- Medical Devices

- Microtainer Blood Collection Market

Microtainer Blood Collection Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Microtainer Blood Collection Market by Product (Serum Separator Gel (SSG) Tubes, EDTA Tubes, Heparin Tubes, Plasma Separator Tubes, and Capillary Blood Collection Tubes), by Shape (Cylindrical and Round-bottom), by End User (Hospitals, Specialty Clinics, Diagnostic Laboratories, Blood Banks, and Academic & Research Institutions), and Regional Analysis from 2026 to 2033

Microtainer Blood Collection Market Share and Trend Analysis

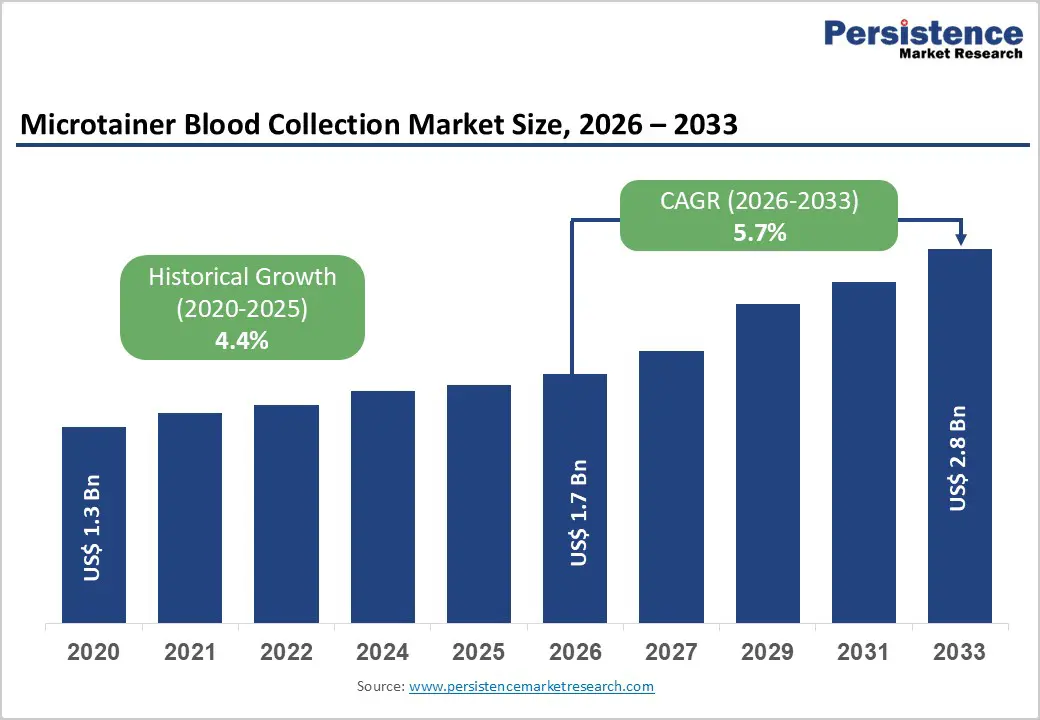

The global microtainer blood collection market size is estimated to grow from US$ 1.7 Bn in 2026 to US$ 2.8 Bn by 2033. The market is projected to record a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for microtainer blood collection products is increasing steadily, driven by rising diagnostic testing volumes, expanding preventive healthcare programs, and a growing emphasis on minimally invasive and patient-centric sampling methods. Hospitals, clinics, and diagnostic laboratories are increasingly adopting microtainer systems to support accurate testing while minimizing blood loss, particularly in pediatric, neonatal, geriatric, and critically ill populations. Aging populations, higher prevalence of chronic diseases, and increased screening for infectious and metabolic disorders are significantly raising the frequency of blood tests worldwide. Microtainer solutions are widely used across hospitals, outpatient settings, and diagnostic laboratories to improve sample quality, reduce pre-analytical errors, and enhance workflow efficiency. Growing preference for standardized, safe, and low-volume blood collection methods is accelerating adoption, especially as healthcare providers aim to improve patient comfort and testing turnaround times. Increased focus on infection prevention, laboratory accreditation, and quality assurance further supports demand. Technological improvements in tube materials, additives, and compatibility with automated analyzers are enhancing performance and usability. In parallel, strengthening healthcare infrastructure in emerging markets and rising investments in diagnostic capacity are reinforcing long-term global demand for microtainer blood collection solutions.

Key Industry Highlights

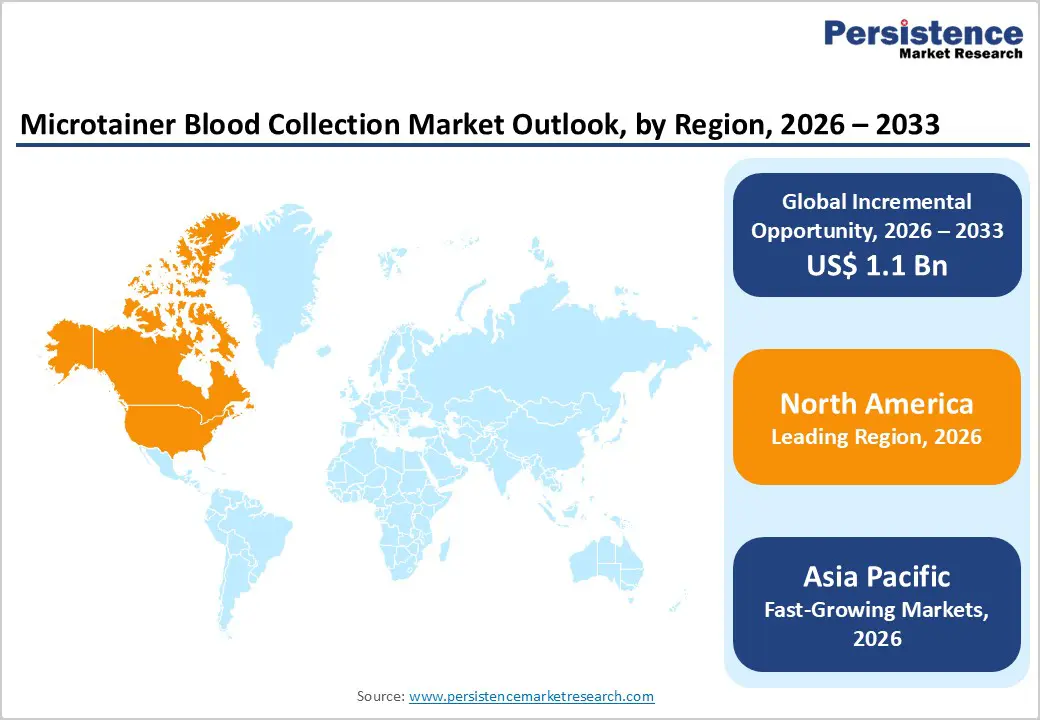

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high diagnostic testing volumes, strong regulatory standards, and widespread adoption of laboratory automation.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid healthcare infrastructure development, rising disease burden, increasing diagnostic awareness, and growth of private healthcare facilities.

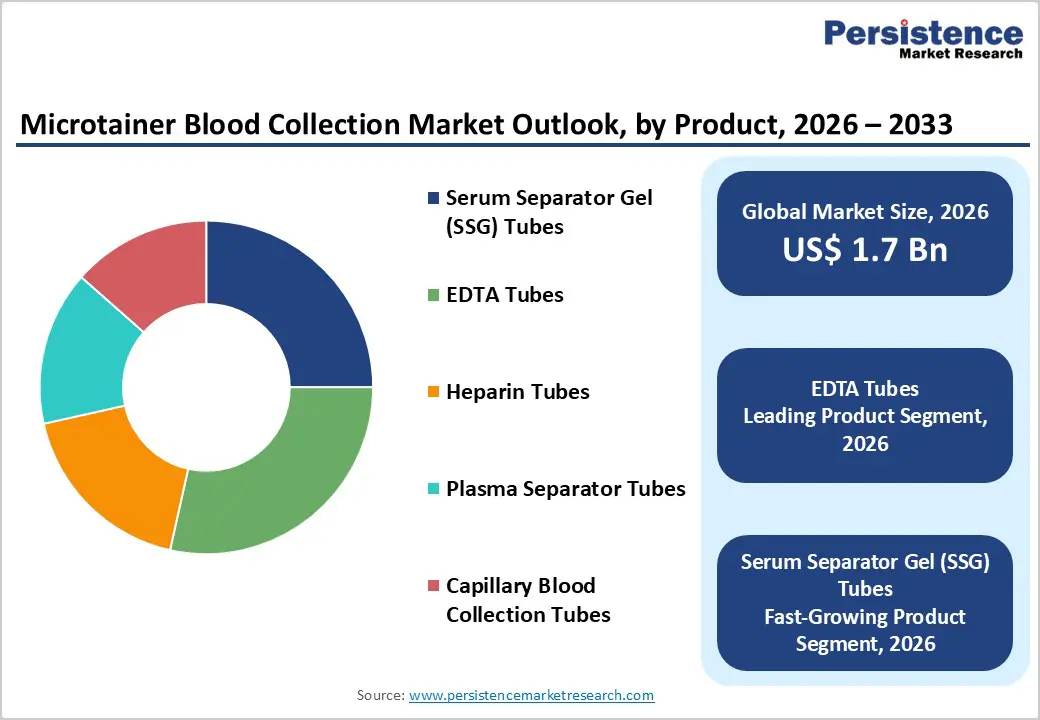

- Leading Product Segment: EDTA Tubes dominate the market due to their critical role in hematology testing, sample stability, and compatibility with automated diagnostic workflows.

- Fastest-Growing Product Segment: Serum Separator Gel (SSG) Tubes are growing rapidly as routine biochemical and immunoassay testing volumes increase across hospitals and laboratories.

- Leading End User Segment: Hospitals remain the top segment, driven by high patient footfall, frequent diagnostic testing, and integrated laboratory services.

- Fastest-Growing User Segment: Diagnostic Laboratories are scaling quickly as testing volumes rise and providers invest in automation and high-throughput diagnostic platforms.

| Key Insights | Details |

|---|---|

| Microtainer Blood Collection Market Size (2026E) | US$ 1.7 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver – Rising Diagnostic Testing Volumes, Shift Toward Minimally Invasive Sampling, and Pediatric Care Demand

Growth is strongly supported by the steady increase in diagnostic testing volumes worldwide, driven by the rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, anemia, and infectious conditions. As healthcare systems emphasize early diagnosis and routine monitoring, demand for frequent blood testing has increased across hospitals, clinics, and diagnostic laboratories. Microtainer blood collection products play a critical role by enabling accurate testing with minimal blood volume, which is particularly important in pediatric, neonatal, geriatric, and critically ill patient populations. The shift toward minimally invasive and patient-friendly diagnostic procedures further accelerates adoption, as microtainer systems reduce discomfort, anxiety, and the risk of iatrogenic anemia.

Additionally, the expansion of point-of-care testing and decentralized diagnostics has increased reliance on capillary blood collection methods. Healthcare providers also prioritize sample integrity and pre-analytical accuracy, as errors at the collection stage can compromise diagnostic outcomes. Microtainer tubes are designed to support precise anticoagulant ratios and consistent sample quality, supporting laboratory standardization. Regulatory focus on patient safety, infection control, and standardized diagnostic protocols further reinforces demand. Together, increasing test frequency, demographic-driven healthcare needs, and a growing preference for low-volume, safe blood collection methods continue to drive sustained market growth.

Restraints – Cost Sensitivity, Limited Awareness, and Pre-Analytical Handling Challenges

Market expansion is restrained by cost sensitivity among healthcare providers, particularly in low- and middle-income regions where budget constraints influence procurement decisions. While microtainer products offer clinical benefits, they are often priced higher than conventional blood collection alternatives, which can limit adoption in cost-focused settings such as public hospitals and small clinics. Limited awareness among healthcare workers regarding the clinical advantages of microtainer systems also acts as a barrier, especially in regions where traditional venous collection remains the standard practice.

Pre-analytical handling challenges further constrain growth. Capillary blood collection requires proper technique to avoid hemolysis, clotting, or insufficient sample volume, and inadequate training can lead to higher sample rejection rates. This can discourage laboratories from widespread adoption due to concerns around diagnostic reliability. In addition, compatibility issues with certain automated analyzers or laboratory workflows may necessitate process adjustments, increasing operational complexity. Supply chain limitations, particularly for specialized microtainer variants, can also affect consistent availability in emerging markets. Collectively, pricing pressure, training gaps, workflow adaptation requirements, and logistical constraints limit penetration across certain healthcare environments.

Opportunity – Expansion of Point-of-Care Testing, Home Diagnostics, and Emerging Healthcare Markets

Significant opportunities are emerging from the rapid expansion of point-of-care testing and home-based diagnostic models, where ease of use and low blood volume requirements are essential. Microtainer blood collection products are well suited for decentralized testing environments, including home healthcare, mobile diagnostics, and community screening programs. As healthcare systems shift toward preventive care and remote patient monitoring, demand for convenient and patient-friendly blood collection solutions is expected to rise.

Emerging markets across Asia Pacific, Latin America, and the Middle East present substantial growth potential as healthcare infrastructure continues to expand. Increasing investments in diagnostic laboratories, outpatient facilities, and maternal and child health programs are creating new demand for microtainer systems. Technological advancements in tube materials, additives, and safety features further enhance product performance and usability. Opportunities also exist in pediatric and neonatal care segments, where minimizing blood loss is clinically critical. Strategic collaborations between manufacturers, diagnostic companies, and healthcare providers can support education, training, and broader adoption. As healthcare delivery becomes more decentralized and patient-centric, microtainer blood collection solutions are well positioned to benefit from long-term structural shifts in diagnostics.

Category-wise Analysis

By Product, EDTA Tubes Lead Due to High Diagnostic Accuracy and Hematology Test Demand

EDTA tubes are projected to dominate the global microtainer blood collection market in 2026, accounting for a revenue share of 28.5%. Their leadership is driven by extensive use in hematology testing, including complete blood counts and differential analysis, where anticoagulant stability and sample integrity are critical. EDTA microtainer tubes enable accurate cell morphology preservation even with low-volume capillary samples, making them essential in pediatric, geriatric, and point-of-care settings. Increasing diagnostic testing volumes, rising prevalence of chronic and blood-related disorders, and growing adoption of minimally invasive blood collection methods further support demand. In addition, EDTA tubes are widely compatible with automated hematology analyzers, improving laboratory workflow efficiency and reducing pre-analytical errors. Regulatory emphasis on standardized sample quality and laboratory accreditation also reinforces their widespread adoption. As diagnostic laboratories and hospitals continue to prioritize reliable, low-volume blood collection solutions, EDTA tubes remain the leading product segment.

By Shape, Cylindrical Microtainer Tubes Dominate Due to Ease of Handling and Automation Compatibility

Cylindrical microtainer tubes are expected to dominate the global microtainer blood collection market in 2026, capturing a revenue share of 74.8%. This dominance is primarily attributed to their ergonomic design, ease of handling during capillary blood collection, and seamless compatibility with automated laboratory analyzers. Cylindrical tubes are widely preferred by healthcare professionals as they simplify sample labeling, centrifugation, storage, and transport while minimizing spillage and handling errors. Their standardized shape supports efficient integration into existing diagnostic workflows, particularly in high-throughput hospital and laboratory environments. Cost efficiency and established clinical familiarity further drive adoption across both developed and emerging markets. While alternative designs exist, cylindrical tubes remain the industry standard due to proven reliability and operational convenience. As diagnostic volumes continue to rise and laboratories emphasize workflow standardization, cylindrical microtainer tubes are expected to retain their leading market position.

By End User, Hospitals Lead Due to High Patient Footfall and Diagnostic Testing Volumes

Hospitals are projected to dominate the global microtainer blood collection market in 2026, accounting for a revenue share of 30.6%. This leadership is driven by high inpatient and outpatient volumes, frequent diagnostic testing requirements, and the need for efficient blood collection across multiple clinical departments. Hospitals routinely manage pediatric, neonatal, geriatric, and critically ill patients, where microtainer tubes are preferred due to minimal blood volume requirements and reduced patient discomfort. The availability of advanced laboratory infrastructure and trained phlebotomy staff further supports adoption. Hospitals also prioritize standardized, sterile, and regulatory-compliant blood collection products to maintain diagnostic accuracy and patient safety. While diagnostic laboratories and clinics are increasingly adopting microtainer systems, hospitals remain the largest revenue contributors due to their scale, complexity, and continuous testing demand. Ongoing hospital expansion and rising admissions further reinforce hospital dominance.

Region-wise Insights

North America Microtainer Blood Collection Market Trends

North America is expected to dominate the global microtainer blood collection market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare infrastructure, widespread access to diagnostic services, and high testing volumes across hospitals and laboratories. Strong adoption of minimally invasive blood collection techniques, particularly in pediatric and geriatric care, supports sustained demand for microtainer products. Regulatory emphasis on patient safety, infection prevention, and standardized diagnostic practices further accelerates market adoption.

Healthcare providers in North America actively invest in high-quality, reliable blood collection consumables to reduce pre-analytical errors and improve diagnostic accuracy. High healthcare expenditure, favorable reimbursement frameworks, and strong laboratory automation penetration also contribute to market growth. The presence of established manufacturers, robust distribution networks, and continuous product innovation further strengthens regional leadership. Increasing demand for point-of-care testing and home-based diagnostics is expected to maintain North America’s position as the most mature and revenue-dominant market.

Europe Microtainer Blood Collection Market Trends

The Europe microtainer blood collection market is expected to grow steadily, supported by well-established healthcare systems and strong regulatory oversight across countries such as Germany, the U.K., France, Italy, and Spain. European healthcare providers place significant emphasis on diagnostic accuracy, patient comfort, and compliance with medical device quality standards, driving consistent demand for microtainer blood collection products. Rising aging populations across the region contribute to increased diagnostic testing volumes, particularly for chronic disease monitoring and routine health assessments.

Public healthcare systems are increasingly adopting minimally invasive blood collection methods to improve patient experience and reduce procedural risks. Expansion of outpatient care, diagnostic laboratories, and preventive screening programs further supports market growth. Additionally, hospitals and laboratories are focusing on standardized consumables to improve workflow efficiency and reduce sample rejection rates. Investments in laboratory automation and point-of-care diagnostics continue to reinforce demand, positioning Europe as a stable and steadily expanding regional market.

Asia Pacific Microtainer Blood Collection Market Trends

The Asia Pacific microtainer blood collection market is expected to register a relatively higher CAGR of around 7.7% between 2026 and 2033, driven by rapid healthcare infrastructure development and rising diagnostic demand. Countries such as China, India, Japan, South Korea, and Australia are witnessing increased investments in hospital expansion, diagnostic laboratories, and preventive healthcare services. Growing awareness of early disease detection, coupled with rising prevalence of chronic and lifestyle-related conditions, is significantly increasing blood testing volumes. Microtainer tubes are gaining traction due to their suitability for pediatric care, outpatient diagnostics, and resource-efficient testing environments.

Expansion of private hospitals, specialty clinics, and point-of-care testing facilities is improving market penetration. Cost-effective microtainer solutions are particularly attractive in price-sensitive markets, while advanced healthcare institutions are adopting premium products for accuracy and safety. Government initiatives to improve healthcare access, along with rising medical tourism, further support Asia Pacific’s position as the fastest-growing regional market.

Market Competitive Landscape

The global microtainer blood collection market is highly competitive, with strong participation from companies such as BD, B Braun SE, Sarstedt AG & Co. KG, Terumo Corporation, and Siemens Healthineers. These players leverage extensive global distribution networks, strong brand recognition, and diversified blood collection and diagnostic consumables portfolios to address the rising demand for safe, minimally invasive, and accurate capillary blood sampling across healthcare settings.

Their offerings emphasize product reliability, sample integrity, accurate blood volume collection, ease of use, patient comfort (especially in pediatric and geriatric populations), and compatibility with automated laboratory analyzers and diagnostic workflows in hospitals, clinics, and diagnostic laboratories. Continuous product innovation, regulatory compliance, sterility assurance, material quality, and adherence to international standards for blood collection and in vitro diagnostics remain critical for sustaining competitive positioning in the global microtainer blood collection market.

Key Industry Developments:

- In April 2024, BD launched the BD Vacutainer® UltraTouch™ Push Button Blood Collection Set in India to reduce patient pain and improve single-prick success. Featuring BD RightGauge™ and PentaPoint™ technologies, the device uses a thinner needle to significantly lower insertion pain, while BD Push Button Technology reduces needlestick injury risk by 88%.

- In March 2024, BD India introduced a new blood collection device designed to minimize patient discomfort during sample collection. The launch reflects BD’s focus on enhancing patient experience and improving compliance, particularly in high-volume diagnostic and outpatient settings where repeated blood draws are common.

- In December 2023, BD received FDA 510(k) clearance for a fingerstick blood sample collection device. This regulatory approval enables BD, in collaboration with Babson Diagnostics, to expand blood collection beyond traditional clinical settings by supporting sample collection at community locations such as retail pharmacies and decentralized care sites.

Companies Covered in Microtainer Blood Collection Market

- BD

- B Braun SE

- Sarstedt AG & Co. KG

- Terumo Corporation

- Siemens Healthineers

- Thermo Fisher Scientific Inc.

- Sekisui Diagnostics

- Cardinal Health, Inc.

- Kent Scientific

- Radiometer Medical

- Vitrex Medical A/S

- Greiner Bio-One

- Others

Frequently Asked Questions

The global microtainer blood collection market is projected to be valued at US$ 1.7 Bn in 2026.

Rising prevalence of chronic and lifestyle diseases requiring frequent blood tests, growing demand for point-of-care and minimally invasive sampling, technological advancements in microtainer designs improving ease and safety, and expanding adoption in paediatric, geriatric, and home healthcare settings.

The global microtainer blood collection market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Integration of AI, machine learning, and cloud-based tracking solutions to enhance real-time instrument visibility, workflow efficiency, and predictive asset management.

BD, B Braun SE, Sarstedt AG & Co. KG, Terumo Corporation, and Siemens Healthineers are some of the key players in the body microtainer blood collection market.