- Medical Devices

- Blood Fluid Warming System Market

Blood Fluid Warming System Market Size, Share, and Growth Forecast 2026 - 2033

Blood Fluid Warming System Market by Product (Surface warming systems, Blood & IV fluid warming systems, Portable warming systems, Others), Application (Surgery, Emergency & trauma care, Critical care / ICU, Others), by End User (Hospitals, Ambulatory surgical centers, Clinics & blood banks, Emergency medical services (EMS)), by Regional Analysis, 2026 - 2033

Blood Fluid Warming System Market Share and Trends Analysis

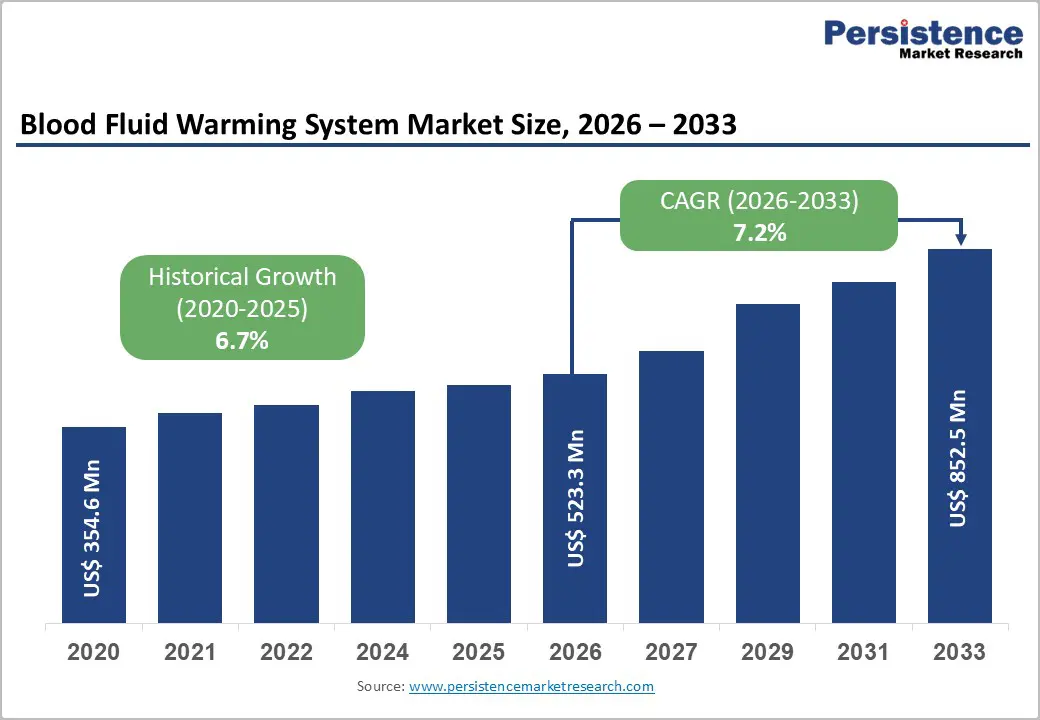

The global blood fluid warming system market size is expected to be valued at US$ 523.3 million in 2026 and projected to reach US$ 852.5 million by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

The market expansion is fundamentally driven by the increasing emphasis on preventing perioperative hypothermia and improving patient safety outcomes across surgical and trauma care settings. According to clinical evidence from the Association of Perioperative Registered Nurses (AORN), unintended perioperative hypothermia affects patients undergoing anesthesia. It triples the risk of surgical site infections, while maintaining normothermia at 36.5 C can reduce patient length of stay by 2.6 days. Additionally, research indicates that approximately 14% of trauma patients arrive at hospitals already hypothermic, and studies demonstrate that the addition of fluid warmers to ambulances alone has been associated with a 22% relative risk reduction in admission hypothermia, creating substantial demand for both stationary and portable warming solutions across emergency medical services and hospital environments.

Key Industry Highlights:

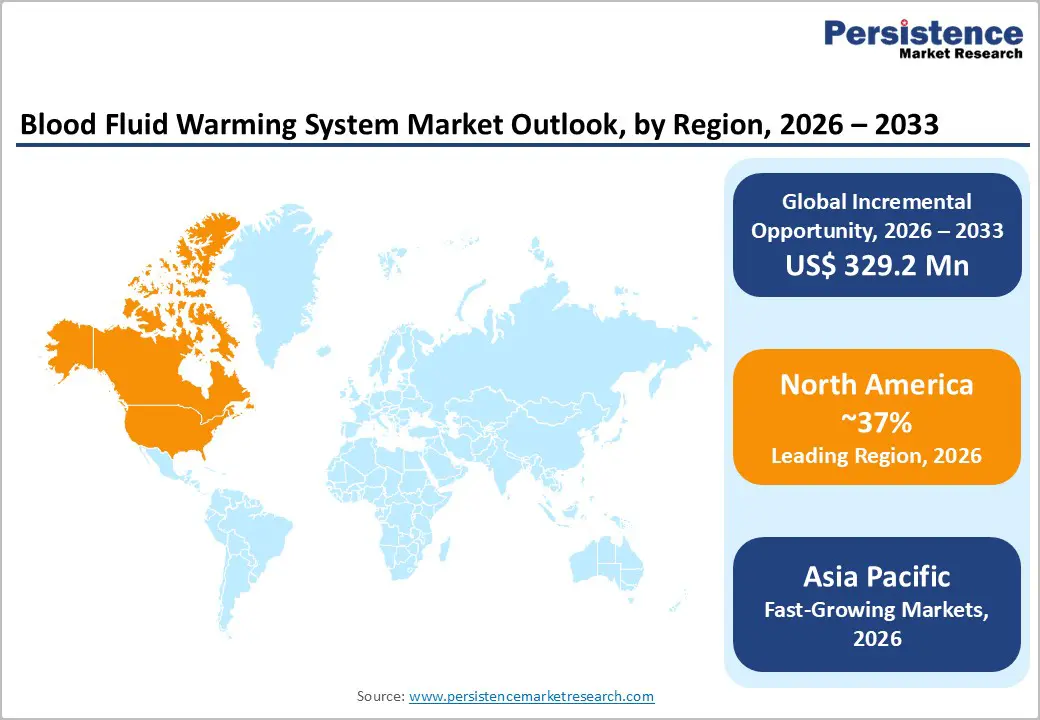

- North America maintains regional market leadership with a 37% share in 2025, driven by advanced healthcare infrastructure, stringent FDA regulatory oversight ensuring device safety, widespread adoption of AORN perioperative normothermia protocols, and strong commercial presence of major manufacturers including 3M Company, ICU Medical, Stryker Corporation, GE Healthcare, and Baxter International serving hospitals and emergency medical services across the United States and Canada.

- Asia Pacific emerges as the fastest-growing regional market with the highest projected growth rate, propelled by massive healthcare infrastructure expansion in China and India, rising surgical volumes, increasing trauma case burdens from traffic accidents, growing awareness of perioperative hypothermia prevention, competitive manufacturing advantages, and government procurement of portable warming equipment for emergency response and disaster relief operations across developing economies.

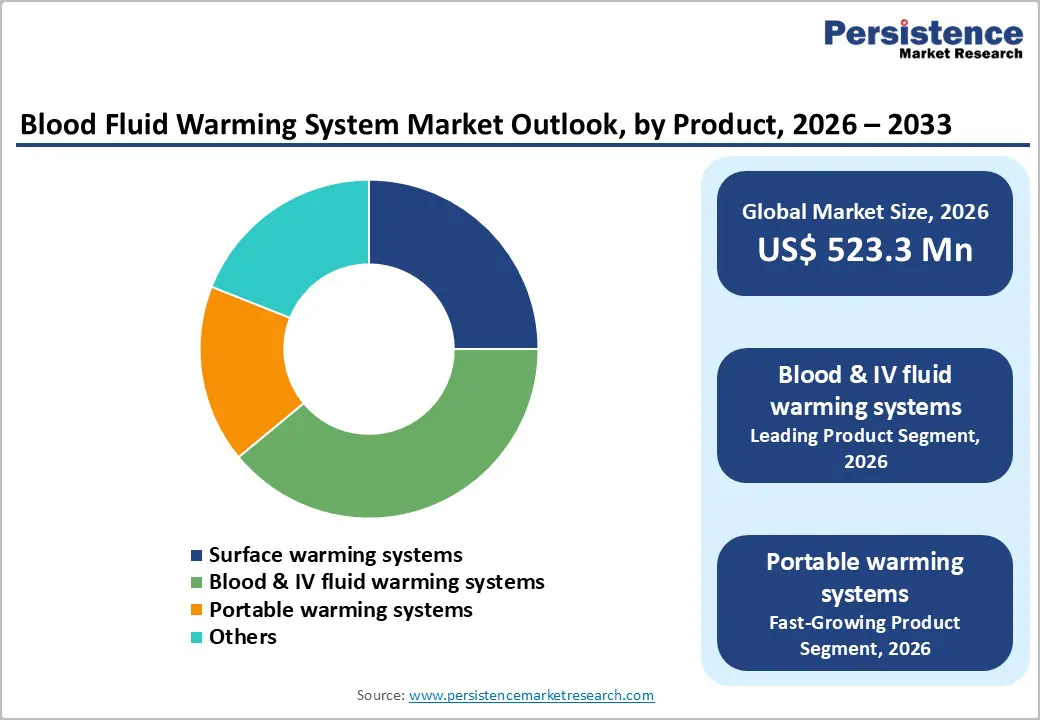

- Blood & IV fluid warming systems dominate the product category with 39% market share in 2025, reflecting their critical role as primary solutions for preventing perioperative hypothermia, extensive clinical validation through over 200 million patient uses of leading systems like 3M Bair Hugger, compliance with regulatory standards under 21 CFR 864.9205, and widespread deployment across operating rooms, intensive care units, and emergency departments for routine surgical procedures and trauma resuscitation requiring precise temperature control.

- Portable warming systems represent the fastest-growing product segment, driven by recent FDA clearances including the MEQU M Warmer System in June 2024 and TSC Life Fluido® AirGuard System in September 2025, expanding prehospital trauma care capabilities for emergency medical services, military medical operations, and ambulance transport where battery-operated devices address critical gaps in hypothermia prevention for hemorrhaging patients during field care and transport to definitive treatment facilities.

| Key Insights | Details |

|---|---|

| Blood Fluid Warming System Size (2026E) | US$ 523.3 million |

| Market Value Forecast (2033F) | US$ 852.5 million |

| Projected Growth CAGR (2026 - 2033) | 7.2% |

| Historical Market Growth (2020 - 2025) | 6.7% |

Market Dynamics

Drivers - Rising Incidence of Surgical Procedures and Trauma Cases Driving Adoption of Temperature Management Solutions

The escalating volume of surgical interventions globally, combined with the increasing prevalence of trauma cases requiring emergency care, serves as a primary catalyst for blood fluid warming system adoption. Perioperative hypothermia remains a significant clinical challenge, with epidemiological studies revealing that 62.5% of elderly patients undergoing abdominal surgery experience intraoperative hypothermia despite active warming measures, while 50.7% of elderly patients in pelvic floor reconstruction surgery develop hypothermia during procedures lasting 120 minutes or longer. The clinical consequences are severe, as hypothermia increases surgical site infection risk, prolongs recovery times, causes coagulopathy, and elevates cardiovascular morbidity rates. Furthermore, regulatory bodies and clinical organizations worldwide have established stringent guidelines mandating temperature management protocols. The U.S. Food and Drug Administration (FDA) classifies blood and plasma warming devices under 21 CFR 864.9205 as Class II medical devices requiring 510(k) clearance, ensuring substantial equivalence and patient safety standards. Healthcare facilities are increasingly implementing normothermia protocols spanning the entire perioperative journey from preoperative warming through postoperative care, creating sustained demand for advanced warming technologies that can precisely control infusion temperatures and maintain patient core body temperature within the optimal 36°C to 38°C range.

Technological Advancements in Portable and Battery-Operated Warming Devices Expanding Market Penetration

Innovation in portable warming device technology has significantly broadened the applicability of blood fluid warming systems beyond traditional hospital operating rooms into prehospital emergency care, military medical operations, and ambulance transport settings. In June 2024, the U.S. FDA granted 510(k) clearance to the M Warmer System from Danish MedTech company MEQU, a battery-powered blood and IV fluid warmer specifically designed for military, emergency medical services, and hospital environments. This device addresses critical gaps in prehospital care by enabling warming at the point of injury during transport in austere environments, thereby reducing hypothermia-related mortality in hemorrhaging patients. Similarly, in September 2025, TSC Life received FDA clearance for its Fluido® AirGuard System, a moderate to high flow blood and fluid warmer capable of delivering flow rates up to 800 mL/min (48 L/hr) with automatic air detection and IV-line clamping to prevent air embolism risks. The device features a removable warming cassette that can move with patients throughout their clinical journey and achieves pressurization in under 20 seconds. These technological advancements align with evolving Tactical Combat Casualty Care (TCCC) guidelines that mandate battery-powered warming devices delivering IV/IO resuscitation fluids at temperatures between 38°C to 42°C at flow rates up to 150 mL/min to reduce hypothermia risk in combat conditions. The convergence of user-centric design, ruggedization for field deployment, and enhanced safety features positions portable warming systems as the fastest-growing product segment in the market.

Restraints - High Capital Investment and Total Cost of Ownership Limiting Adoption in Resource-Constrained Settings

The substantial capital expenditure required for advanced blood fluid warming systems, combined with ongoing operating expenses including disposable warming cartridges, administration sets, and maintenance costs, creates significant financial barriers, particularly for healthcare facilities in developing regions and smaller ambulatory surgical centers. Economic analyses indicate that even mildly hypothermic patients can suffer adverse outcomes costing between US$2,500 and US$7,000 per case, yet the upfront investment in warming equipment and associated consumables may exceed budget allocations for facilities operating under tight reimbursement structures. Price-sensitive public hospitals in emerging markets often delay procurement of sophisticated warming technologies in favor of more basic passive warming methods using blankets and environmental temperature adjustments, despite evidence demonstrating the superior efficacy of active warming systems. This cost-benefit evaluation becomes particularly challenging for emergency medical service providers and rural healthcare centers that must weigh device efficiency against limited capital budgets, creating adoption hesitancy that restrains market penetration in high-potential growth regions.

Stringent Regulatory Requirements and Compliance Complexities Delaying Market Entry

The rigorous regulatory landscape governing blood fluid warming devices imposes substantial compliance burdens on manufacturers seeking market authorization across multiple geographies. Devices must undergo extensive clinical testing and validation to demonstrate substantial equivalence to predicate devices, maintain precise temperature control within narrow therapeutic windows to prevent both hypothermia and hyperthermia risks, and incorporate safety mechanisms addressing potential complications such as hemolysis, air embolism, and thermal injury. Regulatory variability across regions further compounds these challenges, with the European Union's Medical Device Regulation (MDR) imposing different requirements compared to FDA pathways, necessitating parallel compliance strategies that extend development timelines and increase commercialization costs. Additionally, post-market surveillance obligations and adverse event reporting requirements demand ongoing quality management investments. These regulatory complexities create high barriers to entry for smaller device manufacturers and can delay the introduction of innovative warming technologies, particularly portable and field-deployable systems intended for emergency and military applications where device performance must be validated under extreme environmental conditions.

Opportunity - Expansion of Emergency Medical Services and Prehospital Care Infrastructure Creating Demand for Portable Solutions

The global expansion of emergency medical service systems, particularly in rapidly developing economies across Asia Pacific and Latin America, presents significant growth opportunities for portable blood fluid warming devices designed for prehospital trauma care. Epidemiological data reveals that trauma patients face substantial hypothermia risk during ambulance transport, with studies demonstrating that early administration of warmed blood or fluids by emergency responders can dramatically reduce complications associated with the lethal triad of hypothermia, acidosis, and coagulopathy.

The integration of portable warming devices into ambulance fleets has shown measurable clinical benefits, including the documented 22% relative risk reduction in admission hypothermia when fluid warmers are deployed in prehospital settings. Government initiatives focused on strengthening emergency response capabilities, combined with increasing recognition of temperature management as a critical component of trauma care protocols, are driving procurement of battlefield-grade portable warming equipment. The Department of Defense has placed portable warming systems on its priority acquisition list following validation trials with military units and helicopter emergency medical services. Manufacturers developing lightweight, battery-operated warming devices with one-button operation, minimal setup requirements, and the ability to function reliably across extreme temperature ranges are well-positioned to capture this expanding market segment. Furthermore, the increasing deployment of air ambulance services and helicopter emergency medical transport creates demand for compact warming solutions that integrate seamlessly with existing flight medical equipment and can operate effectively at high altitudes and variable environmental conditions.

Category-wise Analysis

Product Insights

Blood & IV fluid warming systems dominate the product category with a commanding 39% share in 2025, reflecting their critical role as the primary solution for preventing perioperative hypothermia across diverse clinical applications. These inline warming devices, which heat banked blood, blood products, intravenous solutions, and irrigation fluids from approximately 4°C to near body temperature (35°C to 37°C) through conductive or resistive heat transfer mechanisms, have become standard equipment in operating rooms, intensive care units, and emergency departments worldwide.

The widespread adoption of blood & IV fluid warming systems is further reinforced by regulatory mandates and clinical guidelines from organizations including AORN, the American Society of PeriAnesthesia Nurses, and international bodies that recommend active warming throughout the perioperative journey. Market leaders, including 3M Company, ICU Medical, Stryker Corporation, GE Healthcare, and Baxter International, have established comprehensive product portfolios with both high-flow rapid infusion systems for trauma and emergency care and standard-flow devices for routine surgical procedures, ensuring segment dominance across multiple end-user applications and geographic markets.

End-user Insights

Hospitals command the largest market share in 2025 across the end-user category, reflecting their position as the primary centers for surgical procedures, critical care, and emergency interventions requiring sophisticated temperature management infrastructure. Hospital operating rooms, intensive care units, emergency departments, and postanesthesia care units maintain multiple warming devices to ensure continuous availability across concurrent procedures and diverse patient populations.

The high patient volume, complex case mix, and regulatory compliance requirements drive hospitals to invest substantially in advanced warming technologies, with large tertiary care centers maintaining device inventories that include both stationary high-flow rapid infusion systems for trauma resuscitation and standard blood & IV fluid warmers for routine surgical cases. Hospital procurement strategies increasingly emphasize total cost of ownership considerations, evaluating device efficiency, disposable consumable costs, maintenance requirements, and integration capabilities with existing electronic health record systems for automated temperature documentation.

Evidence-based medicine initiatives and quality improvement reinforce the segment's dominance programs focused on surgical site infection prevention, with many hospital systems implementing mandatory normothermia protocols as part of enhanced recovery after surgery pathways. Additionally, hospitals serve as the primary training environment for healthcare professionals learning temperature management best practices, creating institutional preferences for established brands such as 3M, ICU Medical, Stryker, and Baxter that offer comprehensive clinical education programs, technical support, and validated performance across millions of patient encounters worldwide.

Regional Insights

North America Blood Fluid Warming System Market Trends and Insights

North America maintains regional market leadership with a dominant 37% market share in 2025, underpinned by advanced healthcare infrastructure, stringent patient safety regulations, and widespread adoption of evidence-based perioperative protocols across the United States and Canada. The U.S. market benefits from robust regulatory oversight by the FDA, which ensures rigorous device validation and post-market surveillance, creating confidence among healthcare providers in warming system safety and efficacy. Major medical device manufacturers, including 3M Company (now operating as Solventum for certain divisions), ICU Medical, Stryker Corporation, GE Healthcare, and Baxter International maintain significant commercial and manufacturing operations throughout North America, ensuring rapid product distribution, technical service availability, and clinical education resources.

The region's leadership is further reinforced by comprehensive clinical guideline adoption, with institutions implementing normothermia protocols aligned with AORN recommendations mandating temperature monitoring and active warming throughout the perioperative continuum. Recent regulatory clearances have accelerated technology adoption, including the 2024 FDA approval of the MEQU M Warmer System for military and civilian emergency medical services, and the September 2025 clearance of the TSC Life Fluido® AirGuard System, expanding portable warming capabilities for prehospital trauma care. Healthcare economic pressures and value-based reimbursement models incentivize hospitals to invest in warming technologies that demonstrably reduce complications, shorten length of stay, and improve surgical outcomes, aligning clinical quality improvements with financial performance metrics in the highly competitive North American healthcare market.

Asia Pacific Blood Fluid Warming System Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with the highest projected growth rate, propelled by massive healthcare infrastructure expansion, rising surgical volumes, increasing trauma case burdens, and growing awareness of perioperative hypothermia prevention across China, India, Japan, Australia, and Southeast Asian nations. China leads regional growth driven by government initiatives to modernize medical facilities, with its total motor vehicle fleet expanding 68.12% from 207 million in 2010 to 348 million in 2019, contributing to substantial increases in road traffic accidents and associated trauma care demand that necessitate temperature management capabilities in emergency departments and trauma centers. Analysts project China's blood warmer market will experience continued expansion throughout the forecast period, supported by rising patient safety awareness, government programs addressing cold weather injury prevention, and rapid medical technology advancement.

Competitive Landscape

The competitive landscape of the blood fluid warming system market is shaped by continuous innovation, technological differentiation, and expanding clinical applications. Manufacturers are focusing on enhancing device accuracy, safety features, and ease of use to meet rigorous healthcare standards and improve patient outcomes. Strategic investments in research and development are driving advanced solutions that address diverse care settings, from emergency response to intensive care units. Market players are also expanding their reach into emerging regions, strengthening distribution networks and after-sales service capabilities.

Key Market Developments

- In February 2026, TSC Life, a global medtech company focused on high-performance devices for temperature management and endoscopy, announced that the U.S. Food and Drug Administration had cleared its Fluido® Compact Fluid Warming System for pediatric use.

Companies Covered in Blood Fluid Warming System Market

- 3M Company

- ICU Medical

- Stryker Corporation

- GE Healthcare

- Baxter International

- Belmont Medical Technologies

- Barkey GmbH & Co. KG

- Biegler GmbH, Inspiration Healthcare Group

- Emit Corporation

- Vyaire Medical

- Estill Medical Technologies

- MEQU A/S, TSC Life

- Gentherm Incorporated

- Smithworks Medical Inc.

- Life Warmer

Frequently Asked Questions

The global blood fluid warming system market is expected to be valued at US$ 523.3 million in 2026, reflecting steady expansion driven by increasing surgical volumes, growing awareness of perioperative hypothermia prevention, and widespread adoption of temperature management protocols mandated by organizations such as the Association of periOperative Registered Nurses (AORN) across hospital operating rooms, intensive care units, and emergency departments worldwide.

Market growth is primarily driven by the increasing incidence of surgical procedures and trauma cases requiring temperature management, clinical evidence demonstrating that hypothermia triples surgical site infection risk and that maintaining normothermia at 36.5°C reduces hospital length of stay by 2.6 days, technological advancements in portable battery-operated warming devices receiving FDA clearances for emergency medical services and military applications, and stringent regulatory requirements under 21 CFR 864.9205 ensuring device safety and efficacy across perioperative care settings.

North America maintains regional market leadership with a 37% market share in 2025, supported by advanced healthcare infrastructure, stringent FDA regulatory oversight, widespread implementation of evidence-based normothermia protocols aligned with AORN guidelines, and strong commercial presence of major device manufacturers including 3M Company, ICU Medical, Stryker Corporation, GE Healthcare, and Baxter International serving extensive hospital and emergency medical service networks across the United States and Canada.

Significant opportunities include the expansion of emergency medical services and prehospital care infrastructure creating demand for portable warming solutions, particularly in rapidly developing Asia Pacific economies where government procurement of battlefield-grade equipment following disaster responses drives adoption, and growing emphasis on pediatric and neonatal temperature management unlocking specialized product development for vulnerable populations where UNICEF data shows approximately 67,385 infants born daily in India alone require advanced thermal regulation during medical procedures to prevent hypothermia-related complications.

Leading market participants include 3M Company (now operating as Solventum Corporation for certain healthcare divisions), ICU Medical, Stryker Corporation, GE Healthcare, Baxter International, Belmont Medical Technologies, Barkey GmbH & Co. KG, Biegler GmbH, Inspiration Healthcare Group, Emit Corporation, Vyaire Medical, and Estill Medical Technologies, along with emerging innovators such as °MEQU A/S and TSC Life receiving recent FDA clearances for advanced portable warming systems targeting emergency medical services, military medical operations, and hospital markets worldwide.