- Automotive Components & Materials

- AC Hose Market

AC Hose Market Size, Share, and Growth Forecast, 2026 – 2033

AC Hose Market by Product Type (Rubber, Plastic, Metal, Composite), Diameter (Less than 1 Inch, 1 to 2 Inches, 2 to 3 Inches, More than 3 Inches), Application (Automotive, Industrial, Commercial HVAC, Residential HVAC), and Regional Analysis for 2026-2033

AC Hose Market Share and Trends Analysis

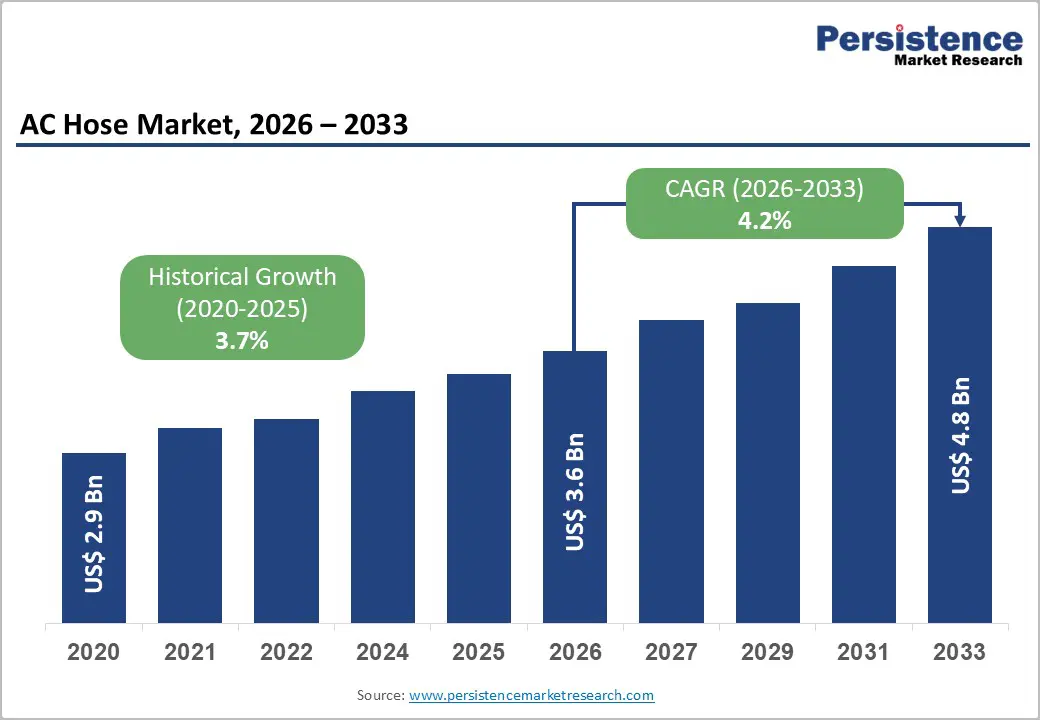

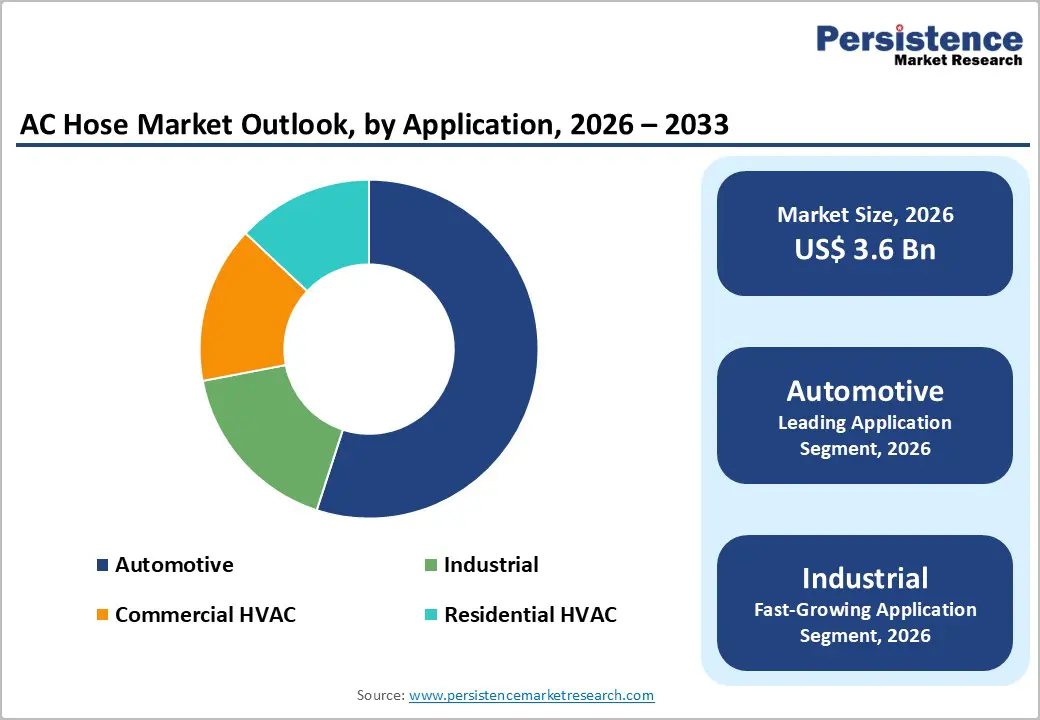

The global AC hose market size is likely to be valued at US$ 3.6 billion in 2026, and is projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033.

Growth is primarily driven by rising demand for air conditioning systems in the automotive and industrial sectors, attributable to expanding vehicle production, urbanization, and infrastructure development. The increasing adoption of electric vehicles (EVs) and hybrid electric vehicles (HEVs) necessitates lightweight, durable, and thermally efficient air-conditioning hoses to enhance system performance and energy efficiency. Technological advancements in materials, including high-temperature rubber, reinforced composites, and corrosion-resistant alloys, enhance reliability and extend service life, thereby fostering broader market adoption. Stringent regulations governing refrigerant containment, emissions reduction, and energy efficiency compel manufacturers to upgrade hose designs, thereby stimulating demand for advanced solutions. Expanding industrial heating, ventilation, and air conditioning (HVAC) installations in emerging markets, combined with growth in residential and commercial construction, further contributes to market growth. Investment in automated manufacturing processes and global supply chain optimization enhances production scalability, reducing costs and supporting wider accessibility.

Key Industry Highlights

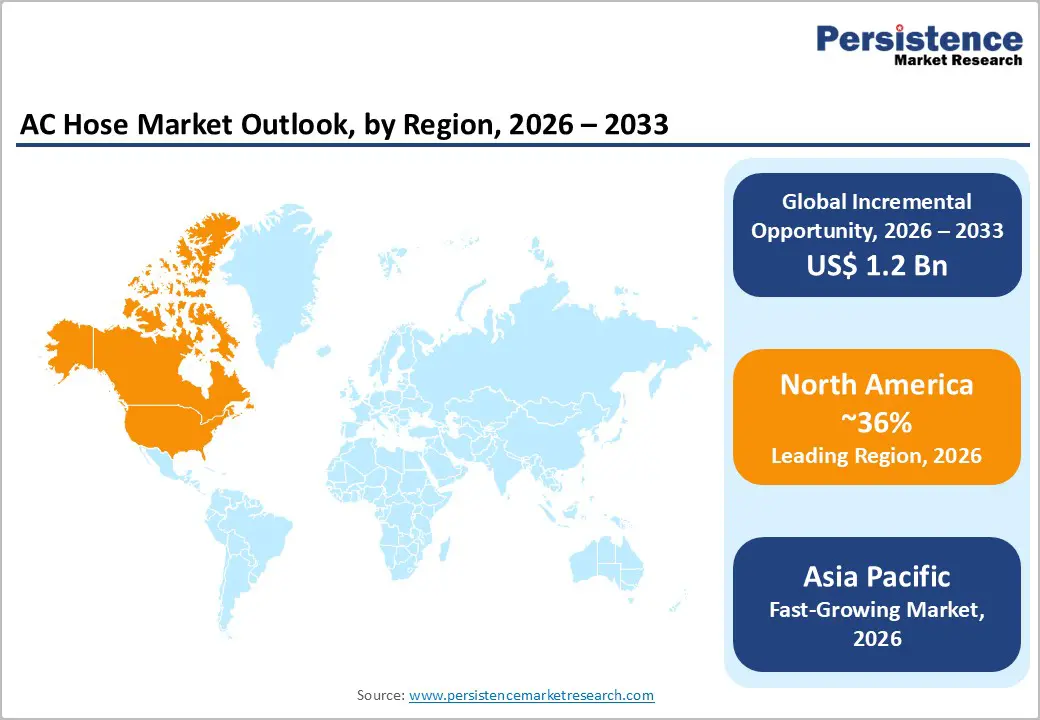

- Dominant Region: North America is expected to hold around 36% share in 2026, fueled by advanced automotive manufacturing and well-established industrial HVAC infrastructure.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing market through 2033, driven by the widening adoption of electrified powertrains, and expanding industrial HVAC installations.

- Leading Application: The automotive segment is expected to account for around 55% revenue share in 2026, owing to soaring vehicle production, air conditioning integration, and electrification trends.

- Fastest-growing Application: Industrial applications are likely to register the highest 2026-2033 CAGR, aided by the proliferation of factories and commercial complexes.

| Key Insights | Details |

|---|---|

| AC Hose Market Size (2026E) | US$ 3.6 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Vehicle Production and Electrification

High levels of vehicle production and the widespread shift to electrified mobility are central to accelerating demand for components that support thermal management in modern vehicles. Total vehicle production drives volume requirements for all supporting systems. As global automotive manufacturing scales, more units require efficient heating and cooling subsystems to maintain cabin comfort and protect powertrain components under varying load cycles and environmental conditions. EVs and other electrified powertrains generate heat differently from traditional internal-combustion-engine vehicles, so thermal pathways must be optimized to maintain battery temperature and power-electronics performance under sustained use. As EV market penetration rises, the aggregate number of vehicles requiring advanced thermal solutions increases at a rate disproportionate to that of traditional platforms, thereby expanding baseline demand for high-performance fluid-transfer and heat-dissipation components.

Growth in electrified-vehicle adoption also redefines the technical requirements for thermal-management infrastructure. Data from India’s Ministry of Road Transport and Highways (MoRTH) indicate that 56.75 lakh EVs were registered in the country by February 2025, reflecting strong uptake supported by government policy and infrastructure investment that are pushing the sector toward electrification targets. Higher EV penetration increases demand for components engineered for enhanced reliability, extended duty cycles, and tighter integration with battery and power-electronics cooling systems. Vehicle electrification programs enacted by governments tighten performance and regulatory criteria for thermal management hardware, necessitating innovation in materials and manufacturing.

Industrial HVAC Expansion and Construction Growth

Rapid expansion in industrial HVAC installations and robust construction activity underpin demand for essential components, including hoses, fittings, and thermal management systems. Growth in industrial infrastructure drives the construction of new and upgraded facilities that require advanced climate-control solutions to maintain operational integrity, worker comfort, and compliance with environmental standards. Industrial facilities encompass manufacturing plants, warehouses, data centers, and processing units where consistent temperature and air quality control are vital for productivity, safety, and equipment performance. As construction output expands, the volume of built space requiring HVAC systems increases proportionally, thereby increasing the demand for distribution networks, piping, hoses, and connectors that form the backbone of these systems.

Industrial HVAC installations also play a strategic role in modern construction projects where energy efficiency, indoor air quality, and sustainable design norms are prioritized. New buildings are increasingly designed with integrated climate control systems to meet regulatory requirements for energy performance and occupant health, leading to escalated specification of HVAC subsystems at the design stage. By elevating the total addressable base of installations, construction expansion ensures sustained procurement of hoses that are engineered for durability, thermal resilience, and compatibility with evolving refrigerants and materials.

Complex Manufacturing Requirements

The manufacturing of automotive air conditioning hoses involves precision engineering across multiple stages, including extrusion, reinforcement, curing, assembly, and rigorous quality validation. These hoses must meet tight tolerances, withstand high pressure, temperature variability, and reliably contain refrigerants with minimal leakage. Achieving such stringent specifications requires specialized tooling, advanced automated production lines, high-precision inspection equipment, and a highly trained workforce. Complex production flows introduce vulnerability to disruption; even slight deviations in material properties, dimensional tolerances, or curing cycles can cause product rejection, rework costs, and delays in vehicle assembly. The reliance on multiple high-specification raw materials, such as synthetic elastomers, multilayer composites, and corrosion-resistant metals, amplifies production complexity, as suppliers must synchronize deliveries and quality standards across global value chains.

This complexity also amplifies supply chain fragility. High-precision manufacturing systems are sensitive to tooling downtime, workforce shortages, and component supply fluctuations, which can have ripple effects on overall production schedules. Regulatory expectations for performance, lifecycle reliability, and compatibility with evolving refrigerant chemistries add further layers of process qualification and testing, extending development cycles. In regions where manufacturing infrastructure and skilled labor are less developed, bridging these gaps demands time-intensive training and capital upgrades.

Fluctuating Raw Material Availability

Inconsistencies in supply of critical inputs, such as engineered polymers, elastomers, and metals, directly undermine production stability. Many base materials originate from a limited number of global suppliers, thereby concentrating risk in specific regions. Government-imposed export restrictions, trade regulations, and fluctuations in the availability of petrochemical derivatives disrupt the steady flow of essential feedstocks. Such disruptions result in intermittent availability and delay component fabrication. Price unpredictability arises when supply channels tighten, forcing manufacturers to reallocate budgets toward alternative sources or buffer inventories. Cost pressure travels downstream, reducing margin flexibility and compressing forecast accuracy for procurement planning.

Concentration of raw material production in a few geographic hubs intensifies vulnerability, as local policy shifts quickly affect global availability. Export quotas, tariffs, and licensing requirements instituted by producing governments can limit shipments, delaying deliveries and extending lead times. The resulting supply chain fragmentation constrains manufacturers’ ability to implement just-in-time manufacturing and increases working capital requirements for stockpiled inputs. Procurement teams face strategic trade-offs between secure sourcing and cost efficiency, often committing to longer-term contracts at premium prices to ensure continuity.

Material Innovation and Lightweight Hose Development

Material innovation and the development of lightweight hose components represent a strategic avenue for growth, given their direct impact on system efficiency, regulatory compliance, and performance under evolving automotive requirements. Government research highlights that reducing overall component weight offers measurable energy benefits. For example, the U.S. Department of Energy (DOE) reports that a 10% reduction in vehicle weight can improve fuel economy by 6-8%, resulting in lower energy consumption and operational costs in transportation applications, particularly for hybrid and electric platforms, where weight penalties are more pronounced. Advanced elastomers, composite reinforcements, and high-strength alloys enhance thermal stability, environmental resistance, and mechanical durability of hoses, enabling them to withstand higher pressures and temperatures demanded by modern thermal management systems. Adoption of these materials aligns with regulatory frameworks targeting emissions and efficiency.

Material advances also deliver competitive differentiation in both original equipment and aftermarket segments. Lightweight solutions contribute to overall system weight reduction, which is integral to meeting vehicle energy efficiency standards and extending the range of electrified powertrains. Suppliers that invest in tailored material formulations and manufacturing methods build resilience against raw material volatility and equip their products for expanded applications in HVAC, commercial fleets, and industrial cooling, where performance consistency and longevity are critical.

Category-wise Analysis

Product Type Insights

Rubber is poised to lead, with a projected 42% share in 2026, owing to its durability, flexibility, and thermal resistance in automotive and industrial HVAC systems. Rubber hoses maintain high elasticity under fluctuating temperatures and pressures, ensuring consistent performance in conventional internal combustion engine (ICE) vehicles and industrial units. Manufacturers prefer rubber for its ease of molding and cost efficiency, thereby enabling rapid integration into mass-production lines. Rubber hoses offer superior vibration damping, reducing system stress and maintenance requirements. Established supplier networks and proven reliability in original equipment manufacturer (OEM) and aftermarket applications reinforce adoption. Regulatory compliance with refrigerant containment and pressure resistance standards further solidifies its position as the preferred material.

Composite hoses are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by their lightweight construction, high-pressure tolerance, and compatibility with electrified mobility platforms. Advanced composites combine polymers and reinforcement fibers, offering superior thermal stability and resistance to chemical degradation, essential for high-efficiency AC systems. Electrification trends in automotive manufacturing necessitate reduced system weight, thereby directly benefiting the adoption of composites. Industrial HVAC applications also favor composites for high-capacity systems with precise thermal control. The ability to customize composites for temperature, pressure, and bend radius requirements enables manufacturers to meet diverse OEM specifications.

Application Insights

The automotive segment is slated to hold a dominant position, with an anticipated 55% of the AC hose market revenue share in 2026, driven by growing global vehicle production and the widespread integration of air conditioning systems. OEM demand for high-performance hoses capable of handling refrigerants under thermal and pressure variations ensures continued adoption. Electrification trends further necessitate hoses that are lightweight, durable, and thermally efficient, accommodating both conventional and electric powertrains. Regulatory frameworks targeting emissions, refrigerant containment, and energy efficiency encourage OEMs to deploy advanced hose designs. Aftermarket replacement demand also contributes, particularly in regions with aging vehicle fleets requiring reliable service components.

The industrial segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by the increasing construction of factories, commercial complexes, and warehouses requiring high-capacity air conditioning systems. Industrial HVAC applications require hoses capable of withstanding elevated temperatures, high pressures, and extended operational cycles. Regulatory compliance with workplace safety and energy efficiency standards accelerates the adoption of hoses made from advanced composites, reinforced plastics, and high-performance rubbers. Digital monitoring integration, including sensors for pressure and thermal performance, enhances system reliability and maintenance efficiency.

Regional Insights

North America AC Hose Market Trends

North America is expected to hold an estimated 36% of the AC hose market share in 2026, reflecting the combination of advanced automotive manufacturing, high integration of air conditioning systems in vehicles, and established industrial HVAC infrastructure. Automotive production hubs in the United States and Mexico support large-scale deployment of air conditioning hoses, requiring materials that sustain high thermal loads, pressure fluctuations, and long operational cycles. Electrification trends in passenger and commercial vehicles further reinforce demand for lightweight, thermally efficient, and corrosion-resistant hose solutions. High-performance material adoption, including reinforced rubber, hybrid composites, and metallic alloys, ensures compliance with environmental regulations, fuel efficiency mandates, and refrigerant containment standards. Large-scale OEM contracts and standardized supply chains facilitate production scalability, consistent quality, and timely delivery, reinforcing market dominance.

The dominance is also driven by strategic integration of industrial HVAC applications into commercial and manufacturing facilities. Large industrial installations, warehouses, and commercial complexes require hoses capable of sustaining high-capacity airflow, pressure, and thermal performance. Regulatory frameworks promoting energy efficiency, environmental compliance, and occupational safety increase adoption of durable hoses designed for long-term operation and monitoring. Investment in digital monitoring systems and predictive maintenance in HVAC applications enhances system reliability and reduces downtime, further reinforcing market preference for high-quality hose solutions.

Europe AC Hose Market Trends

In Europe, the demand for AC hose is likely to be steady, driven by stringent environmental regulations, high adoption of hybrid and electric vehicles, and established industrial HVAC infrastructure. Automotive manufacturers in Germany, France, and Italy prioritize hoses capable of meeting emission reduction targets, refrigerant containment standards, and energy efficiency requirements. Electrification of vehicle fleets increases demand for lightweight, thermally efficient, and durable hoses that integrate with compact battery cooling systems and advanced HVAC units. Advanced materials, including reinforced polymers, high-temperature rubber, and corrosion-resistant alloys, support performance consistency across diverse operating conditions. Industrial HVAC deployments in commercial and manufacturing facilities require hoses that sustain high pressure, thermal cycling, and long-term reliability.

Competitive dynamics in Europe are shaped by a mix of multinational OEMs, specialized hose manufacturers, and regional aftermarket providers, all focusing on quality, reliability, and technological advancement. Strategic investments target production modernization, automation, and material research to meet evolving vehicle and industrial requirements. Joint ventures and collaborations with global suppliers facilitate access to advanced materials and design expertise, reducing time-to-market for high-performance hose solutions. The expansion of commercial infrastructure and the adoption of energy-efficient HVAC systems in emerging European markets create additional opportunities for product deployment. Focus on sustainable manufacturing, digital monitoring integration, and predictive maintenance enhances the value proposition for industrial and automotive applications.

Asia Pacific AC Hose Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for AC hoses between 2026 and 2033, stimulated by rising vehicle production, increasing adoption of electrified powertrains, and expanding industrial HVAC installations across emerging economies. Large-scale automotive manufacturing in Japan and South Korea drives consistent demand for high-performance air conditioning hoses capable of managing thermal loads, pressure variations, and integration with hybrid and electric powertrains. Urbanization and growing middle-class populations further elevate vehicle penetration, increasing aftermarket replacement cycles and reinforcing demand for durable, lightweight, and thermally efficient hoses. Advanced materials, including reinforced polymers and composite alloys, are being deployed to enhance thermal stability, corrosion resistance, and operational lifespan, aligning with evolving regulatory standards for energy efficiency and refrigerant containment.

The expansion of industrial HVAC infrastructure across the commercial, residential, and manufacturing sectors reinforces accelerated market growth. Demand for hoses capable of sustaining high pressure, temperature fluctuations, and long operational cycles incentivizes investment in advanced manufacturing technologies and reinforced material designs. Government policies promoting energy-efficient construction, green building standards, and industrial modernization stimulate adoption of hoses integrated with predictive maintenance and digital monitoring systems. Regional production and distribution hubs reduce logistics costs, increase scalability, and support rapid response to both automotive and industrial demand surges. Emerging urban centers and industrial clusters create concentrated market opportunities, attracting foreign investment and encouraging technology transfer.

Competitive Landscape

The global AC hose market structure demonstrates a moderate level of consolidation, with leading players collectively holding around 45% of the global market. Key participants include Continental AG, Gates Corporation, SumiRiko Ohio, Inc., Parker Hannifin Corp, and MarkLines Co., Ltd. These suppliers operate across original equipment manufacturing and industrial component segments, leveraging established distribution networks to serve automotive and HVAC applications. Competitive positioning emphasizes material innovation, adherence to international safety and environmental standards, and seamless integration capabilities for diverse system requirements. Smaller regional manufacturers contribute to market fragmentation by focusing on aftermarket solutions and niche industrial applications, offering tailored products for specific operational environments.

Market dynamics are shaped by long-term contracts with original equipment manufacturers, strategic partnerships, and the adoption of automated production technologies. Leading suppliers achieve economies of scale, maintain consistent quality, and optimize cost structures, reinforcing their competitive advantage. Differentiation is increasingly driven by product reliability, material performance, and specialization for electrified vehicles and high-capacity HVAC systems. The market environment encourages innovation in lightweight materials, high-temperature resistance, and durability, which are critical for meeting regulatory requirements and supporting evolving system performance expectations.

Key Industry Developments

- In October 2025, Japanese hose maker Nichirin Co., Ltd. announced plans to establish a new manufacturing subsidiary in India to locally produce automotive hose bodies, including brake and air-conditioning hoses, with operations targeted to begin by 2028, strengthening supply chain integration and supporting original equipment manufacturer localization strategies.

- In July 2025, Adani Enterprises entered a 50:50 joint venture with MetTube Mauritius to co-manufacture high-performance copper tubes for the HVAC sector, reducing India’s reliance on imports and strengthening the domestic supply chain.

- In July 2025, Nissens Automotive expanded its North American product portfolio with the release of 868 new part numbers, including a new line of air conditioning hose assemblies covering 77 million vehicles and enhancing aftermarket coverage for popular import brands.

Companies Covered in AC Hose Market

- Continental AG

- Gates Corporation

- SumiRiko Ohio, Inc.

- Parker Hannifin Corp

- MarkLines Co., Ltd.

- Eaton.

- Sanden Vikas (India) Ltd.

- MAHLE GmbH

- DENSO Corporation.

Frequently Asked Questions

The global AC hose market is projected to reach US$ 3.6 billion in 2026.

Rising demand for automotive and industrial air conditioning systems, electrified vehicles, and regulatory compliance are driving the market.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Advancements in material innovation and development of lightweight, durable hoses are opening multiple opportunities for market players.

Some of the key market players include Continental AG, Gates Corporation, SumiRiko Ohio, Inc., Parker Hannifin Corp, and MarkLines Co., Ltd.