- Automotive

- Automotive Performance Accessories Market

Automotive Performance Accessories Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Performance Accessories Market by Product Type (Exhaust System, Suspension Parts, Brake Parts, Transmission Parts), Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), Sales Channel (First Fit, Aftermarket), and Regional Analysis for 2026-2033

Automotive Performance Accessories Market Share and Trends Analysis

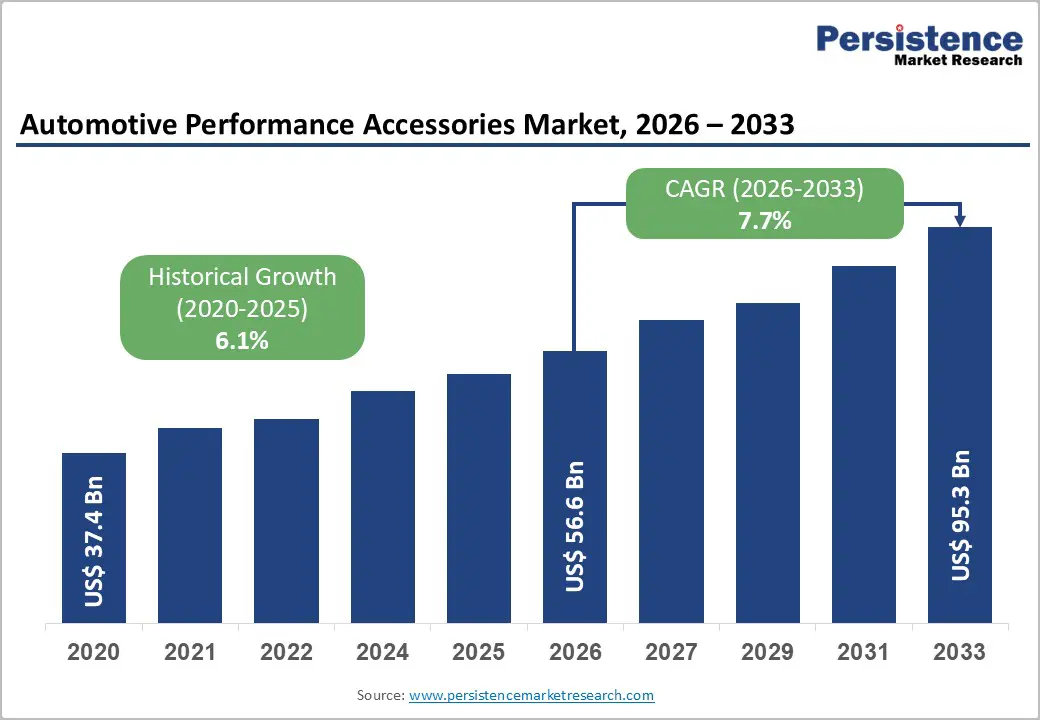

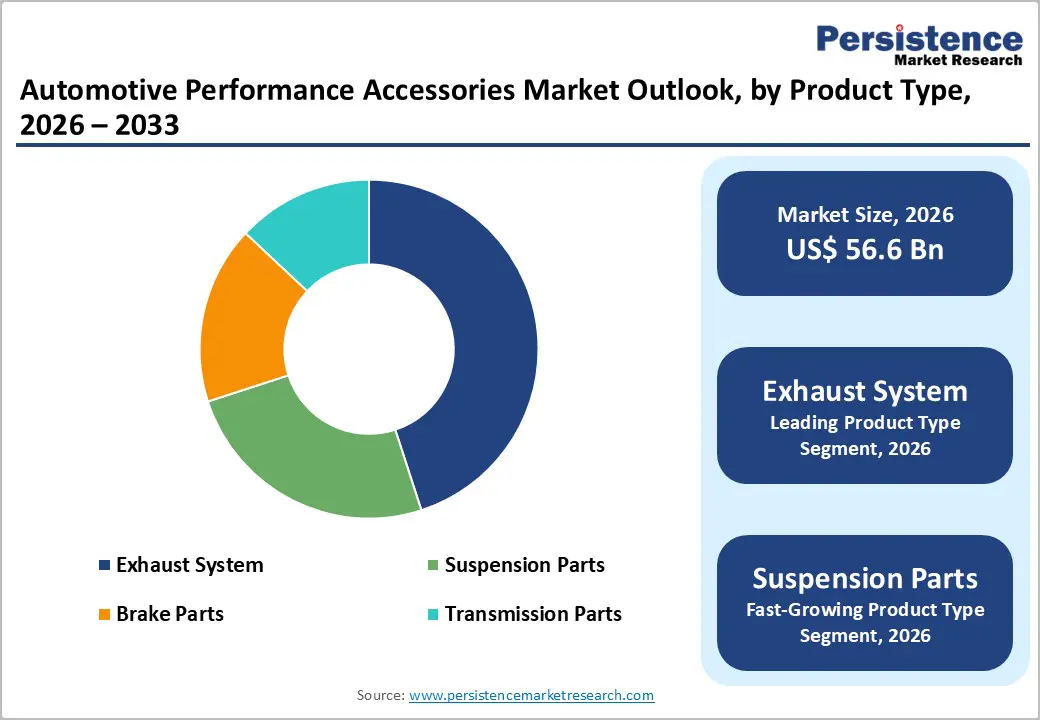

The global automotive performance accessories market size is likely to be valued at US$ 56.6 billion in 2026, and is projected to reach US$ 95.3 billion by 2033, growing at a CAGR of 7.7% during the forecast period 2026−2033. The expansion of this market is underpinned by rising vehicle-enthusiast culture, an expanding motorsports ecosystem, and consumer appetite for personalized driving experiences. Growing disposable incomes across Asia Pacific and North America are channeling discretionary spending toward aftermarket enhancements such as exhaust systems, suspension upgrades, turbochargers, brake kits, and air intake systems. The proliferation of e-commerce platforms has simultaneously widened product accessibility while intensifying price competition, expanding the addressable consumer base beyond traditional specialist retailers.

Key Industry Highlights

- Leading Product Type: Exhaust system is set to command approximately 38% of the revenue share, driven by its role in improving a vehicle's performance.

- Fastest-growing Product Type: Suspension parts are likely to be the fastest-growing through 2033, fueled by their enhanced handling, stability, and ride comfort.

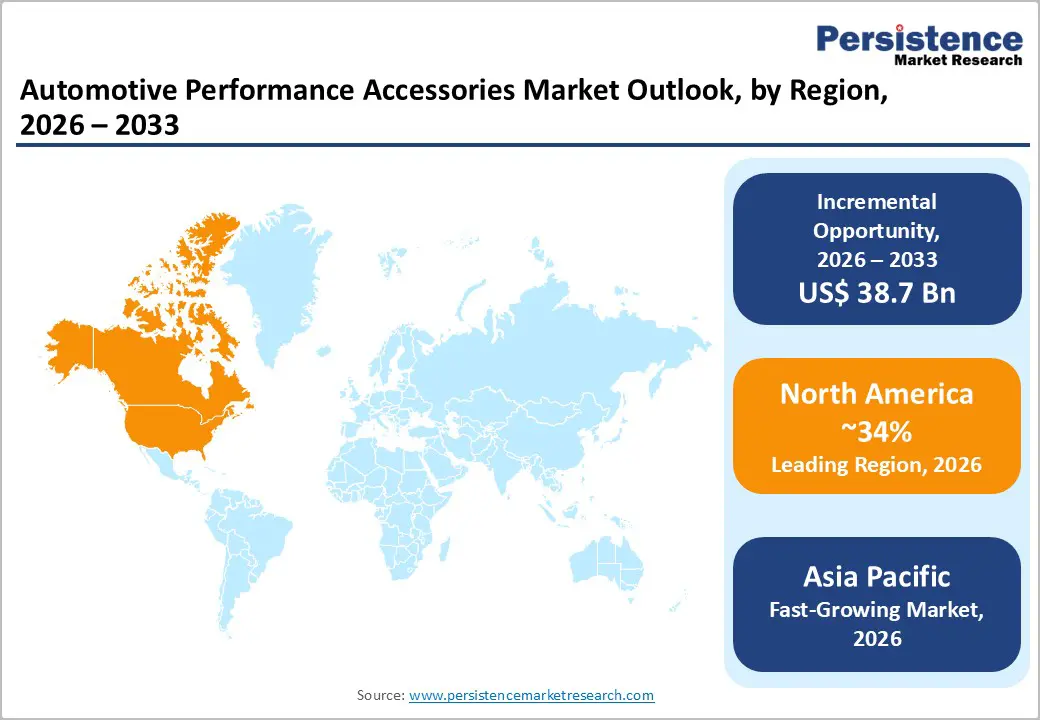

- Dominant Region: North America is expected to hold around 34% market share in 2026, supported by a strong consumer familiarity with health-focused foods and ingredients

- Fastest-growing Market: The Asia Pacific market is the fastest-growing during the forecast period, fueled by a rapidly growing automotive industry and a large consumer base.

- Leading Vehicle Type: Passenger vehicles are slated to capture approximately 62% revenue share in 2026, owing to their vast global numbers and rising personalization trends among owners.

- Fastest-growing Vehicle Type: Light commercial vehicles (LCVs) are expected to be the fastest-growing between 2026 and 2033, as they are commonly equipped with performance parts to enhance their efficiency and carrying capacity.

| Key Insights | Details |

|---|---|

| Automotive Performance Accessories Market Size (2026E) | US$ 56.6 Bn |

| Market Value Forecast (2033F) | US$ 95.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Surging Automotive Enthusiast Culture and Motorsports Popularity

The global motorsports ecosystem is acting as a demand accelerator for performance accessories. The Fédération Internationale de l'Automobile (FIA) is reporting higher participation across organized racing formats, while Formula 1 is sustaining large-scale audience engagement. Consumers are translating this exposure into vehicle upgrades that reflect track-grade engineering. They are installing aerodynamic kits, engine tuning systems, and braking enhancements that mirror professional configurations. Events such as the Dakar Rally and the Baja 1000 are reinforcing demand for off-road durability, prompting adoption of lifted suspensions, reinforced exhaust systems, and terrain-optimized components. This behavioral shift is strengthening preference for performance-led customization and is expanding the addressable aftermarket.

The Specialty Equipment Market Association (SEMA) and its Hot Rod Industry Alliance (HRIA) indicate that the United States automotive specialty equipment aftermarket has reached over US$ 51.8 billion, supported by consistent consumer spending despite macroeconomic pressure. Buyers are prioritizing upgrades that improve handling, power delivery, and aesthetics, with clear alignment to motorsport benchmarks. Manufacturers are responding by engineering crossover products such as lightweight alloy wheels and adaptive air intake systems that integrate race-derived performance into daily driving. Automakers are also forming partnerships with racing platforms to validate and demonstrate these innovations in live environments. This convergence is positioning motorsports as a structural growth driver, and companies will have expanded product portfolios to capture sustained global demand.

Technological Advancement in Lightweight Materials and Engine Management

Advances in material science are reducing cost and mass across performance accessories. Carbon fiber composites, aluminum alloys, and engineered polymers are delivering high strength with lower weight, which is expanding adoption beyond premium segments. Manufacturers are optimizing fabrication processes and integrating recycled inputs to improve cost efficiency and sustainability. As a result, consumers are accessing upgrades such as aerodynamic body kits and reinforced chassis systems with greater confidence in durability and performance. This shift is widening the aftermarket base and is supporting volume-led growth.

Electronic engine control unit (ECU) tuning is moving into the mainstream through simplified, plug and play solutions. User-friendly modules are enabling drivers to recalibrate fuel delivery and ignition timing for improved throttle response without specialized expertise. In parallel, the turbocharger ecosystem is expanding as forced induction becomes standard in production vehicles. Aftermarket offerings such as intercoolers, boost controllers, and performance exhaust components are targeting these platforms to enhance power and thermal management. Companies are integrating software calibration with hardware kits to reduce installation complexity, while automakers are standardizing turbo architectures, which will have unlocked scalable upgrade pathways.

Stringent Emission Regulations Curtailing ICE-Centric Performance Modifications

Tightening emission norms are constraining the performance accessories market across key regions. Frameworks such as Euro 7 in the European Union (EU), Environmental Protection Agency (EPA) standards in the U.S., and China 6b in China are restricting the use of non-compliant components. Authorities are limiting installations of catalytic converter delete kits, high-flow exhaust systems, and uncertified tuning software to reduce emissions. Vehicles are failing mandatory inspections when modifications breach thresholds, which is discouraging adoption. Manufacturers are redesigning products to align with compliance requirements, yet buyers are avoiding upgrades that risk penalties or warranty loss. Enhanced monitoring through digital tracking is further increasing enforcement and limiting unauthorized modifications.

Regulatory pressure is affecting turbocharger and fuel system upgrades in internal combustion engine (ICE) vehicles, particularly older models. Inspection protocols are identifying emission deviations during routine testing, which is reducing demand for aggressive performance enhancements. Consumers are prioritizing compliance and reliability over marginal power gains. Suppliers are developing solutions that align with hybrid standards to balance output with regulatory adherence. Automakers are working with regulators to certify select aftermarket components, which is improving acceptance in structured markets. Industry associations are advocating for adaptive policies that enable innovation while maintaining environmental safeguards.

High Product Cost and Complex Installation Requirements

Premium performance accessories are carrying higher price points than original equipment manufacturer (OEM) components, which is limiting adoption among cost-sensitive buyers. Products such as suspension coilover kits and big brake systems require significant upfront spending, with installation and calibration adding to total ownership cost. Modern vehicle electronics are demanding specialized diagnostic tools, which is increasing service complexity and expense. Consumers are evaluating total value more critically and are prioritizing essential upgrades over discretionary enhancements. Retail financing is improving access, while manufacturers are testing cost-efficient materials and production methods, yet pricing remains elevated due to advanced engineering and performance gains.

Do-it-yourself (DIY) installation is becoming less viable as vehicle systems grow more integrated. Sensor-driven architectures and software dependencies are requiring precise configuration, which is reducing confidence among non-professional users. Buyers are delaying decisions to avoid technical risk, which is shifting demand toward certified workshops. Service providers are ensuring reliability but are raising the total cost of ownership. Suppliers are addressing this gap through pre-calibrated kits and guided installation content to restore accessibility. Automakers are publishing compatibility frameworks, and industry bodies are supporting skill development initiatives. The market is, thus, poised to evolve toward hybrid service models that combine professional support with simplified user interfaces.

OEM Collaboration and Performance Sub-Brand Development

Collaborative product development between aftermarket specialists and OEMs is emerging as a core growth strategy. Automakers are integrating performance upgrades within warranty-backed offerings to capture value that would otherwise shift to independent channels. Programs such as Ford Performance, Mopar, and General Motors Accessories are embedding approved components into dealer networks and financing ecosystems. Customers are selecting these options due to assured compatibility, lower perceived risk, and retained warranty coverage. This approach is strengthening brand retention as vehicle personalization remains within the OEM service framework.

Partnerships between tier one suppliers and new energy vehicle manufacturers are accelerating this transition toward integrated development. Engagements such as Tenneco working with Rivian Automotive are embedding performance technologies such as advanced suspension and noise control systems at the production stage. This model is shifting suppliers from retrofit providers to early stage collaborators in platform engineering. As a result, companies are accessing first fit revenue streams, which are stabilizing demand cycles and reducing dependence on discretionary aftermarket spending.

EV-Compatible Performance Accessories Portfolio Expansion

The surging adoption of electric vehicles (EVs) worldwide is creating a distinct growth avenue for performance accessories. Owners are prioritizing upgrades such as brake system enhancements and suspension tuning to manage instant torque delivery. Battery electric vehicle (BEV) platforms are also driving demand for aerodynamic body kits, wheel and tire packages, and battery thermal management solutions. Manufacturers are engineering these components to improve range, handling, and safety without compromising system integrity. This shift is positioning EV customization as a core segment, as performance-oriented users seek platform-specific enhancements.

Companies that focus on EV-compatible accessories are securing early mover advantage through certification and integration capabilities. Products are aligning with battery management systems and regenerative braking architectures to ensure seamless operation. OEMs are partnering with suppliers to factory-fit performance options, which is improving reliability and customer confidence. Suppliers are advancing lightweight materials to reduce energy consumption while enhancing grip and design appeal. Retailers are promoting these offerings to attract technology-focused buyers, while industry bodies are establishing standards to support safe and compliant modifications.

Category-wise Analysis

Product Type Insights

Exhaust systems are expected to lead among product types with an estimated 38% of the automotive performance accessories market revenue share in 2026. Vehicle owners are upgrading these systems to improve exhaust flow and reduce backpressure, which is enhancing engine output, throttle response, and acoustic quality. Core offerings include performance headers, high-flow mufflers, and emission-compliant catalytic converters that balance power with regulatory limits. Demand is rising alongside stricter emission targets and fuel efficiency goals, prompting engineers to adopt lightweight materials and precision tuning. Manufacturers are supplying modular configurations that support both road and track applications, which is broadening customer reach.

Suspension components are predicted to record the highest 2026-2033 CAGR due to their impact on handling, stability, and ride quality. Consumers are installing performance shocks, struts, adjustable springs, and sway bars to improve cornering control and impact absorption. Interest in off-road driving and track usage is driving demand for systems that perform under varied conditions. Engineers are integrating adaptive damping and lightweight alloys to balance daily usability with high-performance requirements. Manufacturers are offering adjustable kits that enable vehicle-specific tuning, which is strengthening customization across driving environments.

Vehicle Type Insights

Passenger vehicles are anticipated to hold the largest share at about 62% of segmental revenue in 2026, on account of high global parc and strong personalization demand. Owners are adopting upgrades such as engine tuning kits, exhaust systems, and suspension components to improve acceleration, handling, and visual appeal in daily use. Manufacturers are aligning products across segments from compact cars to premium models, with integration that supports modern electronic architectures. This segment is maintaining leadership as urban mobility expands and users combine routine commuting with performance-oriented driving.

LCVs are slated to register the fastest growth during the 2026-2033 forecast period, driven by logistics intensity and cost optimization needs. Fleet operators are deploying upgrades such as improved air intake systems, tuned exhaust setups, and reinforced suspension units to enhance payload handling and efficiency. These modifications are supporting better fuel economy, durability, and uptime under demanding conditions. Manufacturers are engineering robust kits that meet commercial duty cycles while improving responsiveness, which is accelerating adoption across urban delivery networks.

Regional Insights

North America Automotive Performance Accessories Market Trends

North America is expected to account for an approximate 34% of the automotive performance accessories market share in 2026, aided by a strong culture of vehicle personalization. Consumers are investing in upgrades such as exhaust systems, suspension kits, wheels, and engine tuning solutions to enhance both aesthetics and driving dynamics. High disposable income is sustaining discretionary spending, while the United States is anchoring regional demand through active participation in motorsports and enthusiast events. This environment is reinforcing consistent interest in performance modifications across the vehicle lifecycle.

The regional market is also benefiting from a mature automotive ecosystem with established manufacturers, suppliers, and tuning networks. Companies are positioning engineering centers and distribution hubs close to key markets and OEMs to accelerate innovation and delivery. This concentration is enabling faster product rollouts, broader availability, and reliable after-sales support. Growth is being supported by rising use of advanced materials, increasing adoption of performance parts in sport utility vehicles (SUVs) and pickup trucks, and expanding digital retail channels that improve access for a wider customer base.

Europe Automotive Performance Accessories Market Trends

Europe occupies a prominent position in the automotive performance accessories market with a focus on balancing power output and efficiency. Germany, the United Kingdom, and Italy are sustaining demand through strong automotive heritage and active motorsport ecosystems. Consumers are adopting upgrades such as precision exhaust systems, adaptive suspension setups, and lightweight wheels to improve handling and performance. Manufacturers are aligning product design with everyday usability while retaining track-oriented characteristics. Industry events and tuning communities are strengthening awareness and are directing buyers toward specialized retailers and digital channels.

Strict emission frameworks are accelerating the shift toward compliant and efficient performance solutions. OEMs and aftermarket suppliers are certifying components that meet regulatory standards and integrate with modern powertrains. Policy support for low-emission technologies is encouraging both private owners and fleet operators to invest in approved upgrades. Suppliers are advancing hybrid-compatible systems and EV-ready components to address evolving requirements. The market is progressing at a steady pace as harmonized regulations are enabling cross-border trade and supporting innovation in electrification and connected vehicle technologies.

Asia Pacific Automotive Performance Accessories Market Trends

Asia Pacific is set to become the fastest-growing market for automotive performance accessories between 2026 and 2033, driven by rapid vehicle production in countries such as China, Japan, and India. Large vehicle fleets are creating a strong base for personalization, while urban and younger buyers are adopting upgrades such as performance air intake systems, body kits, and handling components. Expanding retail ecosystems are combining dealership networks with digital platforms to improve product access across dense urban clusters. This demand pattern is positioning the region as a high-volume, innovation-responsive market.

Rising disposable income and greater awareness of aftermarket solutions are accelerating adoption among middle-income consumers. Buyers are evaluating trends through social media and automotive events, then investing in upgrades aligned with lifestyle and performance expectations. Policy support for electric vehicles and hybrid platforms is opening new opportunities for compatible accessories such as battery thermal management systems and regenerative braking enhancements. Suppliers are aligning products with evolving powertrain architectures, while governments are incentivizing sustainable innovation. By the end of the forecast period, the region is expected to strengthen its position through cost-efficient manufacturing, integrated supply chains, and expanding export capabilities.

Competitive Landscape

The global automotive performance accessories market structure is moderately fragmented, with top players such as Tenneco, Brembo, BorgWarner, Continental, and Akrapovic accounting for an estimated 37% revenue share. Competition is intensifying as established firms and emerging players are introducing differentiated products aligned with evolving consumer demand. Companies are prioritizing research and development (R&D) to deliver components that improve efficiency, system compatibility, and design appeal.

Market participants are deploying strategic initiatives such as partnerships, mergers, and acquisitions to strengthen positioning and expand product portfolios. These approaches are enabling entry into adjacent segments and improving access to new customer bases. At the same time, agile entrants are leveraging innovation cycles to capture niche demand, which is increasing competitive pressure. This structure is sustaining a dynamic market environment where scale advantages and technological differentiation are determining long-term growth outcomes.

Key Industry Developments

- In February 2026, Genuine Parts Company announced plans to split its automotive and industrial divisions into two independent public entities by 2027 to sharpen focus and accelerate growth. The move will strengthen its automotive aftermarket platform, enabling faster investment, improved supply chain efficiency, and expanded distribution of performance and replacement components across global markets.

- In August 2025, researchers at Oak Ridge National Laboratory (ORNL) developed the DuAlumin-3D alloy, which enables crack-free 3D printing of high-temperature automotive components while outperforming conventional aluminum alloys in strength and durability. The material supports lightweight, heat-resistant designs that improve fuel efficiency and expand additive manufacturing.

- In March 2025, Yamaha Motor announced the launch of its new "SPV" (Smart Power Vehicle) performance parts lineup, targeting enhanced customization for motorcycles and scooters with genuine upgrades like exhaust systems, suspension kits, and aerodynamic components. These parts draw from Yamaha's racing expertise to boost power, handling, and style for street and track use, initially available in select Asian markets with global rollout planned.

Companies Covered in Automotive Performance Accessories Market

- Tenneco Inc.

- Brembo S.p.A.

- BorgWarner Inc.

- Continental AG

- Akrapovic d.o.o.

- Holley Performance Products

- KW Automotive GmbH

- HKS Co., Ltd.

- MagnaFlow Performance Exhaust

- Borla Performance Industries

- Eibach Group

- AEM Electronics

- Injen Technology

- Cusco Co., Ltd.

- Tomei Powered Inc.

Frequently Asked Questions

The global automotive performance accessories market is projected to reach US$ 56.6 billion in 2026.

Increasing vehicle customization demand, growing popularity of motorsport culture, and promising material innovations are driving the market.

The market is poised to witness a CAGR of 7.7% from 2026 to 2033.

Major opportunities lie in electric vehicle-compatible upgrades and expansion in Asia Pacific, fueled by electrification trends.

Tenneco Inc., Brembo S.p.A., BorgWarner Inc., Continental AG, and Akrapovic d.o.o. are some of the key players in the market.