- Automotive

- Compact Wheel loader Market

Compact Wheel loader Market Size, Share, and Growth Forecast for 2025 - 2032

Compact Wheel loader Market by Powertrain Type (Electric Wheel loader and ICE Wheel loader), Application (Construction, Agriculture, Industrial Waste Handling, Landscaping and Scraping, Forestry and Others), and Regional Analysis for 2025 - 2032

Compact Wheel loader Market Size and Trends Analysis

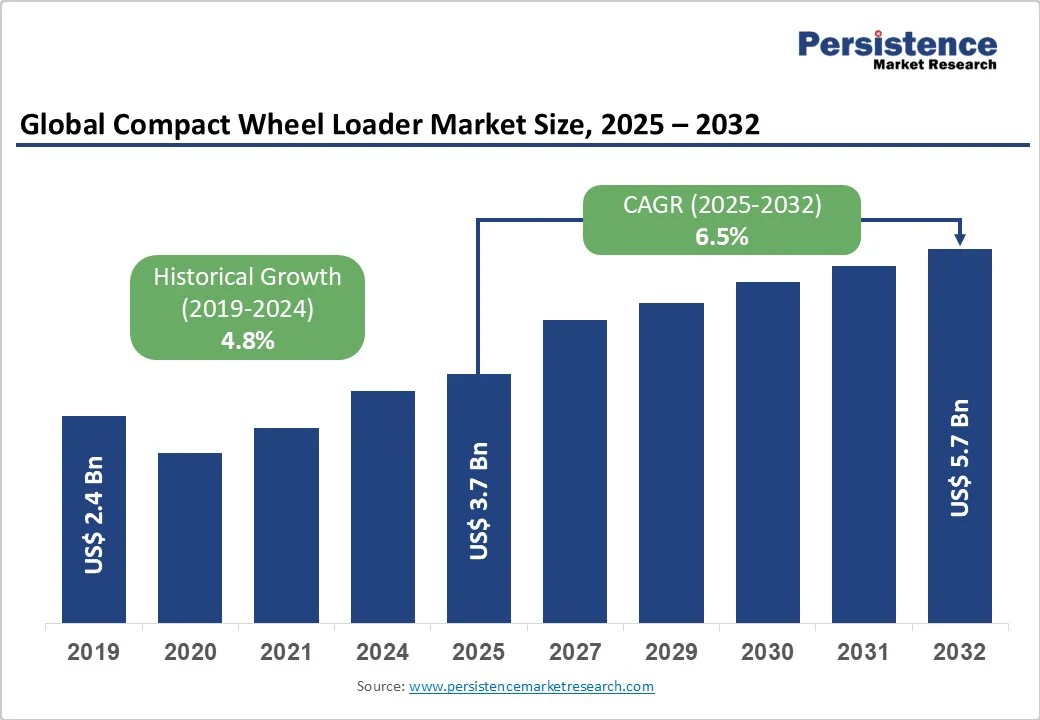

The global compact wheel loader market size is likely to value US$ 3,713.0 Mn in 2025 and is projected to reach US$ 5,749.8 Mn by 2032, growing at a CAGR of 6.5% from 2025 to 2032. The compact wheel loader is a heavy-duty machine used in construction and material handling, featuring a front-mounted bucket operated by hydraulic arms. Its primary functions include loading, lifting, transporting, and dumping bulk materials such as soil, gravel, sand, debris, agricultural products, and construction waste. In the construction industry, wheel loaders play a crucial role in earthmoving, site preparation, backfilling, and loading materials onto trucks.

Key Industry Highlights:

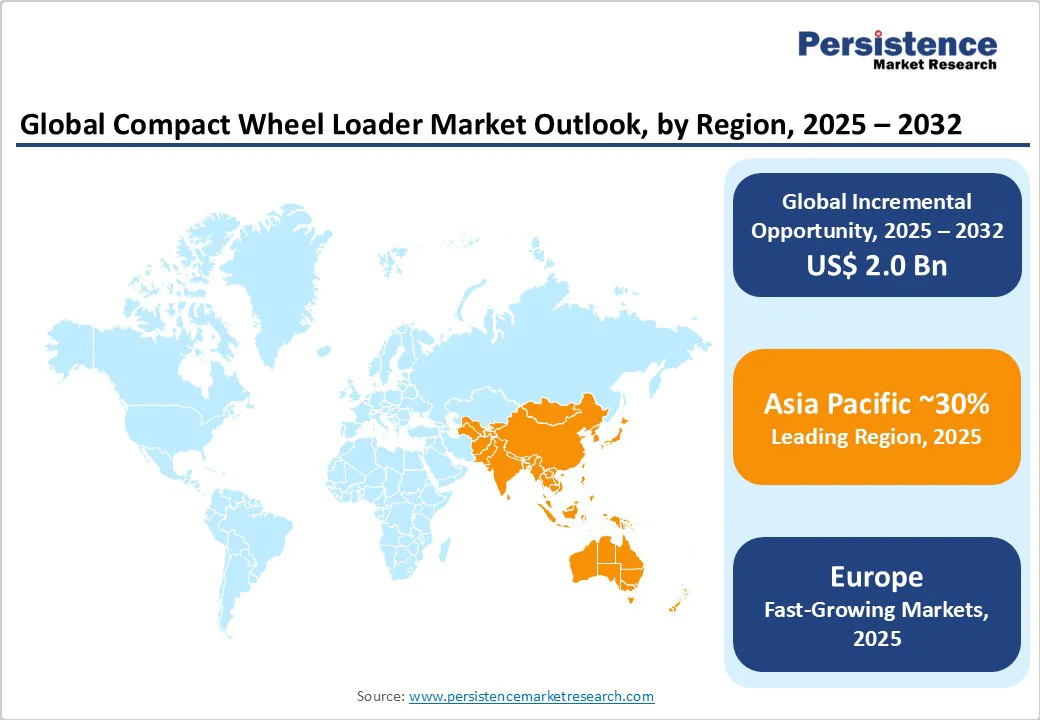

- Leading Region: Asia Pacific is expected to experience strong growth driven by rapid infrastructure development, urbanization, and agricultural mechanization in countries such as China, India, and Southeast Asia.

- In 2025, the 60HP to 80HP segment dominated the Compact Wheel loaders market with a 55% share. This segment’s popularity is driven by its optimal balance of power and efficiency, making these loaders highly versatile for a wide range of applications including construction, landscaping, and agriculture.

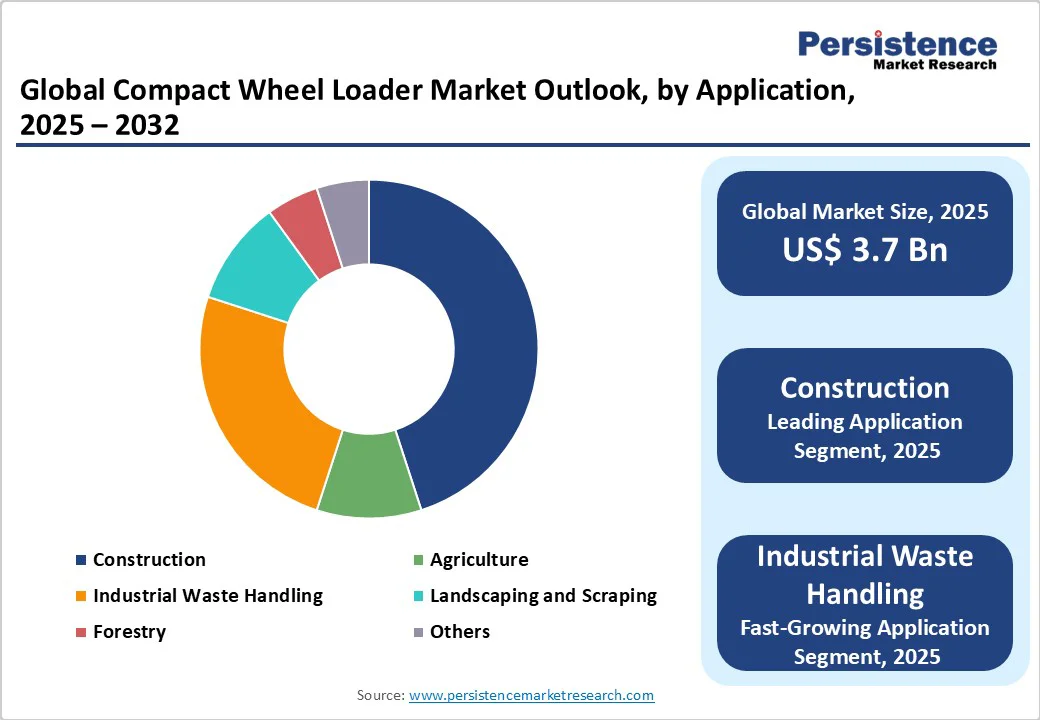

- Leading Application: The construction segment is poised for significant growth in the compact wheel loaders market due to increasing urbanization, infrastructure development, and rising construction activities worldwide. These loaders are favored for their compact size, maneuverability, and fuel efficiency, making them ideal for confined construction sites and urban projects.

| Key Insights | Details |

|---|---|

|

Compact Wheel loader Market Size (2025E) |

US$ 3,713.0 Mn |

|

Market Value Forecast (2032F) |

US$ 5,749.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Dynamics

Driver - Focus on the Adoption of Technologically Advanced Products Items

Manufacturers of loaders are adopting new technology to develop new products and compete in the market. Launching new and innovative products in the market has become a key strategy for manufacturers to gain competitive advantage.

- In 2023, Deere & Company introduced significant advancements to its compact wheel loader lineup by transitioning the 244L, 324L, and 344L models to the new P-Tier series. These P-Tier compact wheel loaders retain the industry-exclusive Articulation Plus™ technology, enhancing maneuverability and stability.

- In Jan 2022, Liebherr launched a new compact loader series with the new L 504 compact model. The most important innovations in this series include the redesigned operator's cab, which provides the operator with excellent visibility thanks to its generous use of glass.

Many market players in the construction vehicle industry are coming up with new compact and sustainable designs. Such new, innovative, and unique machines are boosting the revenue of these companies. Wheel Loaders have seen a significant change in the use of technology in machines over the past few years.

Restraint - Competition from Skid Steer and Backhoe Loaders

In the United States and Brazil, the adoption of compact wheel loaders is restrained by the presence of skid steer loaders and backhoe loaders, that are mostly preferred by construction contractors and fleet operators. These alternative machines offer greater versatility in tight urban environments and are often considered more cost-effective, especially for small- to mid-scale construction tasks. Skid steers, known for their maneuverability and adaptability with a wide range of attachments, dominate the compact equipment category in North America, limiting the demand for compact wheel loaders.

Backhoe loaders, on the other hand, offer dual functionality, excavation and material handling making them highly favored in infrastructure projects across Latin America, particularly in Brazil. Their multi-functional nature reduces the need for deploying multiple machines on-site, offering better value for budget-conscious contractors. As a result, compact wheel loaders often struggle to justify their standalone utility and higher acquisition costs in these competitive environments.

Opportunity - Urban Infrastructure Growth & Infill Development

The rapid expansion of urban infrastructure and the rising trend of urban infill development present a strong growth opportunity for compact wheel loaders. In densely populated cities across Europe, North America, and parts of Asia, the construction focus is shifting inward, targeting previously underutilized or redeveloped urban plots. These job sites require highly maneuverable, space-efficient equipment capable of operating in narrow alleys, sidewalks, and residential zones without compromising on performance.

Compact wheel loaders meet these needs with smaller turning radii, lower operating noise, and multi-functionality through attachments. Their ability to combine lifting, grading, and material handling in tight spaces makes them ideal for road repairs, utility works, and landscaping within city limits. Additionally, municipalities increasingly prefer them for snow removal, park maintenance, and civic infrastructure development.

- Volvo CE, Caterpillar, and Bobcat are expanding their compact ranges for urban suitability. Volvo L20 Electric and L25 Electric are targeted at emission-sensitive zones, offering zero-emission operation with full performance capabilities.

Category-wise Analysis

Powertrain Type Insights - 60HP to 80 HP is expected to Drive High Demand

The 60HP to 80HP segment is expected to drive high demand for compact wheel loaders due to its ideal balance of power, productivity, and efficiency for diverse applications such as construction, landscaping, and agriculture. Leading manufacturers are focusing on this segment with innovative models to meet growing market needs.

- Bobcat’s L95, launched in 2023, features a 74HP engine, a spacious cab, self-leveling bucket, and quick-attach system, enhancing operator comfort and versatility.

This power range offers sufficient Powertrain Type for demanding tasks while maintaining fuel efficiency and maneuverability, making it popular among small and medium enterprises. Additionally, the integration of telematics, smart hydraulics, and electric powertrains is boosting adoption by reducing operational costs and emissions. Market forecasts project steady growth driven by urban infrastructure expansion, precision agriculture, and environmental regulations, positioning the 60HP to 80HP segment as a key growth driver in the compact wheel loader market.

Application Type Insights - Construction to account for a Prominent Market Share

The construction segment holds a prominent share in the global wheel loader market, driven primarily by ongoing infrastructure development and urbanization worldwide. Wheel loaders are indispensable in construction for tasks such as excavation, material handling, site preparation, and loading, making them critical to project efficiency and timelines. The surge in government and private investments in roads, bridges, commercial buildings, and residential projects fuels demand for these machines. Medium-sized wheel loaders, offering a balance of power and maneuverability, are particularly favored in construction applications.

Several industries, including landscaping, forestry, industrial material handling, and mining are contributing to market expansion. For example, in July 2024, the Canadian Ministry of Energy and Natural Resources, together with the Ministry of Energy, Mines and Low Carbon Innovation and the Ministry of Transportation and Infrastructure, announced an investment of approximately USD 195 million to support infrastructure and highway development projects.

Regional Insights

North America Compact Wheel loader Market Trends

The demand for compact wheel loaders in North America is increasing due to several key factors. Rapid urbanization and extensive infrastructure development projects, especially the urgent need to upgrade aging road and bridge infrastructure in the U.S., are major growth drivers. According to U.S. government data, a significant portion of roads and bridges require repair, fueling demand for efficient, versatile machinery like compact wheel loaders in construction and maintenance. Additionally, the agriculture and mining sectors in North America are adopting compact loaders for their maneuverability and efficiency in handling bulk materials.

Manufacturers such as Bobcat and Caterpillar are responding with advanced models that emphasize fuel efficiency, operator comfort, and versatility. For instance, Bobcat’s compact loaders incorporate telematics and hybrid powertrains, aligning with stringent Environmental Protection Agency (EPA) emission regulations pushing for cleaner, electric, and hybrid equipment. Municipalities in cities like New York and Toronto are increasingly procuring electric compact wheel loaders to reduce carbon footprints, further driving market growth.

Europe Compact Wheel Loader Market Trends

The development of the compact wheel loader market in Europe is characterized by the region's dedication to low-emission devices, precision farming, and infrastructure renewal. Cities are becoming more attractive for electric and hybrid compact loaders with Germany, France, and the UK being the largest adopters. Therefore, electric and hybrid compact loaders in urban job locations accounted for more than 18% of the new loader sales in Western Europe while it reflects the impact of the EU decarbonization goals.

Along with the trend of electric vehicles, the agricultural sector is also taking on wheeled loaders with the advanced telematics so that they are capable of tracking productivity, fuel use, and maintenance in real-time. The focus of OEMs lies on ergonomic cab design and automation-ready platforms as both operator comfort and smart farming initiatives are being addressed.

Asia Pacific Compact Wheel loader Market Trends

The demand for compact wheel loaders in the Asia Pacific region is rising rapidly due to accelerated infrastructure development, agricultural mechanization, and industrial expansion in countries such as China, India, and Southeast Asia. Urbanization and smart city initiatives are driving the need for versatile, compact, and fuel-efficient loaders suited for road repair, municipal works, and construction in congested urban areas. Local manufacturers are increasing production of affordable, rugged machines adapted to diverse terrains and climates, meeting the price-sensitive market demand, especially in India where diesel variants remain popular.

Technological advancements such as automation, remote diagnostics, and telematics are enhancing productivity, fueling the adoption of smart loader models. Major manufacturers like Komatsu and Hitachi are actively expanding their presence in the region, offering innovative, durable equipment tailored to local needs. Key factors driving growth include government infrastructure investments, urban construction, agricultural modernization, and rising demand for low-maintenance, efficient machines capable of operating in challenging environments

Competitive Landscape

The global compact wheel loader market is highly consolidated, with organized players holding maximum market share, while regional and unorganized manufacturers hold the remaining. Leading OEMs dominate through technology, service, and global presence. Smaller players compete on price and local manufacturing. As demand grows, market expansion is expected through partnerships, new entrants, and increased production capacity, especially in emerging markets. Innovation and electrification remain key growth drivers.

Chinese companies such as SDLG, Liugong, and XCMG collectively account for over 30% of the market share, reflecting China’s stronghold in the wheel loader segment due to cost competitiveness, domestic demand, and efficient manufacturing capabilities.

Presence of Established OEMs like Wacker Neuson, Hitachi, Caterpillar, Volvo, maintain solid market positions. Their continued emphasis on technology innovation, durability, and global support networks ensures steady demand across developed regions.

Key Industry Developments

- In February 2023, Cat 950 & 962 Next Generation Wheel Loaders introduced standard technologies to boost operator efficiency, consistent bucket fill factors, and up to 10% increased productivity over previous models.

- In January 2025, Next Generation Cat Telehandlers (TH0642, TH0842, TH1055, TH1255), launched to replace previous models, featuring customer-inspired designs, extended service intervals, and enhanced safety features like standard rear-view

- In Jan 2024, Introduced at CES 2024, the RogueX2 is Bobcat's autonomous, all-electric loader concept. Designed as a testing platform for emerging technologies, it emphasizes sustainability and connectivity, aligning with Bobcat's vision for future job-site solutions.

Companies Covered in Compact Wheel loader Market

- Caterpillar Inc.

- AB Volvo

- Wacker Neuson SE

- Doosan Bobcat

- SANY Group

- CHN Industrial

- Tobroco-Giant

- Manitou Group

- Weidemann

- Deere & Company

- Hitachi Construction Machinery Co., Ltd.

- Vermeer Corporation

- JLG Industries

- DIECI Srl

Frequently Asked Questions

The compact wheel loader market is set to reach US$ 3,713.0 Mn in 2025.

Growing Demand for compact and agile loaders in Urban Infrastructure and Municipal Projects are the major growth drivers.

The industry is estimated to rise at a CAGR of 6.5% through 2032.

Development of Emission-Free Compact Machinery, and Urban Infrastructure Growth & Infill Development are the key market opportunities.

SDLG, Liugong Machinery Co., Ltd, Hitachi Construction Machinery Co., Ltd, Schäffer Maschinenfabrik GmbH, Caterpillar are a few leading players.