- Medical Devices

- Europe Urethral Bulking Systems Market

Europe Urethral Bulking Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Europe Urethral Bulking Systems Market by Product (Injectable Materials, Delivery Systems, and Needles and Accessories), by Material (Biocompatible Materials, Synthetic Polymers, and Natural Substances Electrodes), by Indication (Stress Urinary Incontinence, Urinary Sphincter Deficiency, and Recurrent Urinary Incontinence) by End-user (Hospitals, Ambulatory Surgical Centers, and Specialty Clinics), and Regional Analysis from 2026 to 2033

Europe Urethral Bulking Systems Market Share and Trends Analysis

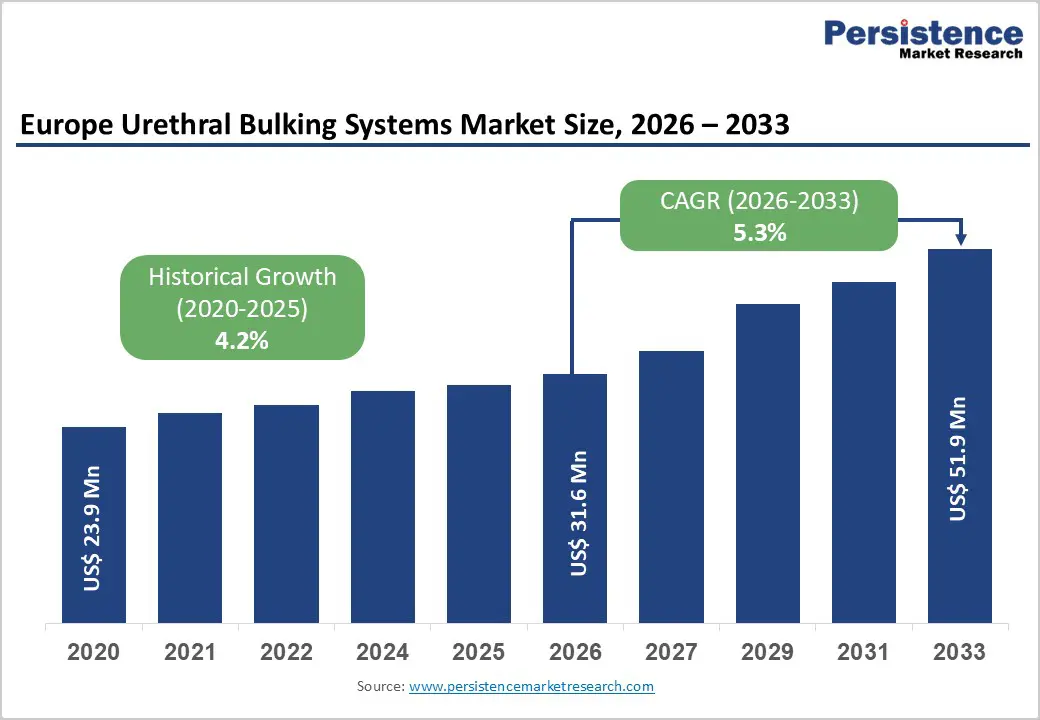

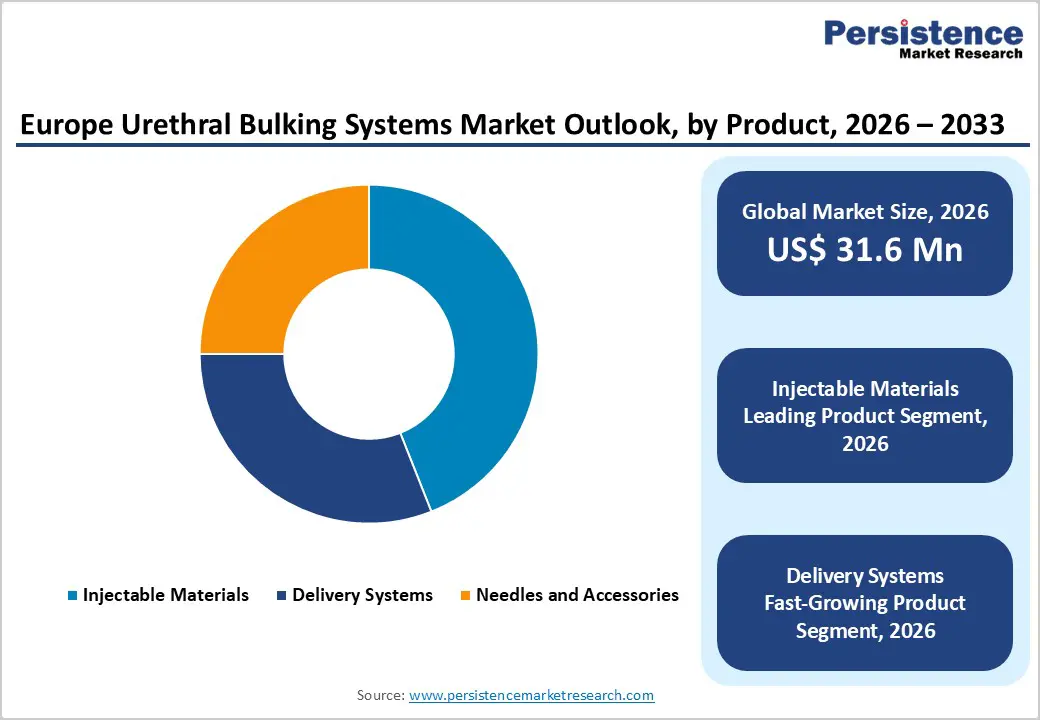

Europe urethral bulking systems market size is estimated to reach US$ 31.6 million in 2026 to US$ 51.9 million by 2033, and is expected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

The demand for urethral bulking systems in Europe is increasing steadily, driven by the rising prevalence of stress urinary incontinence, a rapidly aging population, and a growing preference for minimally invasive, outpatient-based urology treatments. Increasing diagnosis rates of urinary sphincter deficiency and recurrent urinary incontinence across hospitals, ambulatory surgical centers, and specialty clinics are supporting sustained market growth.

Higher procedure volumes linked to conservative incontinence management, repeat bulking interventions, and expanding office-based treatments, combined with rising healthcare expenditure and improved access to urology specialists, are further accelerating demand. Continuous innovation in bulking agent materials, including biocompatible hydrogels and advanced synthetic polymers, is improving safety profiles, durability, and patient outcomes. Additionally, increasing awareness of women’s health, favorable reimbursement trends in key European countries, and broader adoption of minimally invasive continence procedures are further propelling market expansion across Europe.

Key Industry Highlights

- Leading Product Segment: Injectable materials dominate the market owing to their widespread use as first-line, minimally invasive treatments for stress urinary incontinence and intrinsic sphincter deficiency.

- Fastest-Growing Product Segment: Delivery systems are growing rapidly as manufacturers focus on enhanced injection precision, procedural efficiency, and clinician-friendly device designs.

- Leading Indication Segment: Stress urinary incontinence remains the largest application, driven by high prevalence among aging female populations and increasing preference for conservative treatment approaches.

- Fastest-Growing Indication Segment: Recurrent urinary incontinence is expanding quickly as repeat urethral bulking procedures gain clinical acceptance for long-term symptom management.

- Leading End-user Segment: Hospitals remain the largest end users, supported by high patient volumes, the availability of specialized urology services, established procedural infrastructure, and greater adoption of urethral bulking procedures in inpatient and day-care surgical settings.

- Fastest-Growing End-user Segment: Ambulatory surgical centers and specialty urology clinics are expanding rapidly, driven by the shift toward minimally invasive, office-based continence treatments, shorter recovery times, cost efficiencies, and increasing patient preference for outpatient care models.

| Key Insights | Details |

|---|---|

| Europe Urethral Bulking Systems Market Size (2026E) | US$ 31.6 Mn |

| Market Value Forecast (2033F) | US$ 51.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver - Rising Prevalence of Stress Urinary Incontinence and Shift Toward Minimally Invasive Care

The growing prevalence of stress urinary incontinence (SUI), particularly among aging female populations, is a primary factor supporting demand for urethral bulking systems across Europe. Demographic trends show a steady rise in elderly populations, with age-related weakening of pelvic floor muscles significantly increasing incontinence incidence. In addition, lifestyle factors such as obesity, multiple childbirths, and post-menopausal changes are contributing to higher diagnosis rates. As awareness of incontinence as a treatable medical condition improves, more patients are seeking early intervention rather than delaying care.

Additionally, there is a clear shift among clinicians and patients toward minimally invasive treatment options that reduce surgical risk, recovery time, and healthcare costs. Urethral bulking procedures are increasingly positioned as first-line or intermediate therapies for patients who are unwilling or unsuitable for invasive surgical interventions such as slings. The ability to perform procedures in outpatient or office-based settings further enhances adoption. Growing clinical evidence supporting the safety and efficacy of modern biocompatible bulking agents, along with improved injection techniques, continues to strengthen physician confidence. Together, these factors are driving consistent procedural growth and supporting market expansion across major European healthcare systems.

Restraints - Variable Clinical Outcomes, Repeat Procedure Requirements, and Reimbursement Limitations

Several factors continue to impede the broader adoption of urethral bulking systems in Europe. One of the key challenges is the variability of long-term clinical outcomes relative to surgical alternatives. While urethral bulking offers clear advantages in terms of safety and recovery, treatment durability can be limited for some patients, often necessitating repeat injections over time. This requirement may reduce patient acceptance and influence clinician preference in cases where long-term symptom resolution is prioritized. Cost considerations also act as a moderating factor. Advanced bulking agents, particularly those that use proprietary biocompatible materials, can be expensive, and repeated procedures increase overall treatment costs.

Reimbursement policies for urethral bulking vary significantly across European countries, with inconsistent coverage limiting adoption in certain public healthcare systems. In some markets, reimbursement policies that favor surgical interventions over minimally invasive procedures further restrict procedural volumes. From a clinical perspective, concerns around improper injection technique, suboptimal placement, or material migration may impact outcomes and require additional training for practitioners. Patient selection also plays a critical role, as not all incontinence types respond equally to bulking therapy. These clinical, economic, and reimbursement-related challenges collectively limit faster market uptake.

Opportunity - Expansion into Outpatient Settings and Advancements in Long-Lasting Bulking Materials

Significant growth opportunities exist through the expansion of urethral bulking procedures into ambulatory surgical centers and specialty clinics across Europe. Healthcare systems are increasingly focused on reducing inpatient burden and shifting appropriate procedures to outpatient settings. Urethral bulking is well aligned with this transition due to its short procedural time, minimal anesthesia requirements, and low complication rates. As outpatient infrastructure expands and clinician training improves, procedural accessibility is expected to increase substantially. Material innovation represents another major opportunity.

Manufacturers are investing heavily in the development of next-generation bulking agents with improved durability, tissue integration, and reduced need for repeat interventions. Advances in synthetic polymers and hydrogel-based formulations are enhancing volume stability and long-term efficacy, thereby addressing a key limitation of earlier products. Stronger clinical data supporting these innovations is likely to accelerate adoption. In addition, growing focus on women’s health initiatives and aging care programs across Europe is improving awareness and diagnosis of urinary incontinence. As stigma declines and treatment pathways become more standardized, demand for conservative, patient-friendly therapies is expected to rise. These trends create favorable conditions for sustained long-term growth in the urethral bulking systems market.

Category-wise Analysis

By Product Insights

The injectable materials segment is projected to dominate the European urethral bulking systems market in 2026, accounting for a revenue share of 44.0%. This leadership is primarily driven by the widespread clinical use of injectable bulking agents as a first-line minimally invasive treatment for stress urinary incontinence (SUI), particularly among elderly women and patients unsuitable for surgery. Injectable materials offer advantages such as shorter procedure times, reduced hospitalization, repeatability, and favorable safety profiles, making them highly preferred across hospitals and outpatient settings. Growing awareness of conservative and non-surgical incontinence management, combined with rising diagnosis rates of SUI, continues to reinforce adoption. Additionally, ongoing innovation in long-lasting synthetic and biocompatible injectables has improved durability and clinical outcomes, supporting repeat procedures where required. The expanding availability of CE-marked bulking agents and clinician familiarity with injection techniques further strengthen the dominance of injectable materials across European healthcare systems.

By Indication Insights

The biocompatible materials segment is projected to dominate the European urethral bulking systems market in 2026, accounting for a revenue share of 38.5%. This dominance is attributed to the strong clinical preference for materials that demonstrate high tissue compatibility, minimal inflammatory response, and long-term stability following implantation. Biocompatible bulking agents are widely used across Europe due to their favorable safety profiles and lower risk of migration or degradation, which is critical in urethral applications. Increasing regulatory scrutiny and strict medical device safety standards in Europe further encourage the use of proven biocompatible formulations. In addition, growing demand for repeatable, low-complication treatments in aging populations has reinforced adoption. Continuous improvements in hydrogel-based and polymer-based biocompatible materials are enhancing injectability, durability, and patient comfort. Strong clinical evidence, physician confidence, and alignment with European regulatory expectations continue to support this segment’s leading position.

By End-user Insights

The hospital segment is projected to dominate the European urethral bulking systems market in 2026, accounting for 67.9% of revenue. This dominance is driven by the concentration of urology specialists, advanced diagnostic capabilities, and higher patient throughput within hospital settings. Hospitals are the primary centers for the diagnosis and treatment of stress urinary incontinence, particularly among older adults and complex patients requiring multidisciplinary care. Availability of trained urogynecologists, access to imaging and cystoscopic equipment, and established clinical pathways favor hospital-based urethral bulking procedures. In addition, hospitals often serve as referral centers for recurrent or refractory incontinence cases, further increasing procedure volumes. Long-term procurement agreements, standardized treatment protocols, and reimbursement coverage for hospital-performed procedures also support sustained demand. The rising burden of age-related incontinence and increasing emphasis on minimally invasive treatment options continue to reinforce hospital leadership across Europe.

Country-wise Insights

Germany Urethral Bulking Systems Market Trends

Germany is expected to dominate the Europe urethral bulking systems market with a value share of 20.4% in 2026. The country benefits from a highly developed healthcare infrastructure, strong reimbursement frameworks, and early adoption of minimally invasive urological procedures. High awareness of stress urinary incontinence and broad access to specialist urology services support consistent procedural volumes across hospitals and specialty clinics. Germany’s aging population significantly contributes to demand, as urinary incontinence prevalence rises sharply among older adults, particularly women.

The presence of leading medical device manufacturers and strong clinical research activity further enhances the market penetration of advanced bulking agents. Physicians in Germany demonstrate high confidence in biocompatible and long-lasting injectable materials, supporting repeat usage and procedural standardization. In addition, favorable regulatory clarity, robust clinician training programs, and sustained investment in outpatient urology services continue to reinforce Germany’s leadership position in the European urethral bulking systems market.

France Urethral Bulking Systems Market Trends

The French urethral bulking systems market is expected to grow steadily, supported by an aging population and increasing diagnosis of stress urinary incontinence. France benefits from a robust public healthcare system that ensures broad patient access to urology services and conservative treatment options. Growing awareness of minimally invasive alternatives to surgical interventions is driving increased utilization of urethral bulking procedures, particularly among elderly and high-risk patients. Hospitals remain the primary treatment centers, although outpatient and specialty clinics are gradually expanding their role.

France is also witnessing rising adoption of advanced biocompatible bulking agents that offer improved durability and reduced complication rates. Supportive reimbursement policies for incontinence management and strong adherence to clinical guidelines further facilitate market growth. Continuous investments in healthcare modernization, clinician education, and patient awareness campaigns are strengthening adoption, positioning France as a key contributor to regional market expansion.

U.K Urethral Bulking Systems Market Trends

The U.K. urethral bulking systems market is expected to exhibit a relatively high CAGR of approximately 6.8% between 2026 and 2033. Growth is driven by increasing awareness of stress urinary incontinence, rising elderly population, and growing preference for minimally invasive treatments within the National Health Service (NHS). Urethral bulking procedures are increasingly adopted as first-line or interim therapies due to their outpatient suitability and cost-effectiveness. Expansion of specialist continence clinics and improved referral pathways are further supporting procedure volumes.

The U.K. also benefits from strong clinical evidence supporting bulking agents, encouraging physician confidence and broader adoption. Increasing emphasis on reducing surgical burden and hospital stays aligns well with urethral bulking solutions. Continued investment in women’s health, aging care services, and non-surgical urology treatments is expected to sustain long-term market growth.

Competitive Landscape

Europe urethral bulking systems market is highly competitive, with strong participation from companies such as Coloplast Corp, Axonics, Inc., Carbon Medical Technologies, Inc., Promedon GmbH, and Laborie. These players leverage well-established regional distribution networks, strong clinician relationships, and continuous innovation in bulking materials, injection techniques, and delivery system design to address diverse clinical needs in stress urinary incontinence and related indications.

Growing preference for minimally invasive, outpatient-based incontinence treatments is driving product innovation and portfolio expansion across Europe. Manufacturers are increasingly focusing on long-lasting biocompatible materials, improved injectability, and enhanced procedural safety and precision. Strategic priorities include expanding adoption in ambulatory and specialty clinics, strengthening partnerships with hospitals and urology centers, and investing in clinical evidence and R&D to support next-generation urethral bulking solutions and sustain long-term market growth.

Key Industry Developments:

- In September 2023, UroMems, a global innovator in mechatronic solutions for stress urinary incontinence (SUI), announced the successful completion of patient enrollment in its first-in-human study of the UroActive™ System. The device is the world’s first smart, automated artificial urinary sphincter (AUS) designed for the treatment of SUI. Findings from this initial clinical evaluation are expected to inform the design and execution of UroMems’ pivotal SUI trials planned in Europe and the U.S.

Companies Covered in Europe Urethral Bulking Systems Market

- Coloplast Corp

- Axonics, Inc.

- Carbon Medical Technologies, Inc.

- Promedon GmbH

- Laborie

- Palette Life Sciences

- Contura International Ltd.

- CL Medical

- UROMED Kurt Drews KG

- Teleflex Incorporated

- Others

Frequently Asked Questions

Europe urethral bulking systems market is projected to be valued at US$ 31.6 Mn in 2026.

Increasing prevalence of stress urinary incontinence due to an ageing female population and rising awareness/acceptance of minimally invasive treatments.

The Europe urethral bulking systems market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion through strategic partnerships, educational campaigns, and wider adoption of outpatient and office-based bulking procedures.

Coloplast Corp, Axonics, Inc., Carbon Medical Technologies, Inc., Promedon GmbH, and Laborie, are some of the key players in the Europe urethral bulking systems market.