- Automation & Robotics

- Construction Lasers Market

Construction Lasers Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Construction Lasers Market by Laser Type (Spot/Plumb/Dot Lasers, Line Level Lasers, Rotary Level Lasers and Others (Pipe Lasers, Grade Lasers Etc.), and Fluorescent), by Range (1 ft. to 100 ft., 101 ft. to 200 ft., and 201 ft. to Above), by Sales Channel (Indoor and Outdoor) and Regional Analysis for 2026 - 2033

Construction Lasers Market Size and Trends Analysis

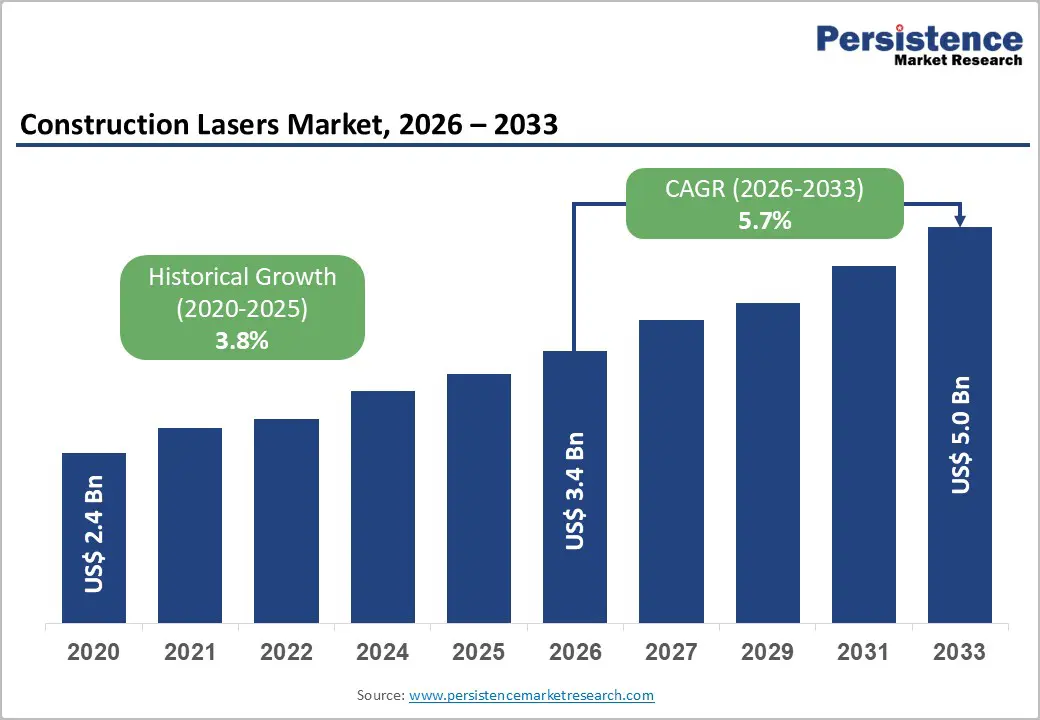

The global construction lasers market is likely to be valued at US$ 2.9 billion in 2026 and is projected to reach US$ 4.3 billion by 2033, growing at a CAGR of 5.7% during the forecast period (2026-2033).

This market expansion reflects accelerating infrastructure development, rising construction project complexity, and widespread adoption of precision measurement technologies across the construction ecosystem. The market demonstrates consistent momentum driven by urbanization trends in emerging economies and technological advancements in laser systems.

Key Industry Highlights:

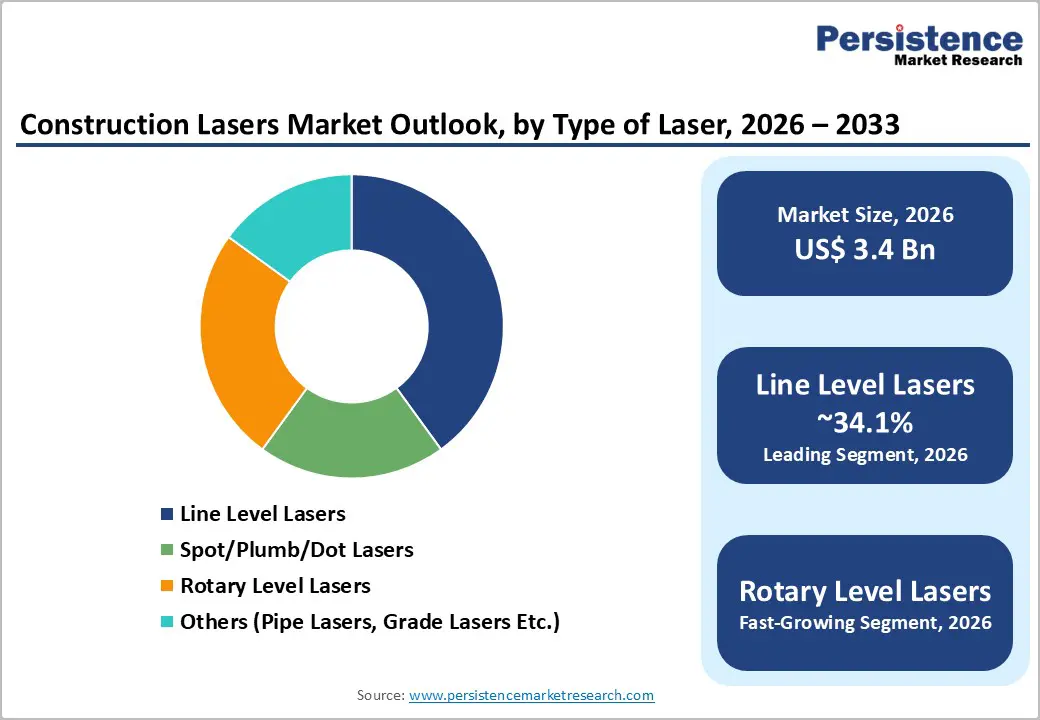

- Dominant Laser Type: Line Level Lasers dominate with 34.1% market share (US$ 990 million in 2025), while Rotary Level Lasers represent the fastest-growing segment with 7.2% annual CAGR, driven by infrastructure expansion and emerging market development.

- Leading Range: The 1 ft. to 100 ft. range leads with 45.6% market share, while the 101 ft. to 200 ft. range exhibits the fastest growth at 8.1% annual CAGR, reflecting infrastructure and civil construction project expansion.

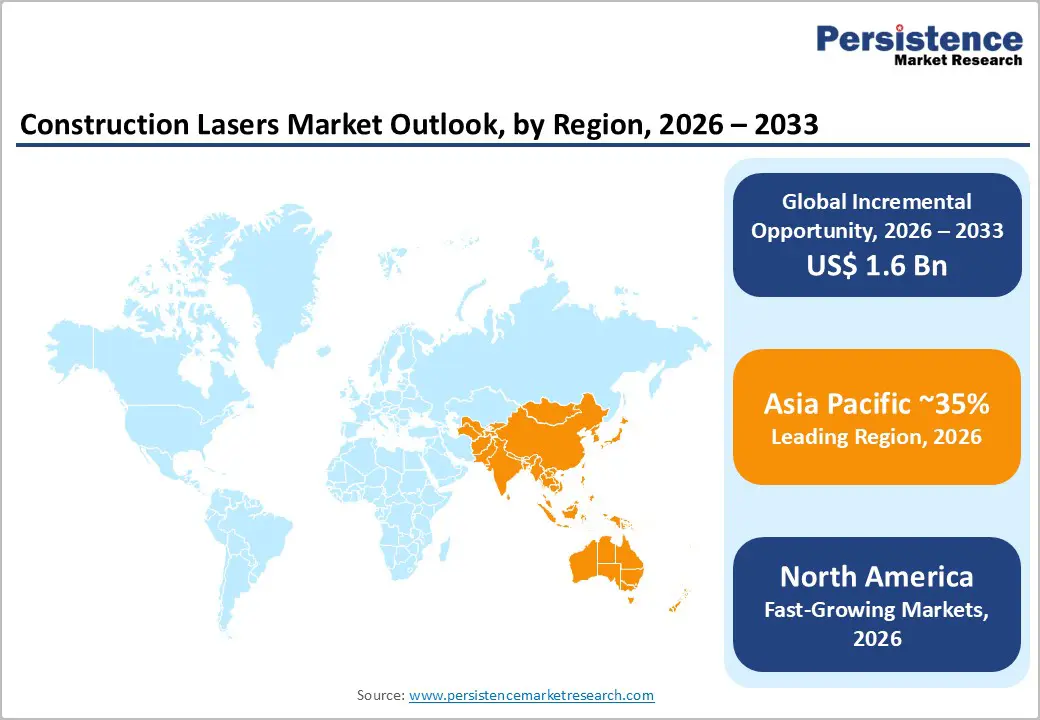

- Regional Market Leaders: Asia-Pacific drives global expansion with 6.8% CAGR (reaching US$ 1.82 billion by 2032), while North America and Europe maintain stable 5.2% growth rates, indicating geographic diversification of market opportunity.

- Market Strategy and Consolidation: The top five manufacturers (Trimble, Topcon, Leica Geosystems, Bosch, Hilti) control 55-60% of global market value, indicating moderate concentration with growth opportunities for specialized and regional competitors.

- Strategic Market Evolution: Recent developments emphasize digital ecosystem integration (Hilti PLT 500 BIM synchronization), artificial intelligence and automation (Trimble X12 AI-powered scanning), and autonomous construction systems (Topcon GPT-6 machine control), signaling market transition toward integrated technology platforms supporting construction digitalization.

| Key Insights | Details |

|---|---|

|

Construction Lasers Market Size (2026E) |

US$ 2.9 Bn |

|

Market Value Forecast (2033F) |

US$ 4.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.7% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.8% |

Market Dynamics

Driver - Accelerating Infrastructure Development and Urbanization

Global infrastructure investment reached unprecedented levels, with Asia-Pacific accounting for over 60% of new construction spending. Urbanization rates in emerging markets—particularly in India (a projected 38.4% urban population by 2030) and China—continue to drive demand for construction lasers in large-scale building projects. Governments worldwide are allocating substantial capital to smart city initiatives, transportation networks, and commercial real estate development. Construction lasers play a critical role in site layout, grading, and alignment—tasks requiring precision to avoid costly rework. The World Economic Forum estimates that digital adoption in the construction industry could improve productivity by 20%, with laser technology serving as foundational equipment for achieving these efficiency gains. Market analysis indicates that for every 1% increase in construction spending, construction laser demand grows by approximately 0.8-1.2%, reflecting the tool's essential role in modern construction operations.

Technological Advancement and Green Laser Adoption

Construction lasers have undergone significant technological evolution, particularly with the transition from red to green beam laser technology. Green beam lasers offer 3-5 times the visibility of traditional red lasers in outdoor and high-brightness environments—a critical advantage on job sites with variable lighting conditions. Modern self-leveling and automatic-leveling systems have reduced operator setup time by 30-40%, improving labor productivity. Integration of construction lasers with GPS, GNSS, and BIM technologies enables real-time synchronization between physical construction and virtual project models. Advanced features, including Bluetooth connectivity, automated data logging, and cloud-based project management, enhance the user experience and operational efficiency. Manufacturers report that adoption rates for feature-rich laser systems have increased by 35% annually, driven by contractor demand for integrated solutions that reduce manual intervention and improve project coordination.

Restraint - High Capital Investment Requirements for Advanced Systems

Premium construction laser systems, particularly rotary level lasers with machine control integration and 3D scanning capabilities, command price points of US$ 3,000-8,000 per unit—significantly higher than basic line lasers priced at US$ 200-500. For small and mid-sized construction contractors operating on tight margins, capital expenditure for complete laser systems represents a substantial barrier. While rental and subscription models have emerged (offering equipment access at US$ 50-150 monthly), adoption remains concentrated in developed markets. Equipment fragmentation across different project types (plumb lasers for interior work, rotary lasers for grading, pipe lasers for underground utilities) necessitates multi-device investments, limiting market penetration among price-sensitive segments. Emerging market contractors cite equipment cost as a barrier in 42% of cases where construction lasers remain underutilized despite project requirements.

Supply Chain Vulnerabilities and Semiconductor Constraints

Construction laser manufacturing relies on specialized optical components, laser diodes, and control electronics, all of which are subject to global supply chain disruptions. The semiconductor shortage that impacted 2021-2023 particularly affected self-leveling and automatic-leveling laser systems requiring advanced microcontrollers. Production capacity for laser diodes is concentrated in three Asian regions (Japan, South Korea, and China), creating geographic concentration risk. Lead times for premium laser systems have increased to 8-12 weeks, up from pre-pandemic levels of 4-6 weeks. Supply volatility has constrained market growth, particularly for commercial contractors with fixed project timelines. Manufacturers report that supply chain unpredictability has delayed approximately 15-18% of anticipated orders during periods of component scarcity.

Opportunity - Emerging Market Expansion and Rural Infrastructure Development

Infrastructure development in South Asia (India, Bangladesh, Sri Lanka) and Southeast Asia presents substantial market expansion potential. India's infrastructure investment pipeline—including the National Infrastructure Pipeline (US$ 1.4 trillion through 2030) and smart city missions affecting 109 cities—creates demand for precision measurement tools across rail, road, water, and utility projects. Current construction laser penetration in India stands at approximately 18-22% of construction projects, compared to 65-75% in North America and Western Europe, indicating significant growth runway. The rental model is gaining traction in emerging markets, with equipment-as-a-service providers addressing capital constraints. Market sizing indicates that emerging market construction laser demand could expand 12-15% annually through 2030, driven by the digitalization of construction practices and rising professional standards.

Integration of Laser Technology with Autonomous Construction Equipment and AI-Powered Systems

The convergence of construction lasers with autonomous grading machines, robotic positioning systems, and AI-powered layout automation represents a transformative market opportunity. Companies, including Trimble and Topcon, are developing integrated systems in which laser sensors provide real-time positioning feedback to autonomous equipment, eliminating the need for manual layout. These systems demonstrate potential to reduce field setup time by 50-70% and minimize measurement errors to sub-millimeter tolerances. Market sizing for autonomous construction equipment indicates a US$ 12-15 billion market by 2032, with laser positioning systems representing 8-12% of system value. The convergence of laser technology with construction robotics could open adjacent market segments worth US$ 800-1,200 million by 2032.

Category-wise Analysis

By Laser Type Insights

Line-level lasers dominate the construction laser market, generating about US$ 990 million in 2026. These tools project precise horizontal or vertical lines, supporting alignment tasks such as drop ceilings, wall tiling, conduit placement, and interior framing. Their popularity is driven by ease of use, compact design, and suitability for contractors with minimal training. Adoption is strongest in residential construction, which accounts for 42% of global construction activity, reflecting the importance of interior finishing work where visible quality is critical. Ongoing innovation, particularly green beam technology and improved self-leveling mechanisms, continues to enhance performance.

In contrast, rotary level lasers are the fastest-growing segment, driven by infrastructure and civil construction projects that require long-range, high-precision leveling. With 360-degree coverage beyond 300 feet, demand is rising in emerging markets such as India, Vietnam, and the Philippines, supported by government infrastructure investments and advancing construction standards.

By Range Insights

The 1–100-foot range is the largest segment of the construction lasers market, accounting for approximately US$ 1,320 million in 2026. It covers the most common applications, including interior finishing, standard site layout, and routine grading. Segment dominance reflects the high volume of small- to medium-sized construction projects and the widespread use of compact, portable laser tools in everyday contracting work. Ease of use, affordability (US$ 300–1,200), and multi-application versatility make this range the primary volume driver. Both professional contractors and DIY users prefer these systems, ensuring stable demand across economic cycles.

The 101–200-foot range is the fastest-growing category, supported by expanding infrastructure and civil construction activity. It enables large-scale grading, utility trenching, and commercial alignment tasks. Improved accuracy at longer distances and rising infrastructure investment are accelerating adoption, with market revenue projected to reach US$ 450 million by 2033, growing at 7% annually.

Regional Insights

North America Construction Lasers Market Trends

North America captured US$ 890 million (30% global share) in 2026 and is projected to reach US$ 1,280 million by 2032, representing a 5.2% CAGR. The United States dominates regional performance, accounting for 78% of North American revenue, driven by mature construction markets, high equipment penetration, and established professional contractor standards.

The U.S. construction market reached US$ 1.72 trillion in 2025, with laser equipment adoption concentrated in commercial construction (68% penetration), residential construction (52% penetration), and civil infrastructure projects (71% penetration). Canada represents a secondary market (12% regional share) with strong adoption in oil sands infrastructure and commercial real estate development.

Federal infrastructure investment (Infrastructure Investment and Jobs Act allocating US$ 110 billion to highways, roads, and bridges) is driving the adoption of laser scanning across transportation and utility projects. Technology Integration Leadership: North American contractors lead global adoption of BIM-integrated laser systems and cloud-connected equipment platforms, with adoption rates exceeding 60% among commercial contractors.

Europe Construction Lasers Market Trends

Europe accounted for US$ 780 million (22.9% global share) in 2026 and is forecast to reach US$ 1,120 million by 2032, achieving a 5.2% CAGR, matching North American growth rates. Germany, the United Kingdom, France, and Spain collectively account for 72% of the European market value.

Germany leads regional markets with US$ 245 million (31.4% European share), supported by strong industrial manufacturing, infrastructure modernization across Eastern European member states, and robust professional construction standards. The United Kingdom (US$ 180 million, 23.1% share) demonstrates strong commercial construction activity and continued transportation infrastructure investment post-2025. France (US$ 165 million, 21.2% share) benefits from sustainable building standards driving construction activity, while Spain (US$ 130 million, 16.7% share) shows emerging market characteristics with rising construction investment.

The EU Construction Products Regulation (CPR) and the Sustainable Buildings Directive (Energy Performance of Buildings Directive) mandate precision measurement documentation, thereby elevating the adoption of professional-grade laser systems. Green building certifications (LEED, BREEAM) require laser measurement verification for construction precision and compliance.

Asia Pacific Construction Lasers Market Trends

Asia Pacific dominated global construction laser markets with US$ 1,140 million (35% global share) in 2025 and is projected to reach US$ 1,820 million by 2032, achieving 6.8% CAGR—the highest regional growth rate. China, Japan, India, and ASEAN markets collectively drive regional expansion.

China represents 47% of regional revenue (approximately US$ 535 million in 2025), supported by continued urbanization, infrastructure-heavy economic model, and manufacturing capacity expansion. Japan (18% regional share, US$ 205 million) demonstrates mature market characteristics with premium equipment adoption and technological leadership. India (22% regional share, US$ 250 million) exhibits explosive growth (12-14% CAGR) driven by infrastructure development programs and the rising professionalization of the construction sector.

Key Industry Developments:

- In October 2023, Topcon Positioning Systems launched the LN-50 3D laser. This new layout navigator offers streamlined precision measurement. The range for this new laser is 50 meters, which is user-friendly, self-leveling and cost-effective.

- In July 2023, Spectra Precision announced its new line product, the Spectra Precision GL 1425C. This GL 1425C comes with a dual-grade, automatic self-leveling laser designed for leveling, grading, and vertical alignment. This launch product can be used in even the toughest construction sites.

Companies Covered in Construction Lasers Market

- THEIS Feinwerktechnik

- AdirPro

- DeWALT

- Hilti Corporation

- Johnson Level & Tool Mfg. Co.

- Kapro Industries Ltd.

- Leica Geosystems AG

- Milwaukee Tool

- Fluke Corporation

- DONGYE Optoelectronics

- Others Key Players

Frequently Asked Questions

The Construction Lasers market is estimated to be valued at US$ 3.4 Bn in 2026.

The key demand driver for the Construction Lasers market is the increasing need for precision and efficiency in construction and infrastructure projects, particularly driven by rising infrastructure development, urbanization, and large-scale construction activity globally.

In 2026, the Asia Pacific region is likely to dominate with an exceeding 35% revenue share in the global Construction Lasers market.

Among the Laser type, Polyurethane holds the highest preference, capturing beyond 34.1% of the market revenue share in 2026, surpassing other Type of Laser.

The key players in Construction Lasers are AdirPro, DeWALT, Hilti Corporation, Johnson Level & Tool Mfg. Co. and Kapro Industries Ltd.