- Pharmaceuticals

- Compounding Pharmacies Market

Compounding Pharmacies Market Size, Share, and Growth Forecast 2026 - 2033

Compounding Pharmacies Market by Product (Oral Medications, Topical Medications, Mouthwashes, Suppositories), Application (Adults, Children, Geriatric, Veterinary), Therapeutic Area, and Regional Analysis, 2026 - 2033

Compounding Pharmacies Market Size and Trend Analysis

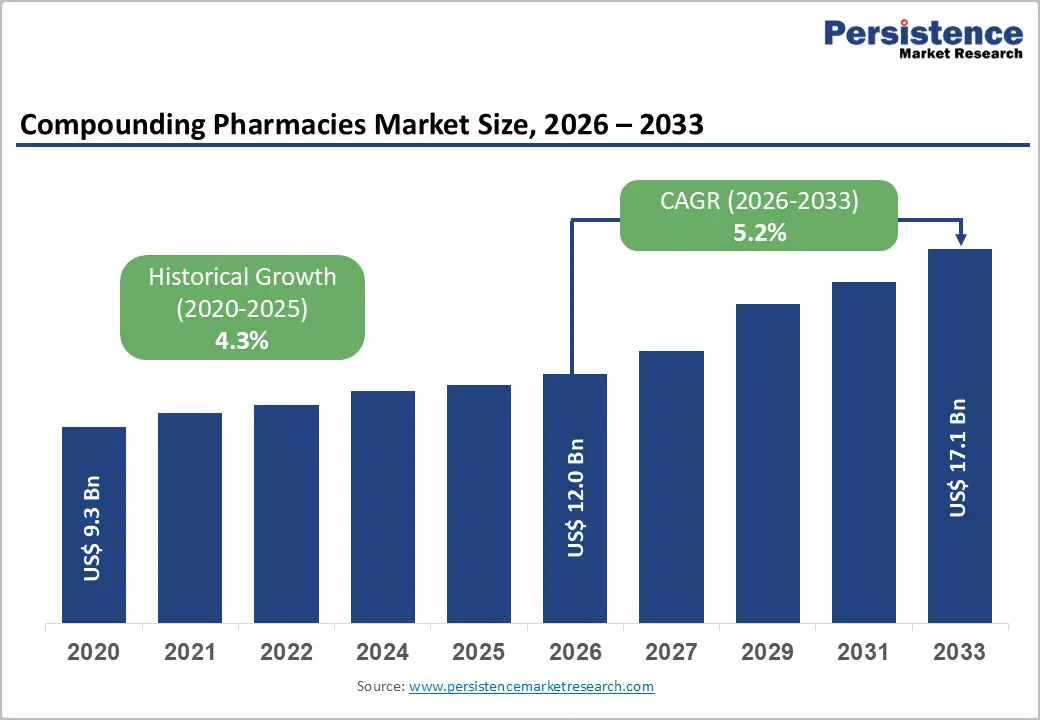

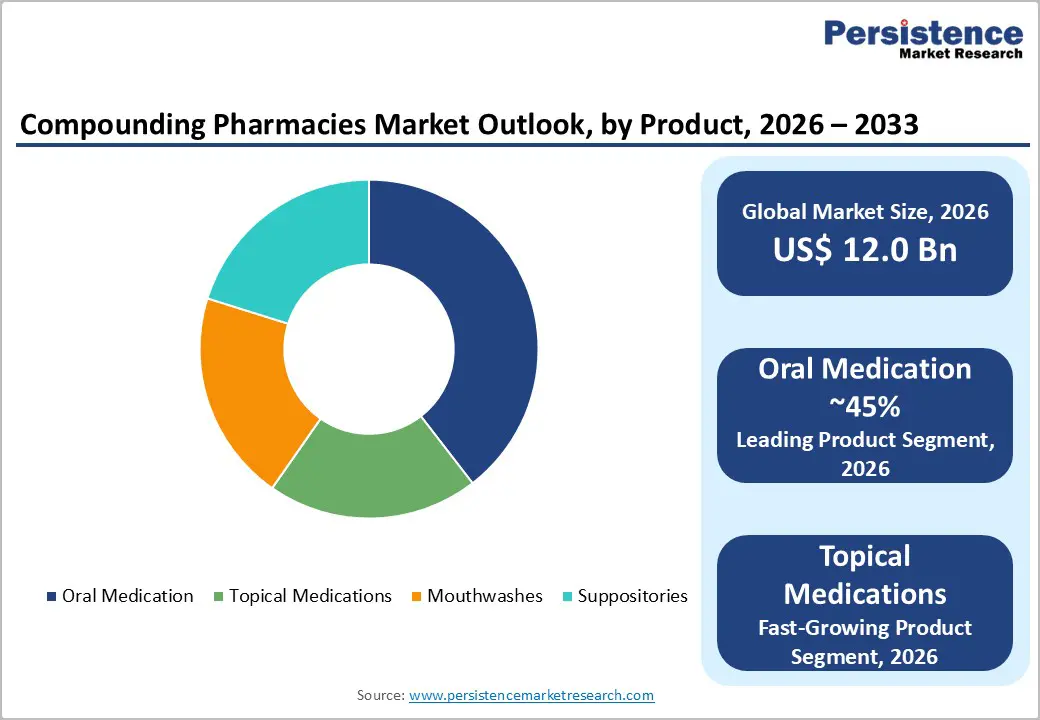

The global compounding pharmacies market size is expected to be valued at US$ 12 billion in 2026 and projected to reach US$ 17.1 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033.

This sustained growth is primarily driven by the increasing clinical demand for personalized medication formulations that address patient-specific needs unmet by commercially manufactured drugs, including dose customization, allergen exclusion, alternative delivery forms, and discontinued drug availability.

The U.S. Food and Drug Administration (FDA) estimates that ~1-3% of all dispensed prescriptions in the United States are compounded medications, with hospital-based and sterile compounding representing the fastest-scaling segments. Simultaneously, the global aging population, rising prevalence of chronic conditions, and expanding veterinary care needs are structurally broadening the patient base for tailored compounded formulations.

Strengthening regulatory frameworks, particularly under Section 503A and 503B of the U.S. Drug Quality and Security Act (DQSA), is professionalizing the sector and expanding institutional confidence in outsourcing facility-prepared compounded products.

Key Industry Highlights

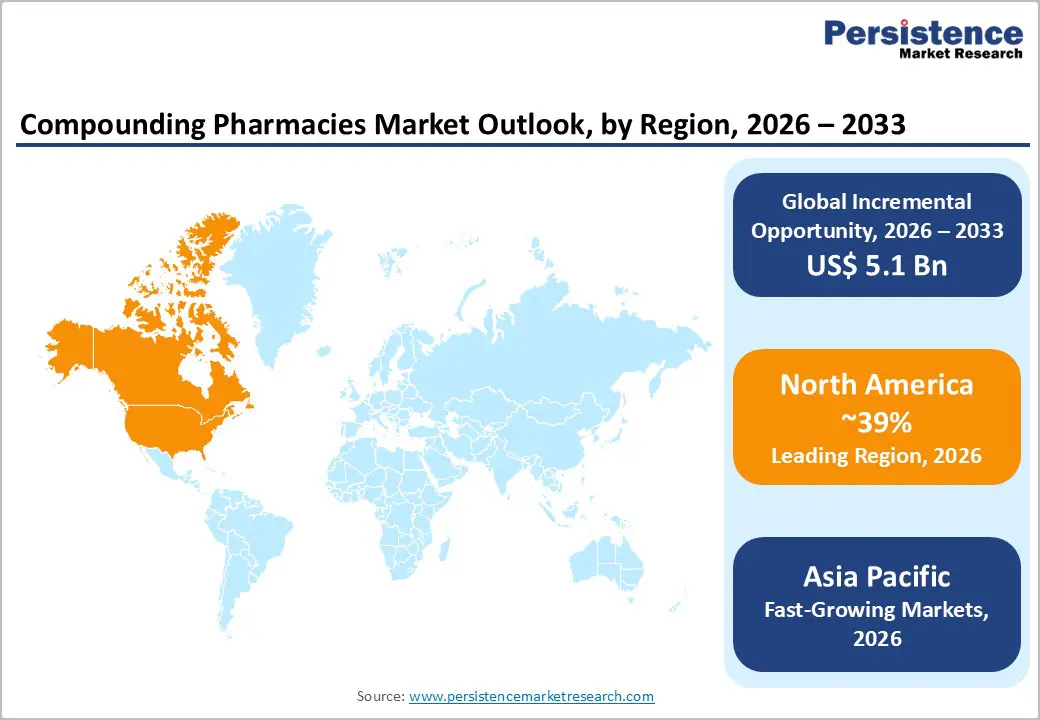

- Leading Region: North America leads the global Compounding Pharmacies market with ~39% revenue share in 2025, underpinned by the FDA's DQSA 503A/503B framework, an estimated 56,000 licensed compounding pharmacies, and high institutional outsourcing demand.

- Fast-Growing Market: Asia Pacific is the fast-growing market for compounding pharmacies driven by China's hospital pharmacy expansion, Japan's geriatric care demand, India's cost-competitive API manufacturing, and rising veterinary care across Southeast Asia.

- Dominant Segment: Oral medications lead the product category with ~45% share in 2026, driven by high-frequency demand for pediatric liquid formulations, geriatric dose modifications, and combination capsules unavailable in commercial products.

- Fast-Growing Product: Topical Medications are the fastest growing product segment, fueled by patient preference for non-systemic delivery, clinical adoption of compounded transdermal analgesics and hormone formulations, and innovation in skin penetration-enhancing base technologies.

- Key Opportunity: Veterinary compounding presents a high-growth commercial opportunity as global pet ownership expands 67% of U.S. households own pets (APPA), creating demand for species-specific, flavored, and dose-appropriate formulations with no commercially manufactured alternatives.

Market Dynamics

Drivers - Rising Demand for Personalized Medicine and Patient-Specific Dosage Formulations

The growing clinical emphasis on personalized medicine is a primary structural driver for the compounding pharmacies market. Commercially available drugs are manufactured in fixed doses and standard formulations that cannot accommodate patients with unique clinical needs, including pediatric patients requiring liquid formulations of adult-only solid drugs, geriatric patients needing lower doses, and individuals with allergies to standard excipients. The International Academy of Compounding Pharmacists (IACP) estimates that over 56 million Americans use compounded medications annually.

The expansion of precision medicine paradigms, endorsed by the National Institutes of Health (NIH) and the FDA's Precision Medicine Initiative, reinforces institutional acceptance of individualized pharmaceutical formulations. As genomic and biomarker-driven prescribing grows, demand for dose-tailored, route-specific, and combination compounded formulations across pain management, hormone therapy, and pediatric care is expected to expand materially.

Commercially Unavailable Drug Shortages and Discontinued Medications

Drug shortages in commercially manufactured products are a persistent and growing driver of compounding pharmacy use. The American Society of Health-System Pharmacists (ASHP) reported that over 300 drug products were in shortage in the U.S. at various points in 2023, encompassing critical sterile injectables, oncology supportive care agents, and pediatric formulations. When branded or generic commercial alternatives are unavailable, FDA-registered 503B outsourcing facilities and traditional 503A compounding pharmacies provide the only legal pathway to supply these essential formulations.

The FDA's drug shortage database consistently lists sterile injectables, including electrolytes, analgesics, and antimicrobials as the most critical compounding-dependent shortage categories, creating durable, non-discretionary institutional demand for sterile compounding services in hospital and ambulatory care settings.

Restraints - Limitations on the Production of Complicated Formulations

Stringent regulatory requirements and GMP compliance remain major restraints for the compounding pharmacies market, particularly in sterile compounding of injectable drugs and intravenous solutions. Pharmacies producing compounded medicines must comply with FDA registration, routine inspections, and USP <797>/<800> standards, which significantly increase operational complexity and costs. The U.S. FDA has also restricted the large-scale compounding of certain medicines, limiting market opportunities for outsourcing facilities and specialty pharmacies.

Restrictions on specific drugs such as bromocriptine mesylate, acetaminophen, aprotinin, and ondansetron hydrochloride have reduced the scope for bulk compounding and negatively affected revenue generation in this segment.

Sterile compounding performed in non-sterile environments creates serious risks of contamination, patient safety issues, and legal liabilities. Injectable compounded medications face stricter sterility labeling requirements and frequent FDA safety warnings, making commercialization more difficult. For example, the FDA issued warnings regarding Becton-Dickinson general-use syringes due to potential interactions with rubber stoppers. Additionally, compounded sterile drugs are more prone to recalls and chemical contamination than conventional pharmaceuticals, causing supply shortages and reducing physician and patient confidence globally.

Opportunities - Veterinary Compounding and Pet Healthcare Expansion in Emerging Markets

The veterinary compounding segment represents a compelling and structurally expanding opportunity, driven by the rapid growth of pet ownership globally and the critical unmet need for species-specific, dose-appropriate pharmaceutical formulations in both companion and large-animal care.

The American Pet Products Association (APPA) reports that ~67% of U.S. households own a pet ~90 million homes with pet healthcare spending exceeding US$ 35 billion in 2023. Veterinary-specific compounded formulations, including flavored oral liquids for cats and dogs, transdermal gels for feline hyperthyroidism, and injectable formulations for large animals, have no commercially manufactured equivalents in many cases. As veterinary care standards rise in Asia Pacific, Latin America, and the Middle East & Africa, the veterinary compounding opportunity will expand significantly beyond the current North American and European market concentration.

Category-wise Analysis

Product Insights

The oral medications segment leads the compounding pharmacies market by product type, accounting for ~45% of total product revenue in 2026. Oral compounded formulations, including custom-dosed capsules, liquid suspensions, chewable lozenges, and lollipops, address the most prevalent clinical customization need: dose modification for pediatric, geriatric, and complex-polypharmacy patients unable to use commercially available dosage strengths.

The IACP identifies oral formulations as the single most frequently compounded product category across traditional 503A compounding pharmacies in the U.S., driven by routine requests for flavored suspensions of antibiotics for children, split-dose capsules for elderly patients, and combination formulations that reduce pill burden. The widespread commercial drug shortage of oral pediatric formulations further reinforces demand, as hospital pharmacies increasingly rely on compounding partners to maintain supply continuity for critical oral medications.

Application Insights

The adults application segment leads the compounding pharmacies market, representing ~38% of application-based revenue in 2026. The adult segment's dominance is driven by the broad range of clinical indications served, including hormone replacement therapy, pain management, dermatology, and treatment of chronic conditions requiring individualized pharmacotherapy. The U.S. Census Bureau estimates that adults aged 18-64 constitute ~60% of the total U.S. population, representing the largest patient cohort for outpatient compounded prescriptions.

The intersection of adult wellness trends including bioidentical hormone therapy and individualized pain management with compounding pharmacy capabilities has generated sustained and high-value demand. However, the Geriatric sub-segment is the fastest growing application, given that patients aged 65+ have the highest prevalence of polypharmacy and dose-modification needs.

Therapeutic Area Insights

The Pain Management therapeutic area leads the Compounding Pharmacies market, accounting for ~42% of therapeutic area revenue in 2025. Compounded pain formulations, including topical analgesic combinations incorporating ketamine, gabapentin, lidocaine, and diclofenac, are widely prescribed for neuropathic pain, musculoskeletal conditions, and post-surgical analgesia where commercially available mono-ingredient preparations are inadequate. The American Chronic Pain Association (ACPA) estimates that over 50 million Americans experience chronic pain daily, with a significant subset requiring individualized multimodal topical regimens available only through compounding.

The ongoing opioid crisis and CDC prescribing guidelines promoting non-opioid alternatives have further accelerated clinician interest in compounded topical analgesics that provide targeted pain relief with minimized systemic exposure and abuse potential.

Regional Insights

North America Compounding Pharmacies Market Trends and Insights

North America dominated the global compounding pharmacies market in 2025, accounting for nearly 39% of total revenue. The region benefits from advanced healthcare infrastructure, high healthcare expenditure, and strong demand for personalized medicines across chronic disease, hormone therapy, dermatology, and pain management applications. Regulatory modernization under the U.S. Drug Quality and Security Act (DQSA) strengthened industry credibility by establishing 503A and 503B pharmacy classifications, improving sterile compounding quality standards and compliance monitoring.

Institutional demand continues to rise as hospitals and specialty clinics increasingly outsource sterile preparation to compliant compounding facilities. Growing elderly populations, expanding biologics utilization, and rising drug shortages are also supporting market expansion. Canada additionally contributes through specialized compounding for pediatric and veterinary applications, while the region’s strong pharmacy network and reimbursement infrastructure continue to sustain high prescription volumes and commercial growth.

U.S. Compounding Pharmacies Market Size

The U.S. represents nearly 90% of North America’s compounding pharmacies revenue, making it the world’s largest compounding market. The country has a highly developed infrastructure supported by approximately 56,000 licensed compounding pharmacies and more than 70 FDA-registered 503B outsourcing facilities. Strong demand for customized sterile injectables, hormone replacement therapies, pain management formulations, and dermatological preparations continues to drive market growth across retail, hospital, and specialty care settings.

The FDA’s DQSA framework significantly strengthened regulatory oversight following prior contamination incidents, leading to increased adoption of compliant outsourcing facilities. Rising chronic disease prevalence, expanding oncology and biologics treatment volumes, and persistent commercial drug shortages are further supporting compounding demand. The growing adoption of veterinary compounding and personalized medicine approaches is also contributing to long-term market expansion across multiple therapeutic areas.

Europe Compounding Pharmacies Market Trends and Insights

Europe is the second-largest compounding pharmacies market globally, supported by strong hospital pharmacy traditions, aging populations, and increasing demand for personalized therapies. The market operates under fragmented national regulatory systems guided broadly by the European Medicines Agency (EMA), while individual member states maintain independent pharmacy compounding laws. Germany, France, and the U.K. collectively account for a major share of regional demand due to their mature healthcare systems and extensive pharmacy infrastructure.

Demand for compounded preparations is increasing across hormone replacement therapy, pediatric medicine, oncology support, dermatology, and pain management applications. Europe is also witnessing greater emphasis on regulatory harmonization, quality assurance, and sterile compounding standards following rising safety concerns. Hospital pharmacies remain central to regional compounding activity, while growing biologics use and shortages of commercial medicines continue to create opportunities for specialized compounding providers across the region.

Germany Compounding Pharmacies Market Size

Germany accounts for nearly 24% of Europe’s compounding pharmacies revenue and maintains one of the continent’s strongest prescription compounding traditions through its Rezeptur system. More than 18,000 community pharmacies operate under strict Apothekenbetriebsordnung (ApBetrO) regulations, enabling pharmacists to prepare individualized formulations for patients requiring customized therapies not commercially available.

The country’s aging population, high chronic disease prevalence, and strong physician acceptance of compounded medicines continue to support market demand. Customized dermatology creams, hormone replacement therapies, pediatric medicines, and pain formulations are among the most commonly prepared products. Germany’s robust reimbursement structure and advanced healthcare infrastructure further strengthen pharmacy-based compounding services, while increasing regulatory focus on sterile preparation quality and patient safety is driving modernization across the sector.

U.K. Compounding Pharmacies Market Size

The U.K. contributes approximately 19% of Europe’s compounding pharmacies market revenue, supported by NHS-backed specials manufacturing and an established unlicensed medicines framework regulated by the MHRA. The market serves growing demand for individualized therapies across pediatrics, oncology support, dermatology, hormone replacement, and rare disease treatment areas where commercial products remain limited or unavailable.

Post-Brexit regulatory divergence has led to updated MHRA guidance regarding pharmacy-prepared medicines and unlicensed specials manufacturing. This evolving compliance environment is creating operational complexity while also benefiting larger specialized operators capable of meeting stricter quality standards. Rising elderly populations, increasing polypharmacy management needs, and persistent shortages of commercial medicines are further driving demand for compounded preparations across hospital and retail pharmacy channels.

France Compounding Pharmacies Market Size

France represents nearly 16% of Europe’s compounding pharmacies revenue, supported by a long-standing legal framework permitting preparation magistrale and officinal compounding across more than 22,000 pharmacies nationwide. French pharmacies regularly provide customized therapies for dermatology, pediatrics, hormone replacement therapy, and pain management where standard commercial formulations may not adequately meet patient requirements.

The country’s aging population and increasing prevalence of chronic diseases continue to sustain prescription demand for individualized medicines. Regulatory oversight from the Agence nationale de sécurité du médicament (ANSM) ensures product quality and patient safety compliance across pharmacy operations. Demand for bioidentical hormone therapy and pediatric dose-adjusted preparations has increased steadily, while ongoing shortages of certain commercial drugs are creating additional opportunities for pharmacy-based customized medication services.

Asia Pacific Compounding Pharmacies Market Trends and Insights

Asia Pacific is projected to be the fastest-growing regional market for compounding pharmacies. Rapid healthcare infrastructure expansion, rising healthcare expenditure, growing chronic disease prevalence, and increasing awareness of personalized medicine are key growth drivers across the region. Countries including China, Japan, India, and Australia are investing heavily in pharmacy modernization and hospital compounding capabilities to improve patient-specific treatment accessibility and pharmaceutical quality standards.

Hospital pharmacy-based compounding remains dominant in many Asia Pacific countries, particularly for sterile injectables, oncology support medicines, pediatric formulations, and traditional medicine preparations. Growing veterinary care demand and increasing pet ownership are also supporting compounding activity. Regulatory authorities across the region are gradually strengthening oversight frameworks to improve quality assurance, sterile preparation practices, and pharmacist training standards, creating favorable long-term opportunities for organized compounding pharmacy operators.

India Compounding Pharmacies Market Size

India represents approximately 12% of Asia Pacific’s compounding pharmacies revenue and is emerging as a high-growth market driven by its large pharmaceutical manufacturing ecosystem and cost-efficient healthcare infrastructure. Compounding activity is expanding across hospital pharmacies, specialty clinics, dermatology, and veterinary medicine applications, particularly in urban healthcare centers where demand for personalized therapies is rising steadily.

The Pharmacy Practice Regulations, 2015, issued by the Pharmacy Council of India, provide the primary regulatory framework governing pharmacy compounding practices. India’s growing chronic disease burden, increasing biologics usage, and rising awareness regarding individualized medicine are supporting market expansion. Additionally, India’s strong active pharmaceutical ingredient manufacturing capabilities position the country favorably for future compounded formulation production and export opportunities across regulated international markets.

Japan Compounding Pharmacies Market Size

Japan accounts for nearly 18% of the Asia Pacific’s compounding pharmacies market revenue, supported by one of the world’s most highly regulated pharmacy systems under PMDA and MHLW oversight. The country’s rapidly aging population is a major demand driver, increasing the need for customized geriatric formulations, dose-adjusted oral medications, topical therapies, and palliative care preparations designed for complex polypharmacy management.

Hospital pharmacies play a significant role in Japan’s compounding ecosystem, particularly in oncology support, pain management, and specialized chronic disease care. High healthcare standards and physician preference for individualized dosing continue to sustain demand for compounded medicines. Additionally, increasing biologics adoption and the need for patient-specific formulations are encouraging further development of advanced sterile compounding infrastructure across major healthcare institutions.

Competitive Landscape

The global compounding pharmacies market is moderately fragmented, with a mix of large multinational sterile outsourcing operators and independent specialty compounding pharmacies. Fagron and Fresenius Kabi AG lead the market through extensive sterile compounding infrastructure, global distribution, and quality-differentiated API sourcing. PharMEDium Services (AmerisourceBergen) and B. Braun Melsungen AG compete strongly in hospital-focused sterile IV admixture compounding.

Key differentiators include 503B regulatory compliance, investment in USP <797>/<800> compliant cleanroom infrastructure, and vertically integrated active pharmaceutical ingredient (API) supply. An emerging trend is consolidation through acquisition, as larger operators absorb compliant independent pharmacies to scale capacity and geographic reach.

Key Developments

- In December 2025, Wolters Kluwer Health launched the Advanced Compounding module for Simplifi 797, enabling pharmacies to meet 2023 USP Chapter 797 requirements with support for high-risk sterile compounding, batch tracking, and beyond-use dating.

- In April 2024, Myonex completed the acquisition of Saveway Compounding Pharmacy to strengthen patient medication supply for clinical trials and expand direct-to-patient and home healthcare provider capabilities.

- In July 2022, Fagron expanded its U.S. sterile compounding footprint by acquiring a 503B outsourcing facility in Boston from Fresenius Kabi AG, including operations, customers, suppliers, around 80 employees, and a supply agreement.

- In March 2021, Osceola Capital and seasoned entrepreneur Jacob Beckel announced the creation of Revelation Pharma Corp. to investigate financing and strategic alliances in the pharmaceutical compounding market.

Companies Covered in Compounding Pharmacies Market

- Fagron

- Fresenius Kabi AG

- PharMEDium Services LLC

- Institutional Pharmacy Solutions

- Cantrell Drug Company

- Lorraine’s Pharmacy

- B.Braun Melsungen AG Company

- Others

Frequently Asked Questions

The global market is estimated to be valued at US$ 12.0 billion in 2026.

Key drivers include rising demand for personalized medicines, persistent drug shortages, and growing patient populations needing customized oral, topical, pediatric, hormone, pain management, and veterinary formulations.

North America leads the market with nearly 39% share, supported by strong compounding infrastructure, FDA-registered 503B facilities, hospital outsourcing demand, and favorable reimbursement systems.

Major opportunities include fast-growing topical medications for pain and hormone therapy, and veterinary compounding driven by rising pet ownership and increasing animal healthcare spending globally.

Leading players include Fagron, Fresenius Kabi AG, B. Braun Melsungen AG, PharMEDium Services, QuVa Pharma, Nephron Pharmaceuticals, Wedgewood Pharmacy, and Cantrell Drug Company.