- Automotive Components & Materials

- Automotive Structural Steel Market

Automotive Structural Steel Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Structural Steel Market by Product Type (Galvanized Steel, Stainless Steel, High-Strength Steel, Mild Carbon Steel, Ultra-High-Strength Steel), Manufacturing Process (Hot Rolling, Cold Rolling), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs), Two-Wheelers), and Regional Analysis for 2026-2033

Automotive Structural Steel Market Share and Trends Analysis

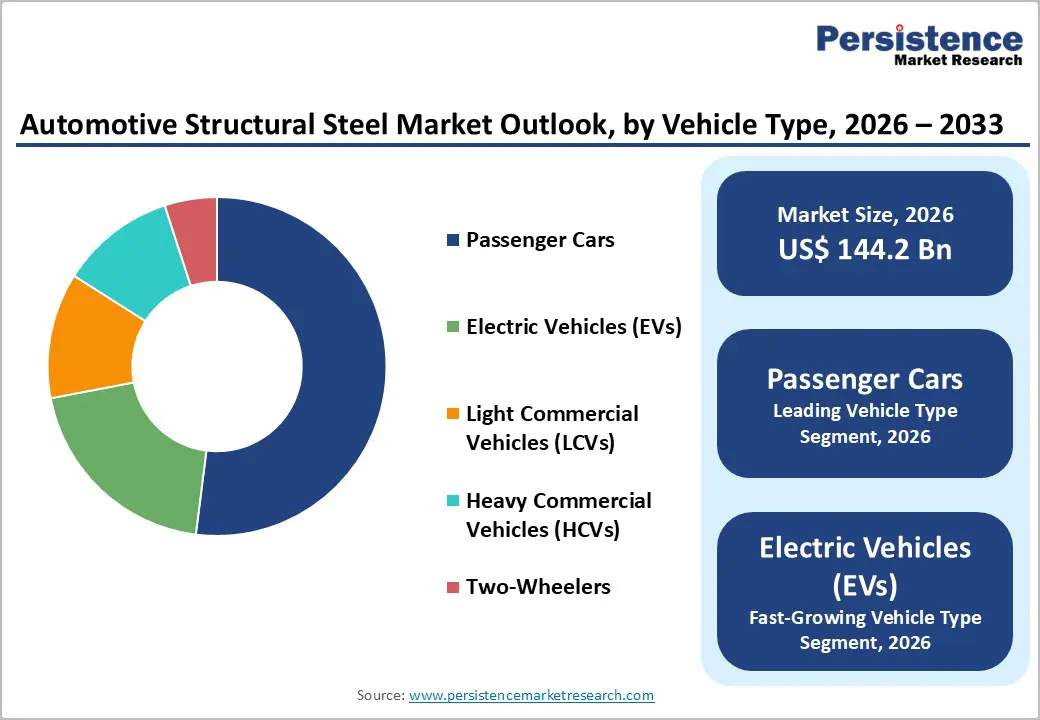

The global automotive structural steel market size is likely to be valued at US$ 144.2 billion in 2026, and is projected to reach US$ 211.2 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026−2033.

Sustained expansion reflects rising vehicle production, electrification transition, safety engineering requirements, and materials engineering innovation. Structural steel adoption increases because automakers require materials that balance weight reduction, crash performance, and manufacturing scalability. Demographic urbanization accelerates vehicle ownership, which increases demand for cost-efficient structural materials.

Industrial automation enables advanced rolling and alloy processing, improving consistency and enabling complex vehicle architectures. Integration of digital engineering tools strengthens predictive crash simulation and structural validation, increasing reliance on engineered steel grades. Expansion of transportation infrastructure and manufacturing ecosystems across emerging economies improves supply chain accessibility, reducing lead times for automotive original equipment manufacturer (OEM) procurement.

Key Industry Highlights

- Leading Vehicle Type: Passenger cars are expected to hold 52% revenue share in 2026 due to high production and steel durability.

- Fastest-growing Vehicle Type: Electric vehicles (EVs) are forecasted to grow the fastest between 2026 and 2033, fueled by policy support and high-strength steel demand.

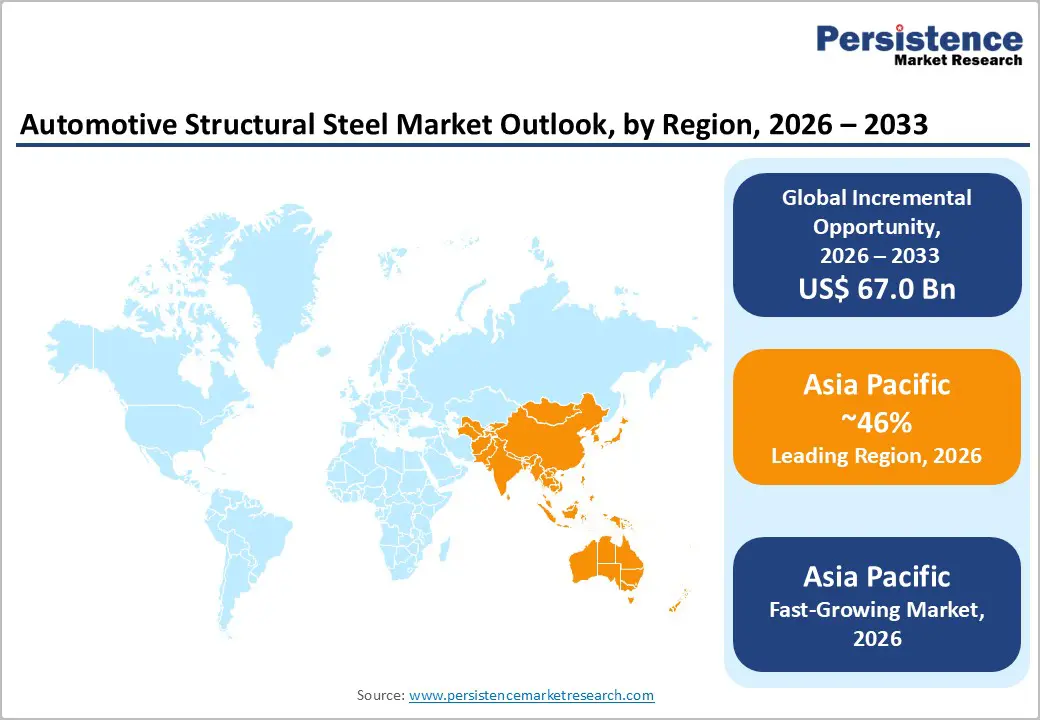

- Dominant Region: Asia Pacific is projected to dominate with 46% market share in 2026, owing to massive vehicle production and surging demand for lightweight steel.

- Fastest-growing Regional Market: The Asia Pacific market is slated to register the highest 2026-2033 CAGR, driven by rapid electrification adoption and escalating deployment of EVs.

| Key Insights | Details |

|---|---|

| Automotive Structural Steel Market Size (2026E) | US$ 144.2 Bn |

| Market Value Forecast (2033F) | US$ 211.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Vehicle Safety Engineering Requirements Intensification

Stringent safety engineering requirements are a primary driver in the automotive sector due to regulatory commitments by government safety authorities aimed at reducing road fatalities and serious injuries. The U.S. National Highway Traffic Safety Administration (NHTSA) selects around 87% of the new 2025 vehicle fleet for its five-star safety rating crash tests under the New Car Assessment Program, reflecting regulatory emphasis on structural crashworthiness and occupant protection in real-world scenarios. Such government-mandated crash evaluations compel vehicle producers to reinforce load-bearing structures, optimize energy-absorbing zones and integrate high-performance materials that enhance collision survivability. Compliance with these rigorous assessments is critical for market access and consumer acceptance, influencing engineering priorities in design, material selection and manufacturing.

Regulatory frameworks such as mandatory vehicle ratings and updated crash testing protocols drive investment in stronger, ductile and high-strength materials, shaping structural design decisions at early stages of product development. National programs such as India’s Bharat New Car Assessment Programme (Bharat NCAP) will make safety ratings compulsory starting in 2025, requiring robust structural performance in frontal and side impacts. Compliance demands translate into heavier use of advanced steels engineered to absorb impact energy without excessive deformation while maintaining weight and cost targets. Car manufacturers integrate enhanced structural design practices to achieve specified star ratings and meet required crash performance metrics across multiple test configurations.

Electrification Transition and Platform Redesign

The accelerating shift toward electrified powertrains and updated vehicle architectures is reshaping material demand due to structural design implications associated with new power sources and packaging requirements. Battery electric vehicles (BEVs) and plug-in hybrid electric vehicles require repositioning of heavy components such as electric motors and large battery packs within the structure, which alters load paths and crash energy management criteria, increasing demand for tailored high-performance steels that deliver strength and stiffness without excessive weight.

Simultaneous platform redesign initiatives adopted by manufacturers to unify electric and conventional models into scalable architectures are driving optimization of structural content. Shared modular platforms enable flexible deployment of different variants, but demand integrated crash structures, battery mounting systems, and improved torsional rigidity packages that rely on engineered steel grades with predictable performance properties. National energy and transport agencies report an expanding availability of light-medium, and heavy-duty all-electric vehicles from a range of automakers, indicating substantial penetration of electrified architectures into mainstream fleets.

Material Substitution Pressure from Multi-Material Design Strategies

Pressure from multi-material design strategies reflects shifting engineering priorities where vehicle manufacturers increasingly integrate disparate materials such as aluminum, magnesium and polymer composites to reduce vehicle weight and enhance efficiency, altering traditional steel-centric architectures. Government and regulatory agencies highlight the energy and emissions benefits of lightweight materials. The U.S. Department of Energy (DOE) states that replacing conventional metal components with lightweight alternatives can reduce overall vehicle mass by up to 50%, improving fuel economy by 6–8% per 10% weight reduction. This trend implies that conventional structural steel must compete with materials offering superior strength-to-weight ratios and recyclability, thereby altering design optimization toward hybrid material systems.

Engineering integration of diverse substrates drives complexity in vehicle assembly, requiring specialized joining technologies, disparate supply chains and new certification processes that challenge legacy steel manufacturing paradigms. Government emphasis on lightweight materials in policy and research programs signals long-term regulatory trajectories favoring weight reduction to meet sustainability mandates, creating competitive environments in which advanced alloys and composites are prioritized alongside, or instead of, traditional steel forms.

Raw Material Price Volatility and Procurement Complexity

Volatility in input costs stems from frequent shifts in prices for key steelmaking materials such as iron ore and coking coal, which are influenced by global supply-demand imbalances, trade policies and logistics constraints that make cost forecasting difficult and weaken procurement planning. Government data indicate that in the 2025-26 fiscal year, India recorded periods of net steel imports due to lower international prices and persistent reliance on imported coking coal, exposing domestic manufacturers to external price swings and supply insecurity while local contracts remain rigid. Such fluctuations force producers to renegotiate supplier contracts regularly, create budgeting uncertainty and weaken bargaining leverage with suppliers, increasing operational risk and pricing risk exposure for manufacturing planning teams.

Procurement complexity intensifies when raw material sourcing spans multiple regions and involves long lead times, particularly for materials without a stable domestic supply, resulting in fragmented vendor networks and extended delivery cycles that burden supply chain coordination. Government reports identify raw material security concerns in the steel sector, noting critical dependence on imported coking coal, which exposes downstream manufacturers to unpredictable maritime freight costs, tariff shifts and geopolitical tensions that affect availability and pricing. When integrated manufacturing operations must align raw material inflows with production schedules, delivery time unpredictability and cost escalations can disrupt production throughput and compress profit margins.

Advanced Metallurgical Innovation and Digital Manufacturing Integration

Advanced metallurgical innovation, paired with deep integration of digital manufacturing tools, unlocks substantial gains in material performance and production efficiency. Innovations in metallurgical science enable development of tailored steel grades with superior strength-to-weight ratios and enhanced crash resistance, reducing material usage while maintaining safety standards. Digital manufacturing platforms, including real-time data analytics and advanced process control, accelerate adjustments during rolling and alloying processes, tightening tolerances and reducing defect rates. Public sector planning for advanced manufacturing underscores this shift as a strategic thrust for future-oriented industries, with a national plan targeting nearly doubling annual business investment in advanced manufacturing sectors such as automotive and advanced materials to maintain competitive leadership in innovation-intensive fields.

Digital manufacturing increases operational visibility, enabling predictive maintenance and process optimization that drive cost containment and quality gains. Automation and networked sensors transform production workflows, reducing downtime and variability while enabling digital simulation of manufacturing systems, thereby shortening design cycles and improving yield. According to government data, India’s domestic steel demand was projected to rise by 8–9% year-on-year in 2025, reflecting the broader industrial role of steel in national development and underscoring the importance of innovation and digitalization in supporting expanding demand

Emerging Manufacturing Hubs and Automotive Industrialization

Rapid growth of manufacturing infrastructure in markets such as India, China and Mexico is driving broader industrial participation through policy incentives, foreign direct investment and export-oriented production zones. In India, vehicle production surged from around 2 million units in the early 1990s to 28 million units in 2023-24, reflecting accelerated capacity additions supported by national manufacturing schemes and export growth targets set by government policy documents. Concentrated manufacturing corridors improve logistics linkages between suppliers, assemblers and OEMs, reducing sourcing costs for structural materials and supporting just-in-time delivery frameworks.

Governments in emerging economies are prioritizing automotive industrialization to secure employment, strengthen supply chains and enhance export competitiveness. Strategic trade agreements, lower labor costs and targeted incentives attract multinational automakers to establish assembly and component plants, creating clustered ecosystems of production and ancillary services. The resulting scale of vehicle output creates predictable demand for high-performance materials, enabling suppliers to invest in upstream processing, quality certification and technology upgrades. Enhanced production volumes also enable amortization of capital outlays on advanced rolling mills, welding and forming technologies, improving yield and consistency of structural grades.

Category-wise Analysis

Product Type Insights

High strength steel is poised to lead with a forecasted 34% of the automotive structural steel market revenue share in 2026, owing to widespread engineering adoption across chassis, pillars, and reinforcement beams. Automakers prioritize materials that deliver structural rigidity while enabling weight optimization, which supports fuel efficiency and electric range objectives. High strength steel offers compatibility with existing stamping and welding infrastructure, allowing manufacturers to upgrade material performance without major capital reconfiguration. Engineering teams value predictable forming behavior and reliable crash energy absorption, which increases specification preference. Supply availability across multiple global producers strengthens procurement flexibility. Design validation processes confirm durability performance across diverse climatic and load conditions, reinforcing industry confidence. Continuous alloy innovation improves ductility and corrosion resistance, extending application scope across multiple vehicle classes.

Ultra-high-strength steel is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by advanced vehicle safety engineering and electrification platform requirements. Ultra-high-strength grades enable thinner structural components while maintaining load-bearing capacity, supporting lightweight design strategies. Engineering validation demonstrates superior performance in impact energy distribution, which enhances occupant protection outcomes. Providers increasingly recommend these materials for critical reinforcement zones because of their high tensile strength and fatigue resistance. Innovation in hot stamping technology improves manufacturability, enabling complex geometries that support aerodynamic vehicle designs. Accessibility expands as steel producers scale production and standardize alloy compositions. Automotive manufacturers integrate these materials into next-generation platforms to meet performance benchmarks.

Vehicle Type Insights

Passenger cars are expected to hold a dominant position, accounting for an estimated 52% of the automotive structural steel market share in 2026, driven by high global production volumes and ongoing model refresh cycles. The clinical credibility analog in automotive engineering reflects strong validation data supporting the safety performance of steel structures. Automotive providers frequently recommend steel-intensive platforms for reliability and repairability. Digitalization in vehicle design accelerates the development of new passenger car models, which increases material consumption. Accessibility of passenger vehicles across multiple price categories sustains steady manufacturing output. Cost efficiency of structural steel supports affordability targets for mass-market vehicles. Technology-enabled service delivery through predictive maintenance systems further reinforces preference for durable structural materials.

The electric vehicles segment is forecast to be the fastest-growing among vehicle types between 2026 and 2033, driven by electrification policy support, battery platform expansion, and charging infrastructure development. Clinical credibility, equivalent in engineering, stems from validated crash simulations demonstrating the effectiveness of structural steel in battery protection systems. Provider referrals analog correspond to engineering consultancy recommendations favoring high-strength steel for underbody shielding. Digitalization accelerates electric vehicle design cycles, increasing material demand for structural prototypes and production units. Accessibility improves as charging networks expand, and manufacturing costs decline. Cost efficiency remains important because steel offers scalable production economics compared with alternative lightweight materials.

Regional Insights

North America Automotive Structural Steel Market Trends

North America exhibits steady demand, anchored by the United States and Canada and characterized by high penetration of advanced automotive technologies and a strong focus on safety and emissions compliance. Structural steel demand is concentrated in light-duty and commercial vehicle segments, where manufacturers prioritize high-strength and ultra-high-strength grades to optimize crash performance and reduce overall vehicle weight. Large-scale production facilities in the United States, Canada, and Mexico support integration of tier-1 and tier-2 suppliers, creating efficient supply chains that facilitate just-in-time delivery of structural components. Government regulations on vehicle safety standards and fuel efficiency contribute to the adoption of engineered steel grades, while domestic production capabilities enable rapid scaling of advanced forming and welding processes.

Rising production of electric passenger and commercial vehicles is driving greater use of specialized steel grades for battery enclosures, chassis reinforcement, and load-bearing structures. Investment in research and development for alloy optimization and forming technologies enhances material performance and reduces production costs for high-volume assembly lines. Strategic manufacturing corridors, particularly in the United States and Mexico, provide streamlined access to raw materials and advanced fabrication facilities, lowering lead times and enabling rapid prototyping of new vehicle platforms. Collaboration between manufacturers and steel producers focuses on the adoption of high-strength steel for safety-critical components, supporting design flexibility and improved crash performance while maintaining cost efficiency.

Europe Automotive Structural Steel Market Trends

Europe maintains a technologically advanced automotive manufacturing base characterized by high engineering standards and stringent regulatory frameworks. Established OEMs in Germany, France, Italy, and Spain operate extensive supplier networks, integrating local and imported raw materials to support consistent throughput for passenger cars and light commercial vehicles. Emphasis on precision forming, welding, and coating processes ensures structural reliability while complying with evolving safety and emissions standards. Government programs promoting low-emission and lightweight vehicle technologies stimulate demand for high-performance steel that balances weight reduction with mechanical integrity. Continuous innovation in steel grades, including advanced high-strength and ultra-high-strength variants, addresses evolving safety requirements and enhances structural efficiency across multiple vehicle platforms.

Europe experiences growth driven by electrification and hybrid mobility expansion, increasing structural steel requirements for battery enclosures and crash-critical frameworks. Collaborative initiatives between vehicle manufacturers and material suppliers in Germany, France, Italy, and the United Kingdom accelerate the development of next-generation steels with improved tensile strength, formability, and corrosion resistance. Advanced production facilities deploy automated rolling, laser welding, and digital simulation tools to optimize material utilization and assembly efficiency. Large-scale vehicle platforms for commercial and passenger segments create predictable demand patterns, encouraging investment in upstream steel processing technologies.

Asia Pacific Automotive Structural Steel Market Trends

Asia Pacific is expected to dominate with an estimated 46% share in 2026, reflecting concentrated vehicle production scale in China, India, Japan, and South Korea, extensive integrated supply chains, and large-scale chassis assembly operations supported by regional manufacturing policies and investment incentives. High output from these major vehicle assembly nations, coupled with cost-competitive steel fabrication capabilities and proximity to tier-1 and tier-2 suppliers, reduces logistics complexity for structural material sourcing and supports efficient assembly line throughput. Driving this scale is robust annual vehicle production in key hubs that together account for the majority of global motor vehicle output, creating consistent demand for structural materials engineered for high strength and lightweight performance in safety-critical components.

Asia Pacific is expected to register the fastest growth between 2026 and 2033, driven by expanding passenger and commercial vehicle production in China, India, Japan, and Thailand, rising adoption of electrified mobility, and policy initiatives aimed at boosting local manufacturing competitiveness. Government-led programs that support automotive and related component production enhance domestic value chains and attract foreign direct investment into advanced fabrication facilities. Strong regional emphasis on newer vehicle platforms accelerates deployment of high-strength and specialty steel grades that meet stringent safety and efficiency standards, increasing structural material penetration across emerging vehicle segments.

Competitive Landscape

The global automotive structural steel market structure demonstrates moderate consolidation, with major multinational steel producers capturing significant revenue through extensive production and distribution networks. Key players such as NIPPON STEEL CORPORATION, POSCO INTERNATIONAL, Tata Steel, JFE Steel Corporation, and United States Steel Corporation operate integrated value chains that encompass raw material sourcing, refining, alloy development, and downstream distribution. These integrated operations enable consistent quality control, cost efficiencies, and scalability across diverse vehicle applications. Investment in research and development supports high-strength, ultra-high-strength, and advanced steel grades that meet evolving automotive safety and lightweighting requirements. Advanced processing technologies, including hot and cold rolling, laser welding, and forming, reinforce the capability of these companies to supply engineered materials for both passenger and commercial vehicles.

Regional and mid-sized producers complement the competitive landscape by targeting specialized steel grades or serving localized markets with faster lead times and tailored services. While multinational companies dominate high-volume contracts, smaller players provide flexibility and niche expertise, supporting a more balanced competitive environment. Revenue concentration among leading companies reflects technology leadership, brand reliability, and established customer relationships, while regional diversity ensures competitive pricing and accessibility across key automotive hubs.

Key Industry Developments

- In February 2026, thyssenkrupp Steel announced that it will start supplying CO-reduced bluemint® recycled steel to BMW Group for the series production of the BMW iX3, covering outer body panels, interior components, and battery housing, while maintaining conventional steel performance without process changes.

- In December 2025, Chery and HBIS Group unveiled a 2400-MPa hot-formed steel that surpasses the previous 2200-MPa industry record held by Xiaomi’s YU7, marking a breakthrough in ultra-high-strength automotive materials suited for critical structural components.

- In June 2025, SSAB and Polmotors announced a strategic collaboration to supply fossil-free steel for structural automotive components and assemblies, advancing the use of decarbonized materials in automotive manufacturing.

Companies Covered in Automotive Structural Steel Market

- NIPPON STEEL CORPORATION.

- POSCO INTERNATIONA

- Tata Steel

- JFE Steel Corporation.

- United States Steel Corporation.

- Hyundai Steel.

- Nucor Corporation

- JSW Steel

- voestalpine Stahl GmbH

Frequently Asked Questions

The automotive structural steel market is projected to reach US$ 144.2 billion in 2026.

Rising vehicle production, electrification adoption, safety regulations, and demand for lightweight, high-strength materials drive the automotive structural steel market.

The automotive structural steel market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Expansion of electric vehicle production, lightweight vehicle design, emerging manufacturing hubs, advanced steel technologies, and integrated digital engineering create key market opportunities.

Some of the key market players include NIPPON STEEL CORPORATION, POSCO INTERNATIONAL, Tata Steel, JFE Steel Corporation, and United States Steel Corporation.