- Specialty & Fine Chemicals

- Sludge Conditioner Market

Sludge Conditioner Market Size, Share, and Growth Forecast 2026 - 2033

Sludge Conditioner Market by Sludge Type (Primary, Secondary, Activated, Mixed, Other), End-use Industry (Wastewater Treatment, Pulp & Paper Mills, Food & Beverage, Oil Refineries, Chemical, Other), and Regional Analysis for 2026-2033

Sludge Conditioner Market Size and Trend Analysis

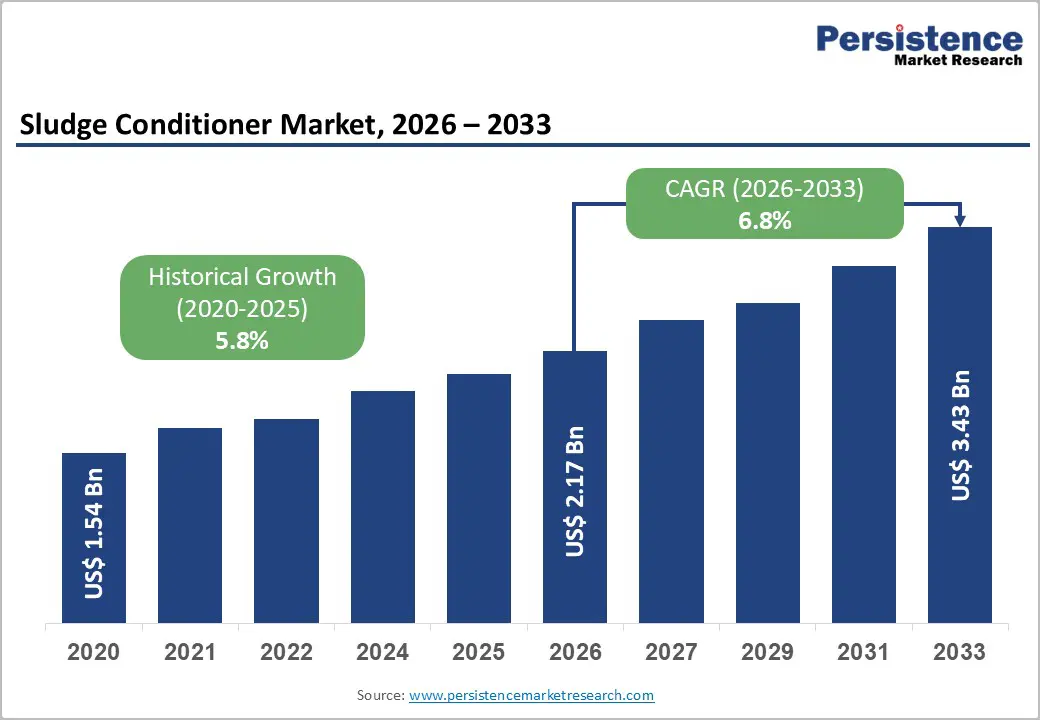

The global sludge conditioner market size is supposed to be valued at US$ 2.2 Bn in 2026 and is projected to reach US$ 3.4 Bn by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Global market growth is primarily driven by increasingly stringent environmental regulations and rapid urbanization in emerging economies, particularly in the Asia-Pacific region. Regulatory frameworks such as the revised EU Urban Wastewater Treatment Directive (UWWTD) 2024, the U.S. EPA Clean Water Act, and India’s CPCB standards mandate advanced wastewater treatment systems with enhanced nutrient removal and sludge management, creating strong demand for efficient sludge conditioning chemicals and technologies. Concurrently, industrial expansion in sectors including pulp and paper, food and beverage, and oil refining is generating substantial sludge volumes that require specialized conditioning prior to dewatering and disposal.

Key Market Highlights

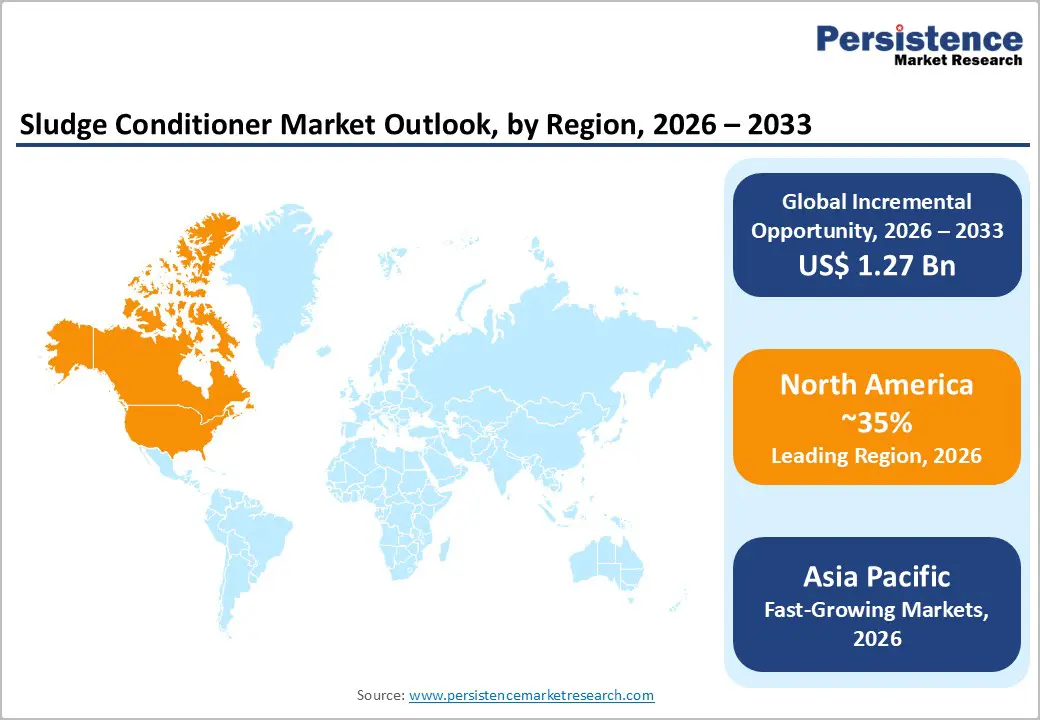

- Leading Region: North America dominates the sludge conditioner market, accounting for approximately 35% of global market value, supported by mature wastewater treatment infrastructure, stringent EPA regulatory compliance requirements under 40 CFR Part 503, and significant municipal investments in advanced sludge treatment technologies.

- Fastest Growing Region: Asia-Pacific demonstrates the highest growth potential with an anticipated CAGR of 8.5% through 2033, driven by India's Namami Gange Programme investments exceeding US$ 3.02 billion, China's advanced wastewater treatment innovations, and rapid industrialization across Vietnam, Thailand, and Indonesia.

- Dominant Sludge Type: Activated Sludge is the leading sludge type segment, commanding approximately 45% market share due to widespread application in municipal and industrial facilities, consistent conditioning requirements, and regulatory mandates that globally emphasize secondary biological treatment.

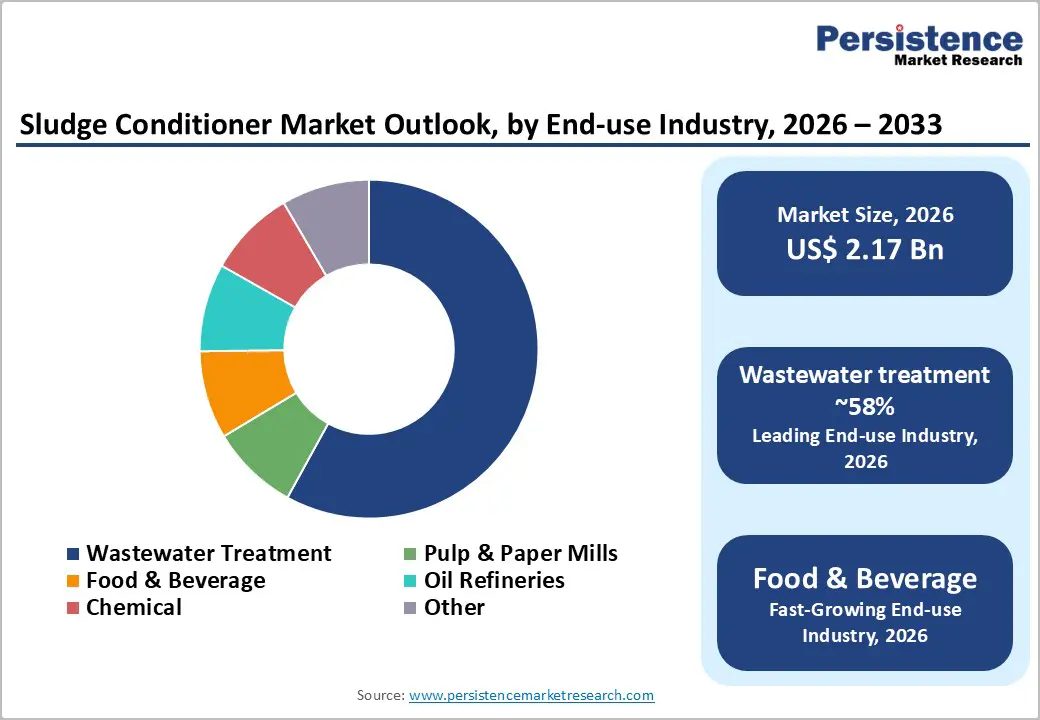

- Fastest Growing Segment: Wastewater Treatment Facilities represent the fastest-expanding end-use industry segment, growing at approximately 7.5% CAGR, driven by population growth, urbanization pressures requiring expanded infrastructure, and increasingly stringent environmental discharge standards requiring advanced treatment technologies.

- Key Market Opportunity: Bio-based and sustainable sludge conditioning solutions present substantial opportunities, with the revised European UWWTD mandating energy-neutral operations by 2045 and increasing demand for biodegradable polymers that achieve 40% biodegradability within 28 days, positioning companies developing sustainable formulations to gain significant market share expansion.

| Report Attribute | Details |

|---|---|

|

Sludge Conditioner Market Size (2026E) |

US$ 2.2 Bn |

|

Market Value Forecast (2033F) |

US$ 3.4 Bn |

|

Projected Growth CAGR (2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

5.8% |

Market Dynamics

Market Growth Drivers

Regulatory Compliance and Environmental Mandates

Stringent environmental regulations serve as the primary catalyst for global sludge conditioner market growth. The revised EU Urban Wastewater Treatment Directive (UWWTD) 2024 introduces mandatory nutrient removal targets and micropollutant treatment requirements for large wastewater treatment facilities, necessitating advanced conditioning technologies to improve operational efficiency. In India, CPCB discharge standards mandate a biochemical oxygen demand (BOD) below 10 mg/L and a chemical oxygen demand (COD) below 50 mg/L, driving the need for optimized sludge conditioning to enhance clarification and dewatering.

Similarly, the U.S. EPA Clean Water Act enforces strict effluent quality norms, stimulating investment in advanced conditioning agents. Additionally, Extended Producer Responsibility (EPR) schemes in Europe incentivize utilities to adopt solutions that minimize sludge volume and disposal costs. Non-compliance results in severe penalties and operational disruptions, compelling operators to prioritize effective conditioning infrastructure and chemical solutions.

Rapid Urbanization and Industrial Growth in Emerging Economies

The Asia-Pacific region is witnessing rapid urbanization and industrial growth, resulting in a significant surge in wastewater generation that necessitates advanced treatment and sludge management solutions. China has emerged as the largest consumer of sludge treatment chemicals, driven by extensive urban development and aggressive wastewater infrastructure upgrades, with nearly two-thirds of its groundwater currently unsuitable for human consumption. Similarly, India’s accelerated sanitation initiatives and an expanding industrial base in sectors such as textiles, chemicals, and food processing are producing substantial sludge volumes that require specialized conditioning.

The ASEAN region reflects comparable trends, supported by the expansion of decentralized wastewater treatment systems for urban and industrial hubs. These dynamics are fueling strong demand for chemical and thermal conditioning technologies, with the regional wastewater treatment equipment market projected to grow at an impressive 8.8% CAGR, significantly outpacing mature markets and creating lucrative opportunities for manufacturers and service providers.

Market Restraints

High Operational Costs and Technical Complexity

Sludge conditioning entails high operational costs and technical complexity, which restricts adoption, particularly among resource-limited municipalities and smaller industrial facilities. Chemical dosing is highly sensitive to parameters such as pH, ionic strength, and sludge composition, requiring continuous optimization and skilled oversight to maintain efficiency. The rising cost of polyelectrolytes and polymer flocculants, often priced higher than conventional inorganic chemicals, creates affordability challenges in developing regions.

Advanced technologies like thermal hydrolysis demand substantial capital investment, specialized equipment, and ongoing maintenance, further straining budgets. Additionally, synthetic polymer flocculants exhibit performance variability under changing feed conditions, necessitating frequent dosage adjustments and monitoring. These factors increase labor and chemical expenses without proportional efficiency gains, discouraging adoption among cost-sensitive operators.

Regulatory Uncertainty and Polymer Environmental Concerns

Emerging regulatory scrutiny over polymer residues in biosolids and the potential environmental accumulation of synthetic flocculants is creating compliance risks and market uncertainty. Variations in regulatory standards across jurisdictions complicate product formulation and market access strategies for manufacturers operating globally. Increasing attention to per- and polyfluoroalkyl substances (PFAS) and microplastics in treated wastewater raises concerns about the long-term safety of polymer-based conditioning agents, potentially leading to future restrictions that could render existing product lines obsolete or necessitate costly reformulation.

Furthermore, alternative disposal methods and advanced thermal treatment technologies that reduce chemical dependence pose competitive challenges, particularly in regions that favor non-chemical approaches. This regulatory ambiguity often results in procurement delays and budget reallocations, suppressing near-term demand as facilities postpone investments pending clarity.

Market Opportunities

Energy Recovery and Thermal Conditioning Technology Integration

The global thermal hydrolysis technology market is forecast to grow, which creates significant opportunities for integrated sludge conditioning and digestion solutions. The revised EU Urban Wastewater Treatment Directive (UWWTD) 2024 mandates energy-neutral wastewater operations by 2045, driving adoption of thermal conditioning technologies that enhance biogas production, reduce sludge volume by 10–25%, and improve methane yields by 10–20%.

Combining anaerobic digestion with optimized conditioning produces stabilized biosolids suitable for agricultural use, aligning with circular economy goals while generating renewable energy to offset operational costs. Leading providers, including Veolia Water Technologies, have secured multi-million-dollar contracts, validating commercial viability. Rising energy costs and growing renewable energy incentives further strengthen the economic case for investing in advanced thermal hydrolysis infrastructure.

Nutrient Recovery and Circular Economy Adoption

Circular economy principles and evolving regulatory frameworks are creating substantial opportunities for sludge conditioning technologies that enable phosphorus and nutrient recovery. Studies indicate that phosphorus recovered from municipal wastewater could meet nearly 50% of Europe’s mineral fertilizer demand, presenting a strong business case for investment in phosphorus-recovery systems and struvite precipitation technologies. Regulations such as the EU Fertilising Products Regulation and emerging soil health directives support the commercialization of biosolids and recovered nutrients, establishing a robust market infrastructure.

Furthermore, Extended Producer Responsibility (EPR) schemes incentivize pharmaceutical and cosmetic producers to fund advanced treatment systems targeting micropollutants, driving demand for specialized conditioning chemistries. Food and beverage manufacturers adopting zero liquid discharge (ZLD) systems require advanced conditioning to reduce sludge disposal costs, with Veolia’s 2024 modular recovery systems validating market potential. Rising agricultural demand for biosolids, coupled with phosphorus supply chain vulnerabilities and growth in organic farming, ensures sustained end-market demand for nutrient recovery solutions.

Category-wise Insights

Sludge Type Analysis

Activated sludge is the predominant sludge type in municipal wastewater treatment, accounting for approximately 45% of the sludge conditioning market. Generated through biological processes, it contains high water content (typically 0.4–1.5% dry solids), colloidal particles, and extracellular polymeric substances that hinder gravity dewatering, necessitating advanced chemical or thermal conditioning before mechanical treatment. The adoption of membrane bioreactor (MBR) technology has introduced reduced-sludge treatment models, producing 40–50% less biological sludge than conventional processes while delivering superior effluent quality. This shift increases demand for specialized, polymer-intensive formulations tailored to MBR sludge.

Primary sludge, formed by physical settling, dewater more easily and requires about 50% less conditioning than secondary sludge, yet contributes roughly 25% to chemical demand. Mixed sludge systems, which combine primary and secondary streams, account for about 10% of the market and require differentiated approaches. The rise of MBR and advanced treatment technologies underscores sludge type segmentation as a key market differentiator.

End-use Industry Analysis

Wastewater treatment facilities remain the dominant end-use sector, accounting for approximately 58% of the global sludge conditioning market value. This leadership is driven by mandatory regulatory compliance and continuous high-volume sludge generation across municipal systems serving urban populations worldwide. The pulp and paper industry, classified as a Red Category sector by India’s Ministry of Environment and Forest, produces significant sludge volumes that require advanced conditioning. Pulp mills generate 0.2–0.6 wet tons per ton of pulp and consume 10–100 cubic meters of water per ton of finished paper.

Industrial food and beverage operations create high-strength wastewater with BOD levels exceeding 1,000–3,000 mg/L, resulting in difficult-to-dewater sludge and fueling an 8.4% CAGR in wastewater recovery solutions. Oil refineries generate hazardous oily sludge, approximately 1 ton per 500 tons of crude processed, necessitating complex chemical conditioning to comply. Chemical and pharmaceutical sectors produce specialized sludges containing heavy metals and synthetic compounds, creating demand for premium conditioning chemicals. Collectively, these industrial segments represent about 42% of market demand and exhibit faster growth than municipal treatment, as operators increasingly prioritize environmental compliance and resource recovery economics.

Regional Insights

North America Sludge Conditioner Trends

North America continues to lead the global sludge conditioning market, supported by advanced municipal infrastructure, stringent regulatory frameworks, and significant investments in wastewater treatment modernization. Compliance with the EPA Clean Water Act and state-level regulations imposes strict effluent quality and sludge handling standards, driving adoption of advanced conditioning technologies and chemical solutions that enhance clarification efficiency and reduce disposal costs. With approximately 30 billion gallons of wastewater treated daily, demand for polymer-based conditioners and thermal treatment technologies remains strong.

Additionally, regional priorities such as water reuse, sustainability, and resource recovery further incentivize investment in innovative conditioning solutions. Industrial sectors, including pharmaceuticals, food and beverage, and oil and gas, generate specialized sludges requiring premium chemicals and integrated treatment systems.

Europe Sludge Conditioner Trends

European markets are undergoing significant regulatory transformation following the adoption of the revised UWWTD 2024, which enforces stricter nutrient removal standards, introduces micropollutant treatment requirements, and sets energy-neutrality targets for wastewater treatment by 2045. These mandates are driving extensive facility upgrades and investments in advanced sludge conditioning technologies that enhance treatment efficiency while reducing energy use and disposal costs. The directive emphasizes circular economy principles, encouraging resource recovery, phosphorus recycling, and biogas generation through integrated thermal hydrolysis and anaerobic digestion systems.

Furthermore, the Extended Producer Responsibility (EPR) framework incentivizes utilities and technology providers to develop innovative solutions for micropollutant capture and nutrient recovery. Growing concerns about phosphorus scarcity and rising agricultural demand for biosolids-derived nutrients are further accelerating investment in struvite precipitation and nutrient recovery technologies. Companies such as Veolia Water Technologies are expanding operations with major sludge line contracts and strategic investments in circular economy-driven treatment solutions.

Asia Pacific Sludge Conditioner Trends

Asia-Pacific is the fastest-growing regional market for sludge conditioning solutions, driven by rapid urbanization, industrial expansion, and significant government investments in wastewater treatment infrastructure. The regional water and wastewater treatment market is expanding at a 7.6% CAGR, with China leading as the world’s largest consumer of sludge treatment chemicals, followed by strong growth in India, Japan, Indonesia, and Vietnam. China’s enforcement of the Water Ten Plan and large-scale facility upgrades create sustained demand for advanced conditioning chemistries, while India’s accelerated sanitation programs and industrial growth in textiles, chemicals, and food processing generate substantial sludge volumes requiring specialized solutions.

Structural advantages, including lower manufacturing costs, rising technology adoption, and greater capital availability, further support market expansion. Strategic investments, such as SNF Group’s US$18 million facility upgrade in Australia (2024) and Veolia’s expansion with mobile and modular treatment systems, underscore growing demand for flexible, scalable solutions. Government initiatives promoting decentralized treatment, wastewater reuse, and circular economy practices will continue to drive the adoption of conditioning technologies enabling biosolids reuse and resource recovery.

Competitive Landscape

Market Structure Analysis

The global sludge conditioner market is moderately concentrated, with leading players maintaining strong competitive advantages through established client relationships, advanced technology portfolios, and integrated service offerings that span equipment supply, chemical solutions, and operational support. SNF Group holds a dominant position as the world’s leading manufacturer of water-soluble polymers, offering over 1,100 specialized products for diverse sludge conditioning applications and maintaining 1,668 active patents, while introducing more than 150 new products annually. Veolia Water Technologies leverages an integrated strategy combining technology development with strategic contract wins across municipal and industrial sectors, supported by multi-billion-dollar investments in acquisitions and platform integration. Market leaders continue to prioritize R&D, with SNF committing over €500 million toward capacity expansion and product innovation. Emerging strategies emphasize digital integration, including real-time monitoring, automated dosage optimization, and predictive maintenance, creating differentiation beyond conventional chemical supply.

Key Market Developments

June 2024: SNF completed a US$18 million facility upgrade at its Lara plant in Australia, significantly expanding regional manufacturing capacity for water-soluble polymers and strengthening supply-chain resilience for Asia-Pacific wastewater treatment operators requiring reliable conditioning chemical availability.

November 2024: Ecolab Inc. acquired Barclay Water Management, a provider of water safety and digital monitoring solutions, for approximately US$ 50 million in annual sales, expanding capabilities for iChlor® Monochloramine System technology and real-time water chemistry monitoring across North American industrial and institutional facilities.

September 2024: Solenis LLC strategically acquired BASF SE's flocculants business, significantly enhancing its specialty chemical portfolio for mining sector applications and solidifying its position as a global leader in polymeric coagulants for wastewater treatment and industrial applications.

Top Companies in the Sludge Conditioner Market

SNF Group (France) - SNF maintains world leadership as the premier manufacturer of water-soluble polymers, offering over 1,100 specialized products and serving treatment applications for over 1 billion people globally. The company operates manufacturing facilities across multiple continents with strategic expansion in Asia-Pacific, maintains 1,668 active patents, and continuously introduces 150+ new products annually to address evolving treatment requirements. SNF's sustained capital investment of €500 million and comprehensive polymer technology platform establishes commanding competitive advantages in municipal and industrial sludge conditioning segments across all geographic regions.

Veolia Water Technologies (France) - Veolia Water Technologies commands market leadership through integrated strategy combining advanced sludge treatment technology development with strategic contract execution across global municipal and industrial segments. The company maintains comprehensive service capabilities spanning equipment engineering, supply, commissioning, and operational support, with recent major contract wins demonstrating continued market dominance. Veolia's focus on circular economy solutions and energy recovery technologies positions the company to capitalize on emerging regulatory requirements mandating integrated sludge conditioning and biosolids management throughout developed economies.

BASF SE (Germany) - BASF operates as a major chemical conglomerate offering diverse water treatment and sludge conditioning chemical solutions serving industrial and municipal applications across all geographic regions. The company leverages extensive chemistry expertise, global distribution infrastructure, and integrated product portfolios to maintain substantial market presence within the polyelectrolyte and flocculant segments critical to sludge conditioning. BASF's investment in sustainable chemistry platforms and emerging treatment technologies positions the company competitively within circular economy-focused market segments.

Companies Covered in Sludge Conditioner Market

- AkzoNobel

- Veolia Water Technologies

- SNF Group

- Ecolab Inc.

- BASF SE

- Solenis LLC

- Kemira Oyj

- Dow Chemical Company

- Kurita Water Industries Ltd.

- Lonza Group

Frequently Asked Questions

The global sludge conditioner market is valued at US$ 2.2 Billion in 2026 and is projected to reach US$ 3.4 Billion by 2033, representing a CAGR of 6.8% during the forecast period, driven by increasing environmental regulations and wastewater infrastructure expansion.

The market is primarily driven by stringent environmental regulations including the U.S. EPA's Clean Water Act, rapid urbanization with 68% of global population projected to live in urban areas by 2050 according to the United Nations, and industrial wastewater generation requiring effective treatment solutions for regulatory compliance.

Activated Sludge represents the leading segment, commanding approximately 45% of market value due to widespread application in municipal wastewater treatment facilities, consistent conditioning requirements, and regulatory mandates emphasizing secondary biological treatment across developed and developing regions.

North America dominates the market with approximately 35% global market value, supported by mature wastewater infrastructure, stringent EPA regulatory standards, and significant municipal and industrial investments in advanced sludge treatment technologies requiring continuous chemical conditioning.

Bio-based and sustainable sludge conditioning solutions represent major opportunities, with the revised European Urban Wastewater Treatment Directive mandating energy-neutral operations and advanced nutrient removal by 2045, driving demand for biodegradable polymers and eco-friendly formulations achieving 40% biodegradability within 28 days.

Major market players include BASF SE, Ecolab Inc., Kemira Oyj, Solenis LLC, SNF Group, Veolia Water Technologies, Dow Chemical Company, Kurita Water Industries Ltd., AkzoNobel, and Lonza Group, collectively controlling approximately 45-50% of global market value through advanced product portfolios and strategic market initiatives.