- Automotive Components & Materials

- Automotive Clutch Slave Cylinder Market

Automotive Clutch Slave Cylinder Market Size, Share, and Growth Forecast, 2026 – 2033

Automotive Clutch Slave Cylinder Market by Material (Plastic, Steel, Aluminum, Composite), System Type (Mechanical, Pneumatic, Hydraulic), Application (Commercial Vehicles, Heavy Trucks, Veterinarians, Motorcycles, Passenger Vehicles), and Regional Analysis for 2026-2033

Automotive Clutch Slave Cylinder Market Share and Trends Analysis

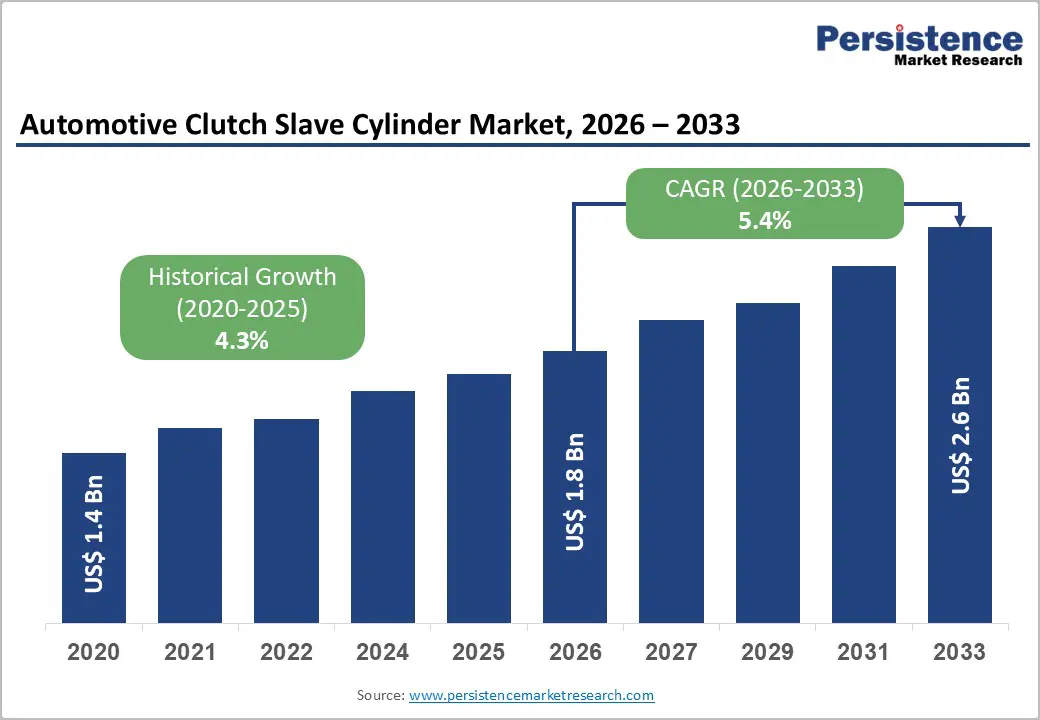

The global automotive clutch slave cylinder market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 5.4% during the forecast period 2026−2033.

Growth trajectory indicates a stable expansion driven by vehicle production recovery, drivetrain durability requirements, and the adoption of hydraulic systems. Increasing global vehicle parc stimulates replacement demand for transmission components, which strengthens aftermarket consumption. Expansion of light-commercial transport networks increases the usage intensity of manual transmission systems, accelerating component wear cycles and sustaining recurring demand. Integration of advanced sealing materials and corrosion-resistant alloys improves reliability, encouraging manufacturers' preference for hydraulic clutch actuation solutions. Industrial automation in component manufacturing improves consistency and reduces defect probability, which supports supplier qualification across original equipment manufacturer programs.

Key Industry Highlights

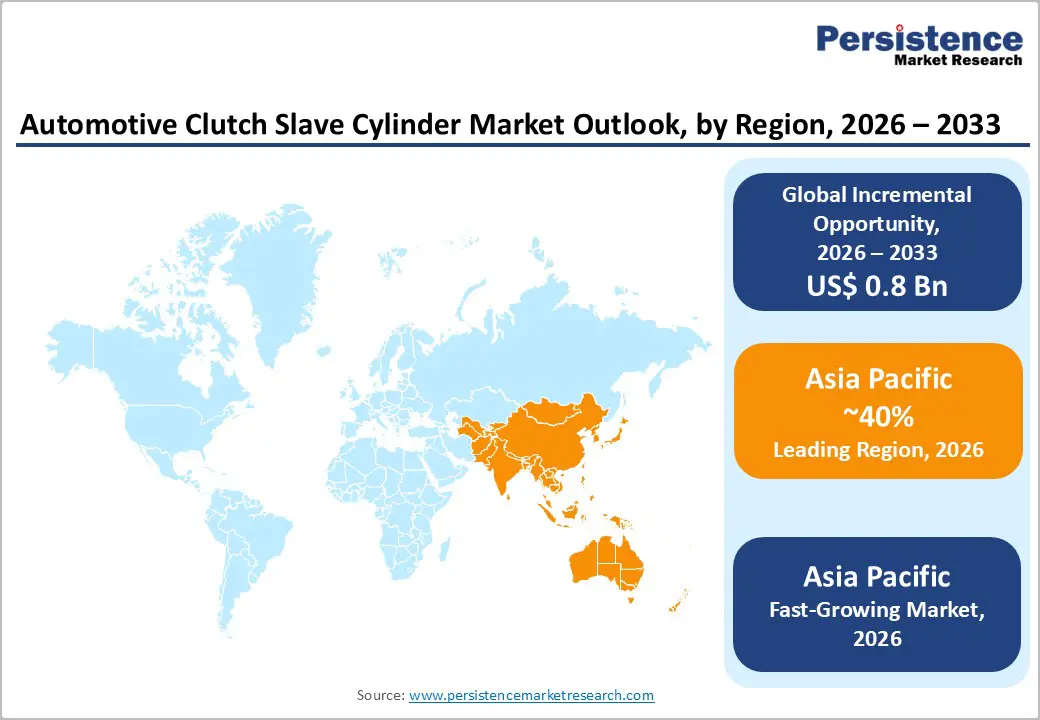

- Dominant Region: Asia Pacific is projected to dominate with 40% market share in 2026, driven by high production, supplier networks, and original equipment manufacturer (OEM) demand.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, stimulated by diverse vehicles, transmission trends, and growing aftermarket demand.

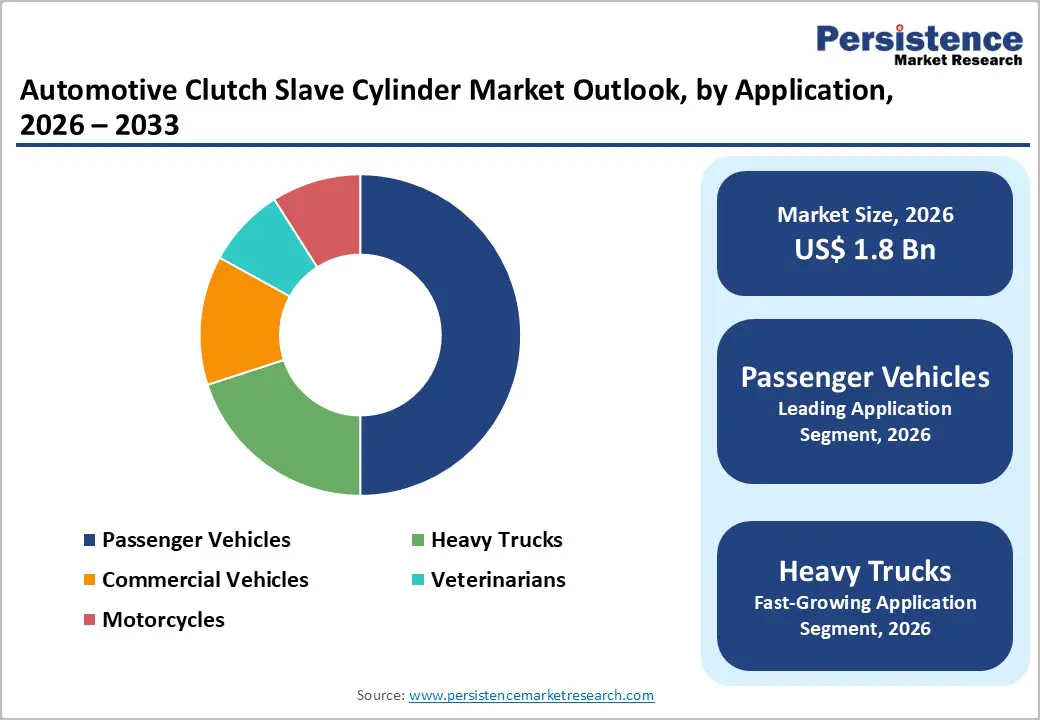

- Leading Application: Passenger vehicles are poised to lead with nearly 50% market share in 2026, fueled by large vehicle parc, routine maintenance, and accessible aftermarket support.

- Fastest-growing Application: Heavy trucks are expected to grow the fastest between 2026 and 2033, supported by logistics expansion, infrastructure investment, and increased clutch replacement demand.

| Key Insights | Details |

|---|---|

| Automotive Clutch Slave Cylinder Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Soaring Vehicle Production in Emerging Economies

The rapid expansion of vehicle production across emerging economies is a critical driver of demand for automotive components such as clutch slave cylinders, as these regions are becoming major manufacturing and consumption hubs. Increased production volumes mean original equipment manufacturers and suppliers are scaling up assembly lines and sourcing larger quantities of driveline and hydraulic system parts to meet both domestic and export orders. Government data show that in India, vehicle production rose by nearly 33% over the decade to FY25, according to the Economic Survey 2025-26 released by India’s Ministry of Finance, indicating strong structural growth in output.

In parallel with domestic demand, export orientation is reshaping production footprints; many emerging markets are integrating into global supply chains as export platforms for both finished vehicles and parts. Expansion of production facilities attracts both tier-1 and tier-2 suppliers to establish operations closer to assembly lines, enhancing responsiveness and reducing logistics costs. Large-scale production clusters improve economies of scale and encourage investment in specialized components such as hydraulic assemblies for clutches, which are essential in manual and automated transmissions widely used in these markets.

Increasing Adoption of Hydraulic Clutch Systems

Adoption of hydraulic actuation in clutch systems is propelled by tangible drivetrain performance improvements that align with evolving powertrain demands. Hydraulic mechanisms transmit force through fluid pressure, enabling consistent and smoother clutch engagement with reduced pedal effort relative to traditional mechanical linkages. This precision supports enhanced drivability, tighter control over engagement timing, and reduced operator fatigue in both passenger and commercial platforms, raising end-user acceptance and OEM integration rates. Compared to cable or purely mechanical systems, hydraulics maintain performance under fluctuating temperatures and loads, supporting reliability across duty cycles and helping preserve component life spans while meeting escalating performance expectations.

Policy-driven trends also reinforce this adoption by shaping powertrain strategies that favor technologies capable of supporting advanced transmissions and electrified platforms. Government data highlight a significant rise in electrified vehicle adoption globally, with more than 20% of new cars sold worldwide being electric by 2024, a trend driven by emissions regulations and incentives documented in global energy outlooks. While electric vehicles increasingly shift powertrain architectures away from conventional clutches, hybrid and automated manual transmissions still leverage hydraulic engagement for torque management and seamless power transitions.

Shift toward Automatic Transmissions

Rising adoption of vehicles with automatic transmissions reduces demand for manual clutch mechanisms, eliminating the need for operator-engaged clutch assemblies. Automatic gearboxes, including torque-converter automatics, continuously variable transmissions (CVTs), and dual-clutch systems, provide smooth gear shifts without manual clutch operation, directly shrinking the installation base for hydraulic clutch components. Consumer preference for convenience, coupled with urban traffic conditions, drives OEM focus on automatic systems, limiting production of traditional clutch parts and affecting supply chain strategies.

Policy frameworks and regulatory priorities reinforce this trend, encouraging vehicle technologies that optimize fuel efficiency, lower emissions, and improve drivability. Automatic and automated gearboxes maintain engines within optimal performance bands and integrate effectively with hybrid and electrified powertrains, aligning with government mobility objectives. Automotive research institutions highlight software-defined vehicle capabilities and advanced transmission systems as key industry focus areas in recent mobility reports, further marginalizing conventional clutch solutions and redirecting manufacturer investments toward fully automated drivetrain technologies.

Electrification of Vehicle Powertrains

Shifts in global powertrain adoption have materially reduced demand for conventional clutch systems. Traditional clutch assemblies, including slave cylinders, are integral to internal combustion engine (ICE) and manual transmission architectures. Electrified vehicles predominantly use electric motors with single-speed reduction gearing, eliminating multi-gear transmissions and the hydraulic actuation mechanisms that clutch slave cylinders support. As a result, investment and production planning across OEMs increasingly prioritize electric and hybrid powertrain components that are incompatible with existing clutch technology, forcing suppliers to explore alternative product lines or risk declining orders. Procurement strategies of tier-1 and tier-2 suppliers accordingly reflect this technological transition, with capital allocation shifting away from legacy mechanical systems toward electric drive components and associated control electronics, a trend that exerts downward pressure on traditional clutch component volumes.

Policy frameworks and commercial incentives are further accelerating this transition. According to the International Energy Agency (IEA)’s Global EV Outlook 2025, global sales of electric cars in 2025 are expected to surpass 20 million units, representing more than one-quarter of all cars sold worldwide, illustrating a material shift in new vehicle powertrain mix toward zero-emission alternatives. This rapid adoption translates into a smaller addressable market for clutch actuators in new-vehicle builds, particularly in advanced automotive markets where electrification targets and emission standards are stringent.

Lightweight Material Innovations to Unlock New Avenues

Material substitution driven by innovative lightweight solutions represents a strategic growth vector because modern vehicle efficiency and emissions regulations demand component mass reduction at scale. Government research highlights that substituting traditional heavy metals with advanced alloys, composites, and engineered polymers can reduce structural part weight by up to 50% and improve fuel economy by 6–8% for every 10% reduction in overall vehicle mass, directly supporting fleet efficiency targets set for the mid 2020s on official energy policy platforms. This regulatory and technical imperative compels manufacturers to explore high-strength aluminum, magnesium, and reinforced polymers in critical subsystems to align with global standards for energy consumption and emissions.

Engineering lighter components creates downstream operational advantages by lowering inertial loads and reducing overall energy demand during vehicle acceleration and deceleration cycles. Policy frameworks from key government agencies promote the integration of lightweight materials as part of broader efforts to reduce petroleum consumption and greenhouse gas emissions across transportation systems. High-strength-to-weight materials also enhance packaging efficiency and enable smaller ancillary systems, such as brakes and suspension units, to be optimized without degrading performance. This convergence of manufacturing capability, materials science, and regulation forms the rationale for prioritizing lightweight-material innovation as a defining opportunity, as suppliers and OEMs adapt designs to meet performance targets while addressing fuel-efficiency and sustainability benchmarks.

Expansion in Automated Manual Transmission (AMT) Applications

Government regulations promoting vehicle fuel efficiency and emission reductions are accelerating the adoption of automated manual systems in passenger and commercial vehicles. Policies such as Corporate Average Fuel Economy (CAFE) standards emphasize improved fuel economy, encouraging manufacturers to implement transmission technologies that optimize gear shifts and clutch control. Automated systems improve drivability and efficiency while maintaining mechanical simplicity, aligning with policy-driven sustainability goals. This creates a direct opportunity to integrate advanced clutch actuation mechanisms into these powertrains.

Automated manual architectures combine the benefits of manual and automatic systems, delivering reduced shift effort, faster response, and lower drivetrain energy loss compared to traditional manual gearboxes. Lightweight and cost-efficient designs appeal to both fleet operators and individual consumers seeking performance and efficiency gains without premium automatic system costs. Rising preference for these transmissions in urban mobility and commercial applications amplifies demand for precise, reliable clutch control components, positioning them as essential enablers in the broader transition toward automated drivetrains and optimized vehicle operation.

Category-wise Analysis

Clutch System Type Insights

The hydraulic clutch system is poised to lead with a forecasted 60% market share in 2026, owing to performance consistency, driver comfort, and integration compatibility with modern transmissions. Hydraulic actuation delivers uniform force transmission regardless of cable stretch or mechanical wear, which improves reliability. Automotive training institutions promote hydraulic systems as the preferred technology for contemporary vehicles, which strengthens consumer trust. Cultural acceptance grows because drivers associate hydraulic systems with smoother engagement and reduced pedal effort. Retail penetration expands as replacement kits become widely available through online automotive parts platforms. Preventive maintenance awareness encourages vehicle owners to replace hydraulic components before failure, which sustains aftermarket demand.

The pneumatic clutch system is anticipated to be the fastest-growing segment between 2026 and 2033, driven by increasing deployment in heavy commercial transport fleets. Pneumatic assistance reduces the manual effort required for clutch operation, which benefits long-distance drivers operating heavy trucks. Fleet operators recognize ergonomic advantages and reduced fatigue risk, which strengthens acceptance. Industrial vehicle manufacturers promote pneumatic systems for high-torque applications where hydraulic systems alone may require reinforcement. Online distribution networks enable the procurement of replacement pneumatic components in remote logistics regions, which improves accessibility. Preventive maintenance programs implemented by transport companies include periodic inspection of pneumatic assemblies, which increases replacement frequency.

Application Insights

Passenger vehicles are positioned as the leading segment with nearly 50% of the automotive clutch slave cylinder market revenue share in 2026, supported by a large global vehicle parc, routine maintenance cycles, and widespread service infrastructure. Passenger vehicles represent the largest installed base of manual and automated transmissions in operation across developing regions. Automotive service networks recommend periodic inspection of clutch hydraulic components to maintain performance, which increases replacement demand. Digital diagnostic tools used in service centers identify hydraulic leakage or pressure irregularities, which accelerates repair decisions. Accessibility of spare parts through e-commerce platforms improves procurement efficiency for independent workshops. The cost efficiency of replacement components relative to transmission overhaul encourages timely servicing.

Heavy trucks are expected to be the fastest-growing segment between 2026 and 2033, driven by logistics expansion, infrastructure investment, and rising freight intensity. Transport authorities promote road freight corridors to enhance trade connectivity, which increases heavy truck utilization. Higher torque loads in heavy vehicles accelerate wear of clutch components, which increases replacement frequency. Fleet maintenance programs incorporate predictive diagnostics using telematics data to identify hydraulic system degradation early. Accessibility improves through regional distribution centers supplying spare parts to fleet operators. Cost-efficiency considerations encourage preventive replacement rather than reactive repair, thereby sustaining demand. Advanced materials enable production of cylinders capable of withstanding extreme pressure cycles, which strengthens confidence among commercial fleet managers.

Regional Insights

North America Automotive Clutch Slave Cylinder Market Trends

North America maintains a significant position in the automotive clutch slave cylinder landscape, supported by mature automotive manufacturing bases in the United States, Canada, and Mexico. Established OEM operations focus on high-quality production standards and integration of advanced drivetrain technologies, including automated manual and performance-oriented manual transmissions. Strong aftermarket infrastructure sustains consistent demand for replacement clutch components, particularly in light and medium commercial vehicle fleets where maintenance cycles are shorter. Local production efficiency, combined with proximity to major vehicle assembly lines, reduces lead times and logistics costs, reinforcing steady component adoption. Industrial policies promoting technological advancement and emission compliance further stimulate incorporation of reliable clutch actuation systems into new vehicle models, supporting production volume continuity.

Growth trends are shaped by increasing adoption of hybrid drivetrains and commercial transport solutions that retain conventional clutch mechanisms. Fleet operators emphasize operational efficiency, seeking components that reduce maintenance downtime and ensure performance under variable-load conditions. Aftermarket expansion benefits from established dealer networks and widespread service capabilities, enabling rapid replacement and refurbishment of clutch assemblies. Supplier collaboration with engineering teams ensures adaptation to evolving OEM specifications, including enhanced durability and responsiveness.

Europe Automotive Clutch Slave Cylinder Market Trends

Europe maintains a significant position in the market for automotive clutch slave cylinders, driven by established vehicle manufacturing hubs in Germany, France, and Italy. Advanced engineering capabilities and long-standing OEM presence create high standards for precision drivetrain components, supporting integration of sophisticated clutch systems in both passenger and commercial vehicles. Demand is sustained by a mature vehicle parc, in which replacement cycles and aftermarket service requirements consistently contribute to component volume. Focus on light commercial vehicles and mid-size passenger cars, which retain manual and automated manual transmissions, reinforces steady uptake. Well-developed supply chains and localized component production allow manufacturers to optimize cost, quality, and delivery schedules, aligning with stringent industry regulations on safety and emissions.

Growth in this area is influenced by regulatory frameworks emphasizing fuel efficiency and environmental compliance, promoting adoption of advanced transmission systems that improve operational efficiency. Market expansion is supported by gradual electrification trends, where hybrid configurations maintain clutch usage, sustaining demand for actuation systems. Strong aftermarket infrastructure, including widespread authorized service networks, enhances component replacement opportunities and ensures consistent sales across vehicle lifecycles. Collaborative programs between OEMs and suppliers focus on innovation in lightweight materials and durable hydraulic components, optimizing system reliability and performance.

Asia Pacific Automotive Clutch Slave Cylinder Market Trends

Asia Pacific is expected to dominate, with an estimated 40% share of the automotive clutch slave cylinder market in 2026, reflecting the region's scale in vehicle manufacturing and concentrated production hubs. China and India lead output, supported by high domestic demand and export-oriented assembly facilities that attract international OEM investments. Dense supplier networks for mechanical components, including clutch systems, enable efficient integration of original equipment production and aftermarket supply. Competitive manufacturing costs, government incentives for industrial expansion, and rapid urbanization further reinforce market dominance, driving consistent demand for precision drivetrain components across passenger and commercial vehicle segments.

Asia Pacific is forecasted to be the fastest-growing regional market for automotive clutch slave cylinder between 2026 and 2033, stimulated by diversified vehicle portfolios and evolving transmission preferences that maintain clutch utilization in mid-range and commercial vehicle segments. Automated manual systems and cost-efficient manual drivetrains continue to capture market share, creating sustained component demand. Expansion of aftermarket networks, driven by increasing vehicle parc and service requirements, complements production growth. Strategic supplier investments in engineering capacity and advanced quality standards enable rapid adaptation to OEM and aftermarket specifications, enhancing competitiveness.

Competitive Landscape

The global automotive clutch slave cylinder market structure exhibits moderate fragmentation, combining dominant tier-one suppliers with a network of regional component manufacturers. Robert Bosch, EXEDY Corporation, BorgWarner, ZF, and FTE Automotive lead original equipment supply, leveraging extensive production capabilities, technical expertise, and established relationships with major vehicle assemblers. Smaller manufacturers primarily address aftermarket needs, focusing on replacement and refurbishment channels for passenger and commercial vehicles. Market competition is influenced by material selection, machining precision, and consistent performance under varying operational conditions, ensuring component reliability across manual and automated manual drivetrains.

Innovation in clutch actuation systems and integration with transmission assemblies drives supplier competitiveness. Bosch and ZF emphasize proprietary technologies and process automation to enhance durability and reduce response times, while EXEDY Corporation and BorgWarner Inc. focus on high-performance solutions for commercial and performance vehicles. FTE Automotive strengthens positioning through customization and engineering support tailored to regional production requirements. Supply chain reliability and the ability to meet stringent quality benchmarks determine access to new vehicle programs, with engineering agility critical for adapting to evolving OEM specifications.

Key Industry Developments

- In January 2026, Australian Clutch Services’ performance brand XClutch unveiled a new range of complete clutch kits and a universal concentric slave cylinder for motorsport applications at the SEMA Show, expanding its portfolio for high-performance and aftermarket segments.

- In May 2025, Ducati is developing a sport-bike automatic clutch system that allows riders to switch between manual and automated clutch operation for enhanced performance and convenience.

- In April 2025, GAIGAO introduced a new universal clutch slave cylinder designed for broad vehicle compatibility and enhanced hydraulic performance, reinforcing its aftermarket product lineup.

Companies Covered in Automotive Clutch Slave Cylinder Market

- Robert Bosch GmbH

- EXEDY Corporation

- BorgWarner Inc.

- ZF Friedrichshafen AG

- FTE Automotive GmbH

- Aisin Seiki Co., Ltd.

- AISIN Europe S.A.

- Schaeffler AG

- Valeo SA

- Magneti Marelli

Frequently Asked Questions

The global automotive clutch slave cylinder market is projected to reach US$ 1.8 billion in 2026.

Rising adoption of manual and automated manual transmissions, along with increasing vehicle production and aftermarket demand, is driving the market.

The market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Expansion of automated manual transmission applications and growth in light commercial vehicle segments represent key market opportunities.

Some of the key market players include Robert Bosch GmbH, EXEDY Corporation, BorgWarner Inc., ZF Friedrichshafen AG, and FTE Automotive GmbH.