- Off-Road Equipment & Machinery

- Construction Equipment Rental Market

Construction Equipment Rental Market Size, Share, and Growth Forecast, 2026 – 2033

Construction Equipment Rental Market by Equipment Type (Earthmoving Equipment, Material Handling Equipment, Concrete & Road Building Equipment, Others), Application (Residential, Commercial, Industrial), and Regional Analysis for 2026–2033

Construction Equipment Rental Market Share and Trends Analysis

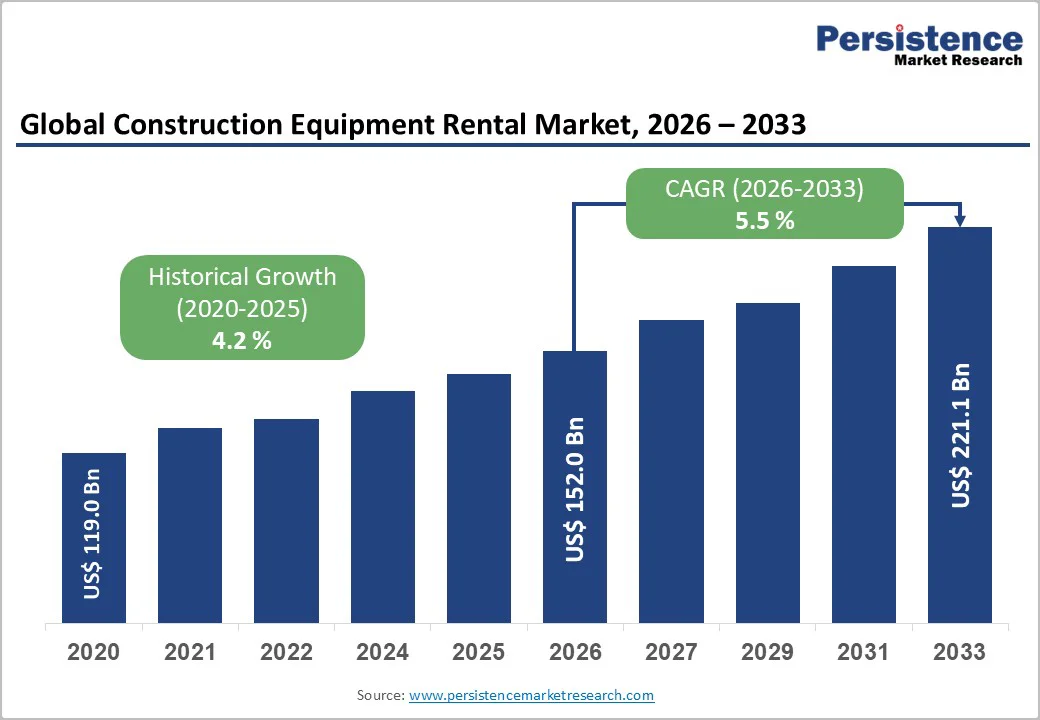

The global construction equipment rental market size is likely to be valued at US$160.4 billion in 2026, and is projected to reach US$233.3 billion by 2033, growing at a CAGR of 5.5% during the forecast period 2026-2033. The market’s expansion is driven principally by rising infrastructure and urban development investments worldwide, increasing preference for rental versus ownership due to cost and flexibility advantages, and accelerating adoption of modern and efficient equipment by contractors. As major economies push forward with road, housing, commercial and industrial projects, often under tight timelines and capital budgets, rental demand is set to increase, particularly for heavy equipment such as earthmoving and road construction machinery.

Key Industry Highlights

- Dominant Equipment Type: Earthmoving equipment is estimated to dominate in 2026 with around 38% share, owing to its criticality in mining and infrastructure projects.

- Fastest-Growing Equipment Type: Concrete & road-building equipment is projected to grow the fastest through 2033 at roughly 5.5% CAGR, due to a surge in highway, urban road, airport, and transit infrastructure projects worldwide.

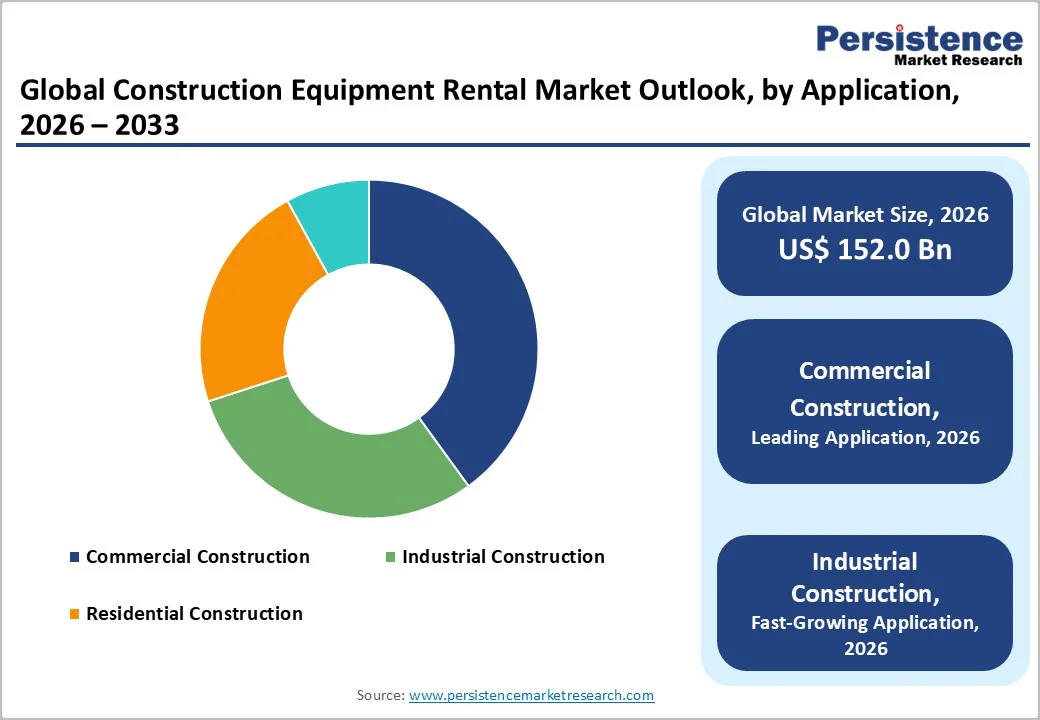

- Leading Application: Commercial construction is likely to lead in 2026 with an estimated 42% revenue share, as a result of soaring investments in commercial real estate.

- Fastest-Growing Application: Industrial construction is expected to grow at around 5.8% CAGR through 2033, as large-scale industrial projects require the intermittent use of specialized, heavy-duty machinery.

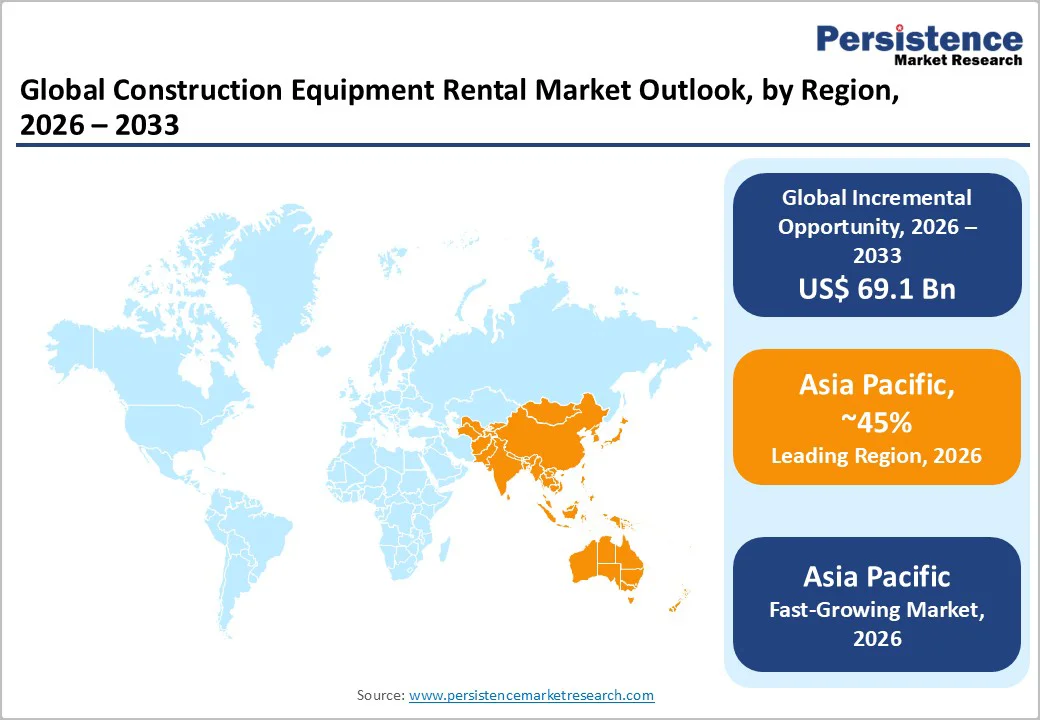

- Dominant Region: Asia Pacific is projected to hold the largest share of approximately 45% in 2026, backed by heavy investments in infrastructure development programs by governments.

- July 2025: Alba-based Mollo Noleggio, the first Italian rental-only company, entered the 2025 IRN 100 global ranking by International Rental News with turnover exceeding € 15 million.

| Report Attribute | Details |

|---|---|

|

Construction Equipment Rental Market Size (2026E) |

US$ 160.4 Bn |

|

Market Value Forecast (2033F) |

US$ 233.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.5 % |

|

Historical Market Growth (CAGR 2020 to 2024) |

4.2 % |

Market Factors – Growth, Barriers, and Opportunity Analysis

Infrastructure Growth, Cost Efficiency, and Technological Advancements Driving Rental Demand

Rising global infrastructure investments, including roads, highways, bridges, commercial buildings, and urban redevelopment projects, are significantly boosting the demand for construction equipment rental. Contractors increasingly prefer rental solutions to avoid high capital expenditures, manage operational costs, and maintain flexibility across projects of varying size and duration. Rental models allow firms to scale their equipment needs efficiently, reduce depreciation risks, and optimize cash flow, making it a cost-effective alternative to ownership. This trend is particularly evident in regions experiencing rapid urbanization and large-scale infrastructure renewal, where access to modern machinery is critical for timely project completion and resource efficiency.

At the same time, technological advancements and fleet modernization are enhancing the appeal of rental services. Integration of telematics, real-time monitoring, and low-emission machinery improves operational reliability, utilization rates, and regulatory compliance. Modern rental fleets provide contractors with performance transparency, reduced downtime, and access to equipment that meets environmental and efficiency standards.

Seasonal Demand Fluctuations and Equipment Maintenance Challenges

The construction equipment rental market growth faces constraints due to seasonal demand variability and project-specific fluctuations. Construction activity often depends on weather conditions, project cycles, and regional peak seasons, leading to uneven rental demand. Rental providers may experience underutilization during off-peak periods, resulting in revenue instability and reduced fleet efficiency. Smaller providers with limited equipment capacity are particularly vulnerable, as inconsistent utilization can affect profitability and force contractors to include additional risk buffers in project planning. These factors can make rental services less attractive for certain projects that require predictable availability and tight timelines.

High maintenance requirements and supply-chain challenges for modern equipment pose additional structural limitations. Timely servicing, spare parts availability, and fleet aging increase operational costs and downtime. Older or poorly maintained machinery may become less reliable, limiting the attractiveness of rental options for contractors who require modern, dependable equipment for large or time-sensitive projects. These combined factors can constrain market growth by impacting service quality, fleet efficiency, and the ability of rental providers to meet client expectations consistently.

Expansion in Emerging Markets and Adoption of Green, Flexible Rental Models

Rapid urbanization, industrialization, and infrastructure growth in emerging markets, particularly in Asia Pacific, are driving substantial demand for construction equipment rentals. Contractors with limited capital budgets increasingly prefer rental solutions for cost-effective and scalable project execution. Early investment in fleet expansion and localized services, including short-term and flexible rentals, allows providers to capture significant demand from growing urban and industrial projects, creating a strong growth trajectory for rental businesses.

Simultaneously, the adoption of low-emission, hybrid, or electric equipment, combined with digital fleet management and on-demand or subscription-based rental models, presents additional opportunities. Eco-friendly and technologically advanced fleets help providers meet regulatory requirements, differentiate offerings, and secure long-term contracts. Flexible rental solutions optimize fleet utilization, reduce idle time, and attract small and medium enterprises (SMEs) and project-specific clients, expanding market reach and revenue potential.

Category-wise Analysis

Equipment Type Insights

Earthmoving equipment, including excavators, loaders, backhoes, and graders, is estimated to hold the largest market share in 2026 at approximately 38%. These machines are essential for construction, mining, and infrastructure projects, and their high capital cost and infrequent use make ownership less attractive for many contractors. Rental provides cost-effective access, enabling contractors to scale equipment use for project-specific needs without large upfront investment. The broad applicability across digging, grading, and site-prep reinforces the segment’s dominance. Contractors favor renting earthmoving machinery for flexibility, operational efficiency, and reduced financial risk.

Concrete and road-building equipment is projected to grow at an estimated CAGR of 5.5% from 2026 to 2033, driven by massive investments in highway, urban road, airport, and transit infrastructure projects. As these machines are capital-intensive and often used intermittently, rental adoption is economically practical. Government infrastructure initiatives and private-sector road expansion create recurring demand cycles, boosting equipment utilization. Specialized road construction and concrete machinery rentals allow contractors to access modern, high-performance equipment without ownership costs. The unprecedented expansion of urban areas and dedicated infrastructure upgrades globally are expected to accelerate growth in this segment.

Application Insights

Commercial construction, including offices, retail complexes, hotels, and hospitality facilities, is estimated to lead the market in 2026 with a revenue share of around 42%. Rapid urbanization and increasing investment in commercial real estate drive consistent rental demand. Contractors rely on rental solutions to meet tight project timelines and scale capacity efficiently without large capital investment. Rental allows flexibility to manage peak workloads and seasonal project surges. Cost efficiency and access to modern equipment make rentals preferable over ownership. The segment benefits from sustained urban development and redevelopment initiatives globally.

Industrial construction, which encompasses factories, plants, mining infrastructure, and heavy manufacturing facilities, is projected to grow at an estimated 5.8% CAGR during the 2026-2033 forecast period. Large-scale industrial projects often require specialized, heavy-duty machinery that is used intermittently, making rental more economical than ownership. Expanding industrialization, energy infrastructure, and logistics hubs fuel the demand for flexible rental options. Rental enables contractors to access advanced equipment, manage operational costs, and maintain project schedules efficiently. The segment is gaining traction due to increasing industrial investment and the growing need for cost-effective, scalable construction solutions.

Regional Insights

North America Construction Equipment Rental Market Trends

North America remains a mature and stable market for construction equipment rental, with an estimated share of 33% of global demand in 2026. The U.S. drives the regional market, supported by infrastructure renewal, commercial construction, and urban redevelopment. High labor costs, strict safety regulations, and emission compliance encourage contractors to rent rather than own equipment. Rental fleets in the region increasingly integrate digital fleet management, preventive maintenance, and flexible rental contracts, enhancing utilization and reducing downtime. Contractors benefit from bundled services, modern equipment access, and scalable solutions that match project-specific needs efficiently.

Rental adoption in the region is further supported by advanced fleet management infrastructure, well-established rental providers, and a competitive landscape that includes both global and domestic firms. Investment trends indicate ongoing fleet modernization, expansion of telematics-enabled machinery, and integration of maintenance and operational services. Regulatory compliance for emissions and safety drives demand for newer, eco-friendly equipment. While growth is moderate compared to emerging economies, the North America construction equipment rental market remains highly efficient, technologically advanced, and strategically important for long-term investments in fleet optimization and service innovation.

Europe Construction Equipment Rental Market Trends

Europe is estimated to account for roughly 27% of the construction equipment rental market share in 2026. Key markets include Germany, the U.K., France, Spain, and Italy, where construction rental services are increasingly favored for urban redevelopment, transportation projects, and infrastructure modernization. Contractors prioritize rental solutions for cost efficiency, regulatory compliance, and access to modern low-emission machinery. Rental adoption is driven by projects requiring temporary equipment, tight timelines, and scalable capacity, particularly for material handling and road-building machinery. Digital platforms for booking and fleet management are gaining prominence across the region, enhancing operational efficiency.

The Europe market is experiencing moderate growth, underpinned by sustainability initiatives, retrofitting projects, and regulatory requirements for environmentally compliant equipment. Pan-European construction equipment rental firms leverage cross-border operations and fleet sharing to improve utilization rates. Companies focus on green fleets, digital service delivery, and emission-compliant machinery to meet evolving regulations. Urban redevelopment and retrofitting projects continue to sustain rental demand, while competition encourages fleet upgrades, service bundling, and technological adoption. Europe’s rental market remains strategically important due to regulatory-driven demand and operational innovation opportunities.

Asia Pacific Construction Equipment Rental Market Trends

Asia Pacific is the leading and fastest-growing regional market for construction equipment rental, estimated to hold around 45% of the market share in 2026. Rapid urbanization, industrialization, and large-scale infrastructure development in China, India, Japan, and Southeast Asia are primary growth drivers. High demand for highways, metro systems, smart cities, housing, industrial parks, and logistics hubs encourages rental adoption over ownership, particularly among SMEs and mid-sized contractors. Rental models provide cost-effective access to high-value equipment, reduce capital investment, and offer flexibility for short- and mid-term projects.

The regional market is projected to grow at an estimated 2026-2033 CAGR of 5.9%, fueled by massive and long-term government infrastructure programs and private-sector investments. Rental companies are expanding fleets across earthmoving, road construction, and material handling equipment, introducing flexible rental models and localized services. High demand for modern, telematics-enabled, and eco-friendly machinery enhances utilization and operational efficiency. The combination of high urbanization, infrastructure expenditure, and rental adoption positions Asia Pacific as the strategic hub for market expansion, making it the most attractive region for both domestic and global rental providers.

Competitive Landscape

The global construction equipment rental market structure is moderately consolidated, led by major international rental firms such as United Rentals, Ashtead Group, Herc Rentals, Loxam, and Sunbelt Rentals. These companies maintain strong control over fleet size, geographic coverage, and equipment variety, offering modern, telematics-enabled, and eco-friendly machinery. They leverage large-scale rental networks, digital fleet management systems, and preventive maintenance programs to ensure high utilization rates and reliability. Their ability to serve diverse construction sectors including commercial, industrial, and infrastructure projects reinforces their dominant position. Continuous investments in fleet modernization, flexible rental solutions, and subscription-based offerings further strengthen their global competitiveness and market leadership.

Regional and emerging rental providers are focusing on localized services, short-term and on-demand rentals, and cost-efficient fleet management, enabling them to capture rising demand from SMEs and contractors undertaking urban redevelopment, industrial, and infrastructure projects. Growing adoption of digital booking platforms, environmentally compliant machinery, and modular rental services is intensifying competition. Market rivalry is expected to increase as operators seek to optimize fleet utilization, expand geographic reach, and differentiate through flexible and technology-driven solutions.

Key Industry Developments

- In December 2025, EquipmentShare.com, a leading US construction equipment rental firm with US$ 3.8B revenue in 2024, filed for a US IPO on Nasdaq under ticker "EQPT," led by Goldman Sachs, UBS, and Wells Fargo. Founded in 2015 with 373 locations across 45 states, its T3 platform and OWN financing model drive growth amid digitalization in rentals.

- In September 2025, Assurant partnered with Evident to launch the commercial equipment rental industry's first end-to-end risk management solution, automating insurance verification and offering instant Loss Damage Waiver (LDW) coverage for uninsured renters. The platform flags non-compliant policies in real-time, streamlines opt-ins at rental points, and protects high-risk sectors such as construction, forestry, and agriculture.

- In June 2025, Volvo Construction Equipment (Volvo CE) agreed to acquire Swecon's operations in Sweden, Germany, and the Baltics for US$ 735 million, adding sales, rentals, services, facilities, and 1,400 employees. The deal strengthens Volvo CE's retail dominance in Europe's largest construction equipment markets and positions retail as a core strategy amid industry transformation.

Companies Covered in Construction Equipment Rental Market

- United Rentals, Inc.

- Ashtead Group plc

- Herc Rentals, Inc.

- LoxamKanamoto Co., Ltd.

- Nishio Rent All Co., Ltd.

- Boels Rentals

- Cramo Plc.

- Caterpillar Inc.

- Volvo Construction Equipment

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

Frequently Asked Questions

The global construction equipment rental market is projected to reach US$ 160.4 billion in 2026.

Heavy investments in infrastructure development, modernization of rental fleets with telematics and low-emission technologies, and growing compliance requirements across jurisdictions are driving the market.

The market is poised to witness a CAGR of 5.5% from 2026 to 2033.

Increasing adoption of eco-friendly and digitalized rental fleets, growth of on-demand and subscription-based models, and an urgent need from industrial and commercial construction projects seeking cost-optimized equipment access are key market opportunities.

Leading market companies include United Rentals, Ashtead Group (Sunbelt Rentals), Herc Rentals, H&E Equipment Services, Loxam, Kanamoto, and Nishio Rent All.