- Non-food Packaging

- Beer Packaging Market

Beer Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Beer Packaging Market by Material (Glass, Metal/Aluminum, Others), Packaging Type (Bottles, Cans, Others), Beer Type, and Regional Analysis for 2026 - 2033

Beer Packaging Market Size and Trends Analysis

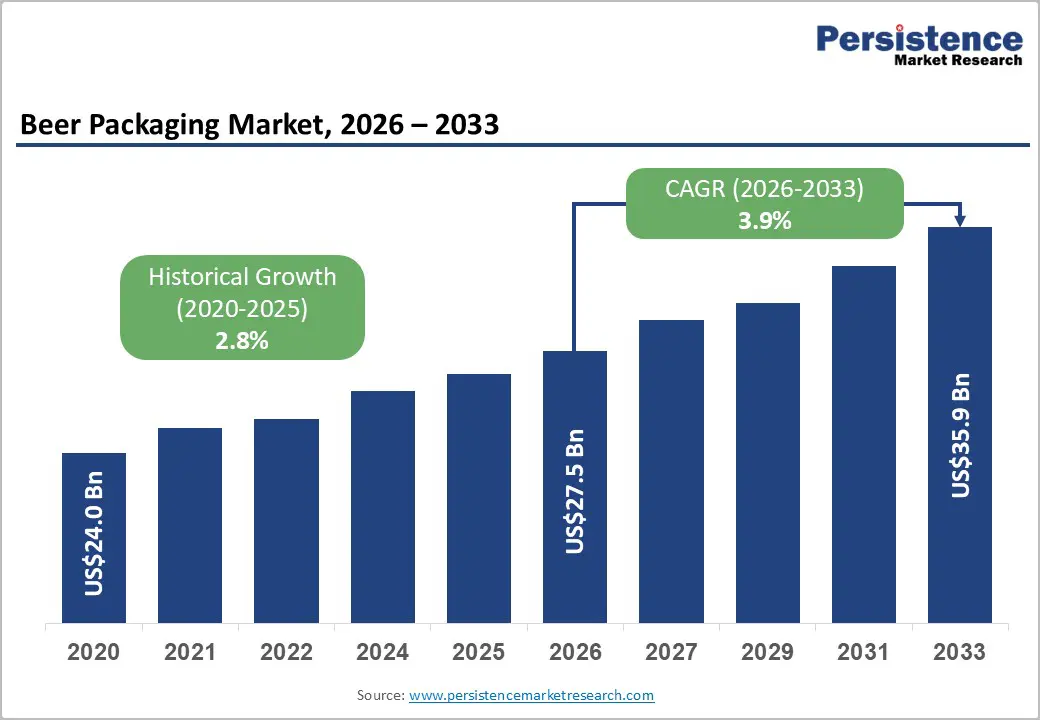

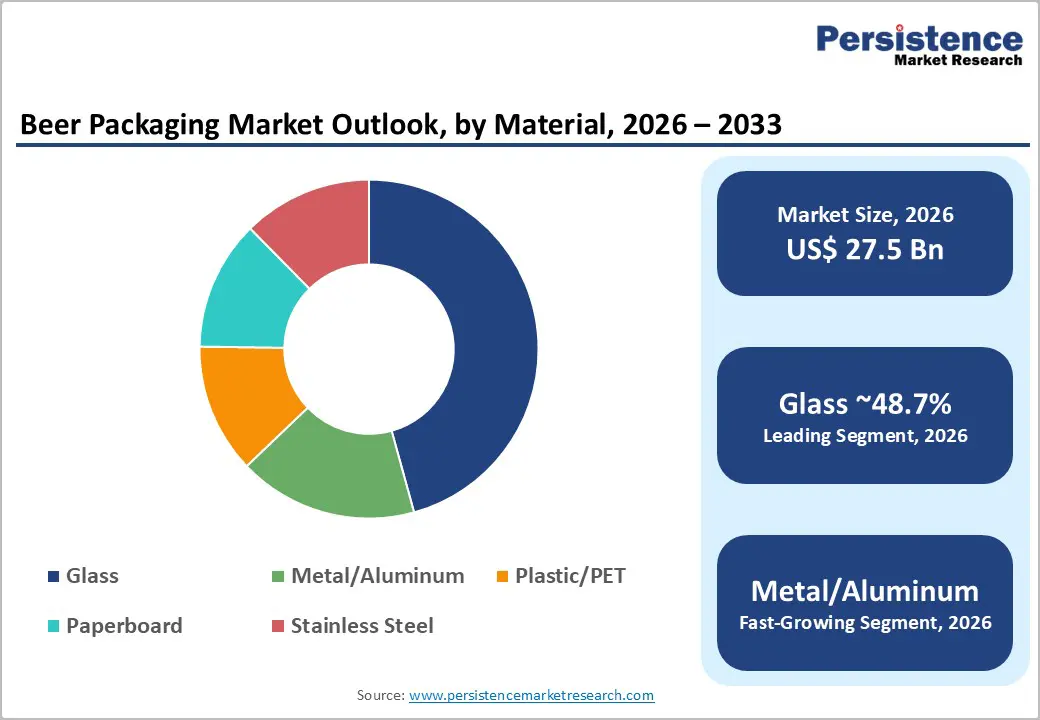

The global beer packaging market size is likely to be valued at US$27.5 billion in 2026 and is expected to reach US$35.9 billion by 2033, growing at a CAGR of 3.9% between 2026 and 2033, driven by structural shifts toward aluminum cans, sustained demand for glass bottles in premium beer categories, and the rapid rise of craft and specialty beers that favor small-format and differentiated packaging.

Sustainability mandates, lightweighting initiatives, and investments in packaging capacity continue to reshape material preferences and supply-chain strategies across global breweries.

Key Industry Highlights:

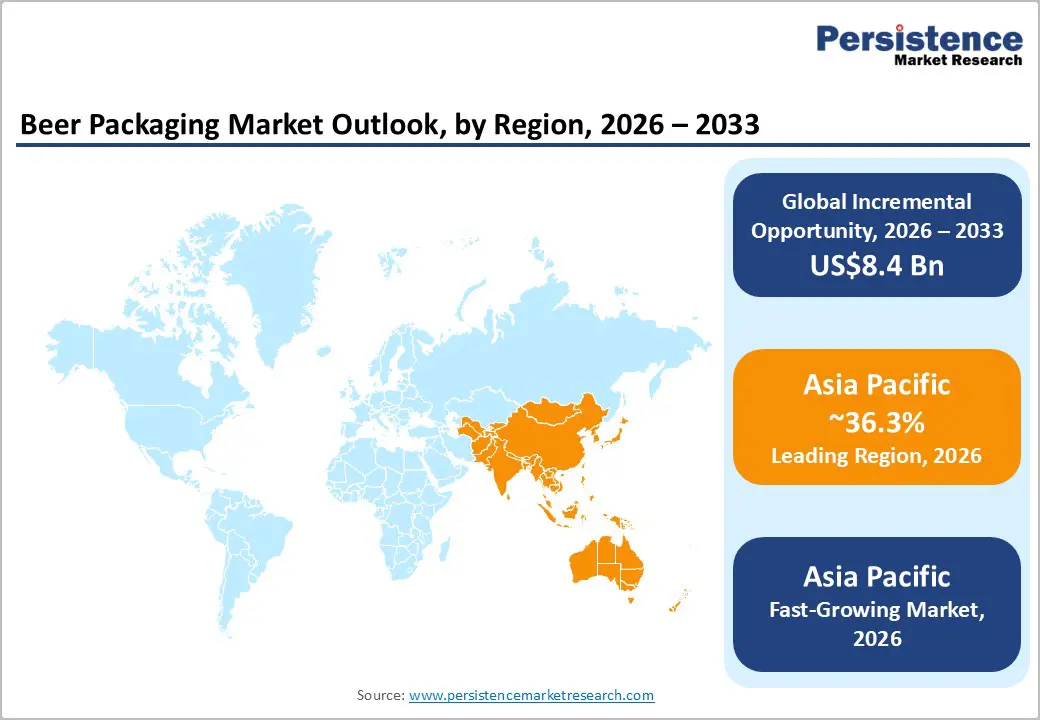

- Leading Region: Asia-Pacific is projected to lead the market, with over 36.3% market share, supported by high beer consumption in China and India, rapid urbanization, and the expansion of convenience retail and e-commerce channels.

- Fastest-growing Region: Asia-Pacific is also likely to be the fastest-growing regional market, driven by rising disposable incomes, premiumization in Japan and Southeast Asia, and increasing adoption of aluminum cans for urban and on-the-go consumption occasions.

- Investment Plans: Breweries and packaging suppliers are prioritizing capacity expansion in aluminum can manufacturing, flexible filling lines, and automated packaging systems, particularly in Asia Pacific and North America, to improve SKU agility, sustainability compliance, and logistics efficiency.

- Dominant Material: Glass is expected to remain the dominant packaging material, accounting for approximately 48.7% of the market, supported by its strong association with premium, imported, and heritage beer brands.

- Leading Packaging Type: Bottles are estimated to represent the leading packaging type, holding over 50.4% of market share, driven by consumer perception of quality, premium pricing, and widespread use across retail and on-trade distribution channels.

| Key Insights | Details |

|---|---|

| Beer Packaging Market Size (2026E) | US$27.5 Bn |

| Market Value Forecast (2033F) | US$35.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Aluminum Can Conversion and Portability

Aluminum cans continue to gain market share across global beer markets due to their portability, high recyclability, and branding flexibility. Cans are lightweight, unbreakable, and compatible with on-the-go consumption occasions, making them well-suited for modern retail and outdoor settings. Their full-surface printability supports strong brand differentiation, particularly for craft and specialty beers. From a manufacturing perspective, can packaging offer higher throughput and operational efficiency than glass packaging? The continued rollout of high-speed can lines and regional capacity expansions support a sustained multi-percentage-point annual increase in aluminum’s share in beer packaging across major markets.

Premiumization and Brand Differentiation through Glass Packaging

Despite rising can adoption, glass bottles remain central to premium and super-premium beer positioning. Consumers continue to associate glass with quality, authenticity, and heritage, particularly for imported, specialty, and limited-edition beers. Packaging producers have responded with lighter-weight bottles, improved ergonomic shapes, and expanded labeling areas, thereby reducing transportation costs while preserving premium aesthetics. These innovations allow glass to retain its leadership position by value, even as volume growth increasingly favors cans. Premiumization trends support higher-margin glass formats and reinforce long-term demand stability.

Sustainability, Circularity, and Regulatory Pressure

Sustainability has become a decisive factor in packaging procurement. Regulatory frameworks and retailer commitments to recycled content and emissions reduction are accelerating investment in circular packaging systems. Aluminum benefits from strong closed-loop recycling economics, whereas glass continues to advance through lightweighting and optimization of recycled content. Paperboard and PET packaging solutions are also gaining traction, with lifecycle assessments supporting lower environmental impacts. Packaging suppliers with credible sustainability roadmaps are increasingly favored in long-term contracts with large brewers, reinforcing sustainability as a core competitive differentiator.

Barrier Analysis - Raw Material and Energy Price Volatility

Beer packaging materials, particularly glass and aluminum, are energy-intensive to produce. Volatility in energy prices and raw material inputs such as alumina and natural gas can significantly affect production costs. Elevated energy prices reduce margin visibility and may temporarily weaken the cost competitiveness of glass packaging in certain regions. Historically, such volatility has resulted in mid-single-digit margin pressure during high-cost cycles and can delay capital investments in new furnaces or production lines if sustained over extended periods.

Capital Intensity and Supply-Chain Complexity

Packaging capacity expansion requires substantial capital investments and long lead times. High-speed aluminum can lines and glass furnaces often require 12-24 months to commission and involve investments running into tens of millions of U.S. dollars. Logistical challenges, including port congestion and container shortages, further complicate supply planning. Smaller breweries face additional risks due to minimum-order requirements and tooling costs when switching packaging formats, thereby limiting flexibility during demand fluctuations.

Opportunity Analysis - Asia Pacific Expansion and Localized Production Capacity

Asia Pacific represents the largest incremental growth opportunity in beer packaging. Rising disposable incomes, expanding urban populations, and increasing beer consumption are driving demand across China, India, and Southeast Asia. Aluminum cans and lightweight glass bottles present particularly strong opportunities. By investing in localized manufacturing capacity, service hubs, and region-specific product offerings, packaging suppliers can capture several billion U.S. dollars in incremental value by 2033 while reducing logistics costs and improving supply responsiveness.

Premium Craft and Single-Serve Innovation

Craft and specialty beers are the fastest-growing beer type globally and favor premium, small-format packaging. If the craft segment expands its market share by even 1-2 percentage points, the resulting value uplift to packaging demand could reach hundreds of millions of U.S. dollars over the forecast period. Opportunities exist in specialty can designs, premium glass finishes, and digitally enabled packaging solutions such as QR codes and augmented reality. These innovations command higher per-unit pricing and strengthen long-term partnerships with brewers.

Category-wise Analysis

Material Insights

Glass is anticipated to remain the leading material in beer packaging by value, accounting for approximately 48.7% of the market share in 2026. Its dominance is anchored in a long-standing association with product quality, flavor stability, and premium brand positioning. Major international breweries such as Heineken, AB InBev, and Carlsberg continue to rely heavily on glass bottles for flagship and export-oriented brands, particularly in Europe and North America. Glass offers excellent barrier properties against oxygen and carbon dioxide loss, which is critical for taste preservation in lagers and specialty beers.

Ongoing innovation has strengthened glass’s competitiveness. Lightweight bottle designs, returnable glass systems, and improved labeling technologies have reduced transportation costs and enhanced sustainability profiles. For example, several European breweries have reduced bottle weight by more than 10% over the past decade, thereby lowering energy use per unit while maintaining shelf appeal. These factors enable glass packaging to retain its value leadership despite its higher energy intensity relative to alternative materials, reinforcing its strategic importance in premium and heritage-driven beer segments.

Metal, particularly aluminum cans, is anticipated to be the fastest-growing material segment. Growth is supported by rising consumer demand for portability, rapid chilling, and high recyclability. Aluminum cans have recycling rates exceeding 65% in several developed markets, making them attractive amid tightening sustainability regulations and circular economy initiatives. Leading craft and multinational brewers, including Molson Coors and Asahi, have significantly expanded can-based product lines to align with evolving consumption patterns.

Cans also offer operational advantages, including lower breakage, reduced transportation costs, and faster filling speeds, thereby enabling breweries to improve margins and production flexibility. Marketing benefits, including full-surface printing and limited-edition designs, further accelerate adoption in the craft and specialty beer segment. While aluminum continues to gain share in volume terms, glass is expected to retain its leadership in value-driven and premium positioning, creating a complementary material mix across global markets.

Packaging Type Insights

Bottles are anticipated to account for more than 50.4% of the market share in 2026, maintaining their leadership position throughout the forecast period. Their dominance is reinforced by premium pricing, strong consumer perceptions of authenticity, and extensive use across on-trade and off-trade retail channels. Bottles remain the preferred packaging format for imported, specialty, and heritage beer brands, particularly in Europe, Latin America, and parts of Asia. For example, many German and Belgian beer styles are closely linked to distinctive bottle shapes that support brand differentiation.

Continuous improvements in closure technologies, such as enhanced crown caps and oxygen-scavenging liners, have improved shelf life and quality consistency. At the same time, lightweight glass bottles and standardized formats have helped breweries reduce logistics costs and improve operational efficiency. These advancements support sustained demand for bottles in mature markets while enabling producers to balance cost pressures with premium brand positioning.

Cans are anticipated to be the fastest-growing packaging type, driven by the global expansion of craft beer, increasing outdoor and event-based consumption, and the rise of ready-to-drink alcoholic formats. Craft breweries in the United States, Japan, and Australia increasingly favor cans due to lower minimum order quantities, faster line changeovers, and improved protection from light exposure.

Cans also align well with e-commerce and direct-to-consumer distribution models, where durability and weight efficiency are critical. Investments in regional canning capacity and mobile canning services have further accelerated adoption, particularly among small and mid-sized brewers. Seasonal releases, limited-edition SKUs, and experimental beer styles benefit from the flexibility cans provide. As a result, cans are expected to continue gaining share across both developed and emerging markets, reinforcing their role as a key growth engine within the beer packaging ecosystem.

Regional Insights

North America Beer Packaging Market Trends - U.S.-Led Can Expansion amid Regulatory Modernization

North America represents one of the most mature and strategically important beer packaging markets globally, led overwhelmingly by the U.S. High per-capita beer consumption, a dense network of over 9,000 craft breweries, and a highly developed retail and distribution ecosystem sustain steady packaging demand. Aluminum cans dominate incremental volume growth, particularly among craft and regional brewers, due to portability, lower freight costs, and alignment with sustainability goals. Leading craft brands such as Sierra Nevada, New Belgium, and Boston Beer Company (Samuel Adams) have expanded can-first product strategies, reinforcing cans as the preferred format for innovation-led SKUs.

Glass maintains relevance in premium, imported, and heritage segments. Imports from Europe and Mexico, such as Corona, Heineken, and Stella Artois, continue to rely heavily on glass bottles to preserve brand identity and price positioning. Regulatory developments increasingly shape procurement decisions, with multiple U.S. states and Canadian provinces strengthening requirements for recycled content and extended producer responsibility (EPR) frameworks.

These policies encourage higher aluminum recycling rates and lightweight glass adoption. In response, packaging suppliers and breweries are investing in flexible filling lines, automated changeovers, and smart packaging technologies, allowing faster SKU rotation and lower operating costs. This combination of regulatory pressure and operational modernization continues to reshape North America’s beer packaging mix.

Europe Beer Packaging Market Trends - Refillable Glass Strongholds vs. Can Adoption in Transition Markets

Europe exhibits highly differentiated beer packaging dynamics, shaped by long-standing cultural traditions, national deposit-return schemes, and harmonized sustainability regulations. Germany, Austria, and parts of Central Europe remain strongholds for refillable glass systems, supported by well-established return logistics and consumer participation. Major brewers such as Krombacher, Bitburger, and Carlsberg continue to operate high-circulation refillable bottle pools, reinforcing glass’s dominance in these markets. These systems significantly reduce lifecycle emissions, thereby aligning with EU circular-economy objectives.

In contrast, the U.K., Spain, and parts of Southern Europe are experiencing faster adoption of aluminum cans. U.K.-based brewers, including BrewDog and Molson Coors Europe, have expanded canned portfolios to support convenience retail, festivals, and e-commerce distribution. EU-wide sustainability legislation, encompassing recycled-content mandates, packaging-waste reduction, and labeling requirements, has increased demand for lightweight materials and high-recycled-content aluminum. While overall market growth remains moderate due to maturity, momentum is strongest in markets transitioning from traditional glass-heavy formats toward cans, particularly in the craft, flavored, and low-alcohol beer segments.

Asia Pacific Beer Packaging Market Trends - High-Growth, Urbanization-Driven Can Scaling and Premium Innovation

Asia Pacific is projected to lead the market with over 36.3% of market share and represents the fastest-growing regional market. China and India account for the largest volumes, supported by large populations and expanding urban consumption, while Japan, South Korea, and Southeast Asia drive premiumization and packaging innovation. In China, leading brewers such as China Resources Snow Breweries and Tsingtao continue to scale aluminum can usage to serve convenience retail and e-commerce channels, where durability and logistics efficiency are critical.

India’s beer packaging demand is rising alongside the expansion of modern trade and changing consumption patterns, with major players such as United Breweries (Kingfisher) gradually increasing can penetration for urban and premium variants. Japan and markets like Thailand and Vietnam are driving innovation in sleek can formats, smaller pack sizes, and high-quality printing to support premium lagers and seasonal offerings.

Across the region, government-led localization policies and investments in manufacturing infrastructure favor domestic production of glass and aluminum packaging. This creates strong opportunities for suppliers that establish regional plants, shorten supply chains, and align with national sustainability and recycling initiatives, thereby reinforcing Asia-Pacific’s leadership and growth trajectory in beer packaging.

Competitive Landscape

The global beer packaging market demonstrates moderate concentration. Large global players dominate aluminum and glass production, while downstream finishing, printing, and conversion remain fragmented with numerous regional suppliers. Competitive positioning is defined by scale efficiency, sustainability performance, and service capability. Customization, rapid turnaround, and low minimum order volumes increasingly differentiate suppliers serving craft and premium brewers.

Leading companies emphasize capacity localization, sustainability investment, product differentiation, and flexible service models. Cost leadership in high-volume segments is balanced with innovation-led growth in premium and craft packaging niches.

Key Industry Developments

- In February 2025, Vidrala launched the BD VIVA LITE 75 CL lightweight glass bottle, weighing only 300 grams, designed to reduce CO2 emissions, raw material use, and transport costs while maintaining strength and premium appeal.

Companies Covered in Beer Packaging Market

- Ball Corporation

- Crown Holdings

- Ardagh Group

- Owens-Illinois

- Verallia

- Amcor

- Berlin Packaging

- Smurfit Kappa

- WestRock

- CCL Industries

- Berry Global

- Nampak

- Orora

- Plastipak Holdings

- Can-Pack

- Rexam

- KHS GmbH

- Toyoda Gosei

Frequently Asked Questions

The global beer packaging market size is valued at US$27.5 billion in 2026.

By 2033, the beer packaging market is expected to reach US$35.9 billion.

Key trends include accelerated conversion from glass bottles to aluminum cans, rising premium and craft beer packaging innovation, increasing use of lightweight and recycled materials, and strong capacity investments in Asia Pacific to support localized production and sustainability mandates.

Glass is the leading material segment, accounting for approximately 48.7% of market share by value, while bottles dominate packaging type with over 50.4% share, driven by premium, imported, and heritage beer brands.

The beer packaging market is projected to grow at a CAGR of 3.9% between 2026 and 2033.

Major players include Ball Corporation, Crown Holdings, Ardagh Group, Owens-Illinois, and Verallia.