- Technology

- Bulk Acoustic Wave (BAW) Filters Market

Bulk Acoustic Wave (BAW) Filters Market Size, Share, and Growth Forecast 2026 – 2033

Bulk Acoustic Wave (BAW) Filters Market by Design (Solidly Mounted Resonator BAW Filters, Film Bulk Acoustic Resonators, Advanced Configurations – Stacked Crystal Filters, Coupled Resonators), by Bandwidth (Below 10MHz, 10MHz–50MHz, Above 50MHz), by Application, by End-User, and by Regional Analysis, 2026–2033

Bulk Acoustic Wave (BAW) Filters Market Size and Trend Analysis

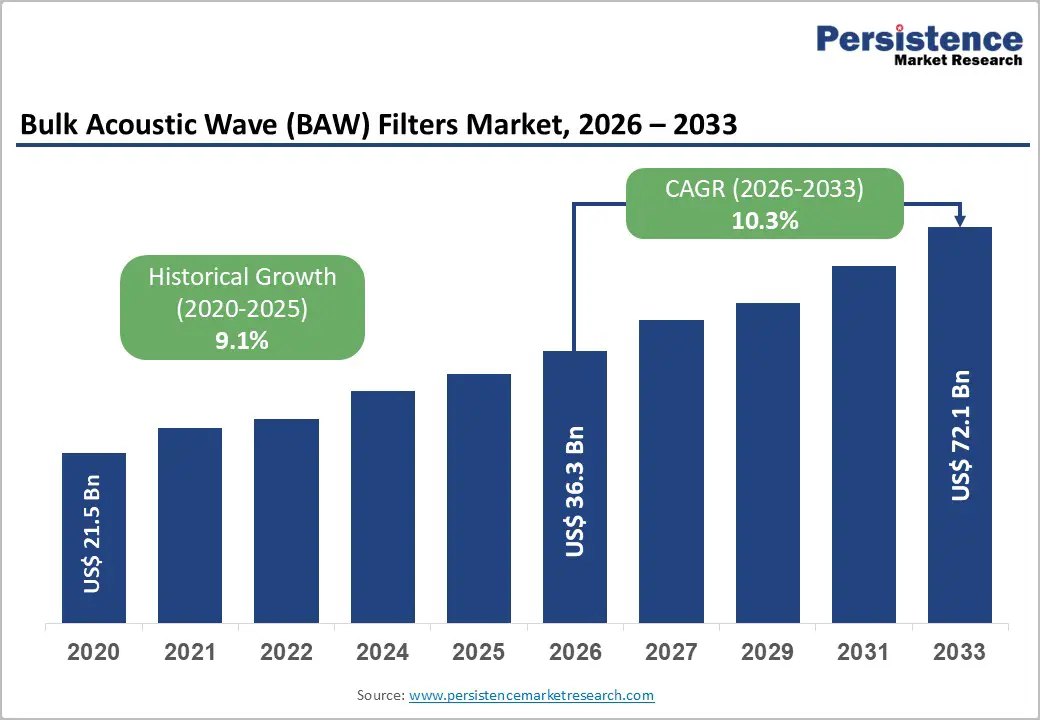

The global Bulk Acoustic Wave (BAW) Filters Market size is likely to be valued at US$ 36.3 Billion in 2026 and is expected to reach US$ 72.1 Billion by 2033, growing at a CAGR of 10.3% during the forecast period from 2026 to 2033. Strong growth is underpinned by the rapid rollout of 5G and Wi-Fi 6/6E networks, the rising RF complexity in smartphones, and increasing RF content per device in automotive, IoT, and infrastructure equipment.

Key Market Highlights

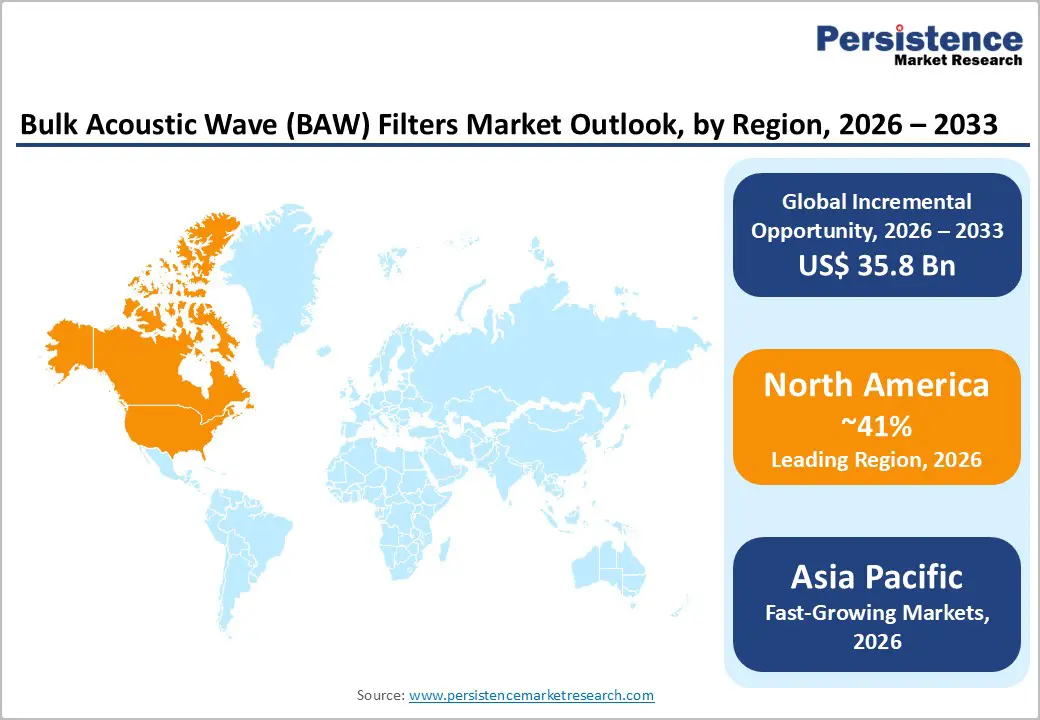

- Leading region: North America currently leads the Bulk Acoustic Wave (BAW) Filters Market with 41% share, supported by early 5G deployment, extensive Wi-Fi 6E adoption, strong RF semiconductor ecosystems, and sustained investments in advanced infrastructure and private network solutions.

- Fastest growing region: Asia Pacific is projected to be the fastest-growing region of around 11.8%, driven by massive 5G rollouts in China, Japan, and South Korea, rapid smartphone replacement cycles, expanding IoT deployments, and growing electronics manufacturing bases in India and key ASEAN economies.

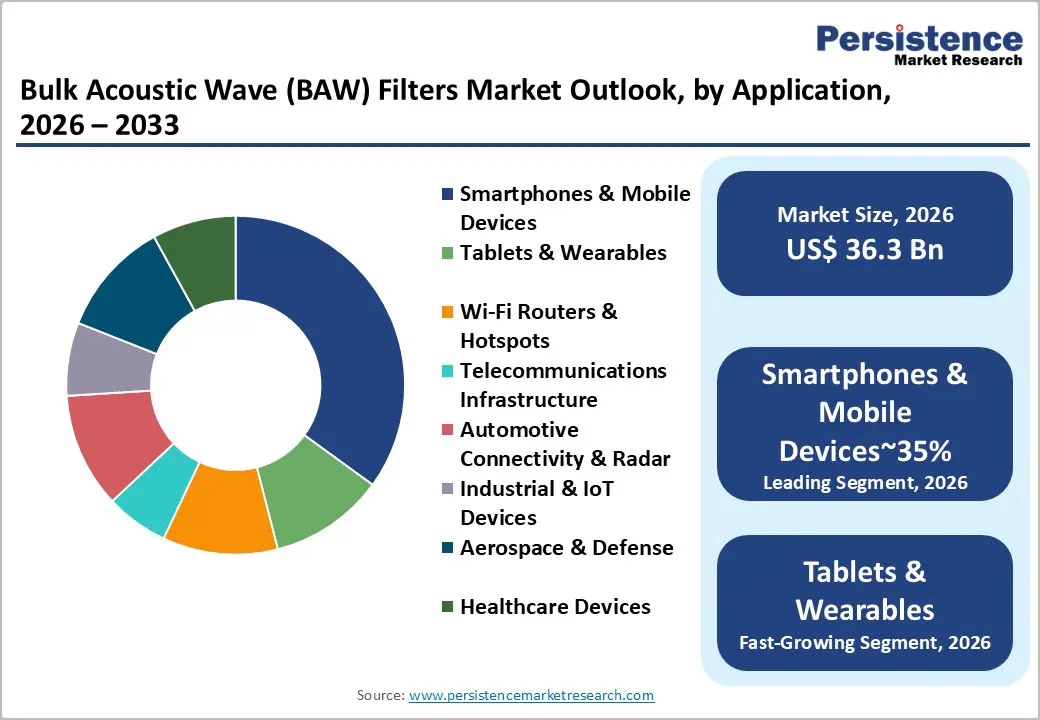

- Dominant segment: Among applications, Smartphones & Mobile Devices remain the dominant segment, accounting for the 45% share of BAW filter unit shipments as premium and mid-tier devices adopt multi-band 5G, Wi-Fi 6/6E, and advanced carrier aggregation requiring multiple high-frequency, high-selectivity filters.

- Fastest growing segment: Within end-users, Automotive is emerging as one of the fastest-growing segments, fueled by expanding ADAS, V2X connectivity, and connected infotainment platforms that depend on robust RF filtering for safety-critical communication and over-the-air software update capabilities.

- Key market opportunity: A key opportunity lies in high reliability BAW solutions for Wi-Fi 7, satellite broadband, and industrial/automotive use, where demanding environmental, bandwidth, and coexistence requirements favor advanced, high-Q filters and integrated RF front-end modules tailored to mission-critical connectivity.

| Key Insights | Details |

|---|---|

| Bulk Acoustic Wave (BAW) Filters Market Size (2026E) | US$ 36.3 Billion |

| Market Value Forecast (2033F) | US$ 72.1 Billion |

| Projected Growth CAGR (2026–2033) | 10.3% |

| Historical Market Growth (2020–2025) | 9.1% |

Market Dynamics

Market Growth Drivers

Surging 5G, Wi-Fi 6/6E, and high-band RF adoption

The foremost growth driver is the explosive increase in high-frequency wireless communication standards that require stringent filtering, particularly in the 3–7 GHz range. BAW filters are now the technology of choice for many mid-band 5G and Wi-Fi 6E front-ends because SAW filters struggle to maintain performance and selectivity at these higher frequencies. Global 5G subscriptions crossed 1.6 billion by the end of 2023, and 5G base station deployment has reached well over 6 million units worldwide, with a large share operating in the 3.3–4.9 GHz bands that rely heavily on high-performance RF filters.

The number of Wi-Fi 6/6E routers shipped has also run into the hundreds of millions annually, and a growing fraction incorporate BAW technology to manage coexistence between cellular and unlicensed bands. This intense spectrum crowding makes BAW filters indispensable for mitigating interference and maintaining signal integrity in advanced RF front end architectures.

Rising RF content in smartphones, automotive and IoT ecosystems

A second key growth driver is the increasing RF complexity per device across multiple end-use sectors. Modern flagship smartphones can integrate dozens of RF paths and require a separate filter for many licensed and unlicensed bands, with several filters often based on BAW technology to support high-band 5G, carrier aggregation, and advanced MIMO schemes.

In parallel, automotive electronics are becoming more RF-centric, with radar operating around 77 GHz, V2X communication in the 5.9 GHz band, and robust connectivity for telematics and infotainment – all of which depend on robust filtering along the RF chain. Industrial and consumer IoT devices—from smart meters to logistics trackers—are also moving toward higher data rates and multi?band connectivity, increasing their reliance on compact, high-Q BAW devices that can be integrated into tight module footprints while delivering low insertion loss and excellent out-of-band rejection.

Market Restraints

High manufacturing complexity and capital-intensive fabrication

Despite strong demand, the BAW filters market faces limitations due to the highly specialized and capital-intensive nature of its manufacturing processes. BAW devices require advanced thin-film deposition, high-precision lithography, and complex wafer-level packaging, often on silicon or piezoelectric substrates such as aluminum nitride (AlN). Defect rates can be significant, particularly in early production runs for new designs, driving up per-unit cost.

Only a handful of global players control large-scale BAW fabrication capacity, leading to a concentrated supply base and high entry barriers. These constraints can result in longer lead times, supply bottlenecks during demand spikes, and higher costs for OEMs compared to lower-frequency SAW filters, which may slow adoption in highly price-sensitive applications or lower-tier devices.

Thermal, design, and integration challenges at ever-higher frequencies

As 5G and Wi-Fi standards push toward higher frequencies and wider bandwidths, design margins for RF components continue to tighten. BAW filters must maintain stringent performance across wider temperature ranges and under high power conditions, particularly in infrastructure or automotive environments. Achieving steep skirts, low insertion loss, and high power handling within a small footprint often demands sophisticated multi-resonator or stacked-crystal structures.

These advanced configurations increase design complexity and can raise sensitivity to process variations and packaging parasitics. Integration within densely populated RF front-end modules—where coexistence with power amplifiers, LNAs, switches, and antenna tuners is critical—further complicates layout and thermal management. Such challenges can delay time-to-market for new filters and require significant R&D investments, limiting the pace of innovation for smaller players.

Market Opportunities

Expansion into next-generation Wi-Fi, satellite, and high-reliability infrastructure

A major opportunity lies in the rapid emergence of Wi-Fi 6E and Wi-Fi 7, as well as the proliferation of high-capacity fixed wireless access and satellite-based broadband services. These systems leverage extended 6 GHz and higher bands with demanding coexistence requirements, where BAW filters can deliver the sharp selectivity and low insertion loss necessary to protect adjacent services and maximize spectral efficiency.

As low-Earth-orbit satellite constellations expand into the thousands of satellites and gateway links scale, there is growing scope for radiation-tolerant, temperature-stable BAW solutions in space communication payloads and ground infrastructure. For suppliers capable of offering robust, high-reliability BAW portfolios tailored to infrastructure-grade and satellite-grade specifications, long-term design wins and multi-year supply agreements represent a significant revenue growth vector.

Automotive connectivity, radar, and industrial IoT as high-growth verticals

Automotive and industrial markets represent another compelling opportunity set. The increasing deployment of advanced driver-assistance systems (ADAS), high-resolution radar, and V2X connectivity requires dense RF front-ends operating across multiple bands with strict safety and reliability criteria. BAW filters with enhanced power handling and temperature stability can address radar front-ends as well as V2X channels in crowded sub?6 GHz spectra, enabling robust performance even in harsh environments.

At the same time, industrial IoT adoption is rising rapidly in manufacturing, logistics, utilities, and smart city infrastructure. These deployments favor compact modules that integrate multi-band cellular, LPWAN, and Wi-Fi connectivity, where high-performance filters are crucial for reducing interference and ensuring regulatory compliance. Vendors that tailor BAW product lines to automotive-grade and industrial-grade qualifications, and that support long lifetime and extended temperature ranges, can tap into these high-growth, higher-margin applications over the coming decade.

Category-wise Insights

Design Analysis

Within design, Film Bulk Acoustic Resonators (FBAR) are expected to retain leadership, accounting for around 55% share of the BAW filters market over the medium term. FBAR structures, which utilize thin piezoelectric films (commonly AlN) with either air-cavity or solidly mounted architectures, offer high resonance frequencies with excellent Q-factors and are well suited for compact RF front-end modules in smartphones, tablets, and Wi-Fi routers.

Global smartphone and Wi-Fi CPE shipments each run into the hundreds of millions of units annually, and a significant proportion of premium and mid-range devices now incorporate multiple FBAR-based filters to address high-band 4G/5G and unlicensed 5–7 GHz spectrum. Their compatibility with standard semiconductor processes and proven reliability in high-volume production underpin their dominance over newer or more complex stacked-crystal and coupled-resonator variants, which are still emerging from a commercialization standpoint.

Bandwidth Analysis

By bandwidth, the 10MHz–50MHz segment is projected to command the largest share, at approximately 48% of total BAW filter demand. This bandwidth range aligns closely with the channel widths used in many 5G NR, LTE-Advanced, and Wi-Fi 6/6E allocations, where each filter must provide sharp roll-off around channels of a few tens of megahertz while maintaining low insertion loss.

As regulators worldwide liberalize spectrum and operators aggregate carriers to deliver higher data rates, networks increasingly utilize wider channels and complex carrier aggregation schemes, driving demand for precise, medium?bandwidth BAW filters. Filters below 10 MHz typically address legacy or narrowband systems, while above 50 MHz targets ultra-wideband or specialty applications; both are important niches, but the bulk of current commercial traffic sits in the 10–50 MHz channelization window, reinforcing this segment’s leading share in the market.

Application Analysis

In terms of application, Smartphones & Mobile Devices represent the leading segment, with an estimated share of roughly 45% of BAW filter consumption. Each new generation of smartphones integrates more RF bands across 2G/3G/4G/5G, Wi-Fi, Bluetooth, and other protocols, substantially increasing the number of filters required per device. Premium 5G smartphones may incorporate dozens of RF filters, several of which are BAW-based to manage high-frequency, high-bandwidth channels above 2.5–3 GHz, including mid-band 5G and Wi-Fi 6E bands in the 5.9–7.2 GHz range.

Strong global smartphone replacement cycles, coupled with the migration of mid-tier devices to 5G, continue to reinforce this segment’s dominance. While infrastructure, automotive, industrial IoT, and aerospace & defense applications are rapidly growing, they are typically lower in unit volume but higher in average selling price, leaving high-volume mobile devices as the primary driver of overall unit shipments.

End-User Analysis

Among end-users, Consumer Electronics is expected to be the largest segment, accounting for close to 50% of overall market share. This category spans smartphones, tablets, wearables, gaming consoles, set-top boxes, and home networking devices such as Wi-Fi routers and mesh systems. Global shipments of smartphones alone exceed 1 billion units annually, while wearables and smart home devices have expanded rapidly on the back of health tracking, entertainment, and home automation trends.

Each of these consumer endpoints requires multiple RF paths, and as devices increasingly support both cellular and high-bandwidth Wi-Fi standards, the reliance on BAW filters grows. Telecommunications infrastructure, automotive, industrial, and aerospace & defense sectors account for the remaining share but are characterized by higher value per unit and stringent performance requirements, positioning them as strategic growth and margin enhancement segments for filter suppliers.

Regional Insights

North America Bulk Acoustic Wave (BAW) Filters Market Trends

North America is a leading market for BAW filters, anchored by early and extensive deployment of 5G networks in the U.S. and strong adoption of Wi-Fi 6/6E in residential and enterprise environments. The region hosts several major RF component and semiconductor companies that design and manufacture BAW filters, supporting a robust local ecosystem for mobile devices, infrastructure, and high-end networking equipment. The U.S. has been aggressive in allocating mid-band 5G spectrum, including C-band and other bands around 3.5–4 GHz, requiring advanced filtering to protect adjacent services and manage interference in dense urban deployments.

Regulatory and innovation frameworks in North America further reinforce BAW filter demand. The Federal Communications Commission (FCC) opened 1200 MHz of spectrum in the 6 GHz band for unlicensed use, catalyzing development of Wi-Fi 6E and Wi-Fi 7 products that rely heavily on high-frequency, high-selectivity filters. At the same time, growth in private 5G networks, industrial IoT solutions, and connected vehicles in the U.S. and Canada is increasing the number of RF front-ends that require robust BAW-based solutions. Strong R&D investments, a high concentration of design centers, and a mature device ecosystem position North America as a technology leader and a significant revenue contributor in the global BAW filters landscape.

Europe Bulk Acoustic Wave (BAW) Filters Market Trends

In Europe, the BAW filters market benefits from a steady rollout of 5G across leading economies such as Germany, the U.K., France, and Spain, combined with the region’s strong industrial base and automotive sector. European operators are leveraging bands around 3.4–3.8 GHz and other mid-band allocations, which demand high-performance RF filters to meet coverage and capacity requirements, particularly in dense urban and industrial zones. The region’s sophisticated regulatory environment, including coordinated spectrum policies under the European Union framework, encourages harmonized use of frequency bands, which in turn supports scale for filter designs optimized for pan-European deployment.

Europe’s prominent role in automotive engineering and industrial automation adds another growth layer for BAW filters. Leading carmakers and Tier-1 suppliers in Germany and other countries are integrating advanced connectivity, telematics, and V2X functions that rely on precise RF filtering. Industrial IoT, smart manufacturing, and energy infrastructure projects across the region also exploit private LTE/5G networks and advanced Wi-Fi, expanding demand for high-reliability RF front-end modules. Moreover, increasing emphasis on energy efficiency, electromagnetic compatibility, and compliance with stringent ETSI standards drives adoption of high-quality filters in both consumer and professional equipment, supporting a stable and increasingly sophisticated European BAW filter market.

Asia Pacific Bulk Acoustic Wave (BAW) Filters Market Trends

The Asia Pacific region is projected to be the fastest-growing market for BAW filters, driven by the sheer scale of manufacturing and consumption in China, Japan, South Korea, India, and ASEAN economies. China and South Korea are at the forefront of 5G rollout, with millions of base stations deployed and intense competition among device OEMs to deliver affordable 5G smartphones, many of which integrate multiple BAW-based RF filters. Japan’s advanced electronics sector and early exploration of next-generation connectivity standards further contribute to demand for cutting-edge filter solutions in both consumer and industrial applications.

Asia Pacific’s status as the global hub for electronics manufacturing also provides a structural advantage. Major contract manufacturers and component suppliers across China, Taiwan, and Southeast Asia assemble smartphones, routers, IoT devices, and automotive electronics for global brands, creating high local demand for RF front-end modules. India and ASEAN countries are rapidly expanding mobile broadband and fixed wireless infrastructure, as well as increasing local assembly of smartphones and connected devices, which will gradually lift regional consumption of BAW filters. Combined with significant investments in semiconductor fabrication, packaging, and advanced materials, Asia Pacific is emerging not only as the fastest-growing consumption region but also as a critical production base within the global BAW filters supply chain.

Competitive Landscape

The BAW filters market is relatively consolidated, with a small group of global leaders controlling a substantial share of design IP, manufacturing capacity, and high-volume supply to top smartphone and infrastructure OEMs. Companies focus on integrated RF front-end solutions that bundle BAW filters with power amplifiers, switches, and tuners to offer compact, system-level performance advantages. Key strategic priorities include continual R&D investment in new piezoelectric materials, advanced resonator topologies, and improved wafer-level packaging to enhance performance at higher frequencies and wider bandwidths.

Leading players are also expanding capacity through new fabs or line upgrades, optimizing cost structures, and forming long-term partnerships with handset vendors, infrastructure suppliers, and automotive Tier-1s. Emerging business models emphasize close co-design with customers, platform-based architectures to speed customization, and increasing integration of BAW filters into multi-function RF modules to secure design wins and lock in multi-year revenue streams.

Key Market Developments

- February, 2024: Qorvo, Inc. expanded RF filter manufacturing capacity in Asia to support growing 5G device and infrastructure demand, adding new high-volume BAW production lines.

- June, 2024: Broadcom Inc. introduced an advanced BAW filter platform targeting Wi-Fi 7 and high-band 5G applications, featuring ultra-wide bandwidth support and improved isolation for complex carrier aggregation.

- September, 2023: Murata Manufacturing Co., Ltd. announced new BAW-based RF modules for premium smartphones, integrating filters and matching circuits to reduce footprint while enhancing high-frequency performance.

Companies Covered in Bulk Acoustic Wave (BAW) Filters Market

- Qorvo, Inc.

- Broadcom Inc.

- Skyworks Solutions Inc.

- TDK Corporation

- Akoustis Technologies

- Taiyo Yuden Co., Ltd.

- Murata Manufacturing Company, Ltd.

- Microchip Technology Incorporated

- Kyocera Corporation

- API Technologies (APITECH)

- ECS, Inc. International

- Raltron Electronics Corporation

- Abracon LLC

- Golledge Electronics

- EPCOS

Frequently Asked Questions

The global Bulk Acoustic Wave (BAW) Filters Market is expected to reach approximately US$ 72.1 Billion by 2033, up from about US$ 36.3 Billion in 2026, reflecting a forecast CAGR of around 10.3% during 2026–2033.

Key demand drivers include rapid deployment of 5G networks, growing adoption of Wi‑Fi 6/6E and emerging Wi‑Fi 7 standards, increasing RF complexity in smartphones and other consumer electronics, and rising connectivity needs in automotive, infrastructure, and industrial IoT applications.

By application, Smartphones & Mobile Devices form the leading segment, as modern handsets integrate numerous RF paths and rely heavily on BAW technology to support high‑band 4G/5G and unlicensed spectrum with stringent selectivity and low insertion loss.

North America holds a leading position in the market, supported by early and extensive 5G rollouts in the U.S., strong Wi‑Fi 6E adoption, and the presence of major RF semiconductor and system OEMs driving advanced filter integration.

A key opportunity lies in developing high‑reliability, high‑frequency BAW solutions tailored for Wi‑Fi 7, satellite broadband, automotive and industrial IoT, where demanding environmental and coexistence requirements favor advanced, integrated RF front‑end modules.

Prominent players include Qorvo, Inc., Broadcom Inc., Skyworks Solutions Inc., TDK Corporation, Akoustis Technologies, Taiyo Yuden Co., Ltd., Murata Manufacturing Company, Ltd., Microchip Technology Incorporated, Kyocera Corporation, API Technologies, ECS, Inc. International, Raltron Electronics Corporation, Abracon LLC, and Golledge Electronics.