- IT and Telecommunication

- Cloud Camera Market

Cloud Camera Market Size, Share, and Growth Forecast, 2026 - 2033

Cloud Camera Market by Component Type (Hardware, Software, Services), Deployment Mode (Cloud / On-Premises), End Use Industry (Retail & E‑commerce, BFSI (Banking, Financial Services, Insurance), IT & Telecom / Enterprise Offices, Healthcare, Transportation & Logistics, Government & Public Safety, Education & Smart Campuses, Hospitality & Entertainment, Oil & Gas / Industrial, Miscellaneous) and Regional Analysis for 2026 - 2033

Cloud Camera Market Size and Trends Analysis

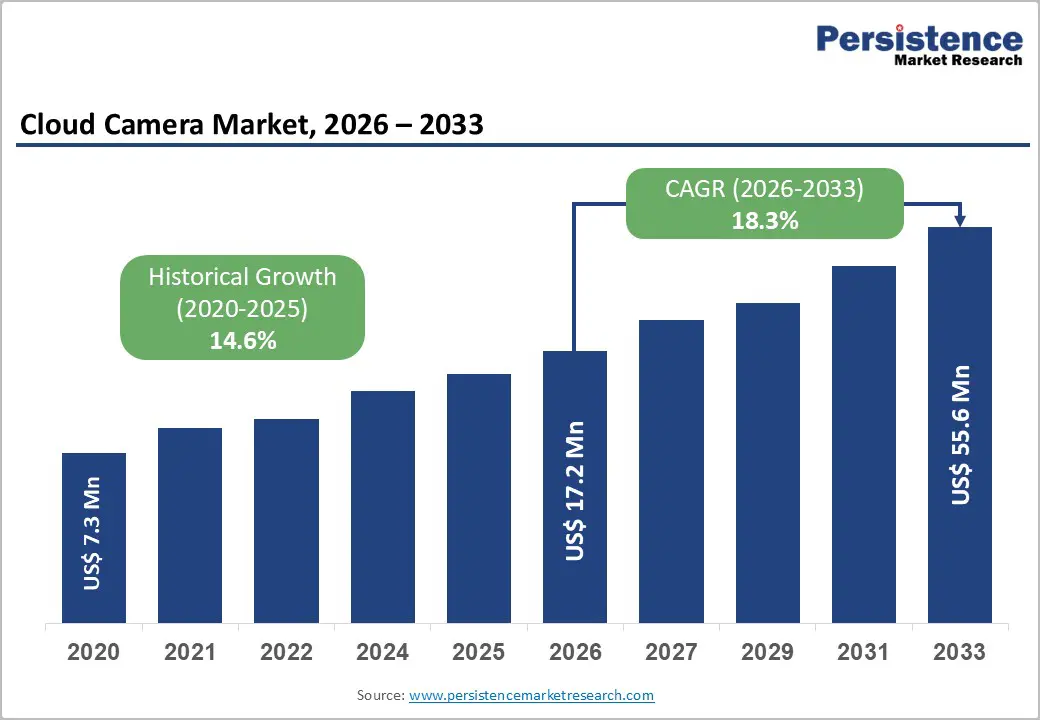

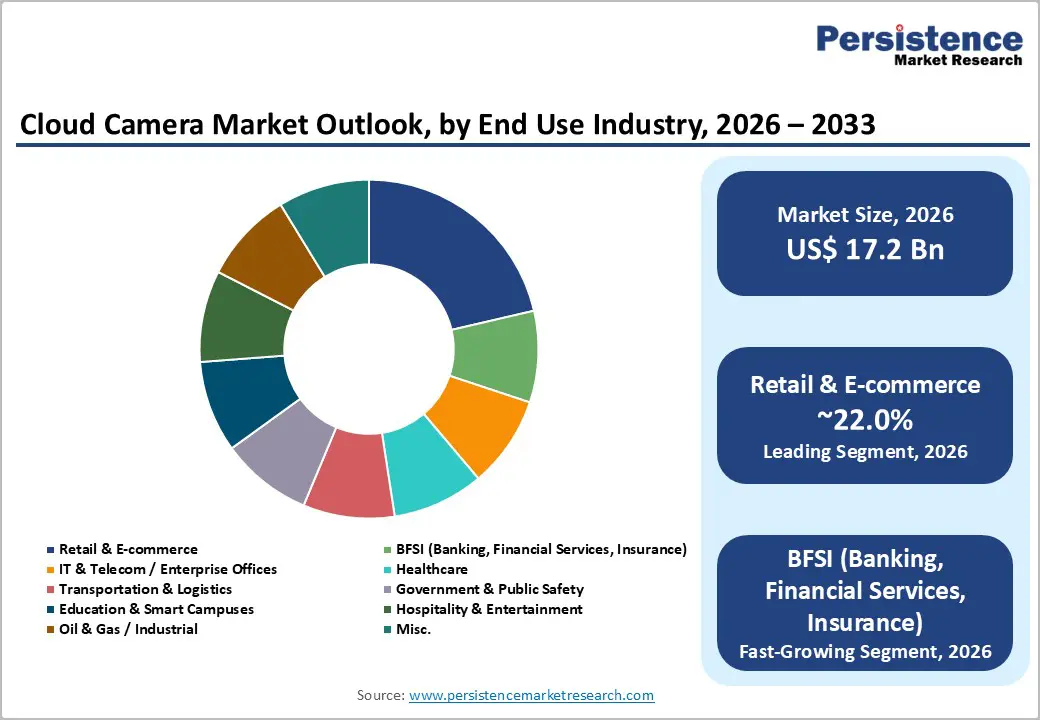

The Global Cloud Camera Market was valued at US$17.2 Billion in 2026 and is projected to reach US$ 55.6 Billion by 2033, growing at a CAGR of 18.3% between 2026 and 2033. This accelerating growth reflects the market's transition from specialized security applications toward mainstream infrastructure supporting smart buildings, intelligent retail operations, and comprehensive urban safety ecosystems.

The convergence of AI-powered analytics capabilities, hybrid cloud-edge deployment architectures, and rapid smart city infrastructure investments catalyzes sustained market expansion across government, commercial, and residential segments globally.

Key Industry Highlights:

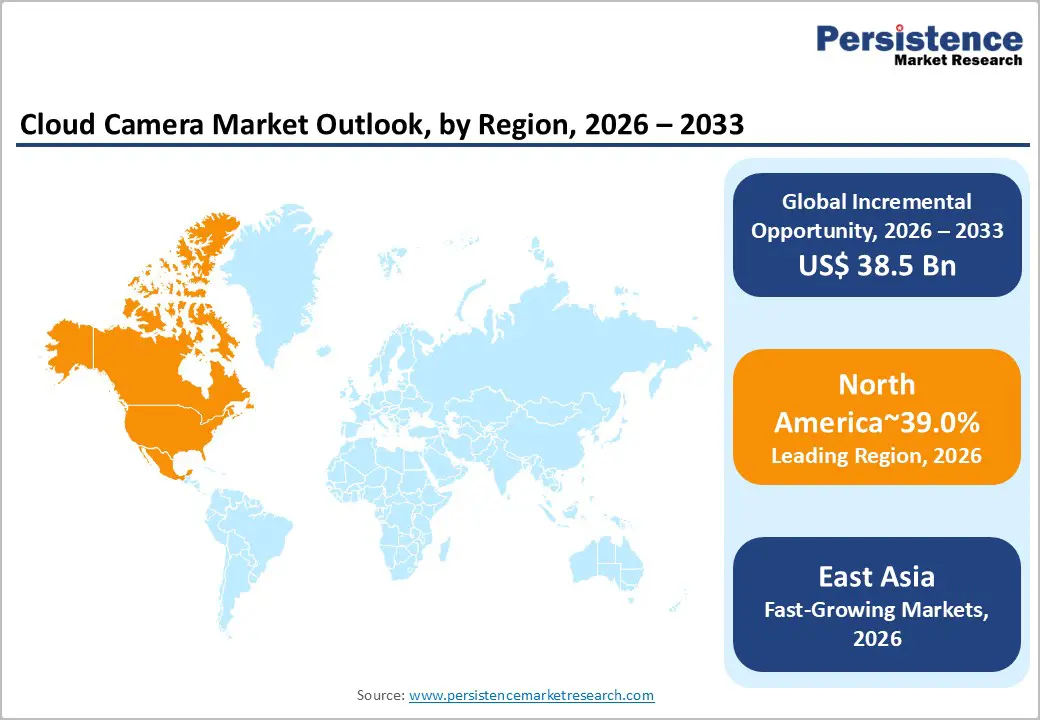

- Regional Leadership: North America leads the Cloud Camera market with ~39% share in 2026, driven by high enterprise cloud adoption, federal smart city investments, and strong demand from BFSI and public safety agencies.

- Fastest-Growing Region: East Asia holds ~28% share and represents the fastest-growing region, supported by large-scale government surveillance programs in China and rapid e-commerce and logistics expansion across the region.

- Leading Component Segment: Hardware dominates the market with ~58% share in 2026, reflecting continued reliance on high-performance sensors, optics, and edge-enabled IP cameras as the foundation of cloud video systems

- Fastest-Growing Component Segment: Services emerge as the fastest-growing segment, driven by Managed Video Surveillance-as-a-Service (MSaaS) adoption and enterprise preference for OPEX-based cloud deployment models

- Top End-User Segment: Retail & e-commerce accounts for ~22% share, leading the market due to extensive use of AI-powered video analytics for loss prevention, customer behavior analysis, and operational optimization.

| Key Insights | Details |

|---|---|

|

Cloud Camera Market Size (2026E) |

US$ 17.2 Bn |

|

Market Value Forecast (2033F) |

US$ 55.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

18.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.6% |

Market Dynamics

Growth Drivers

Smart City Infrastructure Expansion and Government Digital Transformation Initiatives

Government agencies globally are deploying comprehensive cloud-based surveillance networks as foundational infrastructure for smart city development and public safety modernization, thereby driving substantial Cloud Camera Market demand. India's 100 Smart Cities Mission with INR 48,000 crore approximately USD 5.76 billion budget allocation has catalyzed deployment of 76,000 cameras integrated with centralized command-and-control centers that aggregate surveillance across traffic management, emergency response, and law enforcement functions.

China's sophisticated surveillance infrastructure including the 'Skynet' video surveillance program represents one of the world's largest surveillance networks, establishing technological and operational benchmarks that motivate international governments to implement comparable systems. The United States federal government allocated USD 42.5 billion through the Broadband Equity Access and Deployment Program for high-speed internet infrastructure, with resultant connectivity enabling deployment of advanced cloud camera systems across municipalities.

Smart city surveillance systems generate data streams supporting multiple operational functions simultaneously traffic optimization through congestion detection, emergency response coordination through incident detection and alerting, public safety enhancement through facial recognition and behavior analysis, and administrative enforcement through license plate recognition. The Cloud Camera Market benefits from government procurement processes that standardize cloud-based surveillance architecture, creating sustained multi-year revenue streams for platform providers securing government contracts. Municipal budgeting for surveillance infrastructure, while subject to fiscal constraints, prioritizes public safety outcomes that cloud camera systems demonstrably deliver through real-time threat detection and operational coordination.

Explosive Adoption of AI-Powered Video Analytics and Intelligent Surveillance Capabilities

The Cloud Camera Market is fundamentally transformed by breakthrough advances in artificial intelligence and machine learning applied to video analysis, enabling organizations to extract actionable intelligence from continuous video streams previously limited to archival recording.

The global AI in video surveillance market demonstrates exceptional growth, validating the market-wide transition from passive recording toward active intelligence generation. AI-enabled cameras deployed in the Cloud Camera Market deliver capabilities including facial recognition, license plate reading, behavior analysis, anomaly detection, and predictive threat identification that transform surveillance from reactive after-the-fact investigation toward real-time operational decision support.

Retail organizations specifically benefit from AI analytics enabling people-counting, dwell-time analysis, heat-mapping customer flows, and automated theft detection capabilities that directly impact conversion rates and operational efficiency. Research indicates that retailers implementing AI-powered video analytics report 60% increases in store foot traffic and 94% higher conversion rates for products with AR/3D visualization enabled by intelligent video analytics. Healthcare institutions leverage AI-enabled cloud cameras for infection control monitoring, fall detection in elderly care facilities, and unauthorized access prevention in sensitive areas. Manufacturing and logistics organizations deploy AI video analytics for quality control automation, safety compliance monitoring, and inventory tracking across warehouse operations. The Cloud Camera Market's expansion is directly proportional to organizations' recognition that investment in intelligent video infrastructure delivers measurable business outcomes beyond traditional security applications, justifying substantial technology spending across multiple customer segments.

Market Restraining Factors

Privacy Concerns and Regulatory Compliance Complexity Elevating Deployment Barriers

Data privacy regulations such as GDPR in Europe, CCPA in California, Digital Personal Data Protection Act in India create substantial compliance obligations and operational friction that constrain Cloud Camera Market adoption, particularly in jurisdictions with stringent personal data protection requirements. Healthcare and financial services sectors face heightened privacy obligations protecting patient and customer information, creating organizational hesitation toward comprehensive video surveillance despite security benefits.

Regulatory requirements mandate explicit consent collection before capturing biometric data (facial recognition), transparent disclosure of surveillance practices, and robust data protection mechanisms including encryption and access controls. Public sentiment toward surveillance systems, particularly government-operated networks, creates political resistance to cloud camera deployment despite public safety justifications. These regulatory and social constraints create implementation costs and timeline delays that moderate Cloud Camera Market growth compared to less-regulated jurisdictions.

Organizations must navigate complex jurisdictional variations in privacy standards, creating fragmented global market with region-specific compliance requirements preventing single standardized platform deployment across international operations.

Key Market Opportunities

Transportation and Logistics Modernization Through Real-Time Fleet and Asset Visibility

The Cloud Camera Market encounters substantial opportunities in transportation and logistics operations where vehicle-mounted and facility-based cloud cameras provide real-time visibility into fleet operations, asset security, and operational compliance addressing a critical information gap limiting logistics industry efficiency optimization. Transportation & Logistics represents the fastest-growing segment within the Cloud Camera Market, driven by e-commerce demand for package tracking accountability, driver safety monitoring requirements, and operational efficiency optimization through behavior-based coaching.

Cloud camera systems deployed in delivery vehicles enable automatic documentation of delivery completion (photographic proof), customer interactions complaint resolution evidence, and road safety compliance supporting liability management and insurance cost reduction.

Logistics facilities leverage cloud cameras for real-time inventory visibility, automated stock rotation (FIFO enforcement), shrinkage prevention, and dock safety monitoring preventing forklift incidents and loading errors. Cross-docking operations benefit from cloud-enabled analytics tracking pallet movements and identifying congestion points requiring process optimization.

The Transportation & Logistics segment's fastest-growth trajectory reflects profound industry pressure to improve last-mile delivery economics where cloud camera visibility directly reduces operational costs through route optimization, delivery verification automation, and safety incident reduction. Integration with IoT sensors enables cloud platforms to correlate video-documented handling events with product condition data, enabling accountability for damage responsibility and supporting claims management. Cold-chain logistics particularly benefits from this visibility pharmaceutical and perishable goods sectors require documented temperature compliance alongside video documentation of proper handling procedures, which cloud cameras enable through integrated monitoring.

Smart Building Integration and IoT-Enabled Infrastructure Optimization

The Cloud Camera Market addresses transformative opportunities in smart building ecosystems where cloud cameras serve as foundational sensory infrastructure enabling intelligent building management across occupant safety, energy efficiency, and operational automation dimensions. IoT-enabled smart buildings are integrating cloud cameras as primary security and operational intelligence systems, with opportunities emerging across multiple use cases: automated occupancy detection triggering HVAC adjustments, emergency evacuation coordination through crowd monitoring, unauthorized access prevention through integrated access control systems, and facility utilization analytics optimizing real estate portfolio decisions. Enterprise offices increasingly deploy cloud cameras not merely for security but for operational intelligence detecting conference room occupancy patterns to optimize room booking systems, monitoring workspace utilization to guide return-to-office policies, and tracking compliance with workplace safety protocols

Educational institutions leverage cloud cameras for campus safety, building access security, and operational management. Healthcare facilities deploy cloud cameras for infection control monitoring (hand hygiene compliance), patient safety, and emergency coordination.

The Market's expansion within smart buildings reflects institutional recognition that comprehensive video surveillance represents foundational sensory infrastructure enabling broader automation and optimization of building operations. Standards-based integration enables cloud camera systems to participate in open smart building ecosystems rather than proprietary vendor lock-in situations, reducing customer adoption friction.

Category-wise Analysis

Component Type Insights

Hardware comprises 58% of the Global Cloud Camera Market in 2026, reflecting the continued centrality of sophisticated camera devices as foundational infrastructure despite the market's transition toward software and services revenue models. Cloud camera hardware encompasses diverse form factors and capabilities: compact dome cameras for retail and residential applications, ultra-wide panoramic cameras for large-area coverage, thermal imaging cameras for low-light and night operations, and specialized cameras (e.g., license plate recognition optimized) addressing specific application requirements.

Hardware's leading position reflects fundamental physicssensor quality, optical capabilities, and processing power embedded within physical cameras directly determine downstream analytics capabilities, with superior hardware enabling more sophisticated AI feature extraction and edge processing functions. The segment's dominance particularly reflects ongoing transition from legacy analog CCTV hardware toward sophisticated IP-based cloud cameras incorporating on-device processing, local storage capability, and native cloud connectivity.

Services represent the fastest-growing component segment within the Cloud Camera Market, driven by organizational preference for operational expense models over capital expenditure and the increasing complexity of cloud camera platform management requiring specialized expertise. Cloud hosting, managed analytics, integration services, and professional support services increasingly represent larger revenue components than hardware sales, reflecting broader industry transition toward software-centric business models. Managed Video Surveillance as a Service (MSaaS) platforms eliminate customer responsibility for infrastructure operation, security patch management, backup administration, and analytics model updates, with providers assuming these operational burdens.

End User Insights

Retail and e-commerce sectors hold 22% of the Global Cloud Camera Market in 2026, establishing clear vertical leadership driven by the sector's sophisticated use of video analytics for operational optimization beyond traditional security applications. Retail organizations deploy cloud cameras for loss prevention (shrinkage reduction through theft detection), customer analytics (people counting, dwell time analysis, heat mapping), staff compliance monitoring (point-of-sale procedures, customer service quality), and merchandise optimization (out-of-stock detection, planogram compliance verification).

Cloud camera analytics in retail enable measurement of critical KPIs: conversion rates correlated with floor layout and merchandising changes, traffic pattern analysis identifying peak periods requiring staffing optimization, and theft detection supporting loss prevention ROI calculation justifying surveillance investments.

E-commerce companies leverage in-warehouse cloud cameras for order fulfillment accuracy, inventory management automation, and worker safety compliance monitoring. The retail segment's leading position reflects unique combination of factors: acceptance of surveillance in commercial customer environments, direct correlation between video-derived analytics and measurable business outcomes enabling ROI justification, and technology sophistication driving innovative analytics applications beyond security toward operational intelligence.

Regional Insights and Trends

North America Market Trend

North America commands 39% of the Global Cloud Camera Market, establishing the region as dominant through convergence of advanced technology adoption, substantial enterprise IT budgets, regulatory emphasis on security and data protection, and concentration of major technology vendors supporting cloud infrastructure deployment. The United States market demonstrates particularly strong growth dynamics driven by federal government cybersecurity mandates (NIST frameworks requiring advanced monitoring infrastructure), Department of Defense procurement standards (CMMC compliance), and federal law enforcement modernization initiatives.

The region's enterprise segment particularly demonstrates strong cloud camera adoption Fortune 500 companies operate complex multi-site operations requiring centralized surveillance management, driving substantial cloud platform spending. Financial services institutions in North America face stringent compliance requirements (SOX, PCI-DSS) mandating comprehensive audit trails and surveillance infrastructure documentation, creating institutional demand for managed cloud camera platforms.

East Asia Market Trend

East Asia holds 28% of the Global Cloud Camera Market, with growth driven by aggressive smart city infrastructure investments (particularly China's surveillance programs), rapidly expanding e-commerce retail operations, and emerging digital governance initiatives across the region. China's surveillance infrastructure development including facial recognition technology deployment and smart city programs positions the nation as center of cloud camera innovation, with technology development and deployment scales exceeding other global regions.

The region's rapid e-commerce growth (particularly in China, India, Southeast Asia) drives retail surveillance investment addressing fraud prevention and operational analytics requirements. Asia Pacific's e-commerce market growth directly correlates with cloud camera demand across warehousing, logistics, and retail operations supporting transaction verification and fraud prevention.

Europe Market Trend

Europe accounts for 25% of the Global Cloud Camera Market, with growth constrained by stringent privacy regulations (GDPR) requiring explicit consent and proportionality assessment for surveillance systems, but supported by substantial regulatory compliance demand and government digital transformation initiatives. European financial services institutions (dominant in banking and insurance sectors) deploy cloud cameras for regulatory compliance, with PSD2 (Revised Payment Services Directive) requiring robust authentication and fraud prevention infrastructure. The region's data protection emphasis creates premium demand for privacy-respecting cloud camera architectures incorporating on-device processing, encryption, and granular access controls addressing regulatory requirements. European banking sector with €43.6 trillion in total assets demonstrates substantial capital availability supporting cloud infrastructure investments. Smart city initiatives across major European cities drive government surveillance spending, though constrained by public resistance to comprehensive surveillance and strict regulatory oversight.

Competitive Landscape

The Global Cloud Camera Market is moderately consolidated, dominated by a handful of key players while still allowing space for innovative smaller companies. Leading companies such as Axis Communications, Hanwha Vision, March Networks, Eagle Eye Networks, TP?Link (VIGI), and ONVU Technologies hold significant market share through their robust cloud-connected surveillance solutions, AI-powered analytics, and scalable storage platforms.

Axis Communications and Hanwha Vision focus on enterprise and SMB customers with hybrid cloud offerings, while Eagle Eye Networks and March Networks emphasize advanced cloud video management and AI integration. TP?Link’s VIGI and ONVU Technologies provide cost-effective, easy-to-deploy solutions with direct camera-to-cloud connectivity, appealing to price-sensitive and niche segments. The market sees strategic partnerships, product innovations, and AI-driven services as key differentiators, while barriers like cloud infrastructure and cybersecurity expertise limit excessive fragmentation.

Key Industry Developments

- 31 March 2025 – Velosting launched myCloudCam, India’s first fully cloud-based surveillance solution, marking a key development in the Cloud Camera market by eliminating on-premises storage through multi-CDN cloud infrastructure. The platform offers AI-powered analytics, real-time HD monitoring, and scalable cloud storage with plans starting at INR 499, targeting both individual and enterprise surveillance needs. Built for integration with ISPs, SIs, and CSPs, myCloudCam strengthens cloud-native adoption in India’s security and surveillance ecosystem.

- 20 November 2025 – Xthings launched the Ulticam IQ V2, a next-generation cloud-connected security camera integrating edge AI with Gemini cloud intelligence, reinforcing advances in the Cloud Camera market. The Matter 1.5–ready 4K PoE camera combines on-device object detection with cloud-based scene analysis, natural-language search, and free rolling cloud storage. This development highlights the market shift toward open-standard, AI-driven cloud cameras with reduced subscription dependency and broad smart-ecosystem.

Companies Covered in Cloud Camera Market

- Verkada Inc.

- Eagle Eye Networks / Brivo

- Arlo Technologies, Inc.

- Wyze Labs, Inc.

- Axis Communications AB

- Hikvision Digital Technology Co., Ltd.

- March Networks Corporation

- Camcloud

- Cloudvue (Johnson Controls)

- Amazon (Ring / Blink)

- Google Nest (Alphabet)

- D‑Link Corporation

- Logitech (Circle cameras)

- CP Plus (Aditya Infotech)

- TP‑Link (VIGI)

- Honeywell Building Products

- Sparsh CCTV

- VVDN Technologies

- Avtron Technologies

- Velvu