- Automotive Components & Materials

- Automotive Conversion Kit Market

Automotive Conversion Kit Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Conversion Kit Market by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), Application (Power Conversion, Brake Conversion, Lights Conversion, Locking System Conversion, Energy Saving Conversion), End-User (Personal, Fleet Operators, Government Projects), and Regional Analysis for 2026-2033

Automotive Conversion Kit Market Share and Trends Analysis

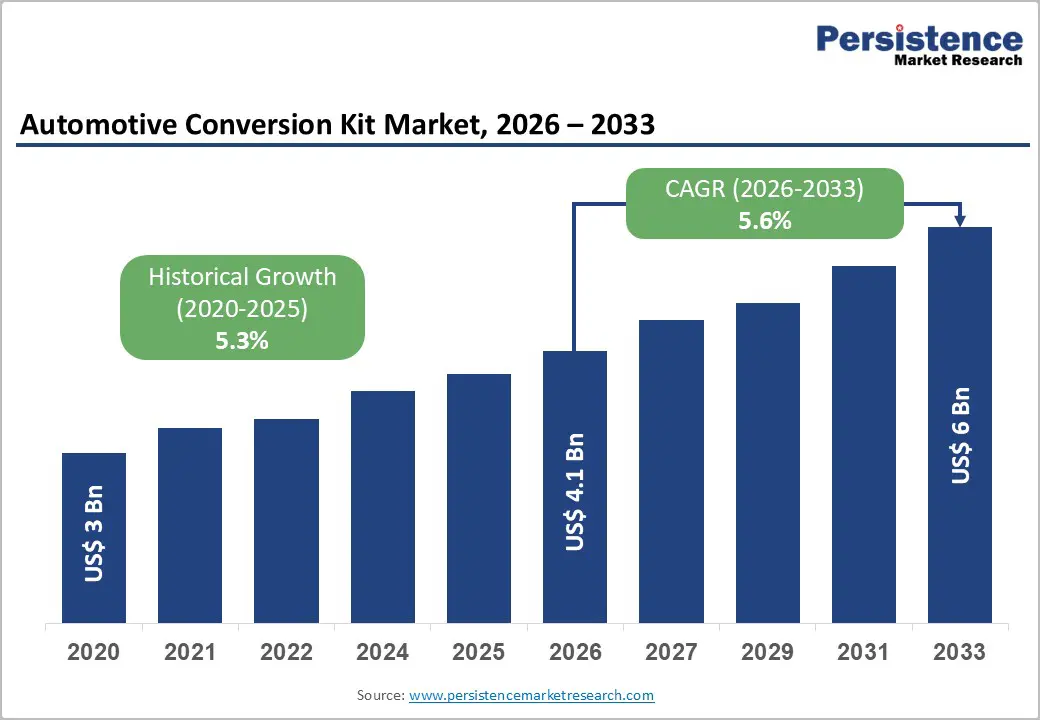

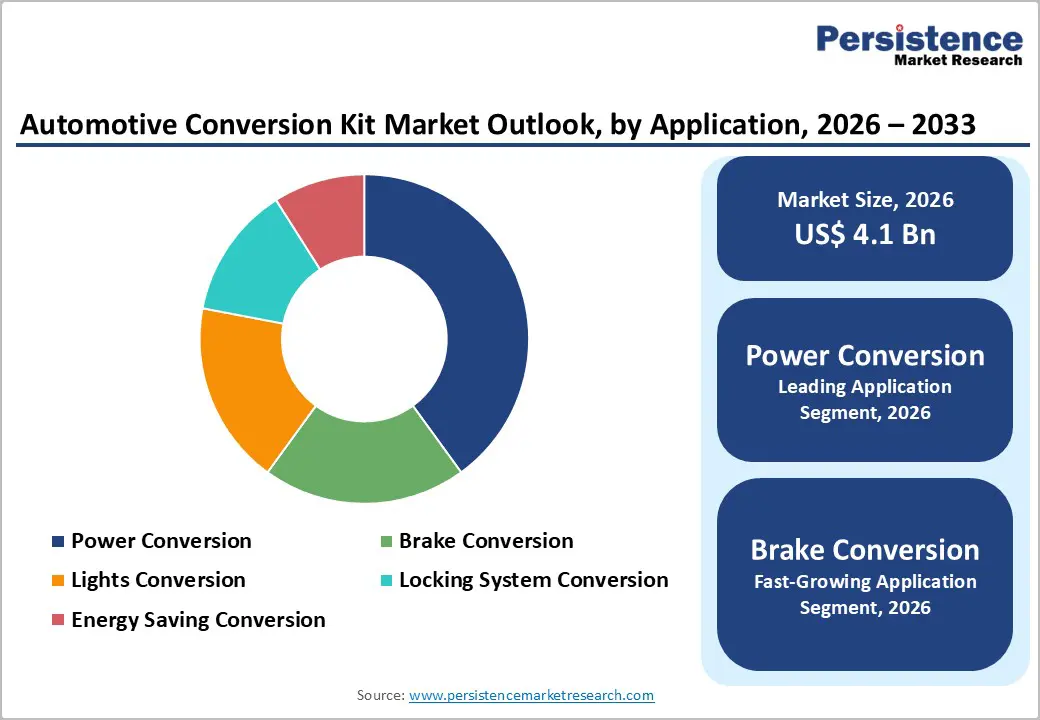

The global automotive conversion kit market size is likely to be valued at US$ 4.1 billion in 2026, and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 5.6% during the forecast period 2026-2033.

Market expansion is driven by rising demand for vehicle customization and a shift towards sustainable mobility solutions, reflecting broader consumer interest in performance and energy-efficient modifications. Technological integration across automotive systems, including advanced powertrain adaptations and intelligent lighting conversions, enhances market adoption by increasing the reliability and functionality of aftermarket solutions. Demographic trends, particularly among urban youth and automotive enthusiasts, contribute to a preference for personalized vehicles, thereby stimulating market activity.

Healthcare and safety regulations governing vehicle performance necessitate upgrades to braking, locking, and energy management systems, encouraging the adoption of conversion kits. Digital commerce and e-commerce penetration facilitate accessibility of conversion kits to a wider audience, improving sales efficiency and consumer reach. Global automotive manufacturing growth provides infrastructure support for aftermarket installations and expands opportunities for collaboration between OEMs and aftermarket providers.

Key Industry Highlights

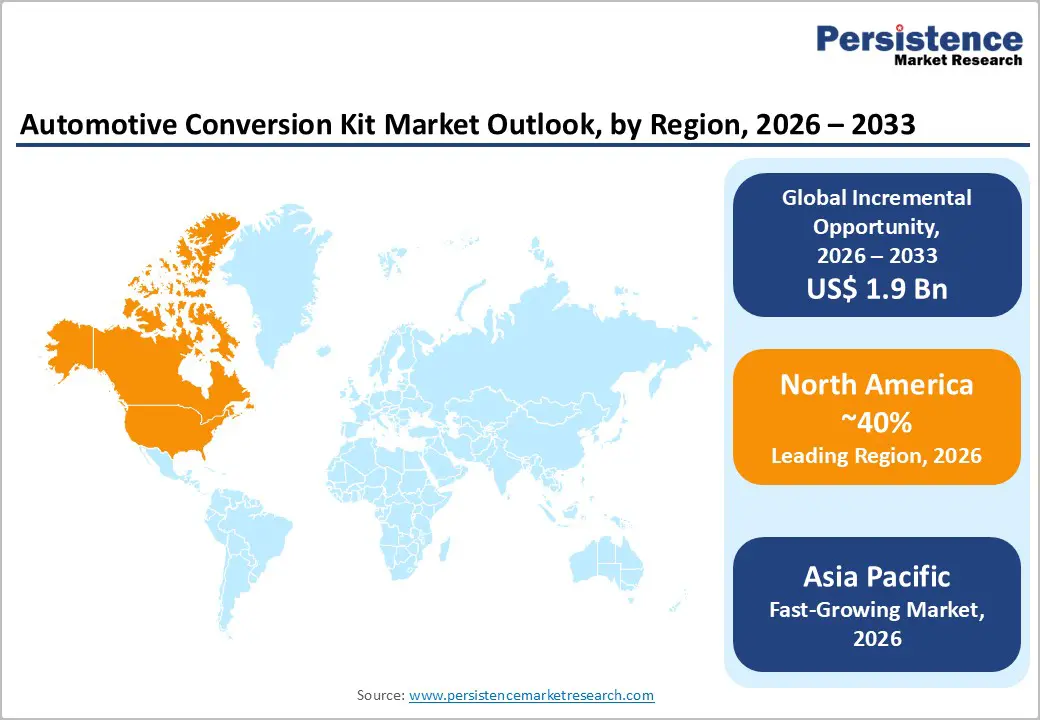

- Dominant Region: North America is projected to hold 40% of the market in 2026, driven by tight automotive safety regulations and widespread adoption of conversion kits.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by urban mobility expansion and rising demand for energy-efficient retrofits.

- Leading Application: Power conversion kits are projected to hold over 40% revenue share in 2026, supported by energy efficiency, performance, and regulatory compliance.

- Fastest-growing Application: Brake conversion kits are expected to be the fastest-growing segment from 2026 to 2033, driven by safety awareness, regulatory enforcement, and fleet adoption.

- February 2026: Royal Enfield introduced E20 fuel conversion kits for Bharat Stage III (BS3) and Bharat Stage IV (BS4) motorcycles, enabling compatibility with 20% ethanol-blended petrol while improving compliance.

| Key Insights | Details |

|---|---|

| Automotive Conversion Kit Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements and Innovation

Continuous development in electric powertrains, modular drivetrains, and advanced energy storage solutions transforms vehicle retrofit opportunities. Innovations in battery management systems and lightweight materials improve energy efficiency, increase operational range, and reduce total lifecycle cost for fleet and individual vehicle owners. Integration of smart diagnostics and adaptive control systems enables real-time monitoring, predictive maintenance, and seamless compatibility with existing vehicle electronics, driving faster adoption among commercial operators. Advanced modular designs reduce installation time, support scalable deployment, and enhance reliability, enabling operators to modernize legacy vehicles while maintaining operational efficiency.

Government policies promoting sustainable mobility amplify the impact of these technological improvements. Incentives for electrification, grants for charging infrastructure, and operational support schemes create economic signals that encourage investment in retrofitting initiatives. National programmes targeting significant electric-vehicle adoption provide a strategic horizon for the research, development, and deployment of modular conversion systems. Integration of vehicle-to-grid capabilities and adaptive energy management improves performance and operational flexibility, while advanced modular components allow rapid scaling and customization across multiple segments.

Urbanization and Demographic Shifts

Rapid demographic shifts and rising population concentration in urban centers are reshaping mobility demand structures and consumer preferences in transport ecosystems. Global data indicate that cities will accommodate about 45% of the world’s population in 2025, with this share more than doubling since the mid-20th century, underscoring the scale of urban growth and migration toward economic hubs. As residents cluster in dense urban agglomerations, the demand for efficient, adaptable, and space-effective personal transport solutions grows, especially where public transit systems are stretched or incomplete. Rising urban incomes and lifestyle shifts towards modern, tech-enabled transport options further contribute to greater interest in custom-upgrade solutions that enhance performance, sustainability and utility of existing vehicles.

Demographic transformations such as a rising working-age population and increasing household formation in cities amplify the demand for flexible transport assets that suit diverse usage patterns across urban and peri-urban zones. Growth in urban populations is accompanied by expansions in employment centers, commercial districts, and satellite towns, creating longer and more complex daily travel routes that strain conventional transport infrastructure and raise interest in alternative mobility approaches. Urban residents frequently seek tailored upgrades to vehicle capabilities, such as enhanced energy efficiency or low-emission retrofits, in response to constraints of traffic congestion, limited parking, and regulatory emissions policies.

High Installation and Maintenance Costs

The cost structure associated with converting legacy vehicles to modern propulsion systems stems from several systemic inefficiencies and technical demands. Retrofitting involves replacing core mechanical and electrical subsystems such as engines, fuel delivery systems, and control electronics with bespoke high-voltage components. Batteries, which typically account for a very large share of total vehicle conversion costs, must meet stringent safety and performance criteria; this necessity drives up procurement costs and requires specialized handling, testing, and integration protocols. Skilled technicians commanding premium labor rates are essential to perform precise calibration of these complex systems, and in many regions, the limited availability of certified facilities further inflates installation expenses, as firms must either invest in training or pay outside specialists for compliance-grade work.

Maintenance costs for converted vehicles also reflect structural complexity and supply chain fragmentation. While electrically powered systems can reduce long-term servicing requirements compared with internal combustion propulsion, they introduce dependencies on high-value spare parts, proprietary management software, and certified diagnostic tools. Batteries in particular require periodic health assessments and potential refurbishment over a vehicle’s life cycle; the absence of standardized component sizes and domestic manufacturing scale amplifies replacement costs.

Regulatory and Standardization Challenges

The absence of harmonized certification protocols forces every conversion project into a bespoke compliance exercise under distinct national and regional rules. In the United States, the Environmental Protection Agency (EPA) exercises authority under the Clean Air Act to enforce emissions standards on modified vehicles, including conversions, and maintains a list of conversion systems that meet applicable requirements updated as of June 11, 2025, on its official site. This creates a technical and administrative burden for kit producers seeking certification across multiple jurisdictions since meeting one set of criteria does not guarantee acceptance elsewhere, increasing lead times and engineering costs. Meeting emissions and safety standards, such as obtaining an EPA Certificate of Conformity or state-certified approval in places like California, requires firms to allocate significant resources toward testing, documentation, and iterative design adjustments rather than scaling production or reducing end-user prices.

In markets such as India, legal frameworks specify that retrofit systems must be approved by designated agencies like the Automotive Research Association of India (ARAI) or International Centre for Automotive Technology (ICAT) under technical standards, while local transport offices verify post-installation certification prior to registration with limited authorized garages available for compliance inspection. The dual dependency on central approval and local execution introduces administrative variability that can delay certification by months, deter investment from smaller manufacturers, and push buyers toward conventional vehicles that carry standard factory certifications.

Fleet Electrification and Commercial Adoption

Rapid integration of electrified commercial vehicles into transport networks is a pivotal growth lever for mobility-focused fleet operators, driven by compelling government targets and policy support that are shifting procurement toward cleaner powertrains. The Government of India has formally set a target for electric vehicle penetration of 30% of total vehicle sales by 2030 under national electrification initiatives and aligned with global frameworks, signaling strategic public-sector commitment to decarbonization and operational efficiency in mass transport and logistics sectors. Commercial transport represents high-utilization assets where electrification can substantially reduce energy costs over the lifecycle and lower fuel dependency for enterprises managing large vehicle pools.

Widespread adoption in public transit, freight, and corporate logistics fleets is underpinned by regulatory mandates for cleaner transport and fiscal incentives that improve return on investment for fleet managers. Public sector electrification agendas (including incentives for electric buses and trucks) encourage capital deployment in zero-emission transport solutions that align with national climate objectives and energy security strategies. Electrified fleets generate operational benefits such as lower maintenance and reduced total cost of ownership relative to conventional vehicles on long-haul and high-usage routes.

Integration with Smart and Autonomous Systems

Smart and autonomous systems unlock significant opportunities by enabling aftermarket kits to support advanced vehicle capabilities aligned with evolving regulatory and infrastructure priorities. Governments are actively modernizing automated driving frameworks and supporting integration of automated driving system technologies with broader transport ecosystems, reflecting public safety and mobility goals. The U.S. Department of Transportation (USDOT) released updated automated vehicle guidance in 2025 that expands its automated driving systems framework to facilitate safer deployment and innovation in automation technologies, while offering public access to testing data tools managed by the National Highway Traffic Safety Administration (NHTSA) for Level-2 and higher systems. These policy initiatives encourage the adoption of sensor fusion, connectivity and advanced control architectures that rely on modular integration with vehicle systems.

Demand trends show that automation technologies such as advanced driver assistance and higher-level autonomous controls are increasingly viewed as foundational elements for future mobility solutions, including connected infrastructure and smart city networks. Real-time interaction among vehicles, roadside units, and communication systems delivers improved situational awareness, traffic flow optimization, and safety outcomes, aligning with government goals to reduce crashes and congestion. Automotive conversion kits that retrofit vehicles with components enabling connectivity, AI-assisted perception and control, and vehicle-to-everything (V2X) interaction align with these trends, creating avenues for revenue streams through tech upgrades, compliance retrofits, and aftermarket innovation.

Category-wise Analysis

Vehicle Type Insights

Passenger vehicles are expected to account for around 55% of the automotive conversion kit market revenue share in 2026, reflecting high demand for customization and widespread urban use. Growing consumer preference for personalizing vehicles through performance, aesthetic, and functional upgrades drives this dominance. Energy-efficient conversions, including braking, lighting, and powertrain modifications, attract environmentally conscious owners seeking reduced operational costs. Technological compatibility with multiple passenger vehicle models allows modular solutions to meet diverse preferences and ensure scalability across different brands. Accessibility to urban service centers, certified technicians, and e-commerce platforms further supports adoption, enabling seamless installation, after-sales support, and timely upgrades.

Light commercial vehicles are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by the adoption of fleet optimization and energy-efficient retrofits. Commercial operators focus on minimizing operational costs while meeting increasingly stringent regulatory requirements, which drives the adoption of braking, locking, and power conversion kits. High vehicle uptime, reliability, and operational performance demands encourage integration of advanced technological solutions, including telematics and energy-efficient modules. Expanding urban delivery networks and emission standards accelerate retrofitting activity. Fleet managers benefit from modular kits that allow rapid deployment across multiple vehicles, while digital service platforms facilitate maintenance, monitoring, and compliance reporting, supporting sustainable operational strategies.

Application Insights

Automotive power conversion kit extracts are poised to dominate with a forecasted market share of over 40% in 2026, powered by increased focus on vehicle energy optimization and performance enhancement. Demand rises from both passenger and commercial vehicle owners seeking reduced fuel consumption and improved operational efficiency. Powertrain modifications help meet global emissions regulations while maintaining vehicle performance standards. Reliability and cross-model compatibility ensure adoption across diverse fleets. Collaborations with OEMs and alignment with regional regulatory frameworks support scalable distribution and aftermarket availability. Advanced technological integration in power conversion systems, including intelligent control modules, enhances consumer confidence and drives large-scale uptake in urban and commercial markets.

The automotive brake conversion kit is estimated to be the fastest-growing segment from 2026 to 2033, driven by heightened safety awareness and stricter regulatory enforcement. Adoption is primarily led by fleet operators, commercial vehicles, and high-performance passenger segments that require enhanced braking efficiency, durability, and reliability. Increasing focus on accident prevention and road safety standards encourages retrofitting older vehicles. Digital commerce platforms and integrated service networks improve accessibility, simplify installation, and reduce downtime. Technological innovations in electronic braking assistance, anti-lock systems, and modular kit designs further accelerate adoption. Support from certified service centers strengthens confidence in operational performance and compliance, driving consistent market expansion.

Regional Insights

North America Automotive Conversion Kit Market Trends

North America is projected to capture an estimated 40% of the automotive conversion kit market share in 2026, reflecting strong adoption of aftermarket vehicle modifications across passenger and commercial segments. Dominance stems from advanced urban infrastructure and high vehicle density in metropolitan corridors, which supports rapid deployment of energy-efficient retrofits, braking enhancements, and power conversion systems. Regulatory frameworks, including emission standards and safety mandates, incentivize operators and private owners to upgrade existing fleets with compliance-ready solutions. High disposable income and a mature consumer base for personalized and performance-oriented vehicles contribute to elevated penetration rates. Technological sophistication in conversion kits, including modular design, telematics integration, and compatibility with electric and hybrid drivetrains, positions this market segment for consistent uptake.

Strong alignment between technological capability and regulatory enforcement reinforces competitive advantage in adoption. Commercial fleets prioritize operational efficiency, uptime, and energy optimization, creating substantial demand for advanced retrofitting solutions. Investment in training programs and certified service networks ensures installation quality and system reliability, which supports customer confidence in high-value kits. Growing public awareness of environmental impact and cost-efficiency benefits accelerates demand for solutions that reduce fuel consumption and extend vehicle lifecycle. Integration with digital platforms, including e-commerce sales channels and mobile service scheduling, allows rapid access to kits and maintenance services.

Europe Automotive Conversion Kit Market Trends

Europe demonstrates significant potential in the automotive conversion kit market, supported by stringent environmental regulations and strong adoption of electrification initiatives. Adoption is driven by regulatory mandates that target emissions reductions, encouraging vehicle owners and fleet operators to retrofit older vehicles with energy-efficient power conversion systems and braking upgrades. Commercial fleets, particularly in logistics and public transport, prioritize operational efficiency, uptime, and compliance with emission standards, creating demand for modular conversion solutions compatible with multiple vehicle models. Integration of digital monitoring tools and telematics enables real-time tracking of fuel consumption, energy efficiency, and system performance, aligning with broader sustainable mobility and smart city objectives.

Investment in advanced infrastructure and technical expertise further accelerates adoption. Certified service networks, installation training programs, and partnerships with vehicle manufacturers ensure high-quality deployment of retrofitting solutions. The presence of mature automotive supply chains allows efficient distribution of modular kits and rapid integration of technological innovations, including energy recovery systems and intelligent braking assistance. Expansion of e-commerce and digital sales channels improves accessibility for small operators and private vehicle owners. Demand for high-performance modifications that enhance safety, reduce emissions, and optimize energy usage positions the market for continued expansion.

Asia Pacific Automotive Conversion Kit Market Trends

Asia Pacific is forecasted to be the fastest-growing market for automotive conversion kits between 2026 and 2033, stimulated by rapid expansion of urban mobility networks, rising vehicle ownership, and increasing emphasis on energy-efficient transportation solutions. Growth is driven by commercial operators in logistics, delivery, and public transport seeking to optimize fleets, improve fuel efficiency, and meet regulatory compliance requirements. High-density urban corridors create demand for braking and powertrain retrofits to enhance safety and operational performance. Infrastructure development, including certified service centers and skilled technician programs, reduces barriers to installation and supports widespread adoption. Consumer willingness to invest in performance-oriented upgrades for passenger vehicles complements commercial demand.

Government programs promoting low-emission vehicles and energy-efficient transport reinforce the growth trajectory. Urbanization trends, high traffic congestion, and evolving delivery requirements drive the adoption of advanced retrofitting solutions, including modular power and braking kits compatible with multiple vehicle models. E-commerce platforms and digital service networks increase accessibility, enable rapid installation, and reduce fleet downtime. Regulatory oversight, such as emission monitoring and compliance reporting, incentivizes the adoption of conversion technologies to meet operational and environmental standards. Operators benefit from modular, scalable kits that allow phased integration, minimizing capital expenditure while maximizing fleet performance.

Competitive Landscape

The global automotive conversion kit market exhibits a moderately fragmented structure, with leading players controlling 40% of the market share. Key players such as Quigley Motor Company, Banks Power, Explorer Van Company, Advanced RV, Sportsmobile, and BraunAbility drive market activity through a combination of technological innovation and robust aftermarket service offerings. These companies focus on developing modular and scalable solutions that cater to diverse vehicle categories, including passenger and commercial fleets. Emphasis on compliance with regulatory standards, particularly emission and safety requirements, strengthens credibility and adoption rates across urban and commercial markets.

Market fragmentation creates opportunities for emerging players to capture niche segments by addressing specialized consumer needs. Smaller providers focus on unique applications such as off-road customization, high-performance modifications, or accessibility-focused retrofits, complementing offerings from established players. Technological advancements, including telematics integration, digital monitoring, and modular system design, enable new entrants to differentiate through innovation and targeted service models. The competitive environment drives continuous enhancement of product offerings, ensuring that both established and emerging providers contribute to overall market expansion.

Key Industry Developments

- In September 2025, Electrogenic partnered with Exedy to develop a classic Mini electric conversion kit featuring a compact axial flux AFT140i motor and pr-?assembled battery pack, enabling Heritage Mini owners to retrofit their vehicles with an EV powertrain that delivers over 125 km of urban range and high torque performance.

- In August 2025, Maruti Suzuki announced plans to roll out E20 fuel conversion kits for older models to help vehicles originally built for lower ethanol blends operate safely and effectively with India’s expanded 20% ethanol petrol rollout, supporting the nation’s ethanol-blended fuel initiative.

- In May 2025, Evolectric unveiled its Gen3 CircularEV electric work truck conversion kit, offering fleets an advanced retrofit solution that extends range, integrates smart vehicle technologies, and lowers conversion costs for medium and heavy-duty work truck electrification.

Companies Covered in Automotive Conversion Kit Market

- Quigley Motor Company

- Banks Power

- Explorer Van Company

- Advanced RV

- Sportsmobile

- BraunAbility

- Ujoint Offroad

- QuadVan 4x4 Conversions

- Off Grid Adventure Vans

- AAMCO Transmissions, Inc.

Frequently Asked Questions

The global automotive conversion kit market is projected to reach US$ 4.1 billion in 2026.

Rising demand for vehicle customization, energy-efficient retrofits, and regulatory compliance is driving the market.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Expansion of electric and hybrid retrofits, fleet electrification, and integration with smart vehicle technologies present key market opportunities.

Some of the key market players include Quigley Motor Company, Banks Power, Explorer Van Company, Advanced RV, Sportsmobile, and BraunAbility.