- Industrial Goods & Service

- Construction Anchor Market

Construction Anchor Market Size, Share, and Growth Forecast, 2025 - 2032

Construction Anchor Market by Product Type (Metals, Chemical, Light Duty Anchors), Application (Building Construction, Civil Engineering, Construction Installation, DIY), Sales Channel (Direct Sales, Distributor Sales, Retail Sales, Home Centers, Online Sales), and Regional Analysis for 2025 - 2032

Construction Anchor Market Share and Trends Analysis

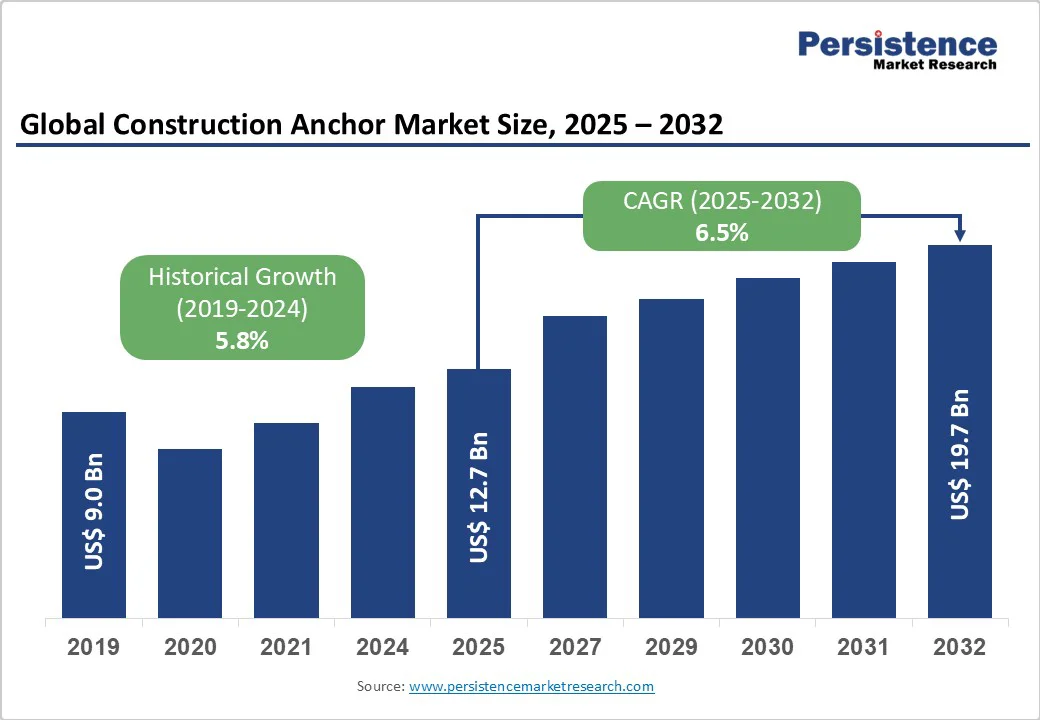

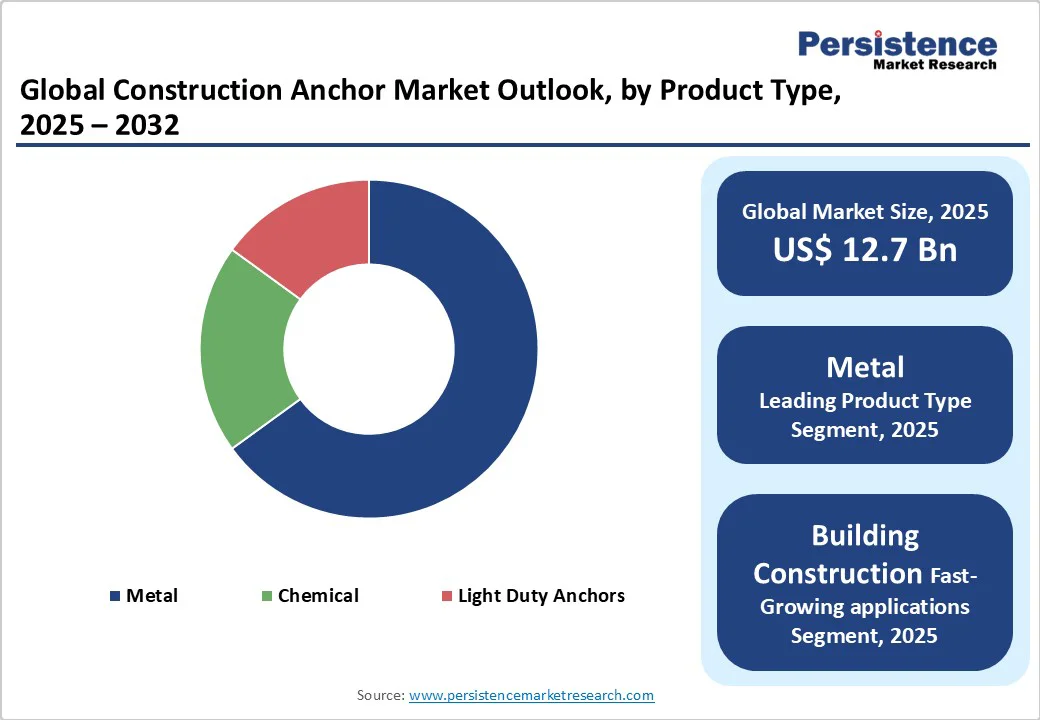

The global construction anchor market size is expected to reach US$12.7 billion by 2025. It is projected to reach US$19.7 billion by 2032, growing at a CAGR of 6.5% during the forecast period of 2025 -2032.

The growth trajectory is driven by accelerating urbanization trends worldwide and substantial investments in infrastructure development projects across emerging economies. The expanding construction industry, particularly in the commercial and residential sectors, continues to drive demand for reliable anchoring solutions that ensure structural integrity and compliance with safety standards.

Key Industry Highlights:

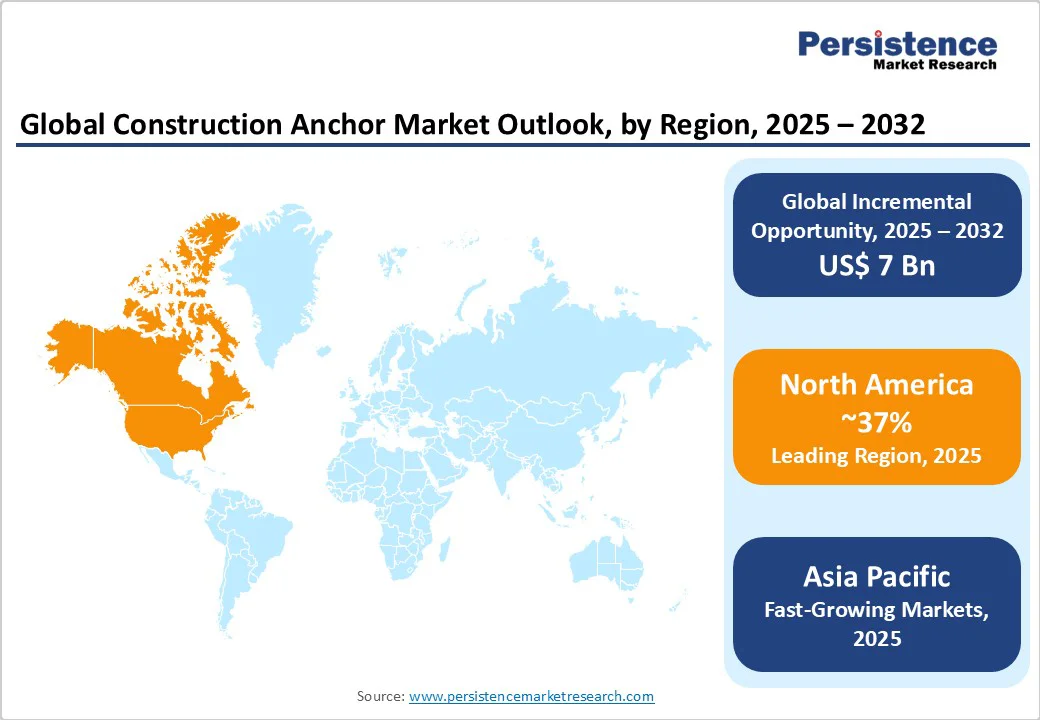

- Dominant Region: North America is likely to dominate the global market owing to advanced infrastructure and stringent safety regulations driving demand for high-performance anchoring solutions across commercial and industrial applications.

- Fastest-growing Regional Market: Asia Pacific represents the fastest-growing regional market, driven by massive urbanization, infrastructure development, and government investments in smart cities and transportation networks across emerging economies.

- Leading Product Type: Metals maintain the largest market share due to the versatility and immediate load-bearing capacity of mechanical anchors, particularly wedge anchors, which are commonly used in heavy-duty construction applications.

- Fastest-growing Product Type: Chemical anchors emerge as the fastest-growing product segment, offering superior load-bearing performance and expansion-free installation capabilities for complex structural applications and retrofitting projects.

- Key Market Opportunity: Infrastructure development and smart city initiatives present the largest market opportunity, with global infrastructure investment reaching US$3.9 trillion annually and driving sustained demand for advanced anchoring systems.

| Key Insights | Details |

|---|---|

| Construction Anchor Market Size (2025E) | US$12.7 Bn |

| Market Value Forecast (2032F) | US$19.7 Bn |

| Projected Growth CAGR (2025 - 2032) | 6.5% |

| Historical Market Growth (2019-2024) | 5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rise in Global Infrastructure Development and Smart City Initiatives

The construction anchor market is experiencing unprecedented growth due to massive infrastructure investments worldwide, with governments allocating substantial resources to modernize urban landscapes and transportation networks.

According to infrastructure investment data, global infrastructure spending is projected to reach US$3.9 trillion annually, with emerging markets driving the majority of this demand. Smart city projects across the Asia Pacific, the Middle East, and Africa are particularly driving the demand for advanced anchoring systems that support complex architectural designs and high-rise structures.

These initiatives require sophisticated mechanical and chemical anchors that can withstand dynamic loads, seismic forces, and extreme environmental conditions. For example, the National Investment Pipeline in India alone has allocated US$1.4 trillion for infrastructure projects, while the Belt and Road Initiative in China continues to generate substantial demand for construction anchors in bridges, tunnels, and commercial developments.

The construction industry's shift toward sustainable building practices is significantly boosting demand for eco-friendly and high-performance construction anchors that meet stringent environmental regulations. Building codes are increasingly mandating the use of corrosion-resistant materials, such as stainless steel and galvanized anchors, to ensure long-term structural durability and reduce maintenance requirements.

The rise of LEED certification requirements and green building compliance standards is driving the adoption of chemical anchors with low-emission formulations and sustainable manufacturing processes. Energy-efficient building designs and prefabricated construction methods require specialized anchoring systems that facilitate faster installation while maintaining superior load-bearing capacity.

High Material Costs and Price Volatility of Raw Materials

The construction anchor market growth faces significant challenges from fluctuating raw material prices, particularly for steel, stainless steel, and specialized chemical compounds used in anchor manufacturing. Price volatility in commodities markets directly impacts production costs, forcing manufacturers to adjust pricing strategies frequently and potentially reducing demand from cost-sensitive construction projects. The ongoing global supply chain disruptions and geopolitical tensions have exacerbated material cost pressures, making it difficult for companies to maintain competitive pricing while preserving profit margins.

Stringent building codes and safety regulations across different regions create compliance challenges that can delay product launches and increase development costs for construction anchor manufacturers. The requirement for extensive testing and certification processes, including ETA approvals and seismic compliance verification, extends time-to-market for new products and increases operational expenses. Varying regulatory standards between countries and regions necessitate customized product development approaches, limiting standardization benefits and increasing manufacturing complexity.

Rapid Expansion in Chemical Anchors for High-Performance Applications

Chemical anchoring systems offer superior load-bearing capacity and enhanced performance compared to mechanical alternatives, making them essential for complex infrastructure projects such as bridges, tunnels, and high-rise buildings.

Growing adoption of prefabricated and modular construction techniques requires specialized chemical anchors that facilitate rapid assembly while ensuring structural integrity. The increasing focus on retrofitting and seismic strengthening of existing structures in developed markets creates substantial demand for high-performance chemical anchoring solutions that reinforce aging infrastructure without extensive demolition.

Large economies such as India and Indonesia are experiencing rapid infrastructure expansion. Meanwhile, countries in the Middle East & Africa present emerging opportunities through diversification efforts and public infrastructure investments, particularly in Saudi Arabia and the UAE, where construction output is expected to grow considerably over the next several years.

Government-led initiatives such as smart city projects, mass transit systems, and renewable energy infrastructure require advanced anchoring solutions capable of supporting innovative architectural designs and extreme load conditions. The growing emphasis on disaster-resilient construction in seismic regions creates additional demand for specialized anchoring systems that meet stringent safety requirements while supporting rapid urban development.

Category-wise Analysis

Product Type Insights

Metals are expected to dominate the construction anchor market revenue share with approximately 65% in 2025, driven by the versatility and reliability of mechanical anchoring solutions across diverse construction applications. Wedge anchors represent the largest segment within metal anchors due to their exceptional holding power in concrete applications and ease of installation, making them ideal for heavy-duty structural connections in commercial and industrial projects.

The popularity of wedge anchors stems from their immediate load-bearing capacity upon installation and their ability to handle high tensile and shear loads without requiring curing time. Concrete screws and sleeve anchors also contribute significantly to this segment's dominance, offering cost-effective solutions for medium-duty applications in residential and light commercial construction.

Application Insights

Building construction is poised to emerge as the dominant application segment, capturing approximately 45% of the construction anchor market share by 2025, reflecting sustained growth in residential and commercial building projects globally.

The residential construction market drives substantial demand for anchoring solutions in both new construction and renovation activities. Commercial building projects, including office complexes, retail centers, and mixed-use developments, require sophisticated anchoring systems to support architectural features, facade elements, and structural connections. The growing trend toward high-rise construction in urban areas necessitates advanced anchoring solutions that can handle increased wind loads and seismic forces.

Sales Channel Insights

Direct sales channels are expected to command the largest market share, approximately 40%, in 2025, reflecting the preference of major construction companies and contractors for direct manufacturer relationships that ensure product quality, technical support, and competitive pricing.

Large-scale infrastructure projects and commercial developments typically require customized anchoring solutions and engineering support that are best delivered through direct engagement with manufacturers. Distributor sales represent the second-largest channel, serving as a crucial link between manufacturers and smaller contractors, particularly in regional markets where local relationships and inventory management are essential. Distributor networks provide broad market coverage and technical expertise while maintaining inventory levels that support immediate project requirements.

Regional Insights

North America Construction Anchor Market Trends

North America is set to maintain its position as a leading regional market, supported by robust construction activity and stringent building safety regulations. The United States construction industry demonstrates remarkable resilience, with construction spending exceeding US$2 trillion and employment reaching 8.3 million workers in 2024, surpassing pre-pandemic levels. The regional market benefits from advanced infrastructure and established regulatory frameworks that mandate high-quality anchoring systems for structural safety compliance.

The Infrastructure Investment and Jobs Act continues to attract substantial investments in roads, bridges, and public infrastructure, creating sustained demand for heavy-duty anchoring solutions. Mexico is expected to register the highest growth rate in the region, driven by nearshoring trends and increasing manufacturing investments that require sophisticated industrial construction projects. The emphasis on innovation and quality standards by stakeholders in North America positions it as a testing ground for advanced anchoring technologies, including IoT-enabled smart anchors and sustainable materials that meet evolving environmental regulations.

Europe Construction Anchor Market Trends

Europe represents a mature market with a strong emphasis on regulatory harmonization and sustainable construction practices across member states. The region's construction sector benefits from comprehensive European Union (EU) regulations, including the Construction Products Regulation (CPR) and Energy Performance of Buildings Directive (EPBD), which drive the demand for high-performance anchoring solutions. Germany, France, and the United Kingdom lead regional demand through extensive infrastructure modernization programs and energy efficiency mandates that require specialized anchoring systems.

The market demonstrates particular strength in chemical anchoring applications, with manufacturers such as EJOT and Hilti pioneering innovation in facade anchoring systems and seismic-resistant solutions. Sustainability initiatives across the region, including the EU Taxonomy framework and Level(s) standards, are pushing the development of eco-friendly anchoring materials and low-carbon manufacturing processes. The focus on retrofitting aging infrastructure and implementing green building standards creates substantial opportunities for advanced anchoring solutions that support energy-efficient construction and renewable energy installations.

Asia Pacific Construction Anchor Market Trends

The Asia Pacific is expected to emerge as the fastest-growing regional market, driven by unprecedented urbanization and infrastructure development across emerging economies, at a leading CAGR. China and India dominate regional growth, with India's construction market alone expected to grow from US$1.04 trillion in 2024 to US$2.13 trillion by 2030, fueled by smart city initiatives and industrial expansion. The regional market benefits from massive government infrastructure investments, including transportation networks, renewable energy projects, and urban development programs that require advanced anchoring solutions.

Southeast Asian countries, including Indonesia, Malaysia, and Vietnam, present substantial growth opportunities through rapid industrialization and urban expansion projects. The focus of ASEAN on disaster-resilient construction, particularly in seismic and typhoon-prone areas, drives the demand for specialized anchoring systems that meet stringent safety requirements. The region's manufacturing advantages, combined with growing domestic demand, are attracting international anchor manufacturers to establish local production facilities and strengthen their supply chain capabilities for global markets.

Competitive Landscape

The global construction anchor market exhibits a moderately fragmented structure with several established players competing across different product segments and regional markets. Market concentration varies by product category, with mechanical anchors showing higher fragmentation due to lower entry barriers, while chemical anchors demonstrate greater consolidation around specialized manufacturers with advanced formulation capabilities. Leading companies focus on strategic expansion through acquisitions, product innovation, and geographic diversification to strengthen market positions.

Key differentiators include technical expertise, product quality, robust distribution networks, and exceptional customer service capabilities, which enable companies to command premium pricing and maintain customer loyalty. Emerging business model trends include digital integration, IoT-enabled monitoring systems, and sustainable manufacturing practices that address evolving customer requirements and regulatory compliance demands.

Key Market Developments

- In October 2025, researchers at CSIR-SERC in Tamil Nadu developed an indigenous Threaded End Anchor System designed to reduce construction time while enhancing structural safety. This technology enables faster and more secure anchoring in various construction materials without compromising load-bearing capacity.

- In October 2025, fischer introduced the HybridPower anchor, a versatile solution that combines the safety and load capacity of steel anchors with the ease of use of plastic plugs. Designed for both professional and DIY applications, it works in various solid and hollow building materials, ensuring secure, long-lasting fastening even in fire situations.

- In April 2025, the U.S. Army Corps of Engineers awarded Kiewit a US$404 million design-build contract to construct the next phase of the Port Arthur, Texas flood protection project. This work includes replacing 9,525 feet of floodwall, raising 2,300 feet of levees, and upgrading fronting protections at pump stations to enhance resilience against hurricane storm surges. The construction is part of the larger Sabine Pass to Galveston Bay Coastal Storm Risk Management Project (SG2).

Companies Covered in Construction Anchor Market

- Stanley Black & Decker Inc.

- Hilti Corporation

- Simpson Manufacturing Co. Inc.

- EJOT Holding GmbH & Co KG

- Misumi Corporation

- Ancon Limited

- Fosroc Chemicals India Private Limited

- Unika Co Ltd.

- UNIQUE FASTENERS P LTD.

- Yuyao City Xintai Hardware Co Ltd.

- FIXDEX Fastening Technology

- EMC Fasteners and Tools

- Ningbo Londex Industrial Co Ltd.

- HASM Co Ltd.

- ITW

- Wurth Group

- Fischer Group

- MKT Fastening LLC

- SFS Group AG

- Sika AG

Frequently Asked Questions

The global construction anchor market is projected to reach US$ 19.7 billion in 2025.

Key growth drivers include accelerating global infrastructure development, smart city initiatives, sustainable construction practices adoption, and increasing demand for seismic-resistant building solutions across emerging economies.

The construction anchor market is poised to witness a CAGR of 6.5% from 2025 to 2032.

Growing adoption of prefabricated and modular construction techniques and increasing focus on retrofitting and seismic strengthening of existing structures in developed markets are key market opportunities.

Stanley Black & Decker Inc., Hilti Corporation, and Simpson Manufacturing Co Inc. are some key players.