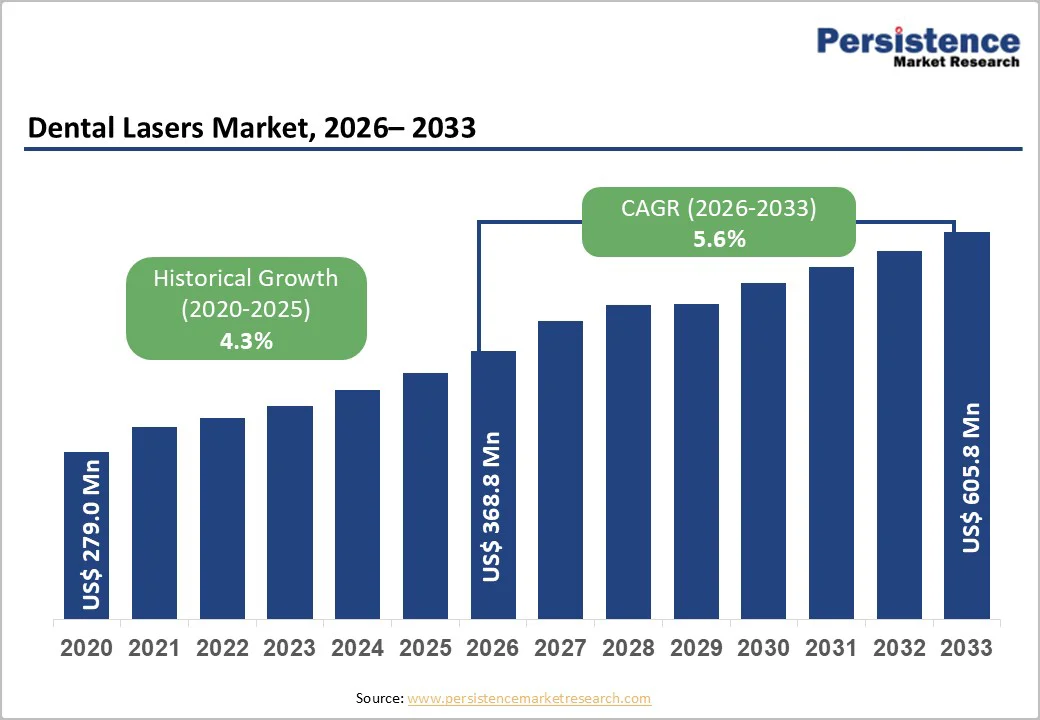

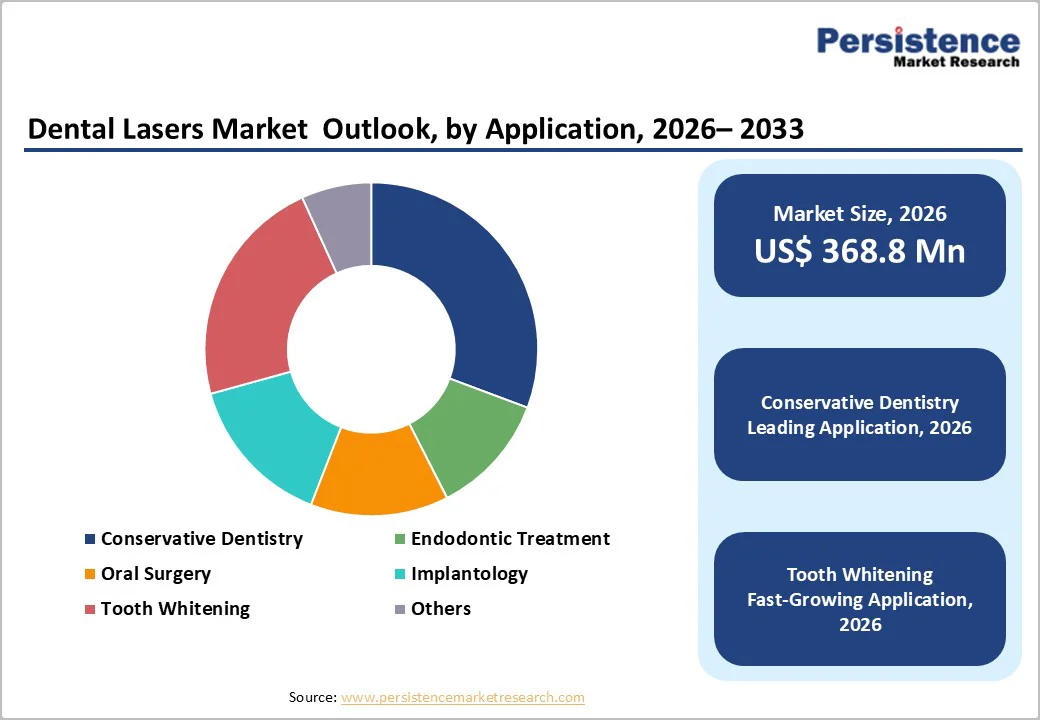

The global dental lasers market size is likely to be valued at US$ 368.8 million in 2026 to US$ 605.8 million by 2033 growing at a CAGR of 5.6% during the forecast period from 2026 to 2033.

Global demand for dental lasers is rising rapidly, driven by the growing preference for minimally invasive dentistry, increasing patient awareness of painless and anesthesia-free treatments, and widespread adoption of advanced laser systems across restorative, periodontal, surgical, and cosmetic dental procedures. The expansion of private dental clinics, dental service organizations (DSOs), and academic training centers combined with higher spending on oral health and cosmetic dentistry is accelerating market growth. Continuous innovations in diode, CO2, Nd:YAG, and Er:YAG technologies are improving treatment precision, reducing chair-time, and enhancing clinical outcomes across soft-tissue and hard-tissue procedures. Additionally, rising focus on digital dentistry, greater acceptance of laser-assisted workflows among younger dentists, and growing demand for tooth whitening and aesthetic smile-enhancement treatments further propelling market growth.

Key Industry Highlights:

- Leading Region: North America holds the largest share at 47.3%, supported by advanced dental infrastructure, strong adoption of all-tissue laser systems, high dental expenditure, and early availability of FDA-cleared devices.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large patient pool, rapid growth in dental tourism, increasing penetration of laser-enabled clinics, and rising investments in digital and cosmetic dentistry.

- Leading Product Segment: Dental surgical lasers dominate the market due to their broad versatility in soft-tissue surgeries, periodontal treatment, frenectomies, flap procedures, and minimally invasive surgical applications.

- Fastest-Growing Product Segment: Dental welding lasers are expanding rapidly as clinics adopt compact, cost-effective systems for soft-tissue contouring, periodontal therapy, and chairside procedures requiring precision and faster healing.

- Leading Application Segment: Conservative dentistry remains the top application due to high procedure volume in cavity preparation, caries removal, and tooth restoration, along with strong preference for minimally invasive laser-assisted techniques.

- Fastest-Growing Application Segment: Tooth whitening is scaling quickly as patients increasingly seek fast, safe, and effective aesthetic enhancements, with laser-assisted whitening providing superior efficiency and reduced treatment time.

| Global Market Attributes | Key Insights |

|---|---|

| Dental Lasers Market Size (2026E) | US$ 368.8 Mn |

| Market Value Forecast (2033F) | US$ 605.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver - Rising Demand for Minimally Invasive and Anesthesia-Free Dental Procedures and Rapid Technological Advancements

Rising demand for minimally invasive and anesthesia-free dental procedures is driving the adoption of dental lasers. Patients increasingly prefer treatments that offer reduced pain, minimal bleeding, shorter recovery time, and lower risk of infection. Laser technologies deliver more effectively than conventional rotary or surgical instruments. This shift is particularly evident in restorative, periodontal, and soft-tissue procedures, where lasers significantly enhance comfort and clinical efficiency. As patient expectations move toward faster, safer, and more comfortable care, dental clinics and dental service organizations (DSOs) are rapidly incorporating laser systems into routine workflows, further driving market growth.

Rapid technological advancements in diode, CO2, Nd:YAG, and Er:YAG laser platforms are also driving market growth. Modern systems provide enhanced precision, improved energy delivery control, and greater versatility across both soft-tissue and hard-tissue applications. Innovations such as smaller footprints, improved cooling mechanisms, multi-wavelength capabilities, and smarter user interfaces are making lasers easier to operate and integrate into digital dentistry ecosystems. These advancements enhance treatment outcomes, expand clinical indications, and encourage widespread adoption among general practitioners and specialists.

Restraints - High Upfront Investment Costs and Limited Reimbursement Coverage

High upfront investment costs for advanced all-tissue and multi-wavelength dental laser systems remain a major barrier to adoption, especially for small and mid-sized dental practices. Premium platforms require significant capital expenditure, making it challenging for independent clinics to justify the purchase without high patient volume or strong return-on-investment potential. In addition, ongoing maintenance requirements and the need for periodic calibration add to the total cost of ownership. Replacement of laser components, optics, fibers, and handpieces can be expensive, creating financial strain for practices with limited budgets.

Limited reimbursement coverage for many laser-assisted dental procedures further restricts market growth. In several regions, insurance providers classify laser treatments as elective or cosmetic, resulting in out-of-pocket expenses for patients. This reduces procedure uptake and discourages clinicians from integrating laser technologies into routine workflows. Moreover, inconsistent reimbursement policies across countries and lack of standardized billing codes create administrative challenges, slowing the widespread adoption of dental lasers despite their clinical advantages.

Opportunity - Rising Penetration of Dental Service Organizations and Increasing Adoption in Pediatric Dentistry

The rising penetration of dental service organizations (DSOs) and chain-based clinics that are rapidly adopting advanced digital and laser technologies are boosting market growth. These large-scale networks prioritize standardized care, faster patient turnaround, and minimally invasive procedures, making laser systems a natural fit. Their strong purchasing power, preference for technologically integrated workflows, and expansion across urban as well as semi-urban regions are accelerating the adoption of soft-tissue and hard-tissue laser systems. As DSOs continue scaling, partnerships with device manufacturers, bundled procurement models, and subscription-based technology upgrades are expected to create consistent, long-term demand.

Furthermore, growing interest in aesthetic dental procedures such as laser whitening, depigmentation, and gum contouring are propelling the market growth, particularly in emerging markets where cosmetic dentistry awareness is rising. Pediatric dentistry is another high-growth area, as lasers offer reduced pain, lower vibration, and faster recovery, improving treatment acceptance among children. These factors collectively boost dental lasers as a preferred modality for modern, patient-centric dental care, creating opportunities in the market.

Category-wise Analysis

By Product, Dental Surgical Lasers Dominate Globally to their Expanding Use in Minimally Invasive Soft-Tissue and Hard-Tissue Surgical Procedures

The dental surgical lasers segment is projected to dominate the global dental lasers market in 2026, accounting for a revenue share of 57.8%. The segment’s strong performance is primarily driven by the increasing adoption of laser-assisted soft-tissue and hard-tissue surgical procedures, which offer superior precision, reduced bleeding, and faster postoperative recovery compared to conventional surgical tools. Rising demand for minimally invasive periodontal surgeries, frenectomies, gingivectomies, flap procedures, and peri-implantitis treatments is further accelerating the use of advanced diode, CO2, and Er:YAG laser systems. The ability of surgical lasers to ensure enhanced visibility, improved sterilization, and reduced chair-time makes them highly preferred in both general and specialty dental practices. Additionally, continuous product innovations such as multi-wavelength platforms, ergonomic delivery systems, and real-time surgical controls along with expanding clinical training programs are driving widespread adoption of dental surgical lasers.

By Application, Conservative Dentistry Lead the Market Globally Due To its Widespread Use in Minimally Invasive Restorative and Cavity-Preparation Procedures

The conservative dentistry segment is projected to dominate the global dental lasers market in 2026, accounting for a revenue share of 30.7%. This is due to the widespread adoption of laser-assisted techniques for cavity preparation, caries removal, tooth reshaping, and composite restoration procedures. Dental lasers offer superior precision, reduced thermal damage, and improved patient comfort, making them increasingly preferred over traditional rotary instruments. Growing awareness of minimally invasive dentistry, rising emphasis on preserving natural tooth structure, and increasing integration of diode and Er:YAG lasers into routine restorative workflows are further supporting segment growth. Faster healing, reduced need for anesthesia, and improved clinical outcomes continue to attract both clinicians and patients. Additionally, technological advancements in compact, chairside laser units and growing training programs in dental schools are accelerating the adoption of laser-based conservative dentistry.

By End-user, Dental Clinics Dominate Globally Due to Their Advanced Technology Adoption and High Patient Footfall

The dental clinics segment is projected to dominate the global dental lasers market in 2026, accounting for a revenue share 54.6%. This is driven by the rapid adoption of laser-enabled procedures across private practices and chain-based dental service organizations (DSOs), which increasingly prioritize minimally invasive treatments, higher patient throughput, and improved clinical outcomes. Dental clinics benefit from greater flexibility in adopting new technologies, enabling faster integration of diode, CO2, and Er:YAG laser systems for restorative, periodontal, cosmetic, and soft-tissue surgeries. Rising patient preference for painless, anesthesia-free treatments and shorter recovery times further boosts demand within clinic settings. Additionally, expanding cosmetic dentistry trends such as laser whitening and gingival contouring are increasing laser utilization in urban and semi-urban practices. Ongoing investments in clinician training, bundled device-service models, and digital workflow integration also boosts market growth.

Regional Insights

North America Dental Lasers Market Trends

The North America market is expected to dominate globally with a value share of 47.3% in 2026, with the U.S. leading the region due to its strong technological base, high dental-care spending, and early adoption of advanced laser systems across general and specialty dentistry. The region benefits from a robust ecosystem of manufacturers, well-established distribution networks, and a large pool of trained dental professionals who actively integrate diode, CO2, and Er:YAG lasers into restorative, periodontal, surgical, and cosmetic procedures.

Growing patient preference for minimally invasive, anesthesia-free treatments and the rising popularity of aesthetic dentistry, including laser whitening and soft-tissue contouring, continue to drive market expansion. Supportive reimbursement for select dental procedures, frequent product launches, and strong regulatory pathways such as FDA 510(k) clearances further accelerate innovation and clinician uptake. Additionally, increasing investments in digital dentistry, high penetration of dental service organizations (DSOs), and extensive continuing-education programs offered by industry leaders contribute to widespread integration of laser technologies in both large dental chains and independent practices across the region.

Europe Dental Lasers Market Trends

Europe is expected to achieve a steady growth, driven by the increasing adoption of advanced dental technologies, a rising geriatric population with greater restorative and periodontal care needs, and a strong emphasis on minimally invasive clinical workflows. Countries such as Germany, the U.K., France, Italy, and the Nordic region are leading in early adoption of diode, CO2, and Er:YAG laser systems due to well-established dental infrastructures and high patient awareness regarding painless procedures. The growing preference for aesthetic dentistry, including tooth whitening and soft-tissue contouring, is further accelerating the shift toward laser-enabled treatments.

Regulatory support for digital dentistry, wider reimbursement for select dental interventions, and integration of laser systems into digital workflows such as CAD/CAM and intraoral scanning—are enhancing the clinical value proposition for practitioners. Continuous product innovation by regional and global manufacturers, professional training programs, and strong presence of dental academies are also driving market growth.

Asia Pacific Dental Lasers Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.6% between 2026 and 2033, driven by rapid growth in dental tourism, rising adoption of minimally invasive procedures, and increasing availability of cost-effective laser systems across emerging economies. Countries such as India, China, South Korea, and Thailand are witnessing a surge in cosmetic dentistry cases, fueled by expanding middle-class income, improved oral-care awareness, and greater acceptance of laser-assisted treatments for whitening, periodontal therapy, restorative procedures, and soft-tissue surgeries.

Technological advancements, including compact diode lasers, multi-wavelength platforms, and enhanced ergonomic handpieces, are further boosting clinician adoption in both urban and semi-urban dental clinics. Government initiatives supporting digital dentistry, rising investments in dental education, and growing penetration of global manufacturers through partnerships and training programs are boosting market growth.

Competitive Landscape

The global dental lasers market is highly competitive, with strong participation from companies such as BIOLASE MG LLC., Fotona, GIGAAMEDICAL, amdlasers, CAO Group, Inc., and Dentsply Sirona. These players leverage extensive distributor networks, advanced all-tissue and soft-tissue platforms, and continuous innovation in diode, CO2, Nd:YAG, and Er:YAG laser technologies. Growing demand for minimally invasive, anesthesia-free procedures and increased adoption of compact, chairside laser units are accelerating penetration across dental clinics, hospitals, and academic institutions.

Manufacturers are increasingly focusing on AI-assisted treatment guidance, app-integrated user interfaces, and multi-wavelength hybrid systems that support a wider range of restorative, periodontal, surgical, and cosmetic procedures. Strategic priorities include expanding product portfolios, enhancing safety and precision through real-time monitoring features, improving clinician training programs, and driving market growth.

Key Industry Developments:

- In September 2025, BIOLASE, a leading dental laser developer, was acquired by MegaGen Implant following its Chapter 11 bankruptcy filing in October 2024, with MegaGen founder Kwang Bum Park assuming leadership of the company.

- In February 2024, BIOLASE, Inc. launched its advanced all-tissue laser system, the Waterlase iPlus Premier Edition™, which debuted at the Chicago Midwinter Meeting 2024 (February 22-24, booth 4608). The new system is a major upgrade to the flagship Waterlase iPlus platform and showcases BIOLASE’s latest innovations in high-precision, minimally invasive dental laser technology.

- In December 2023, Convergent Dental announced that its Solea® All-Tissue CO2 laser is now in use across all 50 U.S. states, following its adoption by North Coast Family Dentistry in Anchorage, Alaska, marking a nationwide milestone for laser-based dental care.

Companies Covered in Dental Lasers Market

- BIOLASE MG LLC.

- Fotona

- GIGAAMEDICAL

- amdlasers

- CAO Group, Inc.

- Dentsply Sirona

- Lumenis Be Ltd.

- Convergent Dental, Inc.

- TBS Dental

- Parkell, Inc.

- Ivoclar Vivadent

- J. MORITA CORP.

- KaVo Dental

- Others

Frequently Asked Questions

The global dental lasers market is projected to be valued at US$ 368.8 Mn in 2026.

Rising demand for minimally invasive and precise dental procedures and growing preference for faster recovery and reduced chair-time treatments are driving the global dental lasers market.

The global dental lasers market is poised to witness a CAGR of 5.6% between 2026 and 2033.

Growing adoption of cosmetic dentistry and expanding use of lasers in minimally invasive dental surgeries are creating opportunities in the market.

BIOLASE MG LLC., Fotona, GIGAAMEDICAL, amdlasers, CAO Group, Inc., and Dentsply Sirona are some of the key players in the dental lasers market.