- Automation & Robotics

- Automatic Checkweigher Market

Automatic Checkweigher Market Size, Share, and Growth Forecast, 2025 - 2032

Automatic Checkweigher Market by Product Type (Standalone Systems and Combination Systems), Technology Type (Strain Gauge and Electromagnetic Force Restoration), Industry (Food & Beverages, Pharmaceuticals, Consumer Products, Cosmetics, and Personal Care, and Others), and Regional Analysis for 2025 - 2032

Automatic Checkweigher Market Size and Trends Analysis

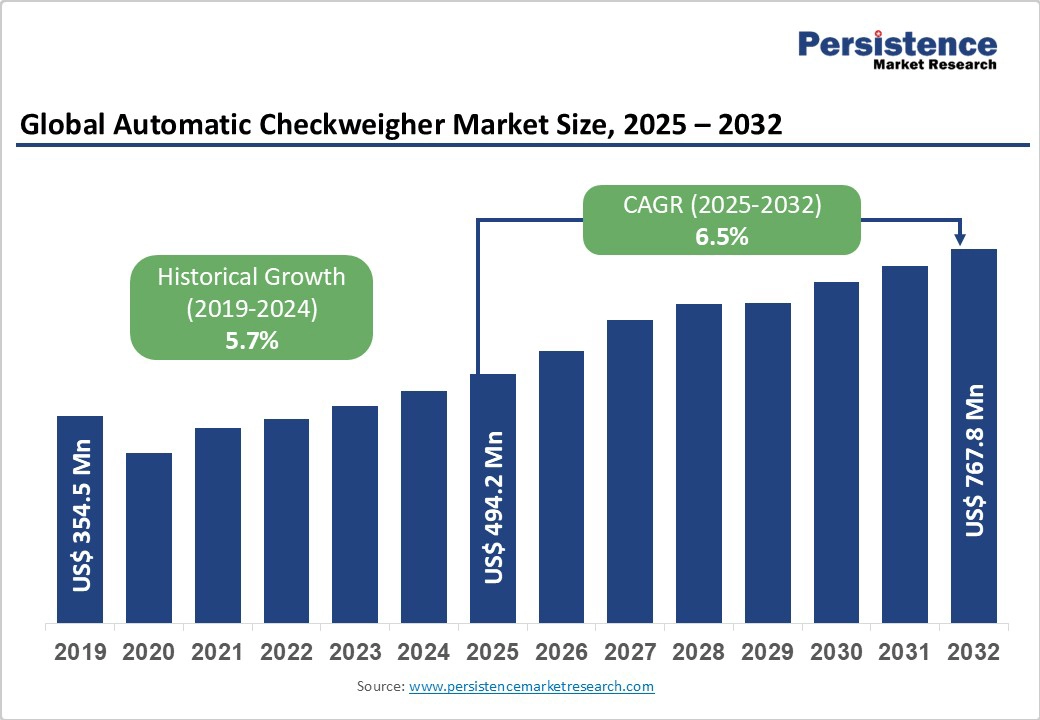

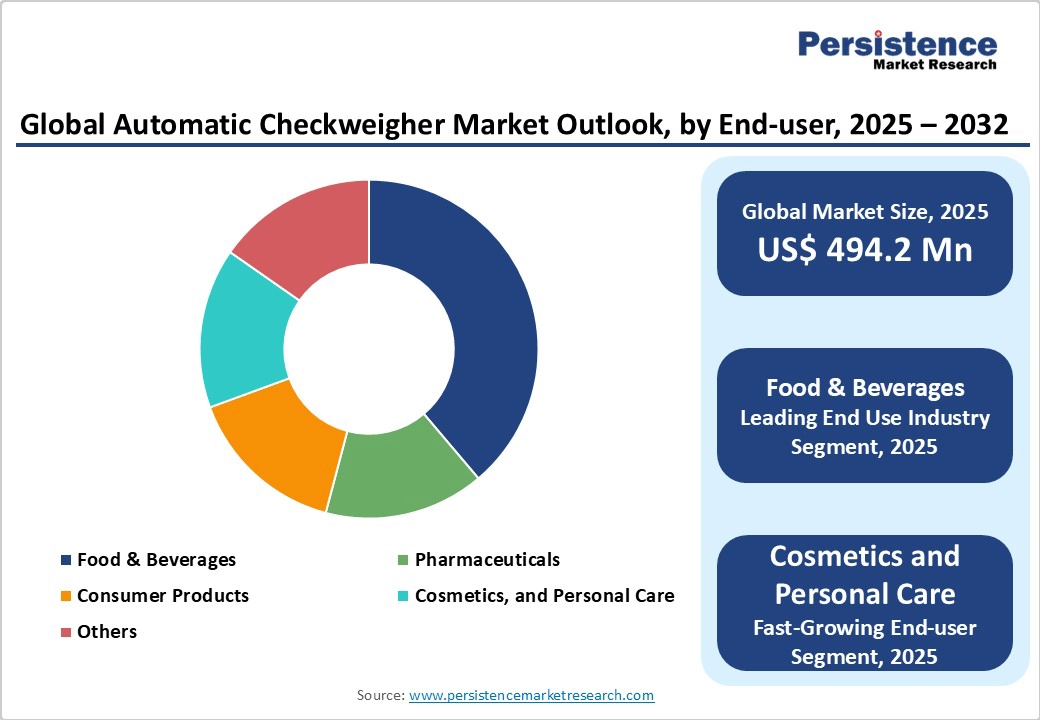

The global automatic checkweighers market size is likely to be valued at US$494.2 million in 2025 and is projected to reach US$767.8 million by 2032, growing at a CAGR of 6.5% between 2025 and 2032. The growing demand for precision automation, stringent regulatory compliance requirements, and digital transformation initiatives within the manufacturing sector are key factors driving global sales of automatic checkweighers.

Key Industry Highlights:

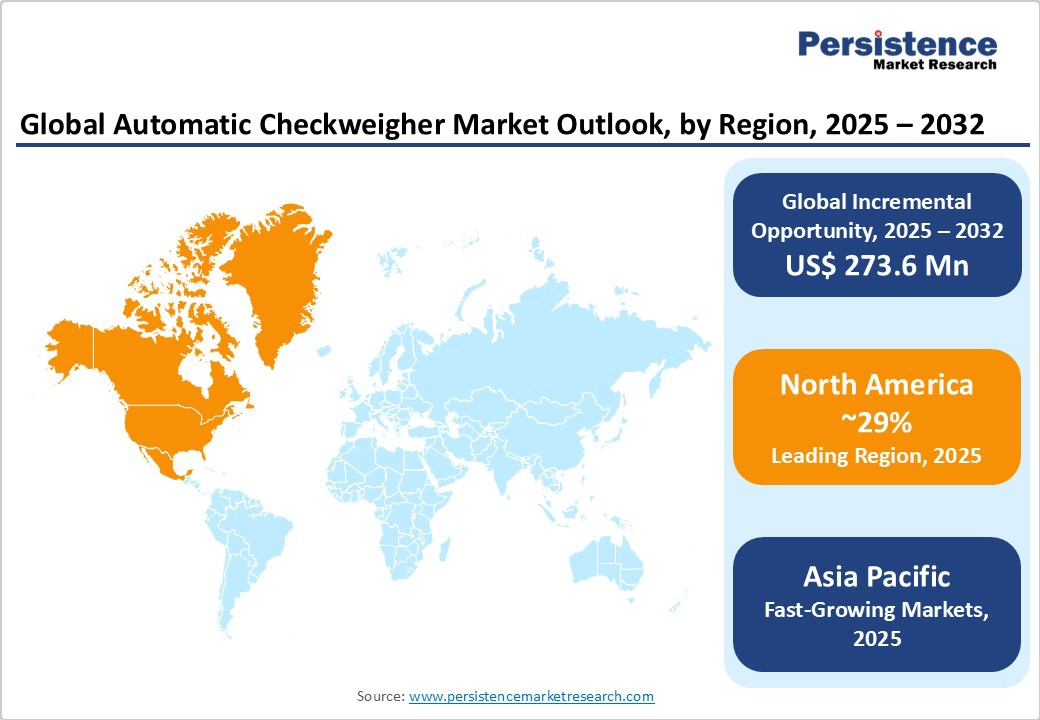

- Regional Leaders: North America is expected to dominate the global automatic checkweigher market, with a 29% market share in 2025, driven by advanced regulatory frameworks and high automation adoption rates.

- Leading Segments: Standalone Systems lead the market with a 59% share, as traditional, dedicated weighing machines are preferred for straightforward applications.

- Technology Performance: Electromagnetic Force Restoration (EMFR) technology dominates the checkweighers market with a 55% market share due to its high-speed operation, superior accuracy, and durability.

- Industry Applications: The food & beverages sector is dominant with approximately 46.9% volume share due to strict weight verification regulations, high production volumes, and quality demands.

| Key Insights | Details |

|---|---|

|

Automatic Checkweigher Market Size (2025E) |

US$494.2 Mn |

|

Market Value Forecast (2032F) |

US$767.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.5% |

Market Dynamics

Drivers - Stringent Regulatory Compliance and Food Safety Standards

The growing enforcement of weight-related regulations and evolving food safety standards have emerged as key drivers of growth for the automatic checkweighers market. Regulatory agencies, such as the FDA and the European Food Safety Authority, have tightened permissible error bands, transforming compliance from a secondary benefit into a primary purchase trigger. The FDA's Current Good Manufacturing Practice (CGMP) rules stipulate that weighing devices must achieve a precision of ±0.2 g at 280 ppm line speeds for pharmaceutical applications.

EU Directive 2014/32/EU harmonizes accuracy classes across member states, encouraging standardized procurement of premium instruments. These regulatory pressures compel manufacturers to invest in sophisticated checkweighing systems, with non-compliance resulting in substantial penalties, product recalls, and reputational damage.

Rising Demand for Quality Control and Waste Reduction

Manufacturing industries increasingly recognize checkweighers as essential tools for minimizing product giveaway and maintaining consistent quality standards. These systems help companies dramatically reduce expenses associated with selling overweight products by lowering average fill weight through increased precision.

The integration of advanced sensor technology and AI-powered analytics enables real-time process optimization, reducing waste while improving operational efficiency. Consumer awareness of product quality and safety has intensified pressure on manufacturers to implement comprehensive quality control measures, further driving the adoption of checkweighers across diverse sectors.

Manufacturing Automation and Industry 4.0 Integration

The rapid adoption of automated production systems is fundamentally transforming checkweigher deployment patterns. Companies pursuing heightened efficiency and reduced human error find automated checkweighers indispensable for real-time precision measurement. These devices integrate seamlessly with other automated processes, enhancing productivity while elevating product quality and regulatory compliance.

Industry 4.0 initiatives emphasize smart manufacturing environments where checkweighers communicate with SCADA and MES architectures through OPC UA protocols. This interconnectedness enables centralized functional control, predictive maintenance capabilities, and comprehensive data analytics that optimize production flows.

Restraint - High Initial Investment, Integration Complexity, and Maintenance Challenges

The automatic checkweigher market faces significant barriers due to the high initial capital expenditure required for advanced systems, which can be a major hurdle, especially for small and medium-sized enterprises (SMEs) operating with limited budgets. Installation and integration with existing production lines often demand specialized technical expertise and may cause operational downtime or disruptions during setup. The complexity increases when ensuring seamless communication between checkweighers, conveyors, sorting machines, and automated equipment, potentially leading to unexpected expenses.

These highly sensitive systems require frequent calibration and ongoing maintenance to preserve accuracy, posing continuous operational costs. Even minor malfunctions can result in regulatory non-compliance or quality issues. Coupled with rapid technological advancements, this creates pressure to upgrade or replace equipment more frequently than anticipated, increasing the total cost of ownership and limiting adoption among budget-conscious

Opportunities - Smart Factory Integration and IoT Connectivity

The evolution toward intelligent manufacturing environments creates significant opportunities for advanced checkweighing solutions. Integration with IoT frameworks enables remote monitoring, predictive maintenance, and comprehensive data analytics, transforming traditional quality control approaches. Artificial intelligence integration offers enhanced capabilities for process optimization, automatic adjustments, and predictive quality assurance, positioning checkweighers as central components in smart factory ecosystems. This convergence of automation, connectivity, and intelligence not only improves efficiency but also opens vast opportunities for global market expansion across diverse industries.

Combination System Innovation and Multi-Function Integration

The rising demand for space-efficient and cost-effective solutions is driving strong opportunities in the global automatic checkweigher market. Combination systems that integrate checkweighing with metal detection, X-ray inspection, or vision systems not only reduce facility footprint requirements by 20–25% but also deliver end-to-end quality assurance throughout the entire process. Moreover, the advancement of modular, scalable platforms tailored to different production capacities enhances flexibility, broadens adoption across food, pharmaceutical, and consumer goods sectors, and creates new growth avenues for manufacturers worldwide.

Automatic Checkweigher Market Insights and Trends

Product Type Insights

Standalone Systems Lead While Combination Systems Gain Ground

Standalone Systems dominate the market with a commanding 59% market share, representing the traditional foundation of checkweighing technology. These systems offer proven reliability and straightforward integration for manufacturers requiring dedicated weight verification capabilities. Their established presence reflects decades of technological refinement and widespread industry acceptance across food processing, pharmaceutical, and logistics applications.

Combination Systems emerge as the fastest-growing product type, driven by increasing demand for space-efficient, multi-functional inspection solutions. These integrated platforms combine precision weighing with contamination detection capabilities, creating comprehensive critical control points that streamline quality assurance processes. The appeal lies in reduced equipment footprint, lower installation costs, and unified operational interfaces that simplify training requirements and maintenance procedures

Technology Type Insights

Electromagnetic Force Restoration (EMFR) technology leads the market with 55% market share

Electromagnetic Force Restoration (EMFR) technology leads the market with 55% market share, establishing itself as the premium solution for high-speed, high-accuracy applications. EMFR systems achieve settling times significantly faster than strain gauge alternatives, enabling more precise weights at higher production speeds. This technology eliminates reliance on bending metal as the primary measurement mechanism, instead utilizing optical and electronic methodologies that deliver superior repeatability and durability.

Strain Gauge technology represents the fastest-growing segment, driven by cost-effectiveness and proven performance in diverse applications. These systems convert mechanical load into electrical signals through metal deformation, providing accurate real-time measurement with simplified design characteristics. The widespread adoption reflects their suitability for applications where ultra-high speed is not critical, offering excellent value proposition for manufacturers seeking reliable weight verification capabilities.

End Use Industry Insights

Food & Beverages maintains its position as the leading end use industry

Food & Beverages maintains its position as the leading end use industry, accounting for approximately 46.9% of market demand by volume. This dominance reflects stringent food safety regulations, high-volume production requirements, and consumer expectations for consistent product quality. The sector's growth is propelled by expanding global demand for packaged foods, ready-to-eat products, and dairy items that require precise weight verification for regulatory compliance.

Cosmetics and Personal Care emerges as the fastest-growing end-use segment, driven by premium product positioning and increasing quality standards in beauty and personal care manufacturing. This sector's rapid expansion reflects growing consumer sophistication and regulatory requirements for accurate product labeling and packaging consistency. The industry's emphasis on brand reputation and customer satisfaction creates strong demand for precision checkweighing solutions that ensure product consistency and regulatory adherence.

Regional Insights and Trends

North America Leads with Strong Regulations and Technological Advancements

North America is estimated to dominate the global automatic checkweigher market with a 29% market share in 2025, characterized by advanced regulatory frameworks and high automation adoption rates. The United States leads regional growth with FDA compliance requirements driving sophisticated checkweigher deployment across pharmaceutical and food processing sectors. The region benefits from established manufacturing infrastructure, significant R&D investments, and early adoption of Industry 4.0 technologies. Canadian market expansion reflects growing emphasis on quality control automation and export compliance requirements.

Key growth drivers include stringent regulatory standards, advanced production capabilities, and substantial manufacturing expenditure supporting industrial automation initiatives. The region's competitive landscape features major global players investing in innovation and expanding cross-border market presence. Investment trends focus on intelligent checkweighing systems with IoT connectivity and predictive maintenance capabilities.

Europe Advances Through Stringent Regulations and Offshore Developments

Europe commands a significant market share, accounting for 26% of the global market with Germany, U.K., France, and Spain leading regional adoption. The region benefits from EU weight compliance regulations for packaged goods, creating consistent demand across member states. German market leadership reflects strong food and beverage sector demand for automated checkweighing solutions supporting precision packaging targets and sustainability initiatives. Regulatory harmonization under EU Directive 2014/32/EU standardizes accuracy requirements, encouraging premium instrument procurement.

European manufacturers prioritize high-speed checkweighers capable of handling diverse product types with enhanced sensor technologies. The region's emphasis on hygienic design standards, particularly in food processing applications, drives demand for IP69-rated systems with washdown capabilities. Innovation focus centers on modular designs, comprehensive after-sales support, and tailored solutions meeting diverse industry requirements.

Asia Pacific Leads Global Growth with Strong Policy Support and Industrial Expansion

Asia Pacific demonstrates the highest growth potential with projected CAGR of 7.5%, driven by rapid industrialization and expanding manufacturing capacities. China and India lead regional expansion through government initiatives promoting industrial automation and quality standards adoption. The region's manufacturing boom, coupled with growing middle-class consumption patterns, creates substantial demand for quality control automation.

ASEAN countries contribute significantly to growth through expanding food processing and pharmaceutical manufacturing sectors. The region benefits from favorable cost structures, increasing foreign investment, and technology transfer initiatives that accelerate automation adoption. Investment opportunities focus on high-volume production facilities requiring cost-effective, high-accuracy checkweighing solutions.

Automatic Checkweigher Market Competitive Landscape

The automatic checkweighers market is moderately fragmented, with established players holding significant market positions through brand recognition, extensive distribution networks, and technological advancement. Leading companies include Mettler-Toledo International Inc., Ishida Co., Ltd., Wipotec-OCS GmbH, Anritsu Corporation, and Minebea Intec GmbH dominate the global automatic checkweigher market.

These companies emphasize innovation, technological integration, and global expansion as their key strategic themes. They focus on developing smart, IoT-connected devices with predictive maintenance and data analytics capabilities. Cost leadership and modular product offerings are also prioritized to capture emerging markets and niche end-use segments.

Key Industry Developments

- In April 2024, Ishida Europe launched the enhanced DACS-GN checkweigher platform featuring MID approval, improved speed capabilities up to 480 packages per minute, and enhanced weight handling range from 5g to 6kg. The system incorporates advanced electronics, simplified software architecture, and plug-and-play installation capabilities.

- In September 2024, Mettler-Toledo introduced next-generation CM and CX Combination Systems integrating C-Series checkweighers with M30 R-Series metal detectors and X2 Series X-ray systems. These platforms deliver enhanced contamination detection sensitivity while maintaining precision weighing capabilities.

- Antares Vision Group unveiled the HR600 PHC checkweigher at ACHEMA 2024, featuring milligram-level precision for pharmaceutical applications with 21 CFR Part 11 compliance and advanced carton handling capabilities. The system demonstrates autonomous error detection and precise alignment adjustment features.

Companies Covered in Automatic Checkweigher Market

- METTLER TOLEDO

- Ishida Co., Ltd.

- Technofour Electronics Pvt Ltd

- Bizerba

- Yamato Scale

- Anritsu Corporation

- WIPOTEC-OCS

- A&D Company, Limited

- Thermo Fisher Scientific Inc

- Syntegon Technology GmbH

- Minebea Intec

- Pico Automation

- Kenwei

- Infinity Automated Solutions

- Das Electronics

- LOMA SYSTEMS

- MULTIVAC Sepp Haggenmüller SE & Co. KG

- Cardinal / Detecto Scale

- Cassel Messtechnik GmbH

- General Measure

- Precia Molen

Frequently Asked Questions

The global Automatic Checkweigher market is projected to be valued at US$ 494.2 Mn in 2025.

The market is poised to witness a CAGR of 6.5% from 2025 to 2032.

Key growth drivers include increasing regulatory scrutiny in food and pharmaceutical packaging, rising automation adoption for efficiency and quality, and advancements in sensor and AI technology that improve precision and predictive maintenance.

Growing demand for space-efficient solutions drives opportunities for combination systems that integrate checkweighing with metal detection, X-ray inspection, or vision systems.

The consumer products industry is the fastest-growing end-use segment for the automatic checkweigher market, amid rising demand for packaged food.

The top key market players in the global Automatic Checkweigher market include METTLER TOLEDO, Ishida Co., Ltd., Technofour Electronics Pvt. Ltd., Bizerba, Yamato Scale, etc,