- Automotive Components & Materials

- Automotive 48V System Market

Automotive 48V System Market Size, Share, and Growth Forecast 2026 - 2033

Automotive 48V System Market by Power Output (Mild Hybrid and Full Hybrid), by Application (Fuel Efficiency Improvement, Start-Stop Functionality, Regenerative Braking, Active Roll Stabilization and Electric Power Steering), Component (48V battery, Electric motor/generator, Power inverter, DC/DC converter and Others), Vehicle Type (Passenger Cars, Light Commercial Vehicles and Heavy Commercial Vehicles), and Regional Analysis for 2026 - 2033

Automotive 48V System Market Share and Trends Analysis

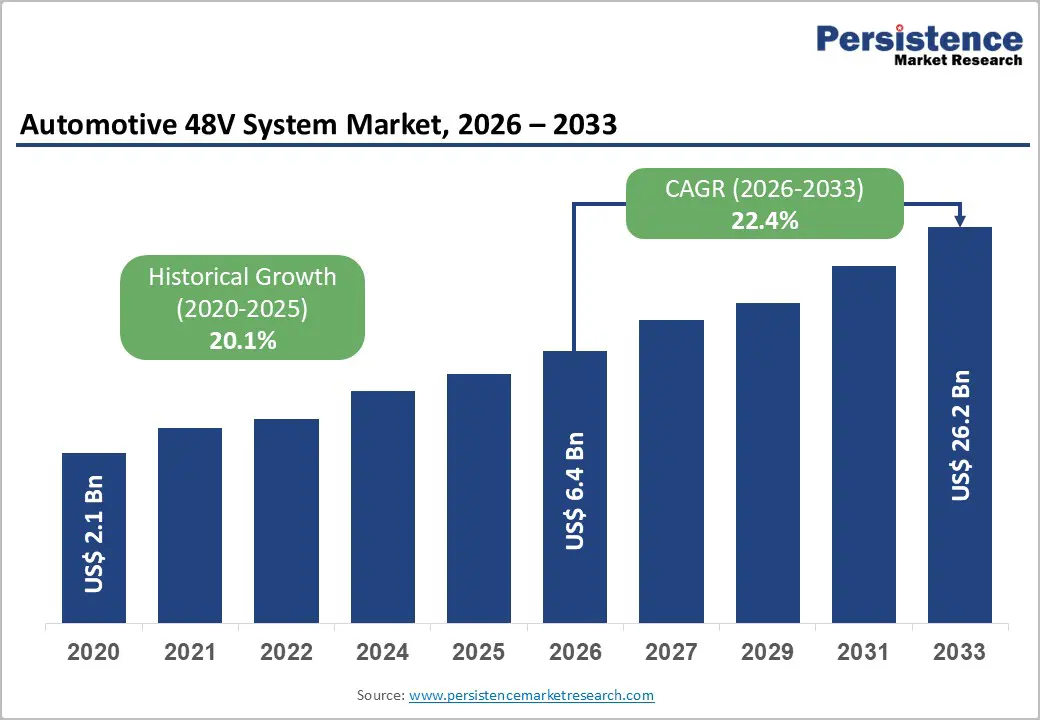

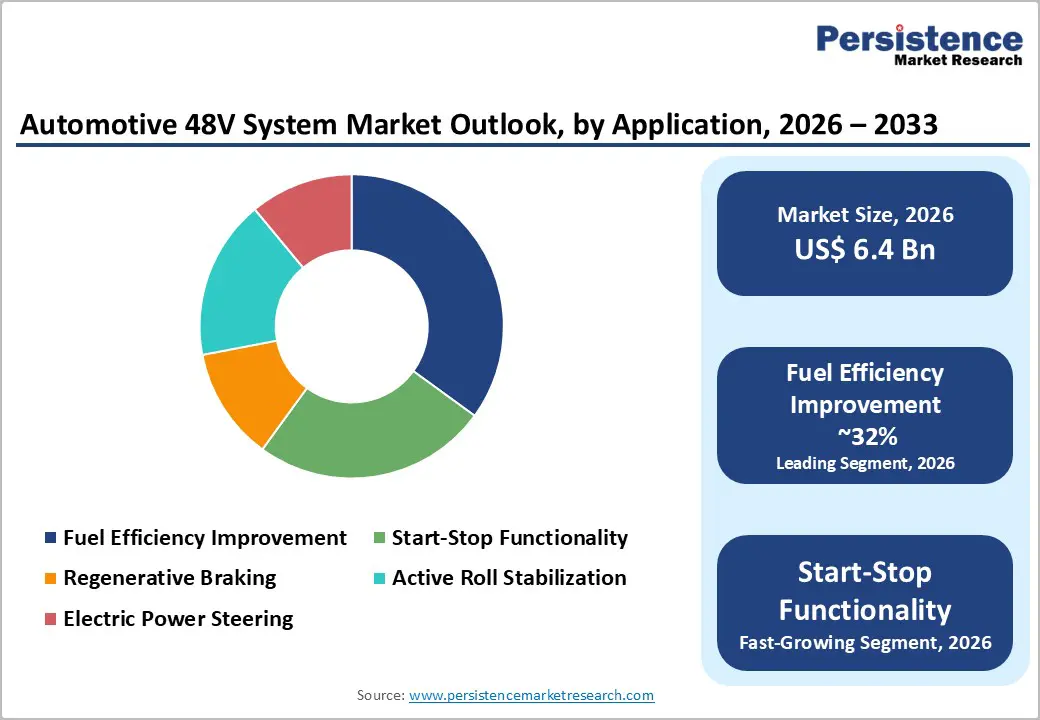

The global automotive 48V system market size is likely to be valued at US$ 6.4 billion in 2026 and is projected to reach US$ 26.2 billion by 2033, growing at a CAGR of 22.4% between 2026 and 2033.

The market's exceptional expansion reflects a fundamental shift toward electrification as automotive manufacturers seek cost-effective solutions for achieving increasingly stringent emissions regulations while delivering enhanced vehicle performance and fuel efficiency. 48V mild-hybrid systems represent a critical bridge technology enabling cost-effective compliance with European Union CO2 emission standards requiring 95 grams of CO2/km and emerging Euro 7 regulations taking effect in November 2026 for light-duty vehicles and May 2028 for heavy-duty vehicles.

Key Industry Highlights:

- Leading Region: Europe dominates with 38% global market share. Stringent EU CO2 emission standards, Euro 7 regulatory requirements, and manufacturer electrification investments establish Europe as the primary market driver, with Germany, United Kingdom, France, and Spain collectively representing 62% of regional market value.

- Fastest Growing: Asia Pacific is the fastest-growing region at 24.6% CAGR Extraordinary vehicle production volumes exceeding 50.74 million units annually, rapid government-supported electrification adoption, and cost-competitive manufacturing establish Asia Pacific as the highest-growth market through 2033.

- Dominant Segment: Mild Hybrid systems dominate with 73% market share. Cost-effective implementation, regulatory compliance capability, and proven fuel efficiency improvements drive mild-hybrid architecture standardization across passenger cars and light commercial vehicle segments.

- Fastest Growing segment: Fuel Efficiency Improvement, fastest-growing application at 32% market share - Consumer demand for total-cost-of-ownership reduction, regenerative braking integration, and start-stop functionality expansion drives accelerating adoption across diverse vehicle platforms and market segments.

- Opportunity: 48V Battery components lead at 41% market share. Lithium-ion battery technology standardization, improved cost profiles, and sophisticated battery management system capabilities establish 48V batteries as foundational system infrastructure supporting expanding electrification applications.

| Key Insights | Details |

|---|---|

| Automotive 48V System Market Size (2026E) | US$ 6.4 Bn |

| Market Value Forecast (2033F) | US$ 26.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 22.4% |

| Historical Market Growth (CAGR 2020 to 2024) | 20.1% |

Market Dynamics

Drivers - Stringent Emissions Regulations and Corporate Average Fuel Economy Requirements

Regulatory mandates across European Union, North America, and Asia Pacific regions are driving accelerated adoption of 48V system technology as a pragmatic compliance pathway balancing cost-effectiveness with environmental objectives. The European Union's Fit for 55 legislation requires CO2 emissions reductions of 55% for passenger cars by 2030, while Euro 7 standards effective from November 2026 impose stringent particle number and particulate matter limits on all engine types. 48V mild-hybrid systems enable manufacturers to achieve mandatory emissions targets substantially more cost-effectively than full hybrid or battery electric powertrains, with production costs estimated at 30% of full-hybrid alternatives while delivering 70% of performance benefits. BMW's comprehensive strategy exemplifies regulatory-driven adoption, with the company planning expansion of its second-generation mild-hybrid electrification to 37 new models, building on existing 51-model lineup equipped with standardized 48-volt starter-generator technology achieving up to nine grams CO2/km reduction per vehicle.

Rising Demand for Hybrid Powertrain Solutions and Enhanced Vehicle Performance Characteristics

Consumer and manufacturer demand for hybrid powertrain solutions combining conventional internal combustion engines with electric propulsion systems is accelerating 48V system adoption through demonstrated benefits in fuel economy, vehicle performance, and operational reliability. 48V mild-hybrid architectures enable implementation of sophisticated features previously restricted to significantly more expensive full-hybrid or electric platforms, including active suspension systems, electric power steering, regenerative braking, active roll stabilization, and electric turbocharging. The market for mid-premium vehicles, commanding the largest aggregate value share, is particularly responsive to 48V system integration, as manufacturers leverage mild-hybrid technology to deliver premium driving experience characteristics while managing production costs and maintaining competitive pricing. 48V belt-driven starter-generator systems recover energy during vehicle deceleration through regenerative braking, storing recovered energy in small lithium-ion batteries for deployment during acceleration, reducing load on internal combustion engines and smoothing power delivery.

Restraints - High Initial Capital Investment and Integration Complexity Challenging Widespread Adoption

The capital-intensive nature of 48V system infrastructure development and integration complexity into existing vehicle architectures presents substantial barriers limiting widespread market penetration, particularly among cost-sensitive vehicle segments and emerging market manufacturers. 48V system implementation requires comprehensive vehicle redesign encompassing electrical architecture modification, integration of sophisticated power management electronics, development of specialized battery systems, and validation across numerous vehicle platforms.

Manufacturing facilities require significant capital investment in specialized production equipment, testing infrastructure, and workforce retraining, with initial implementation costs typically ranging from USD 500 million to USD 1.5 billion per vehicle platform. Regulatory compliance demands include cybersecurity validation, functional safety certification achieving ASIL D ratings, and integration verification with advanced driver assistance systems substantially extend time-to-market and development costs.

Technology Maturation Uncertainty and Competitive Alternative Pathways

Ongoing technological evolution and competitive electrification pathways create uncertainty regarding 48V system long-term market viability and investment returns, particularly as full electric vehicle costs decline and alternative intermediate technologies emerge. Full electric vehicle battery costs have declined approximately 89% from 2010 through 2024, with lithium-ion battery pack costs approaching USD 100/kilowatt-hour and continuing to decline, potentially displacing mild-hybrid technologies through total-cost-of-ownership advantages. Plug-in hybrid electric vehicle technology, enabling extended all-electric range capabilities, presents alternative compliance pathways for manufacturers prioritizing customer flexibility and infrastructure compatibility without incurring complete powertrain redesign.

Manufacturing capacity constraints for lithium-ion batteries, driven by competing demand from battery electric vehicle production, create procurement challenges and elevated costs for 48V system batteries, potentially constraining market growth. Technology standardization remains incomplete, with multiple vehicle architecture approaches including belt-driven, crankshaft-integrated, and axle-mounted starter-generator configurations limiting cross-platform standardization benefits and economies of scale.

Market Opportunities - Emerging Markets and Commercial Vehicle Segment Electrification Requirements

Developing economies in Asia Pacific, Latin America, and Middle East and Africa regions present exceptional growth opportunities through accelerating adoption of 48V technologies enabled by rising regulatory pressures, improving manufacturing infrastructure, and increasing per-capita vehicle ownership. India's automotive market expansion coupled with government commitments to emissions reduction and electrification milestones has catalyzed substantial 48V system adoption interest among domestic and multinational manufacturers. Commercial vehicle electrification represents a particularly compelling opportunity, with heavy-duty truck manufacturers increasingly integrating 48V systems to support advanced telematics, real-time condition monitoring, improved fuel efficiency for cost-sensitive fleet operators, and compliance with emerging emissions standards.

Advanced Driver Assistance Systems Integration and Autonomous Vehicle Development

The rapid proliferation of advanced driver assistance systems and accelerating autonomous vehicle development programs create unprecedented opportunities for 48V system manufacturers through integration of sophisticated sensor platforms, computing systems, safety-critical electrified functions. Modern ADAS platforms including adaptive cruise control, autonomous emergency braking, lane-keeping assistance, and automated parking require substantially elevated electrical power delivery, with 48V architectures enabling reliable operation of multiple concurrent safety systems where traditional 12V systems would experience voltage regulation challenges. Autonomous vehicle development programs conducted by Waymo, Cruise, and established automotive manufacturers require comprehensive electrification of vehicle subsystems including steering, braking, suspension, and propulsion, creating design requirements ideally suited to 48V system architecture capabilities.

Category-wise Analysis

Power Output Insights

Mild hybrid systems dominate the automotive 48V system market with approximately 73% share, driven by superior cost-effectiveness, accessible implementation across diverse vehicle platforms, and proven regulatory compliance capabilities. Mild-hybrid architectures utilizing 48V belt-driven starter-generators enable seamless integration into existing vehicle platforms without requiring fundamental powertrain restructuring, facilitating rapid manufacturer adoption and cost-effective scaling across product portfolios. BMW, Mercedes-Benz, Audi, Ford, and Volkswagen have established comprehensive mild-hybrid model lineups spanning compact vehicles through luxury sport utility vehicles, demonstrating technology accessibility across market segments. Mild-hybrid systems deliver 10-15% emissions reduction and approximately 20% fuel consumption improvement at substantially lower cost than full-hybrid or battery electric alternatives.

Vehicle Type Insights

Passenger cars maintain dominant market position with approximately 64% market share, reflecting substantially higher production volumes and consumer purchasing activity relative to commercial vehicles. The passenger car market demonstrates comprehensive 48V system adoption across compact, mid-size, premium, and luxury segments, with manufacturers recognizing market differentiation and competitive advantages from integrated mild-hybrid technology. Mercedes-Benz E-Class, BMW 5-Series, Audi A6, Volkswagen Passat, and comparable premium sedans standardize 48V systems across model lineups, establishing consumer expectations for integrated electrification across automotive market segments. Light Commercial Vehicles, expanding at approximately 24.7% CAGR, represent the fastest-growing segment driven by fleet operator demand for fuel efficiency improvements and operational cost reduction capabilities.

Application Insights

Fuel efficiency Improvement dominates application adoption with approximately 32% market share, reflecting manufacturer and consumer prioritization of total cost of ownership reduction and environmental impact mitigation. Regenerative braking systems enable recovery of kinetic energy during vehicle deceleration, converting energy traditionally dissipated into mechanical brake systems into stored electrical energy, subsequently utilized to power vehicle accessory systems or assist engine during acceleration. Start-Stop Functionality represents approximately 28% market share, enabling automated engine shutdown during traffic congestion, red lights, and short idle periods, generating proportional fuel consumption reduction and emissions mitigation. Regenerative Braking applications command approximately 18% market share and are expanding at accelerating rates as 48V system architectures increasingly enable sophisticated energy recovery and management capabilities.

Component Analysis

48V Battery components maintain market dominance with approximately 41% market share, reflecting fundamental system infrastructure requirements driving all system functionality. Lithium-ion battery technology utilizing LFP (lithium iron phosphate) or NCA (nickel cobalt aluminum) chemistries have become standardized in automotive 48V systems through demonstrated durability, safety profiles, and cost-effectiveness improvements. Battery management systems incorporating sophisticated cell-level monitoring, temperature regulation, and charge-discharge optimization have become essential components enabling reliable 48V battery longevity and performance consistency across vehicle lifetime applications. Electric Motor/Generator components represent approximately 24% market share, encompassing belt-driven starter-generators (BSG) and integrated motor-generator architectures providing dual functionality enabling both vehicle propulsion assistance and regenerative energy recovery during braking.

Regional Insights

North America Automotive 48V System Market Trends

North America represents the second-largest regional market with approximately 25% global market share, characterized by substantial regulatory drivers including EPA Phase 3 heavy-duty vehicle greenhouse gas standards, California's advanced clean fleet requirements, and progressively tightening CAFE (Corporate Average Fuel Economy) compliance mandates. The United States automotive market demonstrates accelerating 48V system adoption among mainstream manufacturers including Ford, General Motors, Stellantis, and transplant operations by German, Japanese, and Korean manufacturers, with 48V mild-hybrid technologies increasingly integrated across truck, sport utility vehicle, and crossover segments. Commercial vehicle electrification initiatives supported by U.S.

Canada's regulatory alignment with United States emissions standards and electric vehicle incentive programs has generated comparable adoption dynamics. Mexico's emergence as a significant automotive manufacturing hub for North American vehicle production has catalyzed 48V system investment in manufacturing facilities serving regional demand. North American adoption is anticipated to expand at approximately 21.3% CAGR through 2033, driven by regulatory compliance imperatives, consumer demand for fuel-efficient vehicles, and integration of 48V technologies into emerging autonomous driving and advanced driver assistance system platforms.

Europe Automotive 48V System Market Trends

Europe dominates the global automotive 48V system market with approximately 38% market share, driven by exceptionally stringent emissions regulations, comprehensive regulatory harmonization across European Union member states, and substantial manufacturer investments in electrification technologies. Germany, United Kingdom, France, and Spain collectively account for approximately 62% of European market value, with established automotive manufacturing bases including Mercedes-Benz, BMW, Volkswagen, Audi, Renault, Peugeot, and British Leyland derivatives aggressively pursuing 48V system integration across product portfolios.

The European Union's Fit for 55 legislations requiring 55% CO2 emissions reductions by 2030 and Euro 7 standards taking effect November 2026 have established compelling regulatory urgency for 48V system adoption, with manufacturers projecting 40-45% market penetration by 2030. BMW has expanded its second-generation 48V starter-generator technology to 51 vehicle models, with company projections indicating expansion to 88 models through 2030.

Asia Pacific Automotive 48V System Market Trends

Asia Pacific emerges as the fastest-growing regional market, commanding approximately 40% global market share and expanding at approximately 24.6% CAGR through 2033, driven by extraordinary vehicle production volumes, rapid electrification adoption, and progressive regulatory tightening across China, Japan, India, and Southeast Asian nations. China, accounting for approximately 45% of regional market share and producing 31.28 million vehicles in 2024, represents the primary demand engine through government electrification incentives, state-owned enterprise participation in 48V system component manufacturing, and automaker competition for domestic market dominance.

Chinese manufacturers including BYD, Geely, Chery, and Li Auto have rapidly integrated 48V technologies into mainstream vehicle offerings, capitalizing on cost advantages and responsive regulatory environment. Japan's traditional automotive leadership in hybrid technology has translated into substantial 48V system manufacturing capabilities, with companies including Denso, Bosch Japan, Continental Japan, and Panasonic operating advanced component production facilities.

Competitive Landscape

The global automotive 48V system market exhibits moderate consolidation among tier-one automotive suppliers including Bosch, Continental, Denso, Aptiv, Valeo, and Magna International collectively commanding approximately 60% of market share through comprehensive product portfolios, established OEM relationships, and advanced research and development capabilities.

Market leaders pursue growth through strategic acquisition of specialized electrification companies, establishment of enterprise partnerships with automotive manufacturers, and substantial investment in advanced power electronics, battery management systems, and integrated motor-generator technologies. Competitive differentiation increasingly reflects software-driven capabilities, cloud platform integration, and predictive maintenance system competencies rather than traditional hardware specifications.

Key Developments:

- In 2024, Ford launched a new generation of 48V mild hybrid vehicles, extending their reach to the mass-market SUV segment. These vehicles use a combination of internal combustion engines and 48V electric motors to improve fuel efficiency and emissions without the high costs of full electric or plug-in hybrid vehicles. This expansion marks a significant step in making 48V hybrid technology more accessible to consumers looking for affordable electrification options.

- In early 2024, Continental AG introduced an advanced 48V mild hybrid starter-generator (MHSG) designed to improve the integration of 48V systems in conventional vehicles. This system can provide greater energy recovery through regenerative breaking and assist in smoother starts and stops, all while reducing fuel consumption and emissions. It is expected to be used in several mid-range vehicles, contributing to the global adoption of 48V hybrid technology.

Companies Covered in Automotive 48V System Market

- Aptiv PLC

- BorgWarner

- Continental AG

- Denso Corporation

- Infineon Technologies

- Magna International

- Panasonic

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- Other Key Players

Frequently Asked Questions

The global automotive 48V system market is likely to be valued at US$ 6.4 billion in 2026 and is projected to reach US$ 26.2 billion by 2033, expanding at a 22.4% CAGR. This exceptional growth trajectory reflects accelerating manufacturer adoption of 48V technologies as cost-effective compliance solutions for increasingly stringent emissions regulations worldwide.

Primary growth drivers include stringent emissions regulations including EU CO2 standards (95 g/km), Euro 7 standards effective November 2026, and EPA Phase 3 heavy-duty vehicle greenhouse gas requirements. Rising consumer demand for fuel-efficient vehicles offering 10-15% emissions reduction and 20% fuel consumption improvements, combined with manufacturer electrification initiatives supporting advanced driver assistance systems and autonomous vehicle development, substantially accelerate market expansion.

Mild Hybrid systems dominate with approximately 73% market share, driven by superior cost-effectiveness at approximately 30% of full-hybrid powertrain costs while delivering 70% of performance benefits. Mild-hybrid architectures enable rapid integration across diverse vehicle platforms without requiring fundamental powertrain restructuring, facilitating scalable manufacturer adoption.

Europe maintains market leadership with approximately 38% global market share, driven by exceptional regulatory stringency and comprehensive manufacturer electrification investments. Asia Pacific emerges as the fastest-growing region with 24.6% CAGR, driven by extraordinary vehicle production volumes exceeding 50 million units annually and progressive government-supported electrification adoption.

Market leaders include Robert Bosch GmbH, Continental AG, Denso Corporation, Infineon Technologies Panasonic, and ZF Friedrichshafen.