- Aerospace & Defense

- Aircraft Filters Market

Aircraft Filters Market Size, Trends, Share, and Growth Forecast, 2026 – 2033

Aircraft Filters Market by Product Type (Air Filters, Fuel Filters, Oil Filters, Others), Application (Engine, Cabin, Hydraulic Systems, Fuel Systems, Pneumatic System, Others), Aircraft Type (Commercial Aircraft, Business Jets, Military Aircraft, Unmanned Aerial Vehicles (UAVs), Helicopters), and Regional Analysis for 2026-2033

Aircraft Filters Market Share and Trends Analysis

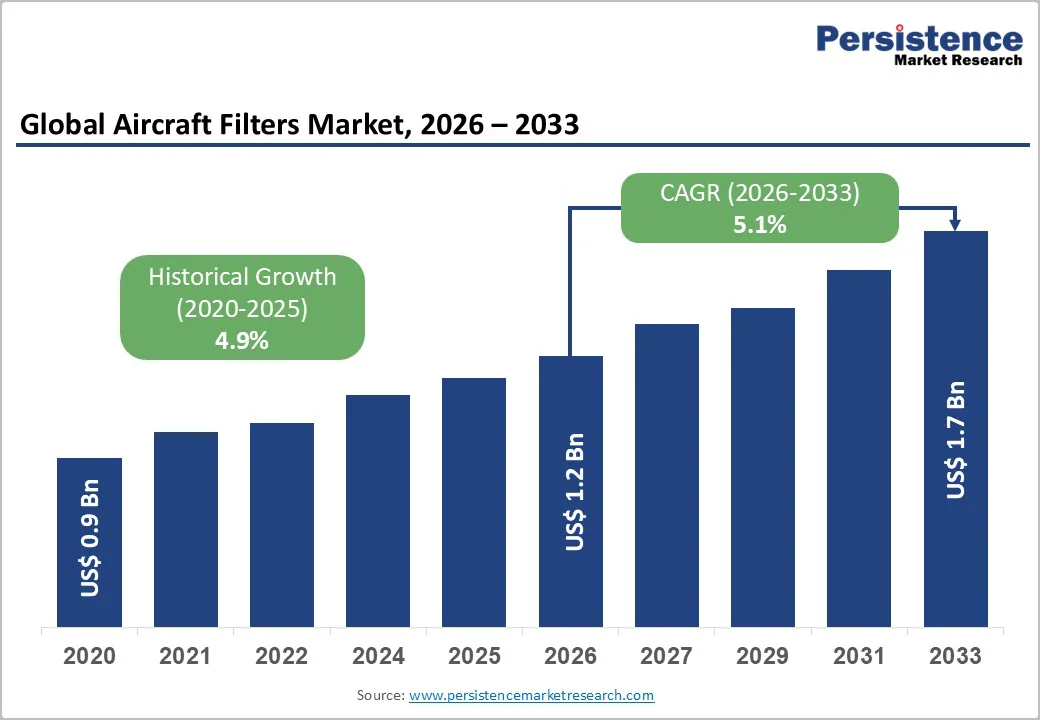

The global aircraft filters market size is likely to be valued at US$ 1.2 billion in 2026, and is estimated to reach US$ 1.7 billion by 2033, growing at a CAGR of 5.1% during the forecast period 2026−2033. Growth is supported by rising fleet modernization programs, increasing aircraft production rates, and stricter aviation safety regulations mandating higher efficiency filtration systems. Additional demand stems from sustained investments in air mobility platforms and rising maintenance, repair, & overhaul (MRO) activities across commercial and defense aviation. The industry benefits from advanced filtration technologies enabling fuel efficiency, component longevity, and compliance with environmental standards.

Key Industry Highlights

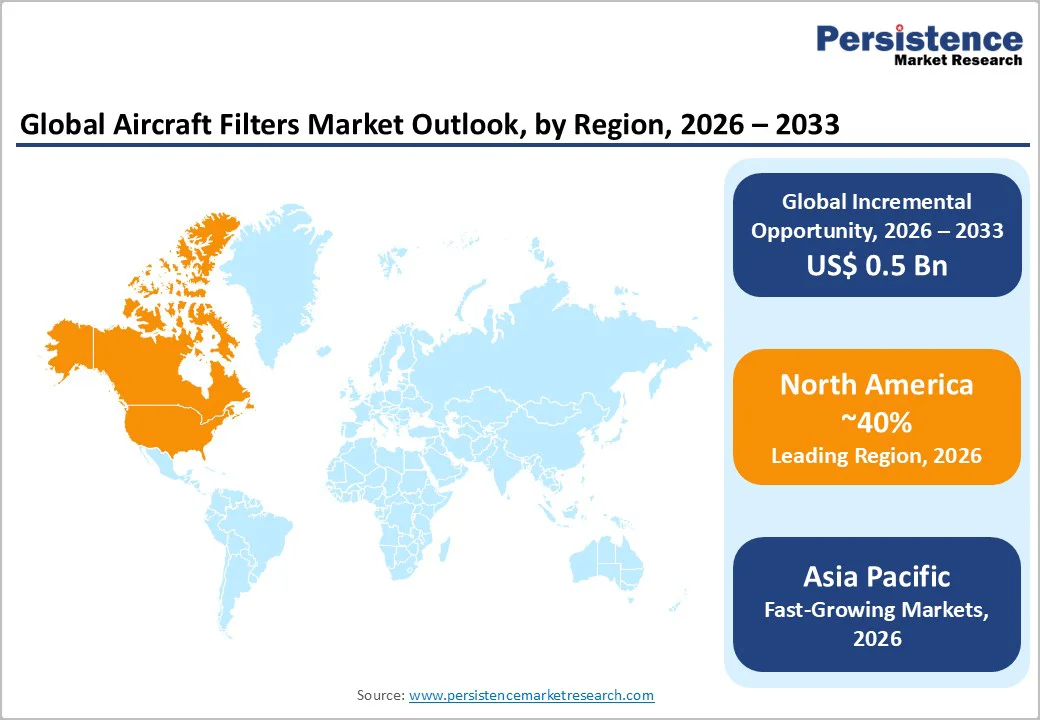

- Dominant Region: North America is projected to lead in 2026 with a 40% share, driven by the presence of major original equipment manufacturers (OEMs) and a mature MRO ecosystem.

- Fastest-growing Market: Asia Pacific is expected to be the fastest-growing market through 2032, fueled by expanding commercial aviation, defense modernization, and next-generation aircraft adoption.

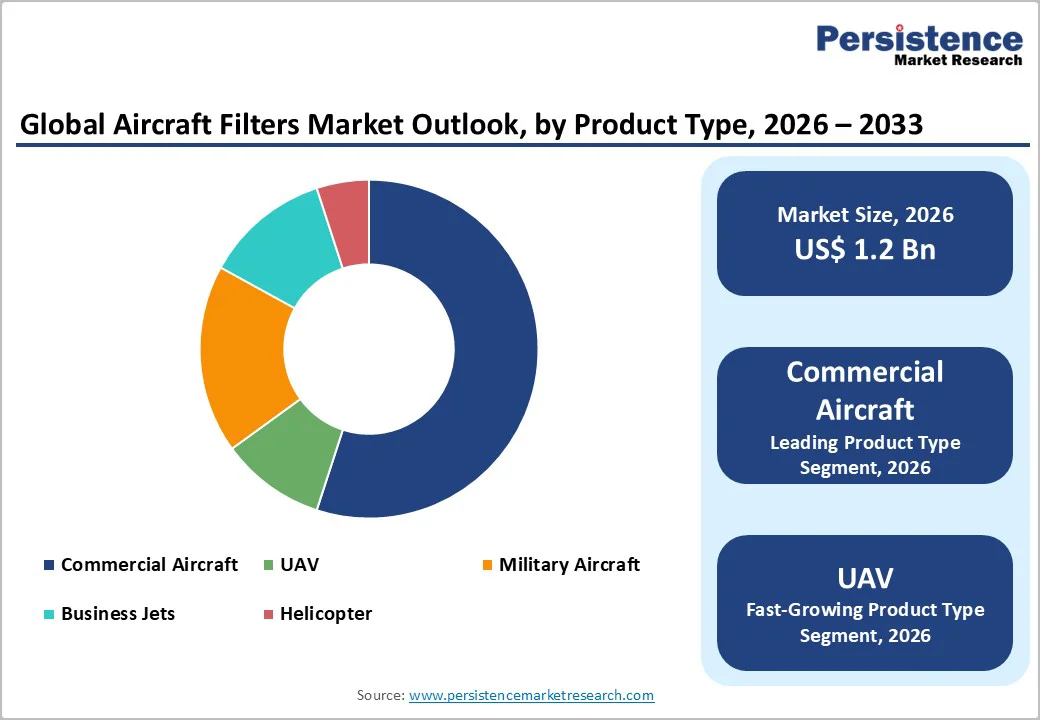

- Leading Product Type: Commercial aircraft are set to dominate with a projected 55% market share in 2026, owing to extensive passenger traffic and complex filtration needs.

- Fastest-growing Product Type: UAVs are poised to be the fastest-growing segment from 2026 to 2033, aided by rising adoption of drones in defense, surveillance, mapping, and commercial operations.

| Key Insights | Details |

|---|---|

| Aircraft Filters Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Air Travel Demand and Aircraft Deliveries

The expansion of air travel demand and aircraft deliveries amplifies filtration requirements across the aerospace sector. As new aircraft enter service, each unit incorporates multiple filtration components, while increased flight hours intensify mechanical stress on engines, hydraulics, fuel systems and cabin environments. This dual dynamic enlarges the initial installation base while simultaneously compressing replacement cycles, creating sustained demand throughout an aircraft's operational lifecycle. Airlines investing in network expansion recognize that system reliability directly impacts operational efficiency and safety margins, establishing filtration as an indispensable element within production workflows, integration processes and maintenance schedules.

The intensification of passenger traffic further necessitates the elevation of performance standards for all aircraft systems, particularly regarding airflow cleanliness, fuel integrity and hydraulic contamination prevention. Heightened operational frequency accelerates both particulate accumulation within engines and fluid degradation across hydraulic networks, necessitating more frequent and rigorous filter replacement intervals to preserve safety protocols and satisfy regulatory obligations. This convergence of fleet expansion and operational intensity creates multifaceted growth pathways across the aerospace filtration ecosystem, strengthening demand trajectories within both OEM supply chains and aftermarket service distribution channels.

High Certification and Development Costs

Stringent certification and development requirements present a formidable constraint within the aerospace filtration sector, as all components must satisfy exacting aviation safety standards established by regulatory bodies. Each product formulation requires comprehensive performance validation, exhaustive environmental endurance testing, and systematic conformity verification across multiple operational scenarios. These mandatory phases necessitate specialized engineering expertise, advanced material compositions, and extended qualification timelines that substantially increase overall development investment. The financial burden becomes particularly acute when filtration units service critical systems such as engines, fuel circuits, hydraulic networks, or pneumatic assemblies, where operational reliability margins remain exceptionally narrow and demand exceptionally high quality assurance.

This rigorous certification landscape creates considerable financial pressure on manufacturers and strongly influences strategic priorities across manufacturing operations and technology innovation initiatives. The elevated cost of regulatory approvals directly influences pricing strategies within both OEM supply channels and aftermarket distribution networks, compelling stakeholders to conduct rigorous lifecycle value assessments for each filtration component. These stringent qualification prerequisites also constrain the commercialization timeline for advanced technologies and establish formidable barriers to entry for emerging suppliers, effectively reducing market flexibility and competitive dynamism. Consequently, the aircraft filters market growth is marred by cost-prohibitive certification frameworks that simultaneously govern technological innovation and determine patterns of supplier participation and competitive positioning.

Lightweight Composites for Next-Gen Aircraft

The adoption of lightweight composites in next-generation aircraft significantly heightens demand for advanced filtration solutions, as these materials enable superior operating efficiency, seamless system integration, and pristine fluid pathways. Composite-based airframes, fuel conduits, and hydraulic assemblies necessitate filtration technologies with exceptional precision to protect performance amid elevated thermal stresses and prolonged service durations. These units must achieve outstanding contaminant capture while adhering to rigorous weight-minimization objectives, spurring development of compact, high-capacity filters tailored for composite-intensive architectures. Manufacturers equipped with such innovations gain a competitive edge by addressing the unique challenges of material compatibility and operational sustainability in modern fleets.

This shift to composite-dominant aircraft architectures fundamentally transforms maintenance protocols, compelling operators to implement filtration systems that preserve long-term structural integrity across diverse applications. Composites exhibit heightened vulnerability to particulate ingress, fluid breakdown, and microscopic contaminants, which opens substantial opportunities for enhanced filtration across engines, cabin environments, fuel distribution networks, and hydraulic circuits. Suppliers offering lightweight filter enclosures, multi-layered filtration media, and superior endurance characteristics position themselves advantageously, as aerospace initiatives emphasize fuel consumption reduction, component longevity extension, and systemic cleanliness optimization. Strategic alignment with these priorities enables filtration providers to capture expanding market share in an era of material innovation and performance-driven design.

Category-wise Analysis

Product Type Insights

Air filters are projected to hold a commanding 42% market share in 2026, reflecting their critical function in managing cabin air quality, protecting engine intake systems, and meeting stringent environmental and safety regulations. Their broad utilization across OEM production and MRO service channels underscores their vital role in ensuring passenger health, regulatory compliance, and overall operational efficiency. This wide adoption guarantees air filters will remain the dominant segment within the aerospace filtration market.

Fuel filters are predicted to represent the fastest-growing segment through 2033, driven by increasingly stringent standards for fuel cleanliness and engine operational performance. Next-generation engines, including advanced turbofan models, emphasize sensitivity to particulate contamination, making fuel filtration essential to achieve cleaner combustion, reduce emissions, and enhance fuel system reliability over extended operating periods. Demand for fuel filters is accelerating in both new aircraft programs and retrofit maintenance initiatives across commercial and military aviation, positioning this segment for sustained expansion alongside evolving engine technologies and regulatory mandates.

Application Insights

Engine applications are anticipated to hold an estimated 37% of the aircraft filters market revenue share in 2026. Their dominance is attributable to the essential function of safeguarding engines from debris and contaminants in demanding high-thrust environments, which is critical for sustaining reliable performance across diverse fleet operations. The use of advanced filtration in engine systems contributes to lengthened maintenance intervals and minimizes operational disruptions, thereby enhancing overall cost efficiency and enabling more strategic allocation of resources in airline operations.

Hydraulic system filtration is expected to post the highest CAGR during 2026-2033, fueled by the widespread adoption of fly-by-wire technology and advanced aircraft architectures. Hydraulic filtration plays a crucial role in preventing fluid leaks, enhancing system efficiency, and facilitating integration with next-generation avionics and control systems. The resulting operational improvements and reduction in maintenance complexities position hydraulic filtration as a strategic priority for aerospace operators aiming to maximize performance reliability and optimize long-term maintenance expenditures.

Aircraft Type Insights

Commercial aircraft dominate the aerospace filtration market with a projected 55% share in 2026, bolstered by substantial production volumes from leading OEMs, surging passenger traffic volumes, and extensive MRO activities. These platforms impose multifaceted filtration demands across engines, cabin environments, hydraulic networks, and pneumatic systems, generating consistent recurring revenue streams for suppliers. The robust growth trajectory of flagship OEM programs guarantees elevated installation rates and underscores the pivotal role of filtration in upholding operational reliability and fleet scalability for airlines worldwide.

Unmanned aerial vehicles are slated to emerge as the fastest-expanding segment from 2026 to 2033, with their demand poised to spike for defense missions, surveillance applications, mapping initiatives, and commercial deployments. These versatile platforms necessitate compact filtration solutions engineered for exceptional tolerance against dust ingress, thermal extremes, and mission-critical contaminants. This surge aligns with escalating operational deployments, escalating system sophistication, and the pursuit of lightweight, high-performance technologies, establishing UAV filtration as a prime opportunity for suppliers targeting diversified aviation growth corridors.

Regional Insights

North America Aircraft Filters Market Trends

North America is projected to dominate in 2026 with an estimated 40% of the aircraft filters market share. The region’s leadership stems from its concentration of major commercial and defense aircraft manufacturers, including both OEMs and Tier-1 suppliers, which drives consistent high-volume filter requirements across new aircraft production. Stringent regulatory frameworks governing engine performance, cabin air quality, and hydraulic system reliability necessitate advanced, high-efficiency filtration solutions, creating a sustained demand environment. The region’s mature MRO ecosystem ensures recurring aftermarket consumption, reinforcing the continuous adoption of replacement and upgrade filters across fleet operations.

Another key factor underpinning North America’s dominance is its technological leadership in next-generation aircraft platforms. The widespread integration of composite airframes, fly-by-wire systems, and high-bypass turbofan engines increases reliance on precision filtration for engine intake, hydraulic actuation, fuel management, and environmental control systems. Anticipated growth in defense modernization programs further strengthens demand, as UAVs, fighter jets, and transport aircraft require compact, high-tolerance filters. These factors have created a sophisticated market where high-value filtration solutions are both essential and strategically prioritized, sustaining North America’s prime position.

Europe Aircraft Filters Market Trends

Europe continues to be a prominent player in the aircraft filters market, propelled by its commitment to sustainable aviation technologies and comprehensive fleet modernization efforts. The region leads advancements in lightweight composite airframes and hybrid-electric propulsion systems, which elevate the need for highly precise, compact filtration solutions across critical components such as engines, hydraulics, and fuel delivery systems. Increasing regulatory mandates targeting particulate emissions and cabin air quality further drive the adoption of high-efficiency filters that meet stringent operational requirements, creating a market landscape characterized by differentiated demand for cutting-edge filtration technologies.

A distinguishing feature of the Europe market is its emphasis on innovation-driven MRO strategies. Predictive maintenance frameworks and sensor-enabled filtration monitoring empower operators to fine-tune filter replacement schedules, minimize unplanned operational disruptions, and prolong component lifespan. Expansion in specialized aircraft sectors, including urban air mobility and UAVs for research purposes, fosters demand for filtration systems designed to withstand thermal stresses, vibration, and contamination in complex operating environments. This blend of sustainability focus, technological innovation, and data-centric maintenance establishes Europe as a strategically advanced and innovation-focused region within the global aircraft filters market.

Asia Pacific Aircraft Filters Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for aircraft filters, stimulated by accelerated commercial aviation expansion, defense sector modernization, and widespread adoption of next-generation aircraft platforms. Surging fleet deliveries from regional manufacturers, coupled with escalating airline passenger traffic, generate robust demand for filtration systems serving engines, hydraulics, fuel circuits, and cabin environments. Concurrent development of MRO infrastructure further intensifies recurring needs for filter replacements and technological upgrades, establishing a foundation for enduring market momentum.

Several strategic elements underpin this trajectory, including substantial investments in civil aviation infrastructure by emerging economies, heightened emphasis on operational efficiency, and integration of advanced turbofan engines alongside fly-by-wire control architectures. The proliferation of UAVs in surveillance, logistics, and commercial roles demands compact, precision-engineered filtration to manage mission-specific contaminants and environmental stresses. Government-led initiatives aimed at elevating aviation safety protocols and environmental standards amplify these opportunities, positioning Asia Pacific as a dynamic, high-potential market that rewards suppliers delivering lightweight, high-performance filtration innovations.

Competitive Landscape

The global aircraft filters market structure demonstrates moderate consolidation, where leading companies command approximately 55% of the total share through their mastery of sophisticated filtration technologies such as multi-layer media, high-temperature hydraulic filters, and precision-engineered fuel filtration systems. These established players strengthen their market leadership via strategic partnerships with OEMs to embed solutions into upcoming aircraft platforms, while their proven regulatory compliance and certification expertise erect substantial barriers against new market entrants. This positioning enables sustained dominance amid evolving industry standards and performance requirements.

Emerging and smaller suppliers carve out competitive niches by delivering specialized products, including lightweight filters optimized for UAVs, adaptive cabin air purification systems, and components tailored for hybrid-electric or sustainable aviation architectures. Their operational agility facilitates swift adaptation to shifting aircraft configurations and diverse regional regulatory frameworks, fostering innovation in response to niche demands.

Key Industry Developments

- In November 2025, Parker Hannifin announced it would acquire air and liquid filtration systems manufacturer Filtration Group from Madison Industries for US$ 9.25 billion. The move is aimed at expanding Parker’s footprint in the aftermarket filtration business, strengthening its capabilities across aerospace, industrial, and defense applications, and enhancing its global supply chain for high-performance filtration solutions.

- In November 2025, Satair renewed its exclusive worldwide distribution agreement with Pall Corporation through 2032, continuing to supply Pall's advanced filter elements and assemblies for air, hydraulic, water, and engine systems in commercial aviation aftermarket. This partnership, established since 1991, emphasizes innovation, reliability, and technical support for airlines and MROs, with both companies exploring new product development.

In July 2025, General Atomics announced that it would accelerate the delivery of a European Collaborative Combat Aircraft (CCA) by combining its U.S. and German aerospace operations. The aircraft, based on a proven U.S. platform and assembled in Europe with European mission systems, aims to strengthen transatlantic defense collaboration and enhance rapid deployment capabilities.

Companies Covered in Aircraft Filters Market

- Parker Hannifin Corporation

- Donaldson Company, Inc.

- Safran Filtration Systems

- Rheinmetall AG

- Eaton Corporation

- Porvair plc

- Collins Aerospace

- Honeywell International Inc.

- ITT Aerospace

- Clarcor Aerospace

- Meggitt PLC

- Holschman Aviation

- UFI Filters Group

Frequently Asked Questions

The global aircraft filters market is projected to reach US$ 1.2 billion in 2026.

Rising global air traffic, stringent safety and emission regulations, and increasing demand for advanced aircraft filtration systems are driving the market.

The market is poised to witness a CAGR of 5.1% from 2026 to 2033.

Growing adoption of next-generation aircraft, UAVs, and lightweight filtration technologies is likely to open up multiple lucrative market opportunities.

Some of the key market players include Parker Hannifin Corporation, Donaldson Company, Inc., Safran Filtration Systems, Rheinmetall AG, and Eaton Corporation.