- Technology

- AI Consulting Services Market

AI Consulting Services Market Size, Share, and Growth Forecast, 2026 - 2033

AI Consulting Services Market by Service Type (Strategy & Advisory, Implementation & Deployment, Managed Services, Training & Change Management, Analytics & Insights, Automation Consulting, Auditing, Compliance & Risk Advisory, Others), Technology (Machine Learning, Natural Language Processing, Computer Vision, Generative AI, Robotic Process Automation, Others), Enterprise Size, Industry and Regional Analysis for 2026 - 2033

AI Consulting Services Market Size and Trends

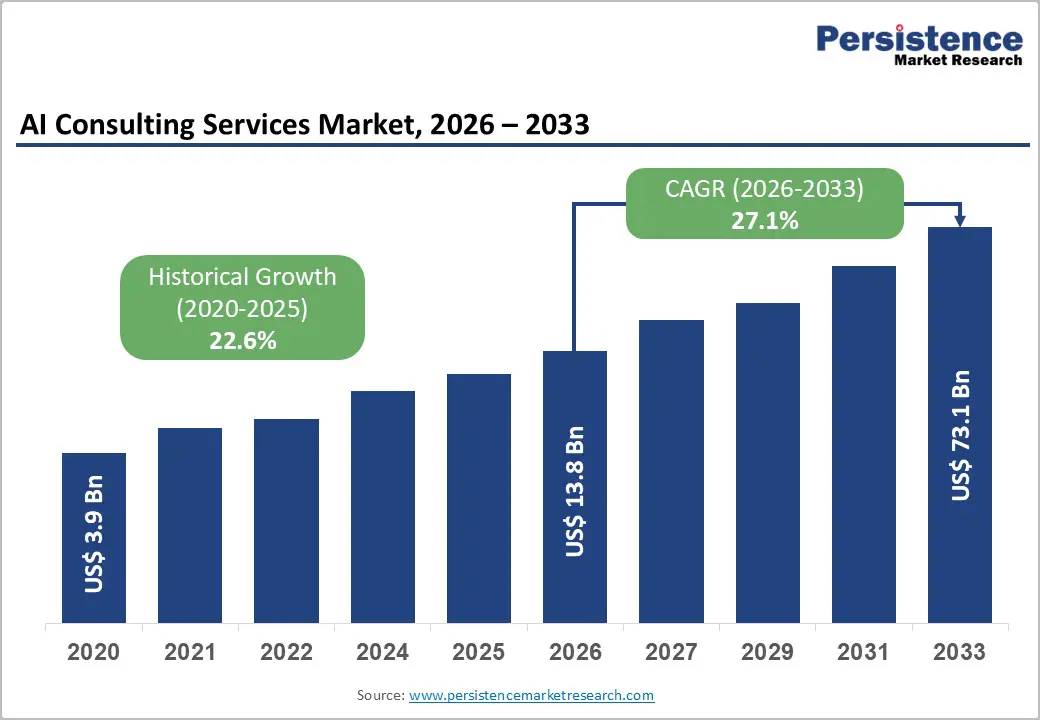

The global AI consulting services market size is projected to rise from US$13.8 billion n 2026 to US$73.1 billion by 2033, growing at a CAGR of 27.1% during the forecast period from 2026 to 2033, driven by widespread enterprise digital transformation initiatives and the rapid adoption of generative artificial intelligence across industries.

Over 70% of global businesses are either actively utilizing or planning to integrate AI into their operations, creating substantial demand for specialized consulting expertise. The heightened emphasis on ethical AI deployment, combined with stringent regulatory frameworks such as the EU AI Act and evolving data privacy requirements, is further increasing demand for consulting services.

Key Industry Highlights:

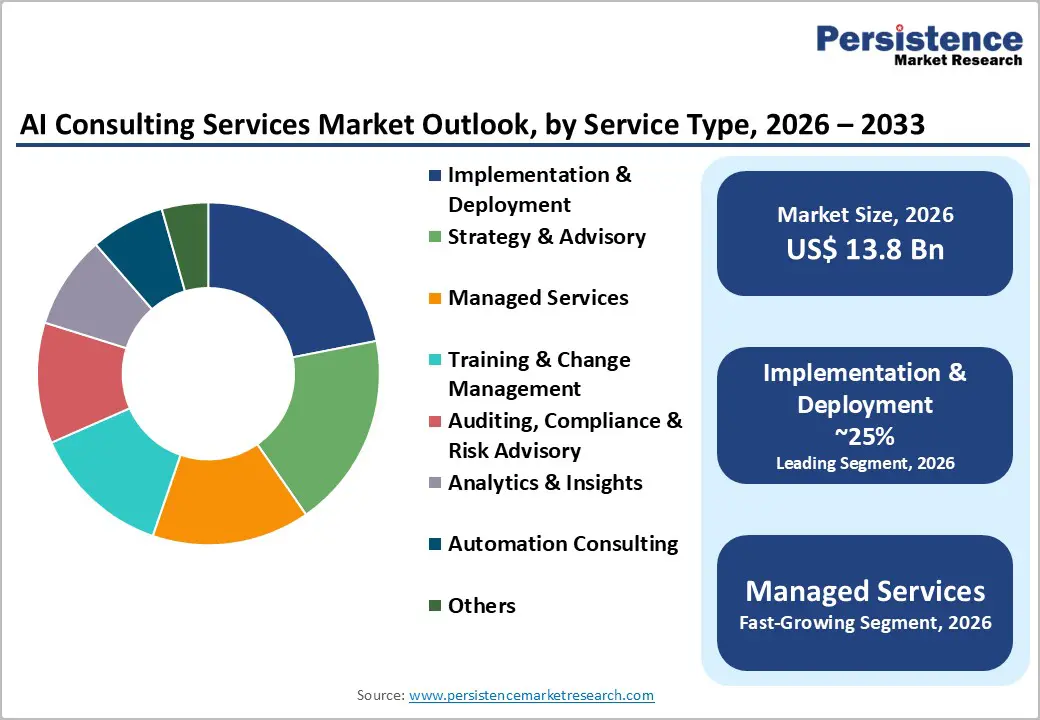

- Leading Service Type: Implementation & Deployment leads the market with over 25% share in 2026, valued at more than US$ 3.5 Bn, driven by the need to customize models, integrate with legacy systems, ensure governance, and achieve measurable business outcomes. Managed Services are the fastest-growing segment at a 31.6% CAGR, supported by the lack of in-house AI talent and the need for continuous monitoring, optimization, security, and compliance.

- Leading Technology: Machine Learning (ML) dominates with over 31% market share in 2026, exceeding US$ 4.3 Bn, due to its ability to deliver immediate, data-driven business value across forecasting, risk detection, and operational optimization. Generative AI is the fastest-growing technology at a 33.4% CAGR, driven by strong enterprise demand for productivity gains, customer experience transformation, and rapid deployment of AI-powered assistants, content generation, and decision-support systems.

- Leading Enterprise Size: Large Enterprises account for more than 72% of market share in 2026, valued at above US$ 9.9 Bn, due to complex operations, large data volumes, regulatory exposure, and strong budgets for enterprise-wide AI transformation. SMEs are the fastest-growing segment at a 32.8% CAGR, as they increasingly adopt AI consulting to access scalable, cost-effective automation and analytics solutions without heavy upfront investments.

- Leading Industry: IT & Telecom holds the largest share at over 22% in 2026, valued at more than US$ 3.0 Bn, driven by the need for network optimization, predictive maintenance, real-time analytics, and customer experience personalization. BFSI is the fastest-growing at a 30.6% CAGR, fueled by fraud prevention needs, regulatory compliance, process automation, and competitive pressure from fintech and digital-native players.

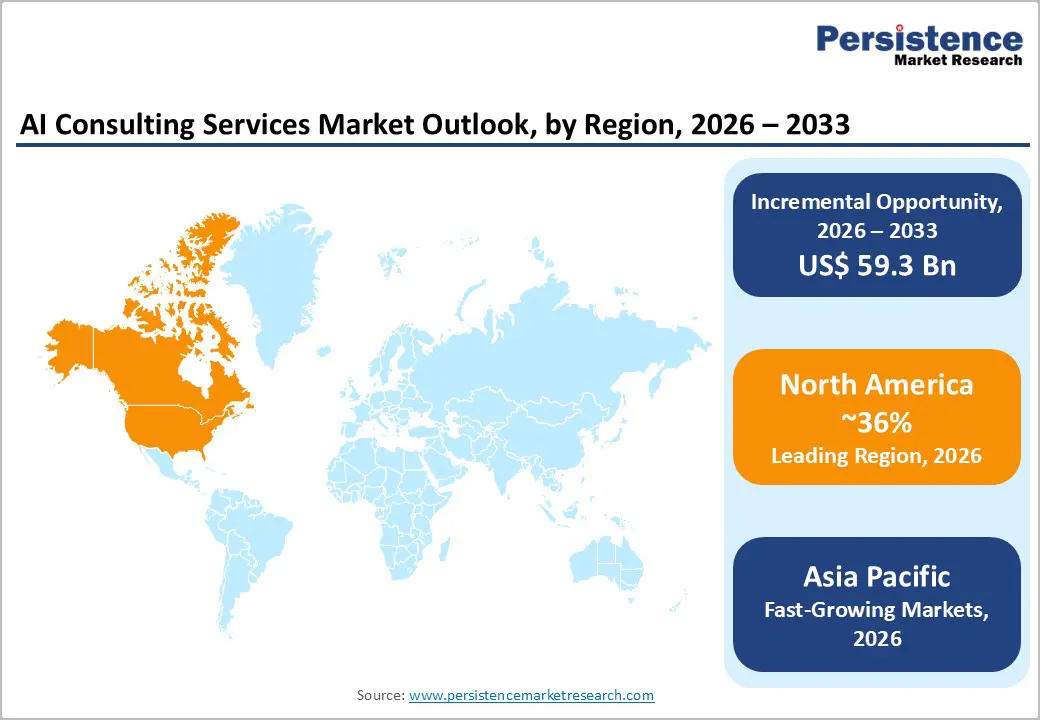

- Leading Region: North America leads the global market with over 36% share in 2026, reaching approximately US$ 5.0 Bn, supported by early AI adoption, a mature consulting ecosystem, and strong regulatory and governance requirements. Asia-Pacific is the fastest-growing region, with a 34.1% CAGR, driven by aggressive government AI initiatives, rapid enterprise digitalization, and large talent pools in China, India, Japan, and South Korea.

| Key Insights | Details |

|---|---|

| AI Consulting Services Market Size (2026E) | US$13.8 Bn |

| Market Value Forecast (2033F) | US$73.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 27.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 22.6% |

Market Dynamics

Driver - Regulatory Compliance and Risk Governance Requirements

Regulatory frameworks worldwide are pushing organizations to seek specialized AI consulting for compliant and responsible deployment. The EU AI Act entered into force in August 2024, with key provisions including transparency and risk-management obligations for general-purpose AI becoming applicable from February 2025 and August 2025, and further requirements phased through 2026. Non-compliance results in fines up to €35 million or 7% of global turnover. Government initiatives such as India’s AI ecosystem investments and China’s New Generation AI Development Plan are accelerating AI adoption, increasing demand for regulatory alignment, ethical frameworks, and guidance on responsible innovation.

Data & Infrastructure Challenges and Pressure to Modernize Legacy Systems

Data and infrastructure challenges are pushing organizations to seek AI consulting services, as many enterprises still run on legacy systems that are not designed for modern AI workloads. These outdated systems struggle with fragmented data, slow processing, and limited integration capabilities, making it difficult to deploy AI at scale. As data volumes grow exponentially, companies face pressure to modernize infrastructure for real-time analytics, cloud migration, and AI-ready platforms. With rising competition, businesses are increasingly prioritizing AI-driven decision-making, forcing them to upgrade legacy IT stacks quickly.

Restraint - Infrastructure Limitations and Digital Divide in Emerging Markets

Many parts of the Asia-Pacific, Latin America, and Africa face significant infrastructure constraints that limit the growth of AI consulting services. Limited digital connectivity, uneven cloud infrastructure, and insufficient data center capacity hinder AI adoption, especially among SMEs and mid-market companies. These gaps raise the cost and complexity of implementing AI solutions, making it difficult for businesses to access advanced technologies. A shortage of local AI expertise and qualified consultants reduces market momentum, as organizations struggle to find partners with the necessary technical depth and industry knowledge. The addressable market remains constrained despite strong digital transformation mandates across these regions.

Data Privacy Concerns and Organizational Risk Aversion

Enterprises, especially financial institutions handling sensitive customer data, are cautious about AI adoption due to concerns about data breaches, algorithmic bias, and operational disruptions that could lead to reputational damage, regulatory penalties, and loss of customer trust. This risk-averse mindset is intensified by the high costs of AI consulting engagements, which range from hundreds of thousands to several million dollars, depending on scope. Cost-conscious SMEs and organizations with legacy IT infrastructure often delay AI investments, preferring incremental technology upgrades over transformative AI initiatives.

Opportunity - Convergence of Generative AI and Robotic Process Automation for Intelligent Automation

The convergence of generative AI and Robotic Process Automation (RPA) is rapidly reshaping intelligent automation, enabling organizations to automate complex, multi-step workflows with high adaptability and minimal human intervention. GenAI-enhanced RPA reduces processing times by 60-80% for sophisticated tasks by handling exceptions, unstructured data, and process variations more effectively. AI consulting firms capture significant value by helping enterprises redesign processes, reduce manual reviews, and redeploy human talent to strategic work. This creates a major growth opportunity across manufacturing supply chain optimization, financial services automation, and HR process transformation, positioning intelligent automation as a high-impact, fast-growing service area.

Cloud & Edge AI Adoption and AI-as-a-Service Adoption

Cloud and edge AI adoption is expanding the footprint of AI across industries, creating new demand for consulting services that help organizations design and right-size hybrid AI architectures. Enterprises need expert guidance to decide what workloads belong in the cloud versus on edge devices, ensuring performance, latency, and cost targets are met. This shift also drives demand for AI consulting services in areas such as edge model optimization, deployment pipelines, device security, and real-time analytics. The rise of AI-as-a-Service and AI platforms is lowering the barrier to entry for AI adoption, encouraging more organizations to start AI initiatives. As companies move from experimentation to production, consultants are needed for model monitoring, MLOps, and enterprise-wide rollout strategies.

Category-wise Analysis

Service Type Insights

Implementation & Deployment dominates the global market, capturing more than 25% market share in 2026 with a value exceeding US$ 3.5 Bn, due to most organizations now moving beyond pilot AI projects and need hands-on support to integrate AI into real business systems and workflows. Firms require expertise to customize models, ensure compatibility with existing IT infrastructure, and manage change across teams. Effective deployment also demands robust testing, governance, and performance optimization, making consulting essential. Many companies lack in-house expertise to operate AI at scale, driving high demand.

Managed Services demonstrate a significant rate at 31.6% CAGR due to a lack of in-house AI talent and the need for continuous support to build, deploy, and scale AI solutions. Businesses prefer outsourcing operational tasks like model monitoring, performance tuning, and infrastructure management to avoid hiring specialized teams. As AI moves from pilot to production, companies need ongoing governance, security, and compliance services that managed providers deliver efficiently. The complexity of AI ecosystems makes managed services the most practical means of ensuring reliable, long-term value from AI investments.

Technology Insights

Machine Learning (ML) is projected to hold over 31% market share in 2026, with a value exceeding US$ 4.3 Bn, as enterprises require practical, data-driven solutions that are deployed quickly and scaled across operations. Organizations already generate large volumes of structured and unstructured data, and ML directly converts this data into predictive insights for cost reduction, demand forecasting, risk detection, and personalization. ML integrates smoothly with existing IT systems and cloud platforms, reducing implementation risk. Consulting demand is therefore highest for ML model development, customization, integration, and lifecycle management aligned to clear business outcomes.

Generative AI is expected to grow at the highest rate, with a CAGR of 33.4%, due to businesses urgently needing help turning powerful models into real, revenue-driving solutions. Many companies lack in-house expertise in selecting appropriate models, building secure deployments, and integrating them into workflows, so they rely on consultants for rapid, practical implementation. The rapid innovation in GenAI tools creates constant demand for training, customization, and governance support. The high impact on productivity and customer experience makes GenAI projects a top priority, driving accelerated consulting spend.

Enterprise Size Insights

Large Enterprises command the largest market share at over 72% in 2026, with a value exceeding US$9.9 Bn, owing to complex, large-scale operations that require specialized AI expertise to modernize legacy systems and integrate AI across multiple business functions. They also have substantial budgets to invest in AI programs from pilot to production, advanced data infrastructure, and high-quality talent. They face strong competitive pressure and regulatory requirements that drive them to adopt AI to enhance efficiency, manage risk, and personalize customer experiences. Their vast data volumes create a strong need for expert consulting to extract value, ensure governance, and scale AI safely.

Small & Medium Enterprises (SMEs) are expected to grow at a CAGR of 32.8% as they are increasingly under pressure to stay competitive while operating with limited in-house AI expertise. They require rapid, cost-effective access to AI solutions that improve customer experience, automate routine tasks, and optimize operations without substantial upfront investment. AI consulting helps them implement scalable tools like chatbots, predictive analytics, and process automation tailored to their specific business context.

Industry Insights

IT & Telecom command the largest market share at over 22% in 2026, with a value exceeding US$ 3.0 Bn, due to these industries are under constant pressure to modernize networks, improve customer experience, and support massive data growth. They need AI to automate network operations, predict faults, and optimize bandwidth in real time. Telecom companies are increasingly adopting AI for customer analytics, personalized offers, and fraud detection, creating high demand for expert consulting. Given complex legacy systems and high scalability requirements, AI consulting is essential for successful implementation and measurable ROI.

BFSI is expected to grow at a CAGR of 30.6% due to financial institutions facing intense pressure to improve customer experience, reduce fraud, and comply with evolving regulations. Banks and insurers also require AI to automate back-office processes and improve operational efficiency, thereby reducing costs and turnaround times. Competitive pressure from fintech and digital-only banks forces BFSI players to rapidly adopt AI-driven personalization and real-time decisioning. The massive volume of transactions and customer data in BFSI creates a strong demand for AI expertise to unlock value and drive innovation.

Regional Insights

North America AI Consulting Services Market Trends

North America holds over 36% share in 2026, reaching US$ 5.0 Bn value, due to its mature technology ecosystem and early adoption of AI across industries. The region’s strong concentration of top consulting firms, world-class research institutions, and abundant venture capital fuels continuous innovation and demand for specialized advisory services. Enterprises benefit from a deep talent pool in major metropolitan hubs, enabling faster deployment of AI solutions. Established regulatory frameworks around data privacy and algorithmic transparency drive sophisticated consulting needs as organizations strive to balance innovation with compliance.

Asia Pacific AI Consulting Services Market Trends

Asia-Pacific is expected to grow at the highest rate, with a CAGR of 34.1%, driven by rapid enterprise digitalization, strong government support for AI initiatives, and large talent pools that enable scalable consulting delivery. China leads the market with major government-led AI programs, heavy enterprise adoption, and a dense concentration of technology companies building advanced AI capabilities. India is emerging as a major growth hub, supported by government investment in AI-driven manufacturing, a fast-expanding digital economy, and its role as a global delivery center for AI consulting. Japan and South Korea are focusing on AI ethics, governance, robotics innovation, and industrial automation, positioning themselves as specialized consulting centers for advanced manufacturing and autonomous systems.

Europe AI Consulting Services Market Trends

Europe is expected to hold more than 23% share by 2026, driven by strong industrial automation and digital transformation needs. The enforcement of the EU AI Act has significantly increased demand for consulting services as organizations prepare for compliance. Germany, the UK, and France are leading adopters, especially in manufacturing, healthcare, and financial services. European clients prioritize consulting support for GDPR compliance, algorithmic transparency, responsible AI governance, and ethical frameworks. Consultants in the region are highly valued for their expertise in navigating regulatory and compliance requirements. Demand is particularly strong for Industry 4.0 initiatives, healthcare automation, and finance transformation.

Competitive Landscape

The AI consulting services market is fragmented, with many global and regional players competing across industry verticals. Companies typically differentiate through industry-specific AI use cases, proprietary frameworks, and deep domain expertise to win long-term enterprise contracts. They also build partner ecosystems with cloud hyperscalers, software vendors, and data platform providers to strengthen delivery capabilities and reduce implementation risks. Many firms compete on end-to-end services from strategy and data engineering to model deployment and managed AI operations to capture higher-value engagements.

Key Industry Developments:

- In June 2025, Accenture announced a new growth model effective September 1, 2025, by consolidating its Strategy, Consulting, Song, Technology, and Operations services into a single integrated business unit called Reinvention Services, led by Manish Sharma as Chief Services Officer. The company will continue to operate through its three geographic markets while focusing on faster Gen AI-led transformation for clients, with several leadership changes across the Americas and global operations.

- In March 2025, PwC launched PwC’s agent OS, an enterprise AI command center that connects and orchestrates intelligent agents across platforms and business systems, enabling faster, scalable AI workflows. The platform supports in-house and third-party AI agents, offers drag-and-drop workflow creation, and enhances governance and compliance for enterprise-wide AI adoption.

Companies Covered in AI Consulting Services Market

- Accenture

- Deloitte

- McKinsey & Company

- Boston Consulting Group

- IBM

- PwC

- Capgemini

- Infosys

- Tata Consultancy Services (TCS)

- Cognizant

- Wipro

- KPMG

- Prismetric

- Others

Frequently Asked Questions

The global AI consulting services market is projected to be valued at US$13.8 Bn in 2026.

Enterprises needing expert guidance to identify high-value AI use cases, integrate AI into legacy systems, and scale models securely and compliantly to achieve measurable business outcomes, are key drivers of the market.

The AI consulting services market is expected to witness a CAGR of 27.1% from 2026 to 2033.

Convergence of generative AI and robotic process automation (RPA) for intelligent automation is creating strong growth opportunities.

Accenture, Deloitte, McKinsey & Company, Boston Consulting Group, IBM, PwC, and Capgemini are among the leading key players.