- Industrial Goods & Service

- Bulk Material Handling System Market

Bulk Material Handling System Market Size, Share, and Growth Forecast, 2026 - 2033

Bulk Material Handling System Market by Equipment Type (Conveyors, Stackers & Reclaimers, Loaders & Unloaders, Mobile Handling Equipment, Others), End-Use Industry (Mining & Minerals, Construction & Infrastructure, Manufacturing & Processing, Agriculture & Food, Recycling & Waste, Others), Technology (Manual Systems, Semi-Automated Systems, Fully Automated Systems, Smart/IoT-Enabled Systems, Electric & Hybrid Systems), and Regional Analysis for 2026 - 2033

Bulk Material Handling System Market Share and Trends Analysis

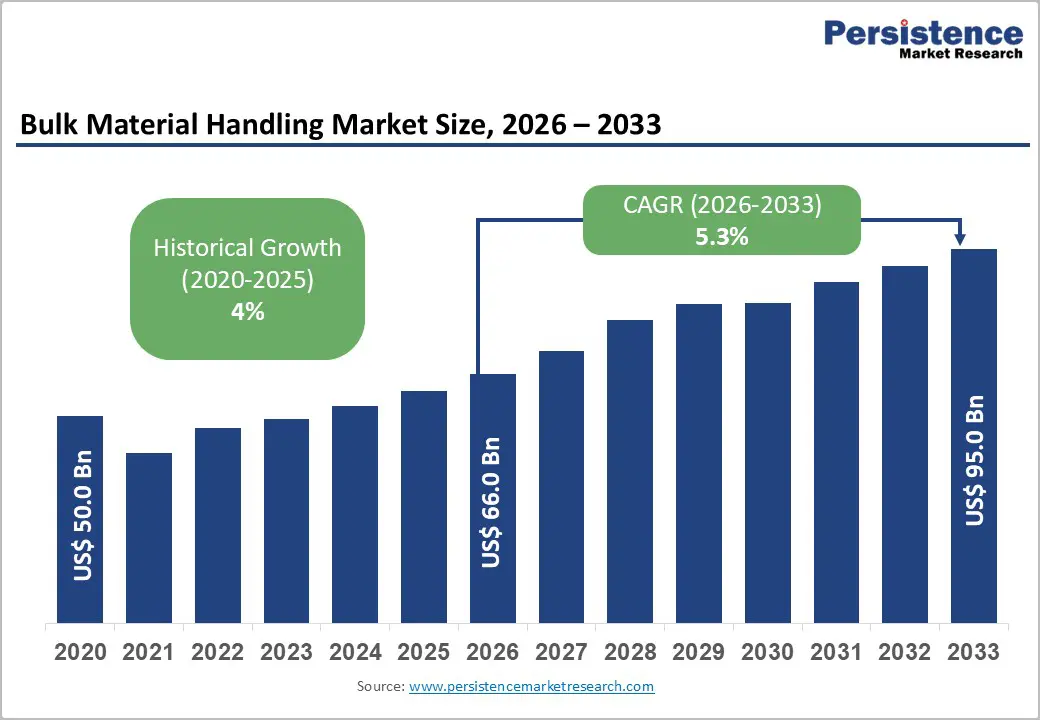

The global bulk material handling system market size is likely to be valued at US$ 66.0 billion in 2026, and is projected to reach US$ 95.0 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026 - 2033.

The market is expanding at a measured pace as mining capacity additions, infrastructure construction programs, and automation adoption across manufacturing and logistics operations are generating sustained equipment demand. Companies are increasingly deploying electrified machinery, automated conveying solutions, and integrated monitoring platforms supported by Industrial Internet of Things (IIoT) to improve throughput efficiency, reducing downtime, and lowering total cost of ownership. Industrial growth across emerging economies is also creating demand for high-capacity material handling infrastructure, particularly in Asia Pacific, where infrastructure spending remains elevated according to the World Bank Global Infrastructure Outlook. Transition toward low-carbon technologies is also heightening the need for bulk transport of minerals such as lithium, copper, and rare earth elements, as highlighted by the International Energy Agency (IEA) Critical Minerals Report.

Regulatory frameworks related to dust emissions, worker safety, and carbon reduction are becoming stricter across developed regions, which is accelerating adoption of enclosed conveying systems, filtration technologies, and automated equipment compliant with Occupational Safety and Health Administration (OSHA) and European Union (EU) standards. These compliance requirements are increasing engineering complexity but are simultaneously creating replacement demand for advanced solutions. The industry is therefore transitioning from standalone mechanical equipment procurement toward integrated, technology-enabled material handling ecosystems that combine hardware, automation software, and lifecycle services.

Key Industry Highlights

- Dominant Equipment Type: Conveyors are expected to command about 38% of total market revenue in 2026, reflecting their central role in continuous material transport across mining, cement, ports, and manufacturing operations.

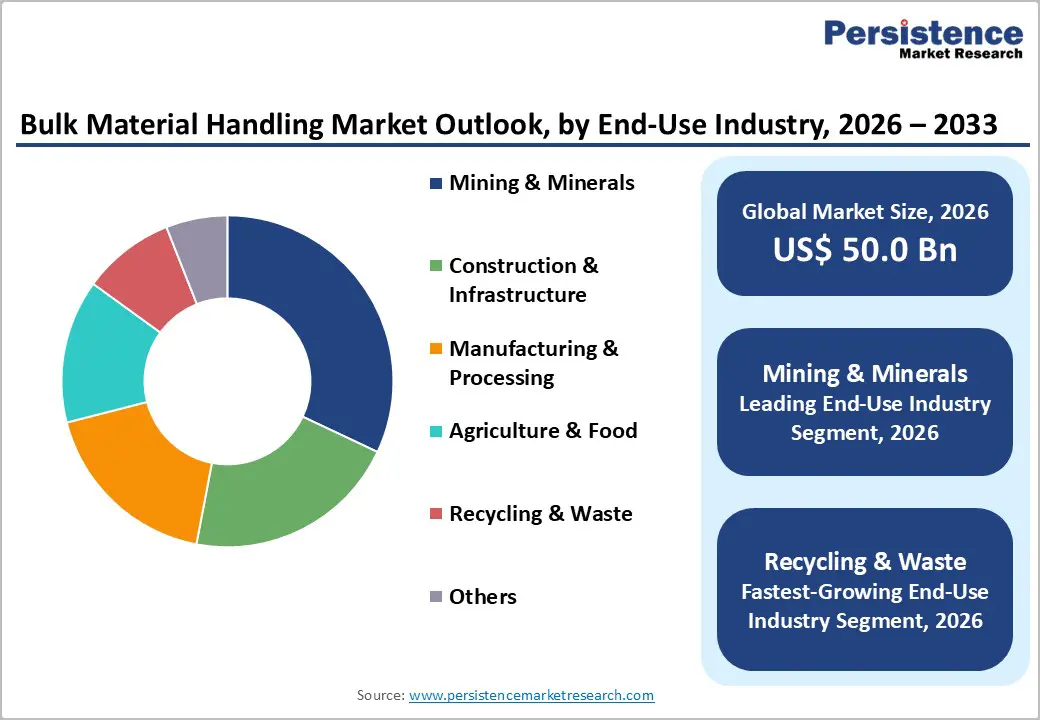

- Leading End-Use Industry: Mining & minerals are anticipated to account for approximately 32% of global revenue in 2026, driven by increasing production of critical minerals such as copper, lithium, and iron ore.

- Fastest-Growing End-Use Industry: Recycling & waste management are forecast to record the strongest growth through 2033 with an estimated 6.8% CAGR, driven by circular economy policies and increasing investments in material recovery facilities globally.

- Regional Leadership: Asia Pacific is expected to lead with approximately 41% revenue share in 2026 and showcase the highest 2026 - 2033 CAGR of about 6.1%, owing to large-scale infrastructure spending and mining expansion.

- Competitive Dynamics: Market competition is increasingly being shaped by automation capabilities, lifecycle service offerings, and digital integration, with leading companies prioritizing predictive maintenance platforms and energy-efficient equipment designs.

- November 2025: Sierra International introduced a patented operator cab that lowers to ground level to improve safety and accessibility in bulk material handling operations.

| Key Insights | Details |

|---|---|

| Bulk Material Handling System Market Size (2026E) | US$ 66.0 Bn |

| Market Value Forecast (2033F) | US$ 95.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electrification of Mining and Heavy Industry Supply Chains

Industries are transitioning toward electrified material handling systems to meet decarbonization objectives and higher operational efficiency across production environments. Demand for minerals required for clean energy technologies is increasing substantially, with the IEA projecting that consumption could rise more than threefold by 2030. This expansion is driving new mining projects and associated handling infrastructure investments, which are increasing procurement of advanced conveying and loading equipment. Electrified conveyors, automated loaders, and energy-efficient drive systems are reducing fuel consumption, minimizing maintenance requirements, and improving reliability across continuous operations. Although initial capital expenditure remains higher, lifecycle cost savings and regulatory compliance benefits are strengthening the business case for electrified systems across mining, ports, and heavy industry applications.

Mining operators are also deploying long-distance conveyor networks to replace conventional truck haulage in order to improve cost efficiency and environmental performance. Engineering studies from mining industry associations indicate that conveyor-based transport can reduce operating expenses by approximately 30-50% over asset lifecycles while lowering greenhouse gas (GHG) emissions and workforce safety risks. This shift is stoking the demand for high-capacity belt conveyors, advanced drive technologies, and integrated automation platforms capable of managing large material volumes over extended distances. Equipment manufacturers are benefiting from both greenfield project investments and modernization cycles as companies are upgrading legacy fleets to comply with environmental standards and productivity targets.

Expansion of Port and Bulk Logistics Infrastructure

Global seaborne bulk trade is continuing to expand, particularly across commodities such as iron ore, coal, grains, and fertilizers that require large-scale handling infrastructure at ports and terminals. The UN Conference on Trade and Development (UNCTAD) indicates that bulk cargo represents more than 40% of global maritime trade volume, and infrastructure investments are increasing across Asia, the Middle East, and Africa as governments are strengthening export logistics capacity. National development strategies are prioritizing port efficiency improvements to enhance trade competitiveness and reduce supply chain bottlenecks, which is accelerating the procurement of automated ship loaders, stackers, reclaimers, and high-capacity storage systems.

Port operators are increasingly integrating digital inventory management platforms and automated material flow technologies to improve throughput performance and reduce vessel turnaround time. Advanced monitoring systems supported by IIoT are enabling real-time asset tracking, predictive maintenance, and operational optimization across terminals. This transition is shifting procurement preferences toward integrated bulk handling solutions rather than standalone mechanical equipment purchases, as operators are seeking end-to-end system efficiency and lifecycle cost control. Consequently, system integrators and engineering, procurement, and construction (EPC) contractors are gaining strategic importance within the market ecosystem by delivering turnkey infrastructure projects that combine equipment, automation software, and operational services.

High Capital Intensity and Commodity Cycle Exposure

Bulk material handling systems entail substantial capital investment and long project payback periods, which is making procurement decisions highly sensitive to commodity price fluctuations across mining and heavy industry sectors. Mining capital expenditure historically follows commodity cycles with pronounced volatility. The World Bank Commodity Markets Outlook indicates price variability hovers around 30% across major minerals within relatively short timeframes. Companies are therefore delaying or scaling capital projects when commodity prices weaken, which is directly influencing demand for large-scale handling equipment and infrastructure installations.

This cyclical environment is creating revenue instability for equipment manufacturers and is limiting adoption among smaller operators that face tighter financial constraints. Financing conditions are becoming more challenging as global interest rates remain elevated, increasing the cost of capital for infrastructure and industrial expansion projects. Vendors are responding by offering alternative procurement models such as leasing arrangements, equipment-as-a-service (EaaS), and performance-based contracts to reduce upfront investment risk for customers. However, the adoption of these financing models is remaining uneven across regions due to differences in credit access, regulatory frameworks, and project risk profiles.

Regulatory Compliance Costs and Environmental Constraints

Environmental and occupational safety regulations are becoming increasingly stringent, particularly across Europe and North America, as policymakers are strengthening industrial emission controls and workplace protection standards. Dust emission thresholds, noise exposure limits, and safety compliance requirements are raising engineering complexity and increasing the cost of designing and installing bulk material handling systems. The EU Industrial Emissions Directive (IED) and regulatory enforcement by the OSHA in the U.S. require enclosed conveying infrastructure, advanced filtration technologies, and higher levels of automation to minimize worker exposure and environmental impact. Companies are therefore incorporating dust suppression systems, sealed transfer points, and automated monitoring solutions to meet compliance standards, inflating capital expenditure.

Compliance-related costs are increasing total project expenditure by approximately roughly 15%, particularly in retrofit scenarios. Smaller industrial operators are facing financial constraints when upgrading facilities, which is slowing equipment replacement cycles in cost-sensitive sectors such as aggregates and regional processing plants. Regulatory pressure is also accelerating the demand for technologically advanced solutions that improve safety and environmental performance, including automated conveyors and real-time monitoring platforms supported by IIoT. This dynamic is creating a mixed market impact, as compliance challenges are delaying some investments while simultaneously generating new opportunities for vendors.

Autonomous and Smart Material Handling Systems

Automation and digitalization are producing enormous growth opportunities across mining, ports, and manufacturing industries. Smart sensors, predictive maintenance platforms, and AI-driven optimization tools are enabling real-time performance monitoring and data-driven decision-making across material handling operations. These technologies are improving asset utilization, reducing unplanned downtime, and extending equipment lifespan, with the International Federation of Robotics (IFR) reporting continued adoption growth across heavy industrial sectors, including mining and processing facilities. Organizations are increasingly integrating IIoT architectures with supervisory control and data acquisition (SCADA) systems to achieve centralized visibility and operational control across large infrastructure environments.

The smart bulk handling segment is expected to represent a multi-billion-dollar opportunity by 2033, supported by demand for remote operations, workforce risk reduction, and throughput optimization. Autonomous conveyor networks, robotic loading equipment, and automated storage systems are gaining adoption in hazardous environments such as mining operations and chemical processing plants where safety requirements are stringent. Companies that are investing in digital platforms are transitioning toward recurring revenue models through software subscriptions, predictive maintenance services, and performance optimization contracts, which extend value beyond traditional equipment sales.

Emerging Market Infrastructure and Resource Development

Emerging economies across Asia, Africa, and Latin America are increasing investments in infrastructure, mining, and energy development as governments are prioritizing industrial expansion and export competitiveness. As per the World Bank, global infrastructure investment requirements could exceed US$ 90 trillion by 2040. Large economies such as India, Indonesia, and Brazil are expanding mining output and manufacturing capacity to support domestic consumption and international trade, which is generating strong demand for conveyors, storage systems, and loading equipment. Rapid urbanization and population growth are also increasing demand for construction materials and energy resources, further strengthening procurement of high-capacity handling infrastructure across these regions.

These markets are typically requiring cost-efficient and modular solutions that can scale with project development phases, creating opportunities for manufacturers that are offering flexible system designs and localized production capabilities. Strategic partnerships such as joint ventures, technology transfer agreements, and regional manufacturing investments are becoming critical for market entry and long-term competitiveness. As industrialization continues accelerating, companies that are aligning product portfolios with regional requirements and regulatory frameworks will be well positioned to capture sustained growth opportunities across emerging economies.

Category-wise Analysis

Equipment Type Insights

Conveyors are expected to dominate with approximately 38% of the bulk material handling system market revenue share in 2026, as continuous material transport continues to be fundamental across mining, cement production, port operations, and manufacturing environments. Industrial operators are relying extensively on belt conveyors and screw conveyors to move large material volumes efficiently while minimizing labor requirements and operational disruptions. Large mining projects are increasingly deploying long-distance conveyor networks to replace conventional truck haulage in order to reduce fuel consumption, operating expenses, and carbon emissions. This transition is reinforcing the dominant market position of conveyor systems within overall equipment demand. Replacement demand is also contributing significantly as aging infrastructure in developed economies is reaching the end of its operational lifecycle.

Mobile handling equipment is projected to record the fastest growth between 2026 and 2033, fueled by prioritization of operational flexibility and scalable deployment models by industries. Mobile conveyors, loaders, and portable transfer systems are witnessing widening adoption across construction, mining, and logistics applications where project requirements are changing frequently. Contractors are preferring modular equipment configurations to reduce fixed infrastructure investment and improve project mobility, particularly in temporary or remote operating environments. Electrification trends are further accelerating adoption, especially in indoor facilities and urban industrial zones where emission regulations are becoming stricter. Financing innovations such as rental agreements, leasing programs, and EaaS models are lowering capital barriers for customers, which is supporting market expansion.

End-Use Industry Insights

Mining and minerals are expected to lead in 2026, holding around 32% of the bulk material handling system market share, powered by the massive equipment deployment for large-scale material transport and processing infrastructure. Mining operations are handling high material volumes continuously, which is creating sustained demand for conveyors, storage systems, reclaimers, and loading equipment across extraction and processing sites. The demand for metals such as copper, lithium, and iron ore is surging in response to electrification trends and infrastructure expansion, as reflected in production data published by the IEA and the U.S. Geological Survey (USGS). Large mining projects are investing heavily in integrated handling networks to improve operational efficiency and reduce logistics costs across long production cycles. Automation adoption is also accelerating within mining environments, with remote monitoring systems, predictive maintenance platforms, and autonomous material transport solutions becoming increasingly common in new installations.

Recycling and waste management are projected to grow the fastest at an estimated CAGR of 6.8% through 2033, as governments are strengthening circular economy policies and environmental regulations globally. Regulatory authorities are implementing stricter waste management standards and recycling targets, particularly across Europe and Asia, which is increasing investment in material recovery infrastructure and waste processing facilities. Bulk handling systems are playing a critical role in sorting, transporting, and processing large volumes of municipal and industrial waste materials within centralized facilities. Rapid urbanization and population growth are also increasing waste generation levels, which is further supporting demand for automated handling technologies. The segment is also benefiting from investments in advanced sorting equipment, robotics-enabled processing systems, and integrated facility designs that improve material recovery efficiency.

Regional Insights

North America Bulk Material Handling Market Trends

The market in North America is anticipated to grow steadily through 2033. This is attributable to mining modernization initiatives and infrastructure investments funded through federal programs such as the Infrastructure Investment and Jobs Act (IIJA) in the U.S. The market is also making considerable gains from rising domestic production of critical minerals that are supporting energy transition supply chains, including lithium, copper, and rare earth elements. Industrial operators are investing in advanced conveying systems, storage infrastructure, and automated loading technologies to improve efficiency and reduce operational risks across mining and processing environments. Continued investment in logistics infrastructure and manufacturing reshoring initiatives is further strengthening demand for bulk handling solutions across multiple industries.

Regional regulatory frameworks are becoming increasingly stringent, particularly regarding emissions control and workplace safety compliance, which is accelerating the adoption of enclosed conveying systems, dust suppression technologies, and automated monitoring platforms. Standards enforced by OSHA and environmental regulators are increasing compliance requirements for industrial facilities, prompting modernization of legacy infrastructure. The competitive landscape is characterized by technology-focused manufacturers, system integrators, and well-established aftermarket service providers that are offering lifecycle maintenance and digital optimization solutions. Investment opportunities are emerging in mining electrification projects, port modernization programs, and recycling infrastructure expansion as governments and private sector stakeholders are prioritizing supply chain resilience and sustainability objectives.

Europe Bulk Material Handling Market Trends

In Europe, the growth of the market is being driven by regulatory frameworks and sustainability priorities that are influencing investment decisions across industries. Environmental compliance requirements under the EU IED and broader decarbonization policies are encouraging adoption of energy-efficient, enclosed, and low-emission material handling systems across manufacturing, logistics, and processing facilities. Companies are increasingly upgrading legacy infrastructure to meet stricter emission thresholds and workplace safety standards, which is supporting replacement demand across developed industrial economies. Automation adoption is also remaining strong across European manufacturing and logistics sectors, with industrial operators integrating digital monitoring platforms and advanced control systems to improve productivity and operational transparency.

Europe is generating demand for bulk material handling systems through modernization initiatives across chemical processing industries, recycling infrastructure, and bulk logistics terminals. Circular economy policies are accelerating investments in waste processing and material recovery facilities, particularly across Northern and Western Europe, where governments are prioritizing sustainability targets and resource efficiency. Port modernization programs across countries such as Germany, the Netherlands, and Belgium are also driving procurement of automated loading and storage systems to improve logistics efficiency.

Asia Pacific Bulk Material Handling Market Trends

Asia Pacific is anticipated to dominate in 2026, capturing an estimated 41% of the bulk material handling system market share. The market here is projected to post the fastest growth at an approximate CAGR of 6.1% from 2026 to 2033. Rapid industrialization, large-scale infrastructure construction, and expanding mining activity across countries such as China, India, and Indonesia are generating massive demand for conveyors, storage systems, and loading equipment. Investment programs supported by the World Bank and regional development institutions are continuing to fund transportation corridors, energy facilities, and industrial production capacity, which is strengthening procurement of high-capacity material handling infrastructure. Manufacturing growth across sectors such as cement, metals, and chemicals is also contributing to sustained equipment demand as industrial operators are expanding production capabilities to meet domestic consumption and export requirements.

Port capacity expansion and logistics modernization are further reinforcing regional growth as governments are prioritizing trade competitiveness and supply chain efficiency. Regulatory frameworks across Asia Pacific are evolving, with increasing emphasis on environmental compliance and workplace safety standards, which is accelerating modernization of aging infrastructure and adoption of enclosed and automated handling systems. The region is also attracting significant investments from global equipment manufacturers that are establishing local production facilities, joint ventures, and service networks to improve cost competitiveness and customer proximity.

Competitive Landscape

The global bulk material handling system market structure is moderately fragmented, with a mix of large multinational corporations and numerous regional manufacturers competing across equipment categories and project segments. Leading companies are typically holding individual market shares between 4% and 9%, reflecting the project-based nature of procurement and the importance of regional specialization in industrial infrastructure development. Purchasing decisions are often influenced by local engineering requirements, regulatory compliance factors, and service network availability, preventing monopolization of the market. System integrators and EPC contractors are gaining strategic influence as customers are increasingly seeking turnkey solutions that combine equipment supply, automation integration, and project execution.

Competitive positioning is increasingly being shaped by technological capabilities, particularly in automation, digital integration, and lifecycle service delivery, rather than solely by mechanical equipment performance. Companies are investing in electrification technologies, predictive maintenance platforms supported by IIoT, and advanced software solutions to improve operational efficiency and reduce total cost of ownership for customers. These capabilities are enabling vendors to differentiate through value-added services such as remote monitoring, performance optimization, and long-term maintenance contracts that generate recurring revenue streams. Strategic partnerships with mining operators, logistics companies, and industrial manufacturers are also influencing competitive dynamics by facilitating co-development of customized solutions and securing long-term supply agreements.

Key Industry Developments

- In February 2026, Keith Manufacturing showcased its RX Technology drive systems at the 2026 Mid-America Trucking Show, highlighting advanced thermal protection, cleaner hydraulics, and intelligent controls designed to improve reliability and uptime in bulk hauling and waste handling applications.

- In February 2026, Metso acquired Australia-based MRA Automation to strengthen its bulk material handling portfolio by adding advanced automation, software, and digitalization capabilities for ports and terminal operations worldwide.

- In December 2025, BEUMER Group announced the setting up of a new manufacturing facility in Haryana, India, strengthening its local production capacity for advanced material handling systems across sectors such as airports, logistics, cement, and mining. The plant aims at enabling faster delivery timelines, greater localization, and improved support for large turnkey projects.

Companies Covered in Bulk Material Handling System Market

- FLSmidth & Co. A/S

- Metso Corporation

- BEUMER Group GmbH & Co. KG

- Siemens AG

- Sandvik AB

- Thyssenkrupp AG

- KION Group AG

- Daifuku Co., Ltd.

- Schenck Process Holding GmbH

- Bühler Holding AG

- TAKRAF GmbH

- Liebherr-International AG

- Hitachi Construction Machinery Co., Ltd.

- Komatsu Ltd.

- Honeywell International Inc.

Frequently Asked Questions

The global bulk material handling system market is projected to reach US$ 66.0 billion in 2026.

Mining capacity additions, infrastructure construction programs, and automation adoption across manufacturing and logistics operations are driving the market.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Deployment of electrified machinery, automated conveying solutions, and integrated monitoring platforms supported by IIoT by companies, skyrocketing infrastructure spending in Asia Pacific, accelerated extraction of lithium, copper, and rare earth elements for energy transition, and tightening regulatory frameworks related to dust emissions, worker safety, and carbon reduction are creating lucrative market opportunities.

FLSmidth & Co. A/S, Metso Corporation, BEUMER Group GmbH & Co. KG, and Siemens AG are some of the key players in the market.