- Automotive

- Compact Loaders Market

Compact Loaders Market Size, Share, and Growth Forecast 2025 - 2032

Compact Loaders Market Analysis By Operation (Wheel Loader, Track Loader), Power Source (Diesel, Electric/Hybrid), Design (Backhoe Loaders, Skid-steer Loaders, Mini-track Loaders), Engine Power, and Regional Analysis 2025 - 2032

Compact Loaders Market Share and Trends Analysis

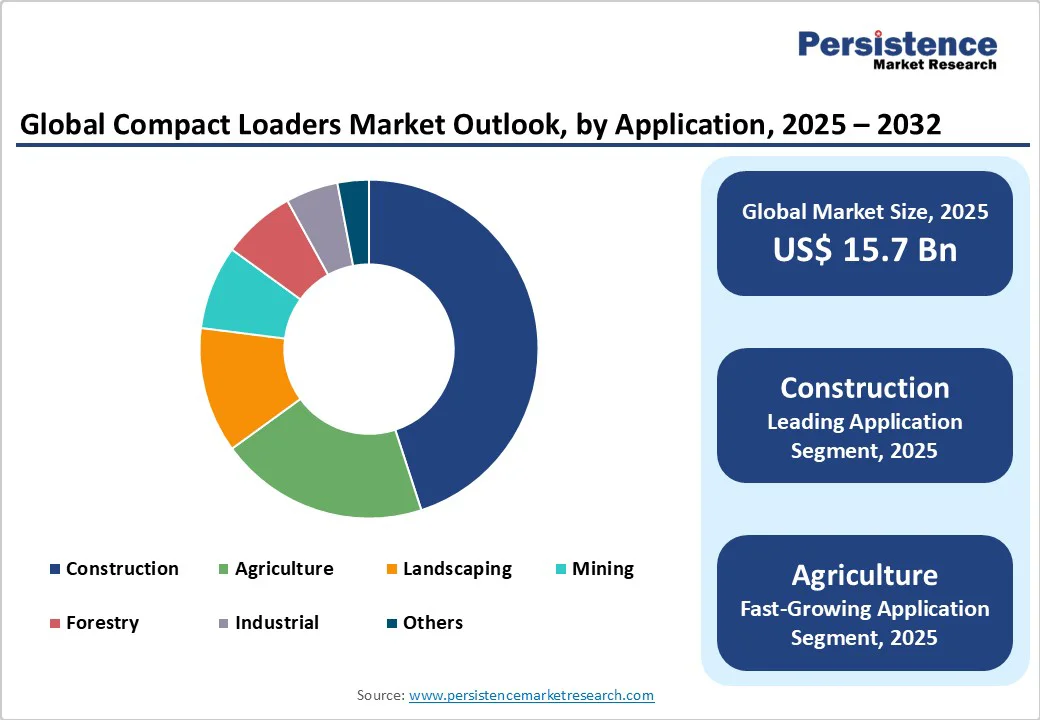

The global compact loaders market size is likely to be valued at US$15.7 billion in 2025 and is projected to reach US$22.7 billion by 2032, growing at a CAGR of 5.4% between 2025 and 2032.

Driven by robust urban infrastructure investment and rental fleet modernization, compact loaders are increasingly favored for their maneuverability in confined worksites. Tighter emission regulations under the U.S. EPA Tier 4 Final and EU Stage V have prompted OEMs to innovate low- and zero-emission platforms, thereby boosting demand for electric and hybrid models in urban and noise-sensitive areas.

Key Market highlights

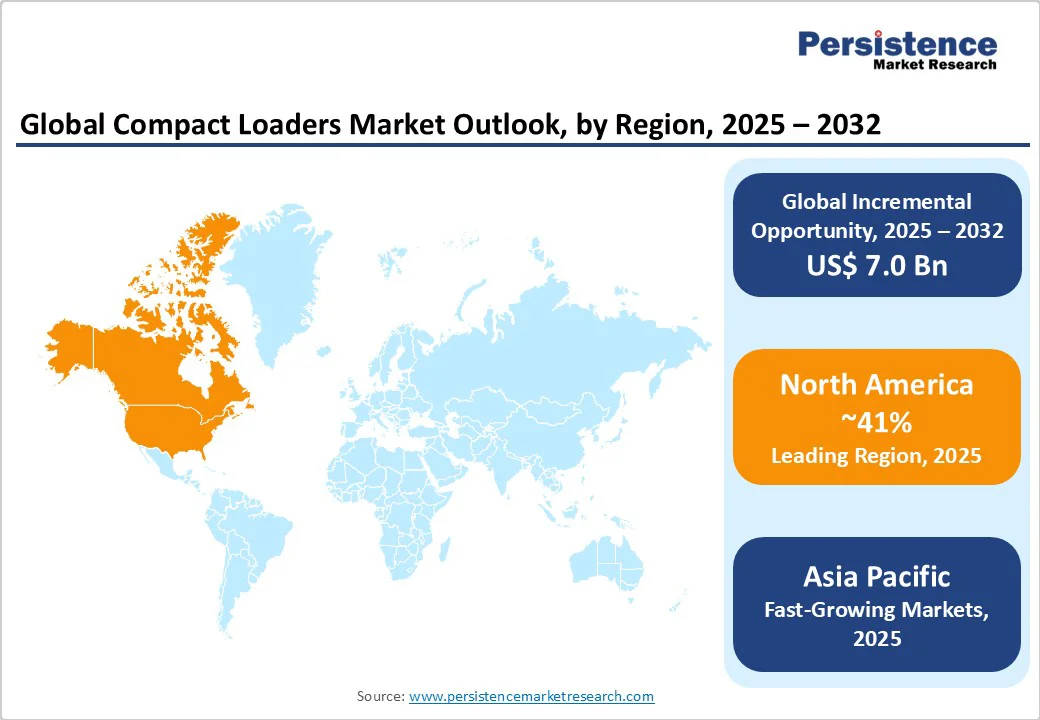

- Leading region: North America remains dominant due to substantial construction spending, mature rental networks, and advanced dealer ecosystems.

- Fastest Growing Region: Asia Pacific outpaces other regions, driven by large infrastructure investments, cost-competitive local manufacturing, and agricultural modernization.

- Dominant Segment: Track loaders lead operations with 54% share, propelled by superior traction, flotation, and rental utilization.

- Fastest Growing Segment: Electric/hybrid power sources expand rapidly from 8%, fueled by urban decarbonization mandates and municipal procurement.

- Key Market Opportunity: Rental-centric electrification combined with telematics-enabled service bundles unlocks new lifecycle revenue streams and accelerates deployment in regulated urban zones.

| Key Insights | Details |

|---|---|

| Compact Loaders Market Size (2025 E) | US$15.7 Bn |

| Market Value Forecast (2032 F) | US$22.7 Bn |

| Projected Growth CAGR (2025-2032) | 5.4% |

| Historical Market Growth (2019-2024) | 4.9% |

Market Dynamics

Driver - Urban Infrastructure Investment and Rental Penetration

Global urban renewal programs, roadway expansions, and utility upgrades are significantly increasing demand for compact loaders, which are valued for their ability to maneuver effectively in confined job sites.

Municipal and industrial landscaping activities have expanded at double-digit growth rates in Europe and North America, prompting contractors to upgrade their fleets to newer models. Compact track and wheel loaders are favored because they combine power, agility, and versatility, supporting both construction and maintenance projects.

Rental penetration has become a key growth catalyst, with mature regions reporting rates above 60% for compact machinery. Rental houses prefer compact track loaders for soft-ground applications, which show 20% higher utilization compared to wheel loaders.

This trend supports continuous technology upgrades, providing operators with access to advanced features such as telematics and automation. It also strengthens OEMs’ recurring revenue streams, aligning with the wider equipment sector’s shift toward fleet optimization and high machine utilization.

Digitalization and Telematics-Enabled Services

The integration of digital tools and telematics in compact loaders is transforming equipment lifecycle management. Real-time monitoring of fuel use, engine hours, and component health supports predictive maintenance, cutting unplanned downtime by around 15% and extending component life by up to 20%. These advances ensure higher reliability and cost-efficiency, which are increasingly vital in urban infill and renovation projects where scheduling margins are tight.

Rental firms and OEMs are also innovating with usage-based billing and uptime-guarantee contracts, already adopted by more than 40% of tier-one rental providers. Such service models provide predictable operating expenses for contractors while building recurring service revenue for OEMs.

Operator-assist features, such as return-to-dig and auto-leveling, further improve jobsite productivity by as much as 12%. This reflects the broader equipment industry’s shift toward connected solutions that provide end-to-end visibility, efficiency, and value.

Restraints - High initial investment for electrified models

The transition toward electric and hybrid compact loaders faces cost-related hurdles. These models often carry a 30%-40% premium over conventional diesel units, limiting adoption among small and medium-sized contractors. In addition to vehicle purchase prices, infrastructure investment adds complexity to the process. Charging solutions require high-capacity stations and grid upgrades, which can increase yard retrofitting costs by around 10%. This capital intensity slows fleet electrification despite environmental and regulatory benefits.

Rental operators also struggle with non-standardized charging protocols, leading to fragmented deployment. Many yards continue to rely on diesel-powered platforms that meet Tier 4 Final standards, favoring proven reliability and reduced upfront expenses. Until total cost-of-ownership analysis shows consistent payback within five years under high-usage rental models, contractors and rental firms remain cautious. This hesitancy delays widespread adoption of battery-electric compact loaders in both developed and emerging markets.

Heterogeneous emissions regulations

Compact loader OEMs face mounting challenges due to the fragmented nature of emissions regulations worldwide. Standards such as EPA Tier 4 Final in the U.S., EU Stage V, and new in-use testing measures in Asia require distinct engineering solutions.

Each regulatory framework requires customized aftertreatment technologies, calibration strategies, and lengthy certification processes. These demands inflate research and development costs by up to 20% while slowing product launches, eroding OEM profitability and delaying market responsiveness.

For rental houses, compliance adds operational burdens. Relocating fleets across borders involves navigating complex documentation and regulatory discrepancies, which restricts equipment mobility. This reduces flexibility in meeting shifting demand across regions.

OEMs and rental operators alike must contend with prolonged approval cycles and additional compliance costs, which hinder ROI. As emissions regulations continue to evolve, regulatory heterogeneity remains a significant obstacle to scaling compact loader operations globally.

Opportunities - Electrification in Urban and Sensitive Zones

Zero-emission mandates enacted by major cities, including Oslo, London, and Los Angeles, are driving municipal and rental procurement of battery-electric compact loaders. These electric units deliver up to 50% noise reduction and eliminate local particulate emissions, satisfying stringent urban deployment restrictions.

In the Compact Electric Construction Equipment Market, early deployments in municipal landscaping and indoor materials handling report payback periods of under five years due to lower energy and maintenance costs. As low-emission zones expand, OEMs and rental houses can establish charging ecosystems and service-based contracts, capturing first-mover advantages in this high-growth niche.

Aftermarket Telematics and Service Bundles

As rental providers and contractors seek to stabilize fleet economics amid tight margins, bundled service offerings present a high-value opportunity. By pairing telematics-driven uptime guarantees with usage-based maintenance subscriptions and digital operator training, OEMs can secure multi-year contracts that account for an average of 15% of machine revenue.

These integrated packages enhance asset availability, reduce lifecycle costs, and strengthen customer loyalty. Regions with rental penetration above 60%, such as North America and Western Europe, are particularly receptive, offering fertile ground for scaling subscription-based models and retrofitting existing diesel fleets with telematics hardware.

Category-wise Insights

Operation Analysis

Track loaders hold an estimated 54% share in 2025, largely due to their performance on soft, uneven, or inclined terrain. Their superior flotation and traction minimize ground disturbance, which is critical for landscaping, forestry, and agricultural applications. Contractors operating in wet or loose soils prefer track loaders due to their stability and ability to maintain productivity even in challenging ground conditions.

Rental fleet financing data shows track loaders deliver 20% higher utilization rates than wheel loaders, reflecting their growing appeal. Recent product innovations in the 60-80 HP range integrate advanced hydraulics and operator-assist features, resulting in a 12% reduction in cycle times. This reinforces their dominance, aligning with demand in the Construction and Mining Equipment Market for terrain-adaptable, high-value machinery.

Power Source Analysis

Diesel dominates as the primary power source, accounting for nearly 92% of the compact loader share in 2025. Contractors and rental firms prefer diesel because of established Tier 4 Final engine reliability, existing refueling infrastructure, and widespread dealer support networks. Diesel units remain critical for remote projects and long-duration operations where charging solutions are impractical.

Electric and hybrid loaders are gradually gaining market share, representing 8% of shipments. These machines are particularly suited for noise-sensitive urban sites and indoor environments. Municipal ESG initiatives and corporate decarbonization goals are expected to accelerate adoption, pushing electric/hybrid penetration toward 20% by 2032. OEMs are expanding electric portfolios and working to standardize charging infrastructure, positioning themselves for this upcoming transition.

Design Analysis

Skid-steer loaders maintain around a 31% share in 2025, valued for their compact footprint, tight turning radius, and versatility with more than 50 attachments. From buckets and augers to trenchers and grapples, their hydraulic adaptability makes them a preferred choice across agriculture, small construction, and industrial maintenance. These features provide unmatched flexibility for contractors handling diverse workloads.

Recent advances in hydraulic systems and ergonomic cab designs have boosted operator efficiency while reducing fatigue. Productivity gains of up to 15% have cemented skid steers as a staple in rental fleets and small-scale projects. Despite the expansion of track loaders, skid steers remain indispensable in high-density areas, where maneuverability and quick attachment changes are essential for jobsite productivity.

Engine Power Analysis

The 60-80 HP engine category accounts for approximately 38% market share, balancing hydraulic output with ease of transport. This segment is favored because it provides sufficient power for widely used attachments such as snow blowers, pallet forks, and sweepers while maintaining efficient fuel consumption of around 5 L/h. Its efficiency makes it the most versatile option for contractors.

Advanced features, such as programmable load-sensing valves, return-to-dig, and auto-dig, enhance cycle times and operator accuracy, reducing task duration by up to 15%. North American rental data shows this category alone generates over 40% of total rental hours. Its dominance reflects its role as the backbone of mixed-fleet operations, combining productivity with affordability in compact equipment.

Application Analysis

Construction leads with about 45% market share, driven by non-residential and civil projects alongside heavy investment in infrastructure upgrades. Compact loaders are essential in earthmoving, trenching, and handling materials within constrained urban sites. Rental fleet turnover for the construction sector is 25% faster than for other sectors, driven by diverse attachment needs and frequent job site relocations.

Agriculture follows with nearly 20%, supported by applications in feed handling, barn cleaning, and bale management. Landscaping and industrial maintenance each account for 12%, reflecting widespread use in snow removal, lawn care, and facility upkeep. Smaller shares come from forestry, mining, and other segments, which leverage loaders’ versatility and transportability, ensuring their adoption across varied industrial and commercial applications.

Regional Insights

North America Compact Loaders Market Trends

North America continues to dominate the compact loaders market, with the U.S. serving as the primary driver of regional demand. Monthly non-residential construction spending has consistently exceeded US$1,300 billion during 2024-2025, fueling equipment utilization in urban and infrastructure projects.

High rental penetration rates over 65% encourage frequent fleet replacement, enabling rental operators to trial electrified models while gradually building charging-enabled yards. Mature Tier 4 Final diesel regulations have also advanced powertrain efficiency and reliability, ensuring continued relevance for diesel-powered loaders.

Federal and state incentives are reducing adoption barriers for electric and hybrid loaders, while rental houses and OEMs increasingly offer uptime guarantees and telematics-enabled service contracts. These innovations boost equipment availability by nearly 15% while lowering overall ownership and operating costs. The strength of North America’s dealer networks, combined with supportive financing and advanced service models, cements its leadership in the global Construction Equipment Market.

Europe Compact Loaders Market Trends

Stringent regulatory frameworks and strong momentum toward electrification define Europe’s compact loaders market. The Stage V emission standard, which includes particle number limits and in-service monitoring, has prompted OEMs to introduce ultra-clean diesel platforms and modular electrified powertrains.

Urban low-emission zones in cities such as London, Paris, and Milan now require zero-tailpipe machinery for municipal projects, resulting in annual sales growth of electric loaders exceeding 30%. Germany and France continue to drive demand for advanced diesel models, whereas Norway and the Netherlands lead in electric vehicle adoption, with penetration levels exceeding 15%.

OEMs in Europe compete through innovative attachment ecosystems, shared charging solutions, and telematics integration tailored to fragmented national regulations. These strategies enable equipment providers to cater to diverse customer needs while ensuring compliance with environmental policies. The combination of regulatory pressure, urban restrictions, and technological innovation positions Europe as a frontrunner in sustainable compact loader deployment.

Asia Pacific Compact Loaders Market Trends

Asia Pacific is the fastest-growing compact loaders market, supported by large-scale infrastructure investments in China and India. China’s Belt and Road Initiative continues to stimulate demand for earthmoving and construction equipment, while India’s Smart Cities mission drives adoption in urban transit and roadway projects.

Competitive local manufacturing provides affordable entry-level loaders, enabling penetration into cost-sensitive emerging markets. Japan, in contrast, emphasizes automation and operator safety, incorporating advanced control systems, telematics, and collision-avoidance technologies into compact loader designs.

Electrification remains in its early stages, with penetration below 5%. However, pilot deployments in urban redevelopment projects across China, South Korea, and Japan highlight increasing interest in battery-electric loaders. Regional supply chain localization and component manufacturing resilience further strengthen Asia Pacific’s position in the global market. This foundation supports long-term growth across construction, agriculture, and industrial applications, making the region a key focus for both global OEMs and domestic equipment producers.

Competitive Landscape

The compact loaders market shows moderate consolidation, with global leaders focusing on platform synergies, wide attachment ecosystems, and extensive dealer networks to strengthen market position. Regional specialists intensify competition by targeting niche applications and tailoring equipment to local needs. High rental penetration has also shaped competition, with manufacturers prioritizing designs that simplify maintenance, ensure uptime, and integrate seamlessly with telematics platforms.

Differentiation increasingly centers on electrification, advanced aftertreatment systems, and operator-assist technologies. New business models, including pay-per-hour service contracts, bundled telematics subscriptions, and attachment-as-a-service offerings, highlight the industry’s shift toward recurring revenue streams and long-term customer lifecycle value.

Key Market Developments

- In September 2025, Gehl unveiled five new large-frame skid steers and compact track loaders ranging from 72-114 HP. These models feature vertical-lift arms, load-sensing hydraulics, and upgraded cabs, designed to boost breakout force, visibility, and operator comfort in heavy-duty construction and agricultural applications.

- In August 2025, JCB introduced its most powerful compact track loaders to date, the 4TS teleskid and 400T CTL, each delivering 109 HP and ~4,000 lb rated operating capacity. Built for forestry and demanding construction work, they provide higher hydraulic flow, extended lift reach, and stronger breakout performance.

- In July 2025, Yanmar Compact Equipment: Yanmar launched four new compact track loader models in the U.S., marking its entry into the CTL category. With operating capacities ranging between 2,100 and 3,700 lbs, these machines expand Yanmar’s compact equipment lineup and strengthen its dealer network presence in North America.

- In April 2025, CASE Construction Equipment debuted new compact loaders, including an electric wheel loader and upgraded skid-steer and track loader models. Designed for rental markets, the lineup emphasizes easy maintenance, enhanced operator ergonomics, and advanced telematics integration to ensure uptime and reduced operating costs.

Companies Covered in Compact Loaders Market

- Bharat Earth Movers Limited

- Hyva Global B.V.

- Schmitz Cargobull AG

- Thompsons (UK) Limited

- JCB Ltd.

- IVECO S.p.A.

- Meiller Group

- Ashok Leyland Limited

- Komatsu Ltd.

- Volvo Construction Equipment

- Hitachi Construction Machinery Co., Ltd.

- Caterpillar Inc.

- Mercedes-Benz Trucks

- Daimler AG

- Tata Motors Limited

Frequently Asked Questions

The market is valued at US$ 15.7 Bn in 2025, rising to US$ 22.7 Bn by 2032 at a CAGR of 5.4% .

.

High urban infrastructure investment, rental fleet modernization, and digital telematics services underpin strong equipment utilization and recurring revenue growth.

Track loaders lead with 54% share due to superior terrain adaptability, flotation, and higher rental utilization compared to wheel loaders.

North America leads due to its substantial construction spending, mature rental networks, advanced dealer ecosystems, and supportive emissions regulations.

Rental-centric electrification paired with telematics bundles unlocks new lifecycle revenue streams and accelerates adoption in regulated urban environments.

Top players include Caterpillar Inc., JCB Ltd., Volvo Construction Equipment, Komatsu Ltd., Hitachi Construction Machinery, Deere & Company, and Bobcat Company.