- Automotive Components & Materials

- Automotive PCB Market

Automotive PCB Market Size, Share, and Growth Forecast 2026 - 2033

Automotive PCB Market by Form (Double-Sided PCB, Multi-Layer PCB, Single-Sided PCB), Vehicle Type (Passenger Car, Commercial Vehicle), Level of Autonomy (Autonomous Vehicles, Conventional Vehicles, Semi-Autonomous Vehicles), Application (ADAS and Basic Safety, Body, Comfort, and Vehicle Lighting, Infotainment Components, Powertrain Components), and Regional Analysis for 2026 - 2033

Automotive PCB Market Size and Trend Analysis

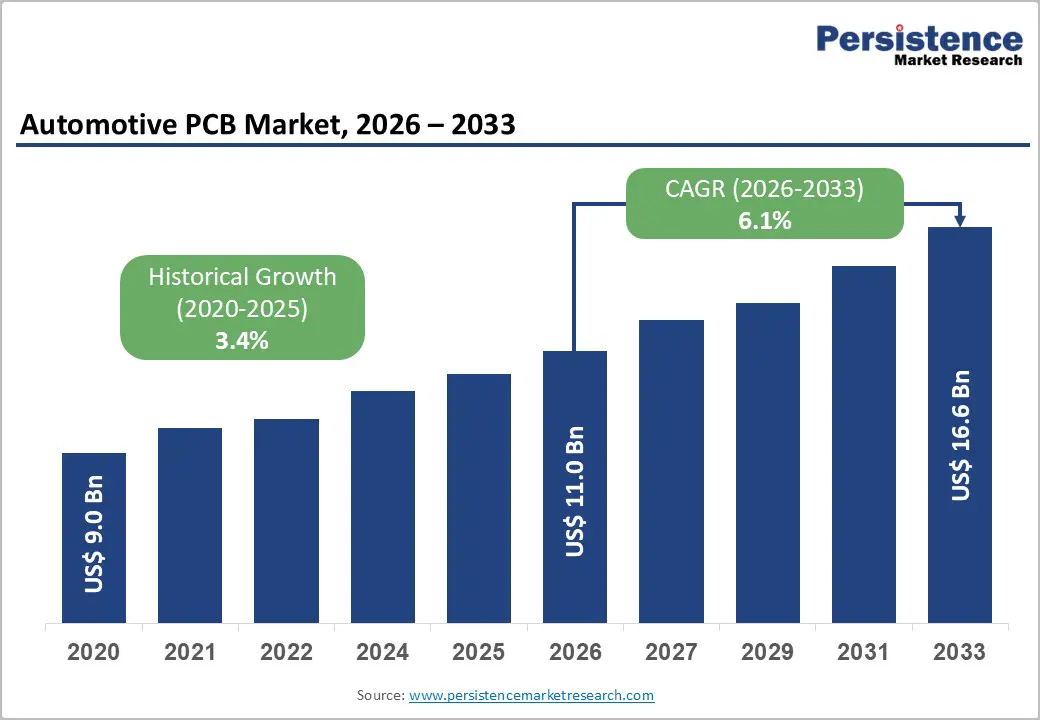

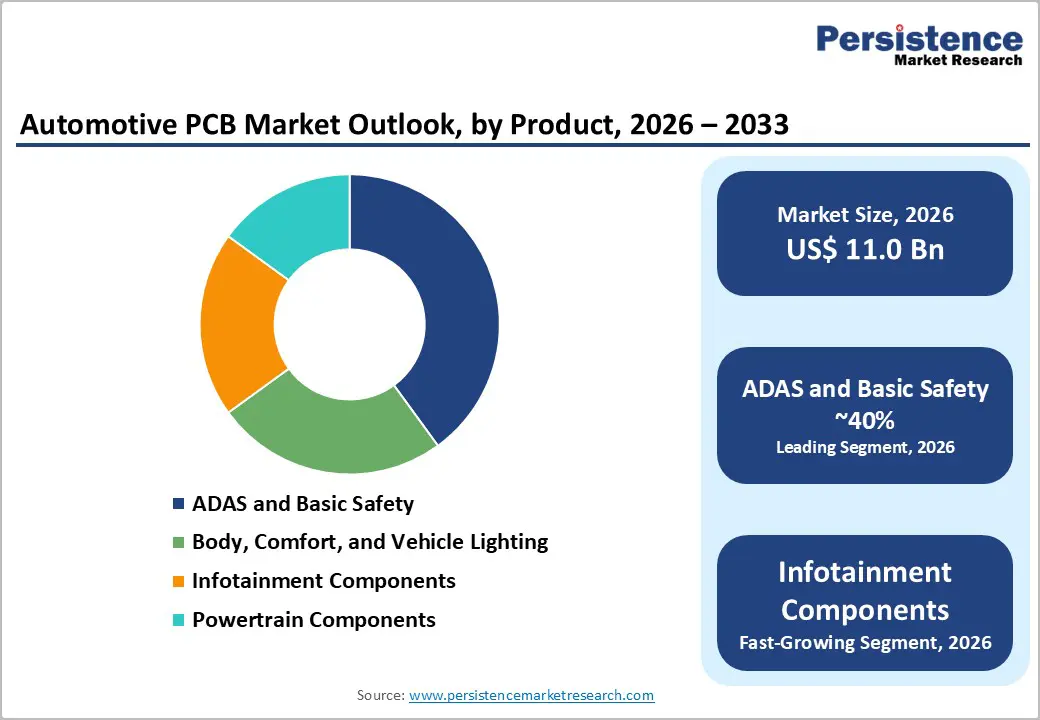

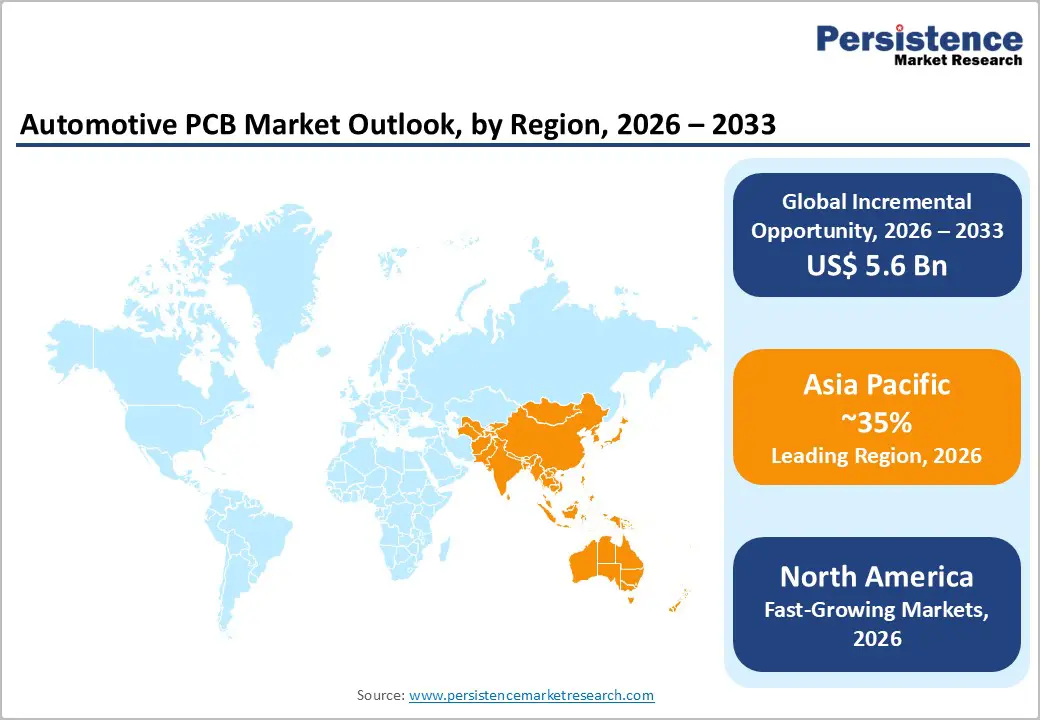

The global automotive PCB market size is supposed to be valued at US$ 11.0 billion in 2026 and is projected to reach US$ 16.6 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

This reflects a steady electronics penetration per vehicle and the transition toward software-defined and electrified vehicles. Increasing adoption of advanced driver assistance systems, connectivity features, and power electronics is boosting PCB content in both mass-market and premium models.

Key Industry Highlights:

- Leading Region: Asia Pacific leads the Automotive PCB Market, supported by large-scale vehicle production, electronics manufacturing strength, and rapid adoption of electric vehicles and advanced safety systems across China, Japan, South Korea, and ASEAN countries.

- Fastest-growing Region: The fastest-growing regional opportunity lies in Asia Pacific and selected emerging markets, where accelerating electrification and ADAS penetration significantly raise PCB content per vehicle and support long-term investment in local manufacturing capacity.

- Leading Segment: Within product forms, Multi-Layer PCB is the dominant segment, accounting for an estimated 45% share, driven by complex ADAS, infotainment, and power electronics applications that require high-density interconnect and advanced materials.

- Fastest-growing Region: By vehicle type, Passenger Car dominates with around 70% share of the Automotive PCB Market, reflecting high production volumes and richer electronics integration, while commercial vehicles present incremental upside in fleet telematics and safety systems.

- Opportunities: Key opportunities emerge from the transition to autonomous and software-defined vehicles, which will require advanced PCBs for centralized computing, sensor fusion, and redundant safety systems, rewarding suppliers with strong innovation and co-design capabilities.

| Global Market Attributes | Key Insights |

|---|---|

| Automotive PCB Market Size (2026E) | US$ 11.0 Bn |

| Market Value Forecast (2033F) | US$ 16.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.4% |

Market Dynamics

Drivers - Electrification of Powertrain and High-Voltage Architectures

Electrified powertrains are fundamentally reshaping the Automotive PCB Market by sharply increasing PCB value per vehicle. Hybrid and battery electric vehicles require high-density boards for battery management systems, inverters, on-board chargers, DC-DC converters, and thermal control units, far beyond the requirements of internal combustion engine platforms. Global sales of battery electric and plug-in hybrid vehicles have reached many millions of units annually, and in leading markets such as China and Europe, electrified vehicles account for well over one-fifth of new registrations, according to official statistics and regulatory reports. This shift compels automakers and Tier-1 suppliers to adopt multi-layer and high-reliability PCBs that can handle higher voltages, currents, and thermal loads. As power electronics content expands per vehicle, PCB manufacturers that can meet automotive-grade quality, traceability, and reliability standards position themselves to capture sustained, technology-driven demand.

Proliferation of ADAS, Safety, and Connected Infotainment

The rapid deployment of advanced driver assistance systems and connected infotainment is another major drive for the Automotive PCB Market. Modern vehicles now integrate multiple radar, camera, ultrasonic, and lidar sensors feeding domain and zonal controllers that require complex, high-layer-count PCBs. Regulatory bodies in North America, Europe, and Asia are pushing for mandatory fitment of features such as automatic emergency braking, lane keeping assistance, and intelligent speed assistance across mass segments, ensuring that electronic control units become standard rather than optional equipment. At the same time, consumers increasingly expect large displays, high-speed connectivity, and over-the-air update capability, which depend on sophisticated infotainment and telematics hardware. This ecosystem demands robust PCBs capable of high-speed signal integrity, electromagnetic compatibility, and miniaturization.

Restraints - Raw Material Price Volatility and Cost Pressure

One key restraint for the Automotive PCB Market stems from volatility in prices of copper, laminates, specialty resins, and other critical materials. PCB producers operate in a highly cost-sensitive automotive supply chain, where original equipment manufacturers and Tier-1 suppliers exert continuous pressure on component pricing and lifecycle cost. Spikes in commodity prices or disruptions in resin and laminate supply can compress margins, especially on long-term contracts with limited price adjustment clauses. Smaller or less vertically integrated PCB manufacturers may find it difficult to absorb such shocks, which can slow capacity expansion and reduce investment in advanced technologies.

Stringent Automotive Quality Requirements and Qualification Timelines

Another restraint arises from the demanding quality, reliability, and qualification standards required in the automotive PCB market. Automotive-grade PCBs must comply with strict specifications on thermal cycling, vibration, humidity, and long-term reliability, often verified through extensive test regimes and audits. Achieving and maintaining certifications such as IATF 16949 and meeting OEM-specific qualification processes can be resource-intensive and time-consuming. These barriers limit the entry of new players, constrain supplier diversification for automakers, and may slow down the introduction of innovative PCB materials or designs when validation capacity is stretched.

Opportunity - Advanced PCBs for Autonomous and Software-Defined Vehicle Architectures

A major opportunity in the automotive PCB market lies in the shift toward higher levels of autonomy and software-defined vehicle architectures. Autonomous and highly automated driving platforms consolidate numerous ECUs into centralized computing units and domain controllers, which depend on high-density interconnect and multi-layer PCBs with complex stack-ups. In the first step, the proliferation of sensor fusion, high-resolution mapping, and redundant safety systems drives requirements for boards that support high-speed data transmission and robust power distribution. In the second step, software-defined architectures enable continuous feature updates, pushing hardware toward scalable, modular platforms built on advanced PCB and packaging technologies. Suppliers that invest in fine-line manufacturing, high-speed materials, and co-design capabilities with semiconductor and module vendors can secure design wins in next-generation autonomous and connected vehicles.

Regional Manufacturing Localization and Supply Chain Diversification

Another important opportunity for the automotive PCB market is the ongoing regional diversification and localization of automotive electronics manufacturing. In recent years, disruptions in global supply chains, trade tensions, and logistics bottlenecks have motivated automakers and Tier-1 suppliers to localize more of their electronics and PCB sourcing in key production regions such as Asia Pacific, Europe, and North America. Initially, this has led to expanded procurement from regional PCB plants and investments in new facilities near major automotive clusters. Over time, it opens avenues for local and regional PCB producers to move up the value chain from simple single-sided and double-sided boards to multi-layer and specialty PCBs used in ADAS, powertrain, and infotainment systems. Governments in several automotive hubs support local electronics manufacturing through incentives, taxation benefits, and technology programs, further supporting this trend.

Category-wise Analysis

Form Insights

Within the form category, Multi-Layer PCB is the leading segment in the global market, accounting for an estimated share of around 45% of total revenues. Multi-layer boards are essential for applications requiring high circuit density, signal integrity, and compact packaging, such as ADAS controllers, infotainment head units, power electronics, and advanced body control modules. As vehicles integrate more features without significantly expanding available space, multi-layer architectures enable OEMs to consolidate functionality while maintaining reliability and electromagnetic compatibility.

Single-sided and double-sided PCBs still play important roles in cost-sensitive and less complex applications such as basic lighting, simple relay and fuse boxes, and some comfort and body functions. However, their relative share in terms of value is lower because of the lower price per unit and simpler designs. In contrast, multi-layer boards often command higher value due to tighter manufacturing tolerances, advanced materials, and more demanding quality requirements.

Vehicle Type Insights

By vehicle type, passenger car is the leading segment in the automotive PCB market, with an estimated share of about 70% of the total market. Passenger cars represent most of the global vehicle production and are at the forefront of adopting electronics-intensive features such as advanced infotainment, connectivity, ADAS, and electrified powertrains. Regulatory requirements for safety and emissions, combined with consumer demand for comfort, convenience, and digital experiences, are most pronounced in the passenger vehicle segment. This drives higher PCB content per unit, as each vehicle often contains dozens of control units and sensor modules.

Commercial vehicles, including light commercial vehicles, trucks, and buses, contribute a smaller but steadily evolving share, focused more on telematics, fleet management, powertrain efficiency, and safety systems. While unit volumes are lower, commercial vehicles are beginning to adopt more sophisticated driver assistance and connectivity solutions, especially in logistics, long-haul trucking, and urban bus fleets.

Level of Autonomy Insights

In terms of level of autonomy, conventional vehicles currently represent the leading segment in the automotive PCB market, with an estimated share of around 60%, reflecting the large global base of vehicles with basic to moderate levels of driver assistance. These vehicles still rely on PCBs for engine control, transmission management, body electronics, infotainment, and limited ADAS functions such as cruise control, parking assistance, or basic collision warning. However, semi-autonomous vehicles form the fastest-advancing segment from a PCB content perspective, as they incorporate more sophisticated sensor suites, centralized controllers, and redundancy. This includes vehicles with highway pilot, adaptive cruise control with lane centering, and automated parking. Autonomous vehicle programs, including robotaxis and pilot fleets, remain limited in volume but require extremely advanced electronic architectures, which drive very high PCB value per unit.

Application Insights

Within applications, ADAS and Basic Safety constitute the leading segment in the Automotive PCB Market, estimated to account for around 40% of total market revenues. The proliferation of safety features mandated or encouraged by authorities in North America, Europe, Japan, China, and other key markets, such as automatic emergency braking, lane departure warning, blind spot detection, and driver monitoring systems, has created strong, sustained demand for sophisticated PCBs.

Infotainment and connectivity, along with body, comfort, and vehicle lighting, also contribute significantly to PCB demand, particularly in passenger cars where user experience is a key differentiator. Powertrain components, including engine control units in combustion vehicles and power electronics in electrified vehicles, add further PCB volume and value, especially for multi-layer and high thermal stability designs.

Regional Insights

North America Automotive PCB Market Trends

In North America, the Automotive PCB Market is driven by strong adoption of advanced safety and connectivity features, especially in the United States, where regulatory agencies and safety organizations promote widespread deployment of ADAS technologies. Many new vehicles incorporate forward collision warning, lane keeping assistance, and advanced airbag control systems, all reliant on robust PCBs in sensors and control units. The region also hosts significant development and deployment of connected vehicle platforms, over-the-air software updates, and digital cockpit architectures, which increase PCB complexity and volume.

The North American automotive ecosystem benefits from a strong innovation base, including semiconductor and electronic component suppliers, research institutions, and a mature Tier-1 supplier network. Investments in electric vehicle platforms by both established automakers and new entrants are adding high-voltage and power electronics requirements. At the same time, cybersecurity and functional safety standards introduced at industry and regulatory levels are driving the use of higher-reliability boards and redundant architectures.

Europe Automotive PCB Market Trends

In Europe, the Automotive PCB Market reflects a combination of stringent safety and emissions regulations, strong premium vehicle production, and rapid electrification. Countries such as Germany, France, Spain, and the U.K. are key hubs for high-end vehicles that integrate sophisticated ADAS, digital cockpits, and connectivity features. European Union regulations targeting road safety and carbon emissions have accelerated the adoption of active safety systems, electrified powertrains, and energy-efficient components, all of which rely on high-performance PCBs.

Regulatory harmonization across the European single market helps standardize requirements for safety and emissions, which facilitates scale for automotive electronics and PCB suppliers. Additionally, Europe’s push toward carbon neutrality and the deployment of charging infrastructure supports higher penetration of electric and plug-in hybrid vehicles, thereby increasing PCB content related to power electronics and battery management.

Asia Pacific Automotive PCB Market Trends

Asia Pacific represents the largest regional share of the Automotive PCB Market, underpinned by high vehicle production volumes, strong electronics manufacturing capabilities, and rapid electrification. China, Japan, South Korea, and ASEAN economies are central to both vehicle assembly and PCB manufacturing, creating dense ecosystems where design, fabrication, and integration occur in proximity. China is a key driver of electric vehicle adoption, supported by policy incentives, large-scale charging infrastructure, and a growing domestic supply chain for batteries and power electronics, all of which significantly increase PCB demand.

Japan and South Korea add further depth through their leadership in automotive electronics, semiconductor technology, and high-reliability PCB manufacturing. ASEAN countries are emerging as attractive hubs for vehicle assembly and parts production, benefitting from competitive labor costs and regional trade agreements. Across Asia Pacific, local regulations on safety, emissions, and connectivity are tightening, pushing automakers to integrate more advanced ADAS and infotainment systems.

Competitive Landscape

The Automotive PCB Market is moderately concentrated at the top, with a cluster of large Asia-based manufacturers and several global electronics players, while a long tail of regional and niche suppliers serves specific customers and applications. This structure reflects high entry barriers related to capital investment, process capability, and stringent automotive quality standards.

Leading companies focus on expanding multi-layer and high-density interconnect capacity, investing in automation, and strengthening relationships with major Tier-1 suppliers and OEMs. Key differentiators include reliability performance, ability to support design for manufacturing, regional production footprints, and experience with automotive qualification and traceability.

Key Market Developments:

- In September 2024, Passive System Alliance, a Taiwan-based company, announced the production of printed circuit boards (PCBs) at its new plant in Malaysia. The electronic part manufacturers aim to leverage the huge demand for automotive components from major car makers.

- In May 2024, Chin-Poon Industrial, known for its significant focus on automotive PCB production, has announced plans to invest an additional approximately US$ 27.3 million to expand its factory site in Thailand.

Companies Covered in Automotive PCB Market

- Chin Poon Industrial

- Meiko Electronics

- Nippon Mektron

- TTM Technologies

- KCE Electronics

- Tripod Technology

- Unimicron Technology

- Kingboard Chem GRP

- Amitron Corp

- CMK Corp.

- Other Key Players

Frequently Asked Questions

The global automotive printed circuit board (PCB) market was estimated at approximately USD 11.0 billion in 2026 and around USD 16.6 billion in 2033.

EV powertrains, battery management systems, and power electronics significantly increase PCB content per vehicle. Growing implementation of safety sensors, radar, lidar, and compute modules raises demand for advanced PCBs.

The multi-layer segment is expected to witness exceptional growth on account of the rise in the need for compact, data-intensive solutions in cars.

Asia Pacific is the dominant hub, accounting for the largest share of automotive PCB production and consumption (often 35% of global revenues).

Leading PCB manufacturers serving automotive customers include Chin Poon Industrial, Meiko Electronics, Nippon Mektron, TTM Technologies, and KCE Electronics.