- Construction & Engineering

- Compact Construction Equipment Market

Compact Construction Equipment Market Size, Share, and Growth Forecast 2025 - 2032

Compact Construction Equipment Market by Product (Track Loaders, Excavators, Backhoe Loaders), Power Output (Less than 40 HP, 40-80 HP, 80-120 HP), Powertrain (Diesel, Natural Gas, Electric/Hybrid), Application, and Regional Analysis 2025 - 2032

Compact Construction Equipment Market Share and Trends Analysis

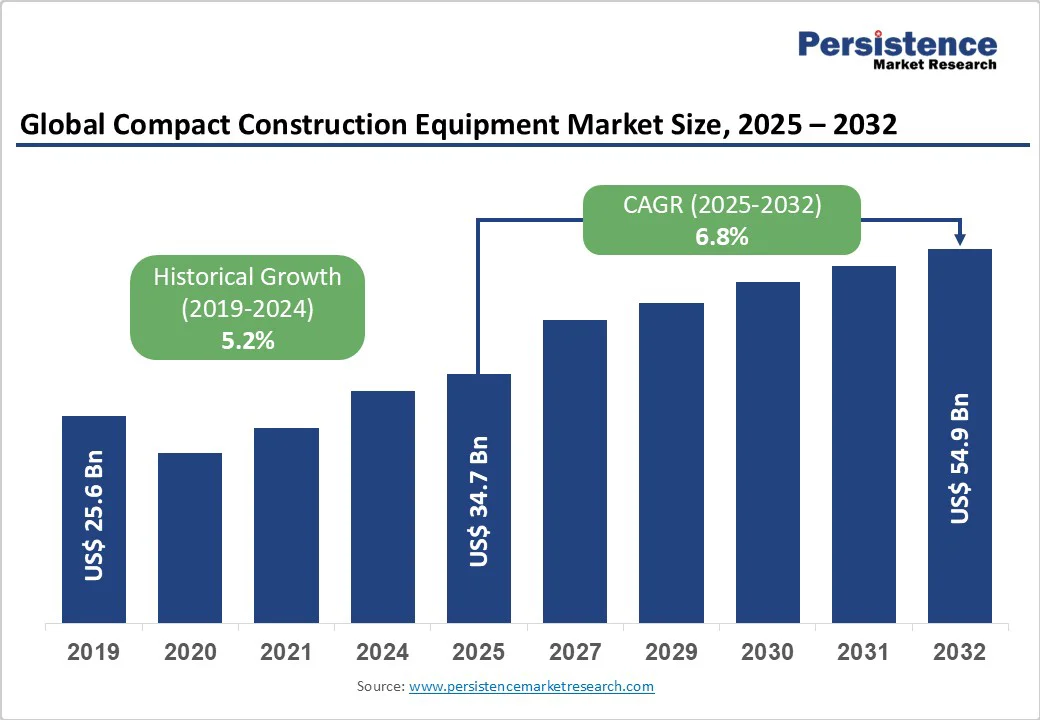

The global compact construction equipment market size is likely to be valued at US$34.7 billion in 2025 and is projected to reach US$54.9 billion by 2032, registering a 6.8% CAGR during the forecast period from 2025 to 2032.

This growth underscores the sector’s resilience, fueled by rapid urbanization, rising infrastructure investments, and innovations that boost efficiency while tackling space constraints.

Demand is especially strong in urban projects where maneuverable, versatile machines are essential. Increasing residential and commercial construction, along with skilled labor shortages is further driving adoption of compact equipment, helping maximize productivity and simplify operations.

Key Market Highlights:

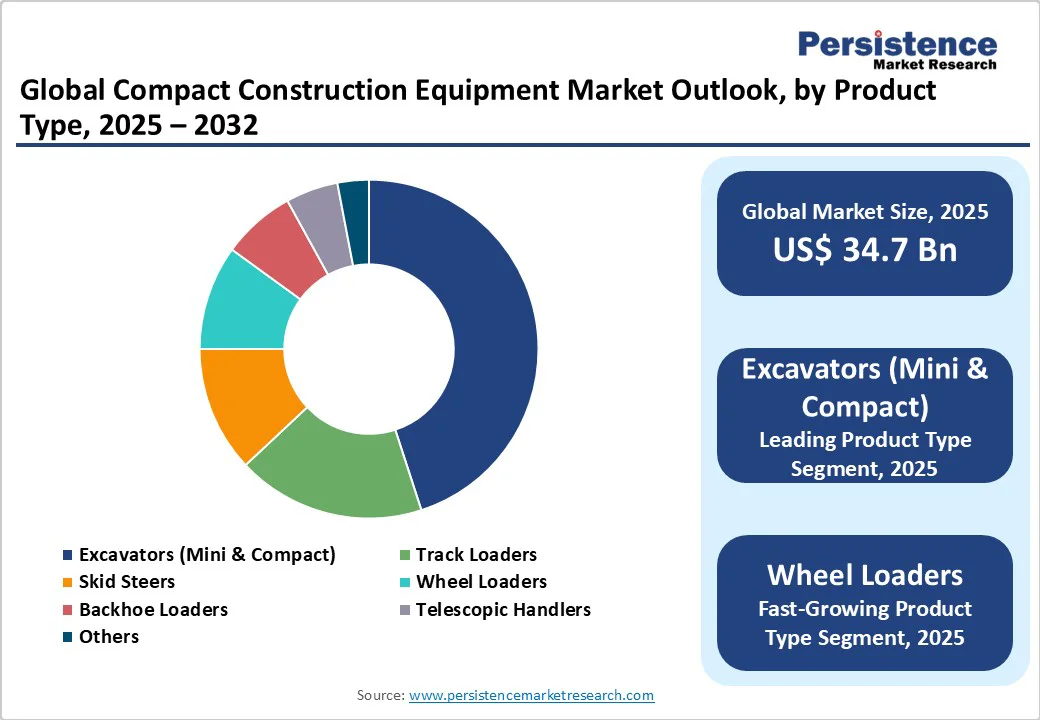

- Leading Product Segments: Mini and compact excavators dominate with over 45% market share; wheel loaders emerge as the fastest-growing segment driven by material handling efficiency.

- Power Output Leadership: Less than 40 HP category holds over 45% market share; 40-80 HP segment demonstrates fastest growth for enhanced capability requirements.

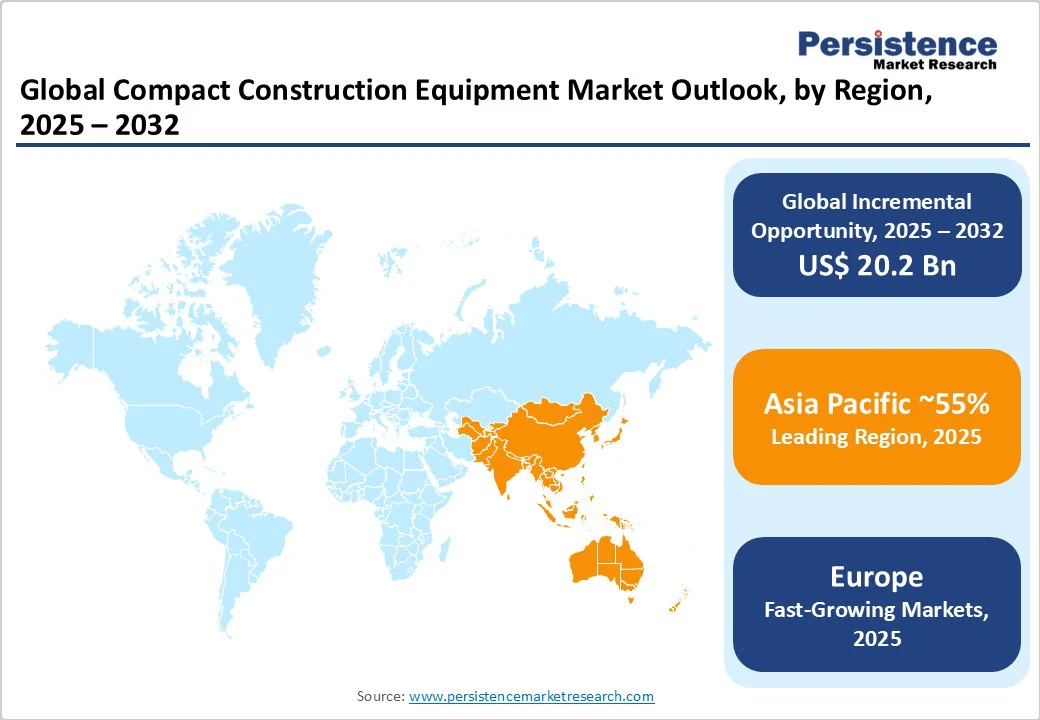

- Regional Market Dominance: Asia Pacific controls over 55% global consumption with China as a major contributor; North America leads in technology adoption and innovation.

- Technology Transformation: Electric/hybrid powertrains represent the fastest-growing category; the electrification market is projected at 20.1% CAGR through 2032.

- Application Growth Drivers: Construction applications maintain 45% market leadership; landscaping emerges as the fastest-growing segment, reflecting green infrastructure emphasis.

- Strategic Market Developments: Leading manufacturers accelerate electrification initiatives, autonomous technology integration, and sustainable equipment solutions addressing environmental regulations and operational efficiency demands.

| Key Insights | Details |

|---|---|

| Compact Construction Equipment Market Size (2025E) | US$ 34.7 billion |

| Market Value Forecast (2032F) | US$ 54.9 billion |

| Projected Growth CAGR (2025-2032) | 6.8% |

| Historical Market Growth (2019-2024) | 5.2% |

Market Dynamics Analysis

Drivers - Unprecedented Infrastructure Investment and Government Spending

Global urbanization is driving significant demand for compact construction equipment, with the United Nations projecting that 68% of the world’s population will live in urban areas by 2050. This shift fuels infrastructure development, requiring machinery that can operate in confined spaces.

Asia Pacific, led by China and India, is advancing massive smart city initiatives, while government programs like the US Infrastructure Investment and Jobs Act and India’s National Infrastructure Pipeline further amplify demand. In 2025, global infrastructure investment hit US$4.4 trillion, led by the US at US$1.3 trillion, China at US$1.6 trillion, and India at US$110 billion, ensuring sustained growth opportunities.

Acute Labor Shortages Driving Equipment Automation

The construction industry is grappling with severe skilled labor shortages, with 85% of firms worldwide reporting difficulty filling positions. This challenge is particularly acute in North America and Europe, where aging demographics further strain workforce availability.

Compact construction equipment mitigates these pressures by allowing single operators to handle tasks that once required multiple workers, supported by advanced operator-assist technologies, telematics, and GPS guidance systems. Simplified controls reduce skill barriers, enabling contractors to sustain productivity despite labor gaps.

With the global construction workforce projected to grow from 220 million in 2020 to 300 million by 2030, demand growth continues to outpace supply, reinforcing equipment adoption.

Accelerated Urban Development and Smart City Initiatives

Modern compact construction equipment integrates advanced technologies such as GPS guidance, telematics, and automated functions that enhance precision, efficiency, and project delivery while maintaining consistent quality standards. The shift toward electric and hybrid powertrains strengthens value by reducing operating costs and ensuring compliance with stricter environmental regulations.

At the same time, accelerating urbanization is fueling significant demand, with Asia-Pacific at the forefront through extensive smart city programs and large-scale urban development missions. These initiatives require specialized equipment capable of operating efficiently in dense environments.

Long-term government infrastructure pipelines and international programs further reinforce sustained growth, making compact equipment a critical enabler of modern construction needs.

Restraint - Supply Chain Disruptions and Material Cost Inflation

Global construction cost inflation reached 6.6% average increase in 2024, with Asia-Pacific experiencing the highest inflation rates, North America at 6.1%, and Europe at 2.8%. Raw material price volatility, semiconductor shortages, and transportation bottlenecks continue to impact equipment manufacturing and delivery timelines.

These challenges result in extended lead times for equipment delivery and increased manufacturing costs, constraining market growth potential. Despite early signs of easing construction cost inflation globally, elevated rates continue to challenge affordability in emerging and price-sensitive markets, particularly across Africa and Asia, where higher costs limit accessibility and slow adoption of new equipment.

Economic Uncertainty and Financing Challenges

Economic uncertainty and rising interest rates are tightening access to equipment financing, especially for small and mid-sized contractors. Global construction activity is expected to contract before returning to growth, highlighting the impact of ongoing economic headwinds.

Residential construction faces added strain, with spending showing sustained declines and multiple months of downturn. These pressures create cautious investment conditions, prompting contractors to delay equipment purchases, particularly across residential and commercial sectors where demand remains subdued.

Opportunity - Electric and Hybrid Equipment Market Transformation

The electric construction equipment market is emerging as the fastest-growing opportunity, driven by supportive policies, environmental regulations, and advances in battery affordability. Adoption is gaining momentum globally, with China accelerating through subsidies and rapid cost parity, Europe pushing demand under strict zero-emission mandates, and North America advancing through federal incentives and corporate sustainability goals.

This transition is reshaping the competitive landscape, creating strong opportunities for manufacturers focusing on battery innovation, charging infrastructure, and electric powertrain development.

Emerging Market Infrastructure Expansion

Rapid infrastructure development in emerging economies, particularly across Asia-Pacific, Latin America, and Africa, is creating substantial growth opportunities for compact construction equipment. Large-scale government programs focused on smart city development, industrial expansion, and national infrastructure pipelines are driving sustained multi-year demand.

These initiatives emphasize urban construction projects where space constraints favor smaller, more maneuverable machinery, positioning compact equipment as a critical enabler. With governments prioritizing modernization and long-term development, demand for versatile, efficient equipment optimized for diverse operating conditions is set to accelerate across these fast-growing markets.

Rental Market Growth and Service Model Evolution

The expanding equipment rental sector provides accessible pathways for contractors to utilize advanced compact construction equipment without major capital investments. This trend particularly benefits regions where project-based construction work predominates over long-term equipment ownership.

Rental models enable technology access for small contractors while reducing ownership risks, effectively expanding the addressable market. The integration of telematics and fleet management technologies enhances rental company operational efficiency while providing customers access to the latest equipment innovations.

Category-wise Insights

Excavators (Mini & Compact) - Market Leadership

Mini and compact excavators dominate the market with over 45% share in 2025, establishing themselves as the most versatile and demanded equipment category. These machines excel in diverse applications, including excavation, grading, demolition, and material handling across various terrain types.

The segment's leadership stems from its ability to operate in confined spaces while maintaining significant lifting capacity and operational precision. Diesel-powered mini excavators dominate due to high torque, power output, and suitability for rigorous outdoor applications, while electric mini excavators represent the fastest-growing segment, driven by demand for low-emission and noise-free equipment in urban construction and indoor projects.

Zero tail swing mini excavators experience rapid growth due to their ability to operate efficiently in confined spaces without rear overhang, making them particularly valuable for urban construction and utility projects.

Wheel loaders represent the fastest-growing product segment, benefiting from their exceptional material handling capabilities and superior mobility across construction sites. These machines offer advantages in material transport and site preparation activities, making them essential for projects requiring frequent relocation of materials and equipment.

Compact wheel loaders are preferred for their lower fuel consumption, operator flexibility, and quick-attach versatility, particularly favored in North America and Europe, where tight urban spaces demand agile equipment.

Power Output Analysis

Equipment with less than 40 HP power output commands over 45% share in 2025, reflecting the preference for highly maneuverable machines in residential and small commercial construction projects. This segment's dominance aligns with urbanization trends where space constraints favor compact, efficient equipment over larger alternatives. The lower power output category offers an optimal balance between operational capability and site accessibility, making it ideal for landscaping, utility work, and residential construction applications.

The 40-80 HP segment emerges as the fastest-growing power output category, driven by contractors seeking enhanced capability without sacrificing maneuverability. This power range provides sufficient capacity for medium-scale construction projects while maintaining the compact footprint essential for urban construction environments.

End-use Analysis

Diesel powertrains maintain market leadership with over 65% share in 2025, reflecting their established reliability, fuel efficiency, and power delivery characteristics. Diesel engines offer proven performance across diverse operating conditions while providing the torque characteristics essential for construction applications. However, this segment faces increasing pressure from environmental regulations promoting cleaner alternatives.

Electric and hybrid powertrains represent the fastest-growing powertrain segment, driven by environmental regulations and operational cost advantages. The compact electric construction equipment market specifically is projected to grow at 13.0% CAGR from 2025 to 2032, reaching US$177.8 billion. Asia Pacific is expected to expand at a rapid CAGR of more than 17.0%, with governments in China, Japan, and South Korea introducing initiatives and subsidies to encourage eco-friendly equipment adoption.

Application Analysis

Construction applications dominate the market with over 45% share in 2025, encompassing residential, commercial, and infrastructure projects. This segment's leadership reflects the fundamental role of compact equipment in modern construction practices, where space constraints and efficiency requirements favor smaller, versatile machinery. The construction segment benefits from sustained infrastructure investment and urbanization trends driving consistent equipment demand.

Landscaping emerges as the fastest-growing application segment, driven by increasing emphasis on green infrastructure and outdoor space development. Urban densification creates demand for professional landscaping services requiring specialized compact equipment for site preparation, material handling, and precision grading operations in restricted access environments.

Regional Insights

North America Compact Construction Equipment Market

North America’s infrastructure spending is creating strong momentum for compact construction equipment demand, supported by large-scale allocations directed toward roads, bridges, and broadband expansion.

The United States continues to dominate the regional landscape with significant long-term investment programs, reinforcing its role as a key growth hub for construction activity. Despite short-term challenges in residential construction spending, commercial segments are showing steady recovery, contributing to equipment demand stability.

Regional market dynamics highlight particular preferences for compact track loaders and mini excavators, reflecting local site conditions and industry requirements. Advanced technologies, including telematics, automation, and electric powertrains, are widely adopted, while the rental market plays a pivotal role in enabling smaller contractors to access modern equipment without heavy capital commitments.

The regulatory environment is equally influential, with stringent emission and safety standards accelerating adoption of clean technology and operator-assist features. Government initiatives such as the Infrastructure Investment and Jobs Act ensure multi-year demand visibility, while the region’s innovation ecosystem supports advancements in autonomous and semi-autonomous machinery, positioning North America at the forefront of global equipment evolution.

Europe Compact Construction Equipment Market

Europe’s infrastructure landscape is being reshaped by historic levels of investment, anchored by the EU Green Deal and major national programs.

In 2025, the region is dedicating vast resources to energy efficiency, climate resilience, and rail electrification, while Germany leads with a landmark multi-year fund aimed at modernizing civil infrastructure and stimulating growth. This expansive package spans bridges, highways, grid upgrades, renewable energy, and defense-related projects, positioning the region for long-term development momentum.

Environmental leadership remains central, with strict emission standards and regulatory frameworks driving strong adoption of electric and hybrid compact construction equipment. Government incentives and Europe’s broader climate agenda reinforce the transition toward clean technologies.

Germany’s fiscal stability provides the capacity for sustained investment, while moderate construction cost inflation compared with global averages supports equipment affordability and demand.

Market recovery is expected to strengthen beyond 2025 as fiscal expansion underpins construction activity. While short-term growth may slow due to political uncertainties, easing monetary policy and favorable financing conditions are expected to support contractors and accelerate equipment purchases, ensuring Europe remains a pivotal hub for advanced construction equipment adoption.

Asia Pacific Compact Construction Equipment Market

Asia Pacific controls over 55% of global compact construction equipment consumption in 2025, establishing unassailable regional market leadership through massive infrastructure development initiatives and manufacturing advantages.

The region benefits from US$2.2 trillion in infrastructure spending in 2025, representing the largest single investment concentration globally. Regional construction equipment markets demonstrate exceptional scale, with Asia-Pacific construction equipment market valued at USD 51.97 billion in 2024, projected to reach USD 114.13 billion by 2033 at 9.13% CAGR.

China dominates regional consumption of mini excavators, which are highly favored for urban construction due to their versatility. Excavators represent 55.28% of the Chinese equipment market, reflecting the country's focus on urban development.

By the end of 2024, Chinese manufacturers will offer nearly 200 zero-emission models, with excavators and loaders making up over 80% of these electric options, driven by government environmental policies. Japan also shows a strong preference for mini excavators, particularly zero tail swing models suitable for space-constrained construction.

The market values advanced technology, with contractors seeking machines featuring sophisticated hydraulic systems and eco-friendly compliance. Government incentives further bolster the demand for electric and hybrid compact equipment.

India has unique demand patterns in construction equipment, with backhoe loaders being the most popular due to their versatility, accounting for nearly 65% of the segment. These machines excel in various tasks like digging, demolition, and material transport, making them ideal for infrastructure projects in both rural and urban areas. Government initiatives like the Smart Cities Mission and Make in India further boost their demand due to cost-effectiveness and operational flexibility.

Competitive Landscape

The global compact construction equipment market exhibits moderate concentration with leading manufacturers maintaining significant market share through technological innovation, global distribution networks, and comprehensive product portfolios.

The market structure reflects intense competition focused on digital services, autonomous operation capabilities, and versatile powertrain options rather than traditional equipment specifications alone. Caterpillar holds approximately 16.3% global market share in the broader construction equipment sector, demonstrating the leadership position of established manufacturers.

Key Market Developments

- In January 2025, Caterpillar introduced five all-new next-generation Cat skid-steer and compact-track loader models (Cat 250, 260, 270 for skid steers and Cat 275, 285 for CTLs), replacing earlier D3-series machines. These machines feature higher lift heights, significantly increased lift and breakout forces, and more torque for better performance, along with a redesigned cab for improved operator comfort and visibility.

- In March 2023, Case Construction Equipment (CNH Industrial) launched a major update to its mini-excavator lineup. The company introduced two new electric mini excavators (the 1.5 t CX15EV and the 2.3 t CX25EV) and one new 4.2 t diesel model (CX42D), broadening its range from 1.5 to 6 t.

- In November 2023, SANY Group rolled out five new small excavator models (SY60C, SY75C, SY80U, SY95C, and SY135C) aimed at Europe and North America. These new SANY machines (ranging roughly 6-13 t) feature upgraded safety and performance (standard rear cameras, improved hydraulics, stronger attachments, etc.) under SANY’s “High-Quality Plan” for global markets.

Companies Covered in Compact Construction Equipment Market

- Caterpillar Inc.

- Komatsu Ltd.

- KUBOTA Corporation

- Deere & Company

- Hitachi Construction Machinery Co., Ltd.

- AB Volvo

- CNH Industrial America LLC

- J.C. Bamford Excavators Ltd. (JCB)

- Doosan Bobcat

- Wacker Neuson SE

- Yanmar Construction Equipment Co., Ltd.

- HD Hyundai Construction Equipment Co., Ltd.

- Liebherr Group

- SANY Group

Frequently Asked Questions

The market is set to reach US$ 34.7 Bn in 2025.

The compact construction equipment market is driven by urbanization, infrastructure investment, and labor shortages, supported by advanced technologies and clean powertrains.

The industry is estimated to rise at a CAGR of 6.8% from 2025 to 2032.

Key opportunities in the compact construction equipment market lie in electrification, emerging market infrastructure expansion, and the rapid growth of rental models that broaden access to advanced technologies.

The major players dominating the global Compact Construction Equipment Market are Caterpillar Inc., Komatsu Ltd., KUBOTA Corporation, Deere & Company, Hitachi Construction Machinery Co., Ltd., AB Volvo.