- Industrial Machinery

- Condition Monitoring System Market

Condition Monitoring System Market Size, Share, and Growth Forecast 2025 - 2032

Condition Monitoring System Market Analysis by System Type (Vibration Monitoring Systems, Ultrasonic Monitoring Systems), Component (Hardware, Software, Services), Application (Oil and Gas, Power Generation, Automotive & Transportation, Others), and Regional Analysis 2025 - 2032

Condition Monitoring Systems Market Share and Trends Analysis

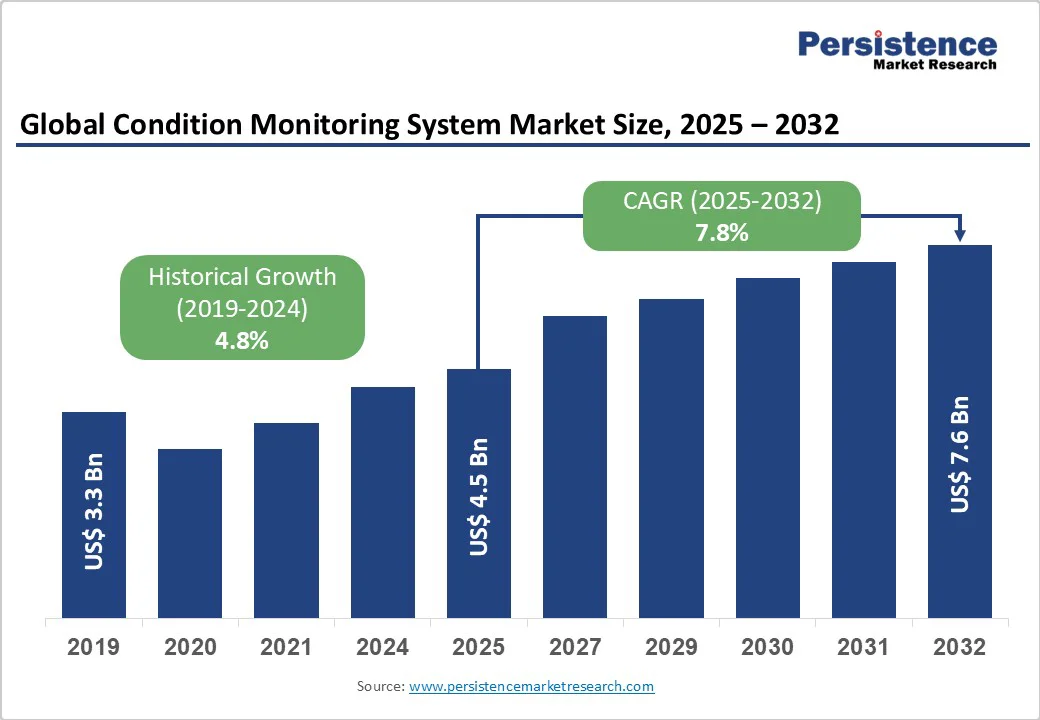

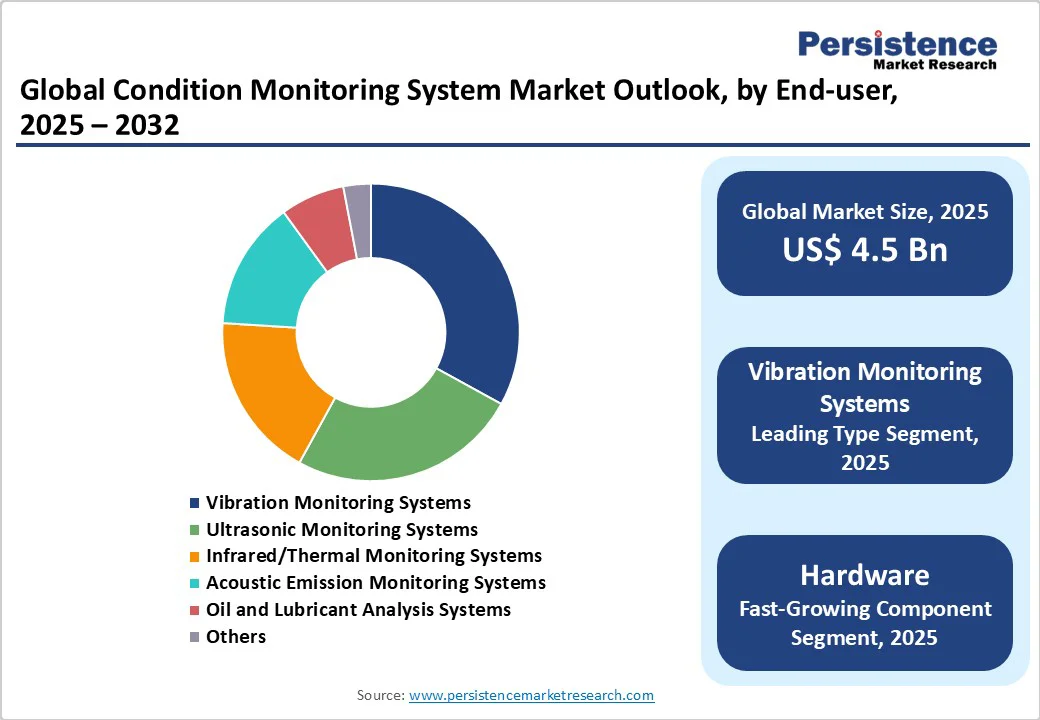

The global condition monitoring system market is likely to be valued at US$4.5 billion in 2025 and is projected to reach US$7.6 billion by 2032, growing at a CAGR of 7.8% between 2025 and 2032.

The emphasis on predictive maintenance and the integration of advanced technologies such as IoT, AI, and cloud-based analytics are pivotal in driving market growth. Industries including manufacturing, oil & gas, and aerospace are increasingly adopting condition monitoring solutions to minimize downtime, reduce maintenance costs, and enhance operational efficiency.

Key Market Highlights

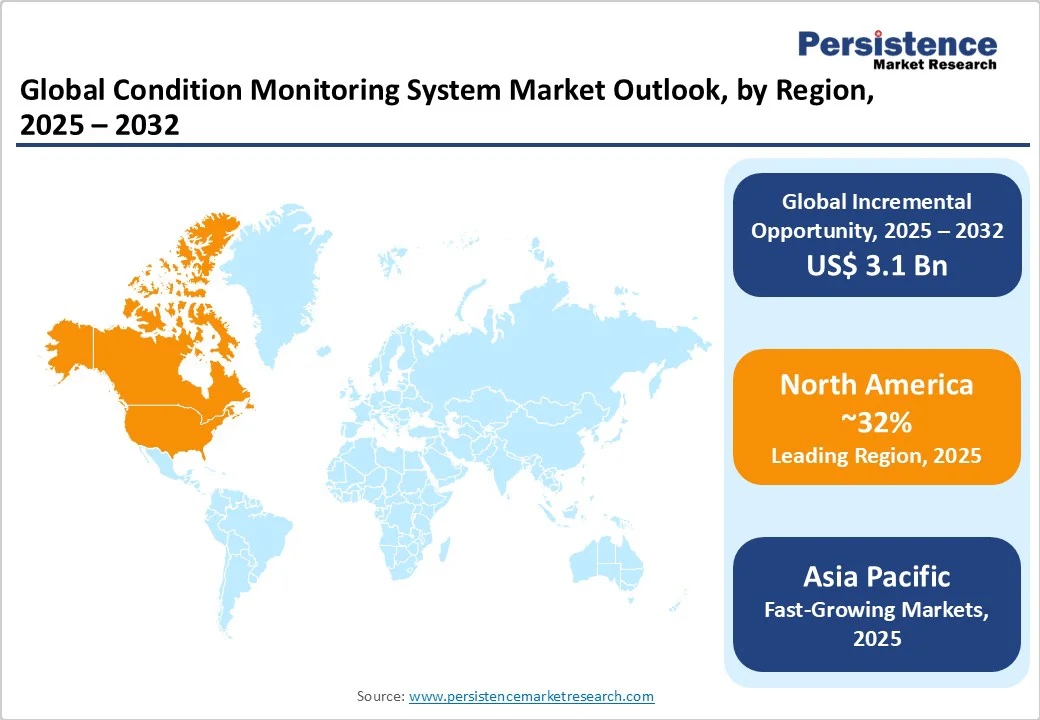

- Leading Region: North America is the leading region for condition monitoring systems due to its mature industrial infrastructure and advanced technological adoption.

- Fast-Growing Region: The Asia Pacific is the fastest-growing region, driven by rapid industrialization and government initiatives in the industry.

- Leading System Type: Vibration monitoring systems dominate the market due to their reliability and wide application across various industries.

- Leading Component: Hardware Components are the fastest growing segment due to demand for precise and rugged monitoring devices.

| Key Insights | Details |

|---|---|

| Condition Monitoring System Market Size (2025E) | US$4.5 billion |

| Market Value Forecast (2032F) | US$7.6 billion |

| Projected Growth CAGR (2025-2032) | 7.8% |

| Historical Market Growth (2019-2024) | 4.8% |

Market Dynamics

Drivers - Increasing Adoption of Predictive Maintenance Strategies

The shift from reactive to proactive maintenance is a key driver of growth in the condition monitoring system Market. Predictive maintenance enabled by these systems helps industries avoid unplanned downtime by identifying equipment faults early, thereby reducing maintenance expenses and extending the life of equipment.

For instance, in the manufacturing and power generation sectors, the adoption of vibration and ultrasonic monitoring systems has significantly enhanced operational reliability, resulting in cost savings of 15-20% in scheduled maintenance processes. The integration of Artificial Intelligence and cloud computing further strengthens the appeal of these systems by enabling real-time diagnostics and analytics, thereby fostering higher adoption rates globally.

Technological Advancements in Sensors and Connectivity

Advancements in sensor technology, including miniaturization, wireless connectivity, and IoT integration, have revolutionized condition monitoring practices. Smart sensors capable of continuous data acquisition improve the detection accuracy for parameters such as vibration, temperature, and acoustic emissions.

The rising demand for remote monitoring solutions, driven by the digital transformation of industries, promotes the deployment of such advanced systems. According to recent technology adoption trends, industries that incorporate these smart sensors observe a 25% increase in predictive accuracy, driving efficiency gains and further boosting the Condition Monitoring System Market.

Restraints -High Initial Capital Investment and Implementation Costs

Despite the benefits, the high upfront costs of advanced condition monitoring equipment and system integration pose significant barriers, especially for small and medium-sized enterprises. Hardware procurement, software licenses, sensor installations, and necessary training investments can be substantial. This is a deterrent in industries with tight operational budgets or where legacy machinery requires costly retrofitting. Consequently, the cost factor restrains faster market penetration in developing regions and among smaller manufacturers.

Data Management Complexity and Cybersecurity Concerns

The massive volume of data generated by continuous monitoring systems demands sophisticated data management and analytics infrastructure, which can be challenging to implement and maintain. Additionally, increased reliance on IoT and cloud platforms exposes monitoring systems to potential cybersecurity threats.

Organizations are cautious due to risks of data breaches that could disrupt operations or compromise sensitive manufacturing data. These concerns slow adoption rates, particularly in sectors with stringent regulatory requirements related to data privacy and security.

Opportunities - Expansion in Industrial Automation and Industry 4.0 Adoption

The rapid expansion of industrial automation and smart manufacturing offers significant opportunities for Condition Monitoring System Market players. Industry 4.0 initiatives globally are pushing for real-time asset health monitoring, integrated with AI-driven analytics, to optimize production lines and maintenance schedules.

Emerging sectors, such as automotive and aerospace, which are increasingly reliant on high precision and uptime, are significant consumers of condition monitoring technologies. Governments promoting smart factory policies are also incentivizing adoption, opening substantial new avenues for market growth.

Growing Demand from Emerging Economies and New End-use Verticals

Emerging markets, particularly in the Asia-Pacific region, present lucrative opportunities driven by expanding industrial bases and infrastructure modernization. Countries such as China, India, and South Korea are witnessing the accelerated adoption of these systems, driven by policies that encourage digital transformation and sustainability.

Beyond traditional sectors, new end-use verticals such as healthcare equipment monitoring and smart infrastructure are increasingly incorporating condition monitoring solutions. This diversification increases market scope and will drive innovation and competition among market players.

Category-wise Insights

System Type Analysis

Vibration monitoring systems lead the system type category with a share of approximately 33% in 2025. This dominance is due to their widespread applicability in early fault detection across various mechanical equipment, including turbines, engines, and pumps.

Vibration monitoring offers critical insights into bearing faults, misalignment, and imbalance, delivering actionable data that prevents catastrophic failures. Besides its reliability, integration with IoT and analytics platforms has enhanced its market preference among industries prioritizing operational continuity, driving steady demand growth.

Component Analysis

Within the component category, hardware accounts for the largest share, approximately 45%, in 2025. This segment includes sensors, data acquisition devices, and condition monitoring instruments critical to system functionality. The demand for robust and precise hardware has surged due to the need for accurate data collection in harsh industrial environments.

Furthermore, hardware innovations such as wireless sensor networks contribute to enhanced deployment flexibility, making this segment critical in the Condition Monitoring System Market.

Application Analysis

Manufacturing & industrial automation is the leading application segment, commanding nearly 30% share. Its leadership stems from the high dependence on machine uptime, operational efficiency, and safety in manufacturing plants.

Condition monitoring solutions ensure predictive maintenance, minimizing unexpected breakdowns and optimizing production line throughput. The increasing industrial digitalization and automation initiatives have entrenched condition monitoring as a key enabler of smart factory environments in this sector.

Regional Insights

North America Condition Monitoring System Trends

North America, particularly the U.S., maintains market leadership due to its mature industrial base, technological innovation, and rigorous regulatory requirements for safety and operational reliability. Leading companies headquartered in this region invest heavily in R&D to innovate condition monitoring solutions integrating AI and cloud computing.

Regulatory frameworks established by organizations such as OSHA encourage industries to adopt these systems, thereby enhancing compliance with workplace safety standards and driving market growth. The robust ecosystem of technology providers and end-users fosters a conducive environment for sustained adoption.

Europe Condition Monitoring System Trends

Europe exhibits steady growth, driven by countries such as Germany, the U.K., and France, where industrial automation and digital transformation are prioritized. Germany's automotive and manufacturing sectors, in particular, are investing heavily in condition monitoring technologies to enhance energy efficiency and minimize downtime.

The European Union's regulatory harmonization on industrial safety and environmental standards further encourages the adoption of these standards. Additionally, initiatives focusing on smart manufacturing and sustainability have a positive impact on market dynamics in this region.

Asia Pacific Condition Monitoring System Trends

The Asia Pacific region leads in terms of growth potential, driven by rapid industrialization in China, India, Japan, and the ASEAN countries. The region's manufacturing sector’s expansion and government policies aimed at Industry 4.0 adoption are pivotal growth factors.

India and China, with their strong focus on infrastructure and energy sectors, are significant contributors. Lower labor costs and increasing industrial automation adoption enhance demand for predictive maintenance solutions, enabling high market penetration. The growing number of small and medium enterprises also presents a large yet untapped market segment.

Competitive Landscape

The global condition monitoring system market is moderately consolidated with major players occupying significant shares but facing competition from emerging niche technology innovators. Industry leaders pursue growth through extensive R&D, portfolio diversification, strategic partnerships, and geographic expansions.

Key differentiators include advanced AI integration, cloud-based platforms, and customized solutions for various industries. Emerging trends show companies adopting service-based business models and predictive analytics as value additions. Market competition fosters continuous innovation and better customer-centric offerings.

Key Market Developments:

- In April 2025, Emerson Electric launched advanced vibration monitoring devices with enhanced AI analytics capabilities.

- In June 2024, Siemens AG expanded in Asia Pacific by partnering with local industrial automation firms to promote IoT-enabled condition monitoring solutions.

- In January 2025, Honeywell International introduced cloud-based condition monitoring software targeting the manufacturing sector focusing on scalability and ease of deployment.

Companies Covered in Condition Monitoring System Market

- Emerson Electric Co.

- General Electric Company, ABB Ltd.

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- SKF Group

- National Instruments Corporation

- Parker Hannifin Corporation

- Rockwell Automation, Inc.

- General Vernova

- Bentley Nevada

- PRUFTECHNIK Dieter Busch AG

- Bruel & Kjaer Vibro GmBH

- Acoem

Frequently Asked Questions

The Condition Monitoring System Market is projected to reach approximately US$ 7.6 billion by 2032, growing at a CAGR of 7.8% from 2025 to 2032.

The growing adoption of predictive maintenance strategies and technological advancements in smart sensors and IoT connectivity are the main growth drivers fueling demand across various industries.

The Vibration Monitoring Systems segment leads with around a 33% market share due to its effectiveness in early fault detection and wide industrial applications.

North America holds the largest market share led by the United States, supported by advanced technological innovation and stringent regulatory frameworks promoting safety.

Expanding industrial automation and Industry 4.0 adoption, coupled with growing demand in emerging economies like China and India, presents lucrative opportunities for growth.

Leading companies include Emerson Electric Co., General Electric Company (GE), and Siemens AG, known for their robust portfolios and technological innovations in condition monitoring systems.