- Industrial Goods & Service

- Extruders and Compounding Machines Market

Extruders and Compounding Machines Market Trends, Size, Share, and Growth Forecast 2025 - 2032

Extruders and Compounding Machines Market Analysis by Machine Type (Extruding Machines, Mixers, Palletizers, Others), Application (Specialty Plastics, PVC Cables, Flooring Sheet), End-user (Packaging, Building & Construction), and Regional Analysis 2025 - 2032

Extruders and Compounding Machines Market Share and Trends Analysis

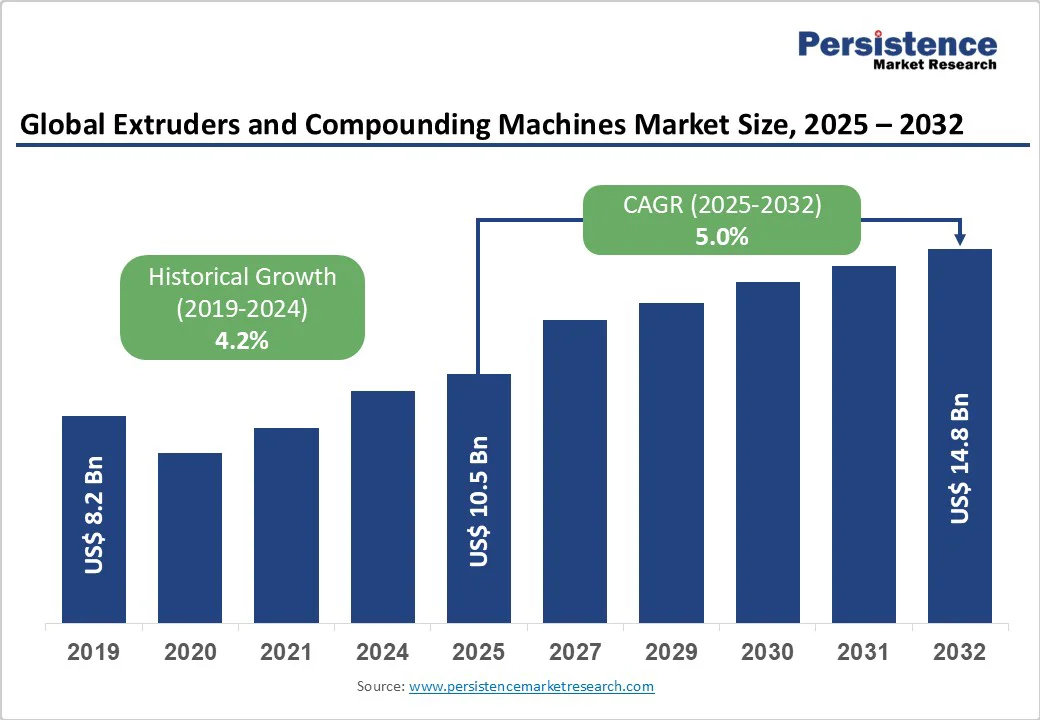

The global extruders and compounding machines market size is likely to be valued at US$10.5 billion in 2025 and is projected to reach US$14.8 billion by 2032, growing at a CAGR of 5.0% between 2025 and 2032.

This reflects robust industry expansion driven by increasing demand from automotive lightweighting initiatives, modernization of the packaging sector, and technological advancements in twin-screw processing capabilities.

Key Market Highlights

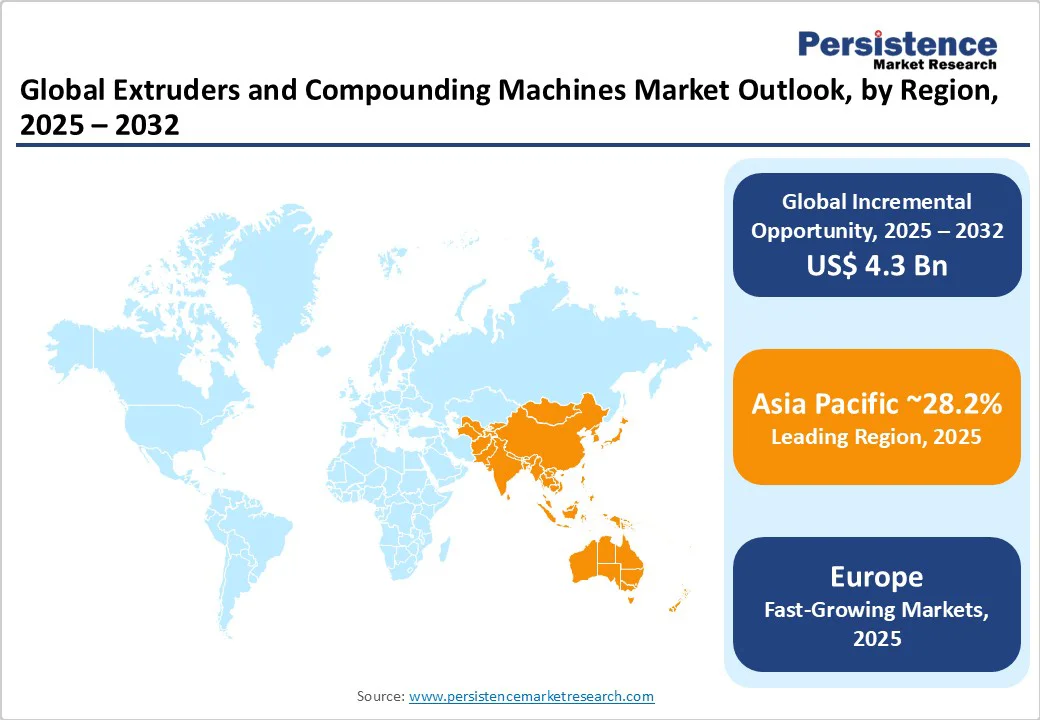

- Leading Region: Asia Pacific leads global market expansion with China achieving 28.2% export growth, becoming the world's largest machinery exporter driven by industrialization and competitive manufacturing capabilities.

- Fastest Growing Region: Europe demonstrates technological leadership through EUROMAP manufacturers controlling 40% of global production valued at €15 billion annually, supported by regulatory harmonization and sustainability initiatives.

- Leading Machine Type Segment: Twin or Multiple Screw extruders command 65% market share through superior mixing capabilities, energy efficiency improvements, and Industry 4.0 integration supporting diverse processing applications.

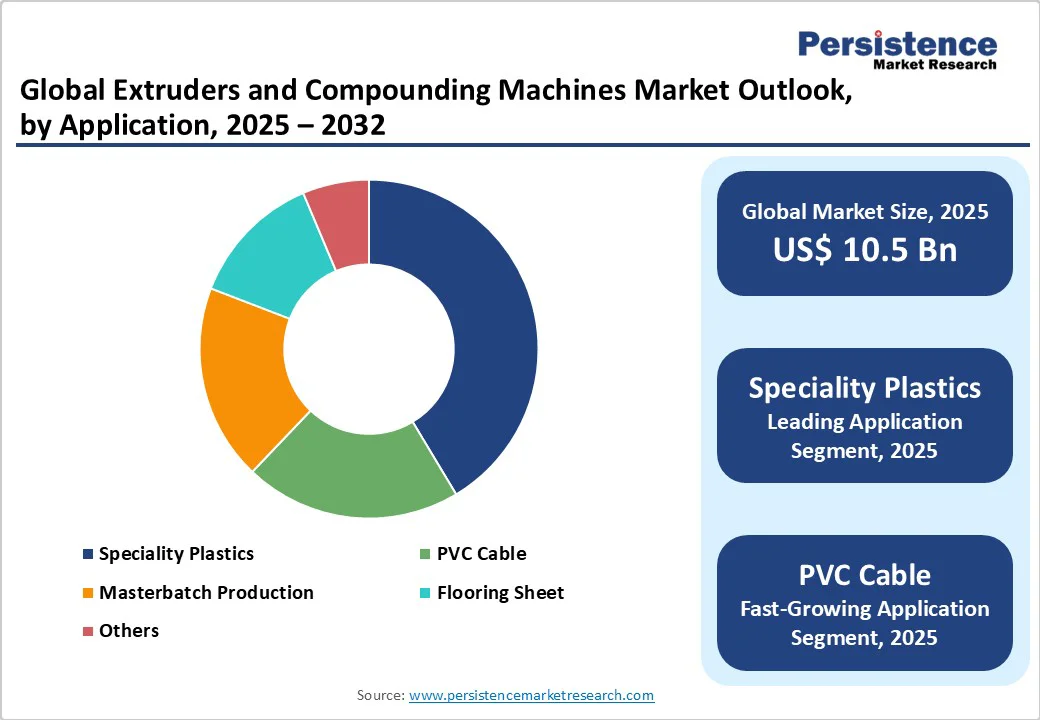

- Leading Application Segment: Specialty Plastics application segment leads with 42% market share, driven by automotive lightweighting trends, electronics miniaturization, and growing high-performance material demand requirements.

- Key Opportunity: Chemical recycling and additive manufacturing convergence present key opportunities with pressure-resistant systems and circular economy principles supporting sustainable manufacturing and innovation initiatives.

| Key Insights | Details |

|---|---|

| Extruders and Compounding Machines Market Size (2025E) | US$ 10.5 Bn |

| Market Value Forecast (2032F) | US$ 14.8 Bn |

| Projected Growth CAGR (2025-2032) | 5.0% |

| Historical Market Growth (2019-2024) | 4.2% |

Market Dynamics

Driver- Expanding Plastic Extrusion Machine Market and Industrial Applications

The expanding plastic extrusion machine market is driven by demand for advanced extruders and compounding machines across healthcare, construction, and consumer goods industries, where plastic extrusion equipment is extensively utilized for producing packaging materials, including sheets, containers, films, and protective barriers.

The automotive industry's strategic transition toward lightweight components to enhance fuel efficiency further accelerates adoption, as manufacturers require sophisticated extrusion systems for processing engineering-grade plastics and composite materials that reduce vehicle weight while maintaining structural integrity and safety standards.

The convergence with additive manufacturing market technologies creates additional opportunities for specialized processing equipment that can handle diverse feedstock materials and complex geometries.

Technological Advancement and Energy Efficiency Integration

Technological advancements in twin-screw extruder systems and Industry 4.0 integration represent significant growth drivers, with manufacturers developing TEX series twin-screw extruders offering superior degassing and kneading performance for direct film and sheet processing applications.

The growing emphasis on energy conservation has intensified demand for energy-efficient machinery, with modern systems delivering up to 20% energy savings compared to conventional equipment through advanced screw design optimization and intelligent control systems.

IoT-enabled monitoring capabilities, predictive maintenance features, and automation integration enhance production efficiency while reducing operational costs, making advanced extrusion systems increasingly attractive to manufacturers seeking competitive advantages in global markets through improved productivity and reduced environmental impact. These systems support the processing of specialty materials, including biodegradable polymers and recycled content, aligning with sustainability objectives across industries.

Restraint- High Capital Investment and Technical Complexity Barriers

High capital investment requirements for advanced extruder and compounding machinery systems create significant barriers for market entry and expansion, particularly affecting small and medium-sized enterprises seeking to upgrade their processing capabilities for competitive positioning.

Modern twin-screw extruders with sophisticated control systems, AI-informed screw design, and specialized material handling capabilities require substantial initial investments that often exceed operational budgets of smaller manufacturers seeking technological advancement. According to U.S.

Bureau of Labor Statistics, employment in extruding and forming machine operations shows 43,140 workers earning an average annual wage of US$ 41,610, while extruding and drawing machine operators number 6,830 with $43,480 average wages, indicating workforce constraints and specialized skill requirements that add operational complexity and training costs for companies seeking to implement advanced processing technologies.

Supply Chain Vulnerabilities and Regulatory Compliance Costs

Supply chain disruptions and regulatory compliance requirements continue challenging market growth, as evidenced by PLASTICS industry data showing 15.4% quarterly decline and 36.2% year-over-year decrease in machinery shipments during Q2 2024, highlighting market volatility and supply chain vulnerabilities.

Complex global supply chains required for specialized components make manufacturers vulnerable to geopolitical tensions and transportation bottlenecks that increase costs and delivery times, particularly affecting the availability of precision-engineered components and control systems.

Additionally, stringent environmental regulations regarding plastic waste management and processing standards increase compliance costs and operational complexity, while the industry faces pressure to develop sustainable processing solutions that may require additional research and development investments without immediate returns, creating financial strain on manufacturers.

Opportunity - Chemical Recycling and Additive Manufacturing Convergence

The expanding additive manufacturing market presents substantial opportunities for extruder manufacturers, as the convergence of traditional extrusion with 3D printing technologies creates specialized application segments requiring customized material processing equipment and innovative feedstock preparation systems.

EUROMAP data indicates that global production of plastics and rubber machinery reached €38.6 billion in 2021, with European manufacturers maintaining leadership positions despite increased competition, demonstrating sector resilience and growth potential across diverse applications.

The chemical recycling sector offers significant expansion opportunities, with companies developing pressure-resistant extruders capable of processing material streams up to 200 bar for applications including pyrolysis oils and advanced recycled materials, supporting circular economy initiatives and sustainable manufacturing practices across diverse industries.

These systems enable processing of previously non-recyclable materials, opening new revenue streams and supporting environmental compliance objectives while meeting growing demand for sustainable material processing solutions.

Category-wise Insights

Machine Type Analysis

Twin or Multiple Screw extruders dominate the machine type segment with approximately 65% market share, driven by their superior mixing capabilities, processing versatility, and energy efficiency advantages across diverse material applications and industrial sectors.

According to EUROMAP industry statistics, European manufacturers maintain technological leadership through advanced twin-screw systems that offer enhanced dispersive and distributive mixing capabilities through AI-informed screw design and CFD-driven reactive extrusion modeling technologies.

These systems excel in processing engineering-grade resins including polycarbonates, polyamides, and specialty compounds while providing energy consumption reductions of up to 20% compared to conventional single-screw configurations, making them particularly attractive for high-performance applications.

The preference for twin-screw configurations reflects industry demands for processing complex materials including recycled content, engineering polymers, and specialty additives that require precise mixing and consistent quality control, supporting applications in automotive, electronics, and medical device manufacturing where material properties are critical for product performance and regulatory compliance.

Application Analysis

Specialty plastics represents the leading application segment with approximately 42% market share, driven by increasing demand for high-performance materials in automotive, aerospace, electronics, and medical device sectors where superior strength, thermal stability, and chemical resistance properties are essential for product performance and safety requirements.

The plastic extrusion machine market growth supports this segment through specialized equipment capable of processing engineering-grade polymers, composite materials, and advanced formulations requiring precise temperature and pressure control throughout the extrusion process.

Global trends including electric vehicle development, electronics miniaturization, and sustainable packaging requirements accelerate specialty plastics consumption, with manufacturers focusing on biodegradable formulations, recycled content integration, and composite materials that demand advanced compounding capabilities and sophisticated processing controls.

The automotive industry's transition toward lightweight components particularly supports specialty plastics growth, as vehicle manufacturers increasingly utilize extruded plastic parts for body panels, interior components, and structural elements that contribute to weight reduction and improved fuel efficiency while maintaining safety standards and durability requirements.

End-user Analysis

The Automotive sector commands the largest end-user market share at approximately 36%, driven by the industry's increasing adoption of lightweight plastic components for enhanced fuel efficiency, emissions reduction, and improved performance characteristics across vehicle platforms and model ranges.

According to U.S. Bureau of Labor Statistics, the plastics product manufacturing sector demonstrates significant employment levels with specialized operators earning competitive wages, supporting automotive applications including dashboard components, door panels, bumper systems, and structural elements that require sophisticated extrusion processing capabilities and quality control systems.

The automotive sector's expansion is further supported by electric vehicle development requirements for specialized plastic components in battery housings, charging infrastructure, and aerodynamic body panels that demand advanced material processing and stringent quality control systems to meet safety and performance requirements.

Packaging represents the fastest-growing end-user segment, benefiting from increasing consumer goods demand, e-commerce expansion, and food safety requirements that necessitate diverse packaging solutions with enhanced barrier properties, sustainability features, and cost-effective production capabilities that support global supply chain efficiency and consumer protection standards.

Regional Insights

North America Extruders and Compounding Machines Market Trends

The United States maintains market leadership in North America through a robust regulatory framework and advanced innovation ecosystem that promotes technological development and sustainable manufacturing practices across diverse industrial sectors and applications.

PLASTICS industry data indicates resilience despite Q2 2024 shipment challenges, with 79.9% of survey respondents anticipating steady or improved market conditions over the next 12 months, demonstrating industry confidence and growth expectations supported by technological advancement and market diversification initiatives.

Davis-Standard's technological leadership exemplifies regional innovation through its January 2024 acquisition of Extrusion Technology Group, including battenfeld-cincinnati, exelliq, and Simplas brands that enhance global competitive positioning and customer service capabilities.

The region's focus on Industry 4.0 integration drives the adoption of smart extrusion systems featuring vibration monitoring, motor parameter analysis, and energy consumption optimization technologies that improve operational efficiency and reduce maintenance costs. U.S. export performance shows plastics machinery exports totaling $341.0 million in Q2 2024, with 53.4% directed to Mexico and Canada, highlighting strong regional trade relationships and manufacturing competitiveness in global markets.

The regulatory environment supports technological advancement through energy efficiency standards and environmental compliance requirements that encourage manufacturers to invest in advanced processing equipment and sustainable production methodologies.

Europe Extruders and Compounding Machines Market Trends

Germany leads the European market through EUROMAP's industry representation of approximately 500 companies manufacturing plastics and rubber machinery across multiple countries, including Austria, France, Italy, Spain, Switzerland, and the United Kingdom, demonstrating comprehensive regional coverage and technological leadership.

EUROMAP statistics demonstrate European manufacturers maintain 40% of global production with annual values reaching €15 billion, supporting export volumes representing 50% of worldwide machinery shipments and technological leadership in advanced processing solutions, including energy-efficient systems and sustainable manufacturing technologies.

The organization's development of OPC UA standardization initiatives enables machine-to-machine communication and Industry 4.0 integration across manufacturing facilities, supporting operational efficiency improvements and quality control enhancement.

European regulatory harmonization emphasizes circular economy principles and environmental compliance, driving investments in chemical recycling capabilities, sustainable processing technologies, and advanced material handling systems that support waste reduction and resource efficiency objectives.

The European Plastics Converters association represents industry interests across approximately 1.6 million employees in more than 60,000 companies generating €360 billion annual turnover, demonstrating sector scale and economic importance across regional economies.

Countries including France, Spain, and the United Kingdom implement advanced digital solutions and automated production systems that reinforce the region's technology leadership position while addressing sustainability requirements through innovative processing capabilities.

Asia Pacific Extruders and Compounding Machines Market Trends

China dominates the Asia Pacific region through rapid industrialization and large-scale manufacturing capabilities that serve both domestic consumption and global export markets across diverse industrial applications and market segments.

EUROMAP statistics show China achieved 28.2% export growth in 2021, reaching €5.7 billion and becoming the world's largest machinery exporter, surpassing traditional leadership positions with competitive pricing and technological advancement capabilities.

The country's manufacturing advantages include cost competitiveness, technological innovation capabilities, and proximity to raw material suppliers that attract substantial investment from global manufacturers seeking production optimization and market access opportunities in growing Asian markets.

India's market expansion is driven by infrastructure development, automotive sector growth, and urbanization trends that increase demand for specialty plastics, cable processing, and advanced manufacturing capabilities across diverse industrial sectors and applications.

CIPET's network of 23 specialized training centers provides critical workforce development through courses in extrusion techniques, injection molding, and plastics processing that support industry expansion and skill development across the country's manufacturing regions.

ASEAN countries, including Thailand, Vietnam, and the Philippines, demonstrate increasing manufacturing capabilities and consumer goods production that support regional market growth through expanding industrial infrastructure, improving technical capabilities, and growing domestic consumption patterns that create demand for advanced processing equipment.

Competitive Landscape

Market Structure Analysis

The extruders and compounding machines market exhibits moderate consolidation with several key players maintaining significant market shares while regional manufacturers contribute competitive dynamics and market fragmentation elements across global and local markets.

Leading companies compete through technological innovation, product customization capabilities, and global manufacturing reach, with continuous research and development investments influencing competitive positioning and market leadership in specialized applications.

EUROMAP represents approximately 1,000 machinery manufacturers across Europe, indicating substantial industry participation while major players leverage advanced engineering capabilities, comprehensive product portfolios, and established customer relationships to maintain competitive advantages.

Companies focus on energy efficiency improvements, Industry 4.0 integration, and sustainable processing solutions as key differentiators, while automation and digitalization enhance operational efficiency and competitive advantages across manufacturing operations, customer service delivery, and global market penetration strategies.

Key Market Developments

- In January 2024, Davis-Standard completed acquisition of Extrusion Technology Group, including battenfeld-cincinnati, exelliq, and Simplas brands, significantly expanding global capabilities and product portfolio for enhanced customer service delivery and technological innovation.

- In June 2024, KraussMaffei showcased advanced machinery solutions at NPE 2024, demonstrating digital solutions for recycling processes and introducing high-performance systems for chemical recycling applications with enhanced sustainability features and operational efficiency improvements.

- In September 2024, EUROMAP elected new leadership to guide plastics machinery sector through digital transformation initiatives, emphasizing sustainability and circular economy principles in manufacturing processes and product development strategies.

Companies Covered in Extruders and Compounding Machines Market

- KraussMaffei, Milacron

- The Japan Steel Works

- NFM Welding Engineers

- BC Extrusion Holding GmbH

- Wenger Manufacturing

- Davis Standard, Extrusion Technik USA

- Graham Engineering, AMUT S.p.A.

- Clextral S.A.S.

- Theysohn Extrusionstechnik GmbH

- Everplast Machinery Co., Ltd.

Frequently Asked Questions

The global extruders and compounding machines market is projected to reach US$ 14.8 billion by 2032, growing from US$ 10.5 billion in 2025 at a CAGR of 5.0%.

Key demand drivers include expanding plastic extrusion machine market growth, increasing specialty plastics applications in automotive and electronics sectors, and rising adoption of energy-efficient processing technologies.

Twin or Multiple Screw extruders lead with approximately 65% market share, offering superior mixing capabilities, energy efficiency improvements, and advanced processing versatility for diverse applications.

Asia Pacific dominates with China becoming the world's largest machinery exporter, while Europe maintains technological leadership with 40% global production share and regulatory advancement.

Major opportunities include additive manufacturing integration, chemical recycling processes, Asia Pacific expansion, and Industry 4.0 technology adoption enabling operational optimization and sustainability initiatives.

Key players include KraussMaffei, Davis-Standard, The Japan Steel Works, Milacron, and WENGER MANUFACTURING, focusing on technological innovation and sustainable processing solutions development.