ID: PMRREP3484| 186 Pages | 6 Nov 2025 | Format: PDF, Excel, PPT* | Packaging

The global foodservice disposables market size is likely to value at US$ 59.7 billion in 2025 and is projected to reach US$ 88.5 billion by 2032, expanding at a CAGR of 5.8% between 2025 and 2032.

The market’s evolution is primarily shaped by the expansion of online food delivery platforms, the growth of quick-service restaurants (QSRs), and increasing consumer awareness of hygienic and convenient packaging options.

Global momentum toward sustainability and government-led actions against single-use plastics continue to redefine materials usage and disposal frameworks across regions.

| Key Insights | Details |

|---|---|

| Foodservice Disposables Market Size (2025E) | US$ 59.7 Bn |

| Market Value Forecast (2032F) | US$ 88.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.0% |

Governments worldwide are implementing stringent sustainability policies and restrictions on single-use plastic, reshaping the foodservice disposables industry. Directives such as the European Union’s Single-Use Plastics Directive and India’s national ban on certain plastic grades have strengthened demand for fibre-based, biodegradable alternatives.

In India, the packaging industry is valued at US$ 86 billion in 2024, with a national mission on sustainable packaging led by the Council of Scientific and Industrial Research (CSIR) supporting eco-friendly material innovation.

The resulting shift to compliant alternatives creates a structural demand layer that redefines raw material preferences and operational practices across foodservice chains. The market impact reflects higher adoption of bagasse, polylactic acid (PLA), and bamboo-based disposables, combined with accelerated R&D investment from corporations to align packaging specifications with evolving government mandates.

The acceleration of digital food delivery platforms represents a transformative institutional driver of consumption behaviour. Post-pandemic logistical networks have solidified delivery ecosystems spanning food aggregators, cloud kitchens, and quick-service chains. With over 1.4 billion annual digital food transactions globally reported in 2024, disposable packaging such as cups, meal containers, and cutlery became critical operational elements within these distribution systems.

Applications like Swiggy, Zomato, DoorDash, and Uber Eats increased reliance on flexible disposables for logistical efficiency and food freshness retention. The industry’s dependence on standardised single-use products supports quick turnaround, hygiene maintenance, and scalability of online delivery.

This infrastructure uplift creates consistent volumetric demand across plastic, fibre, and paper material categories and continues to reshape design standards for lightweight and temperature-resistant disposable solutions.

Large-scale production bases and government incentives in the packaging industries enhance the availability of disposable materials.

In the United States, the flexible packaging sector generated US$ 41.5 billion in 2022, occupying a 21% share of the national packaging market. Similarly, India’s paper and cardboard base recorded 861 mills, with 526 operational units, signifying strong domestic production depth. Policy frameworks supporting 100% FDI in packaging and innovation-led investments foster integration between foodservice disposables and broader material ecosystems.

Cross-border collaborations such as Mold Tek’s capacity expansion in liquid food containers strengthen global accessibility and manufacturing resilience. This industrial foundation translates into stable raw material supply chains, improved price elasticity, and technological diffusion across plant fiber and biodegradable disposables manufacturing segments, reinforcing market scalability and regional competitive advantages.

High production costs of biodegradable disposables and consumer sensitivity to price levels present structural challenges. The economic disparity between conventional plastic and fiber-based products remains significant, with unit costs for sustainable materials often 25-35% higher due to raw material processing and certification requirements. For small and mid-scale restaurants, price sensitivity reduces substitution willingness.

As per 2024 retail studies, disposable price variations influence approximately 40% of procurement decisions in emerging markets, signifying continued margin pressure. This cost imbalance moderates the pace of eco-transition and encourages the parallel existence of low-cost plastics and premium sustainable products, thereby fragmenting buyer segments.

Disposal infrastructure insufficiency and limited recycling facilities hinder proper waste segregation and collection. According to the United Nations Environmental Programme (2023), nearly 60% of single-use food containers globally are not recovered through organised recycling.

Municipal systems often lack centralised collection structures for mixed materials, leading to landfill congestion and community-level pollution risks. This constraint underscores operational inefficiencies within waste systems, elevating environmental compliance costs for manufacturers and foodservice operators facing stringent waste-handling obligations under national urban sanitation programs.

The introduction of circular economy frameworks creates opportunities for systemic industrial redesign. As governments reinforce waste recovery initiatives, closed-loop recycling and reusability systems gain traction. The European Commission’s Circular Economy Action Plan (CEAP) integrates packaging material recyclability targets for 2030, guiding companies toward multi-cycle applications for foodservice items.

Manufacturers adopting compostable polymers and cellulosic materials achieve compatibility with these evolving directives. Corporations leveraging traceable material tracking and partnership with certified recycling systems stand positioned to capture regulatory incentives while reducing long-term production volatility.

This environment stimulates innovation in product labelling, material quality verification, and supply chain transparency directly influencing investment priorities within sustainable disposables.

Companies focusing on modular recycling hubs or city-level waste sortation programs can secure government funding streams, particularly in markets such as Japan and Germany, where structured recovery programs integrate with foodservice chains. This systematic synergy between industry and government enables targeted disposal reforms, improved consumer participation, and measurable reductions in landfill dependency, strengthening commercial sustainability.

The material innovation frontier offers transformative operational agility. Scientific advances in plant-derived materials like bagasse, wheat straw, bamboo pulp, and starch composites have expanded product durability and safety performance.

In the Asia-Pacific, R&D expenditure by leading firms such as SIG and Oji India increased by over 12% in 2024, focusing on performance coatings and structural rigidity in biodegradable containers. UV-cured printing technology has become a leading innovation for customisation, providing minimal volatile organic compound (VOC) emissions during personalised product production.

These developments establish competitive differentiation and broader downstream adaptability across foodservice brands. For manufacturers, the ability to innovate at cost-efficient scalability forms critical leverage in commercial bids with high-volume QSR and catering services.

Advances in heat-sealed fibre wrappers and microwave-safe compostable trays also unlock practical substitution channels for plastic. Active collaboration between material science institutes and packaging converters is supporting predictable biodegradable behaviour, ensuring compliance with international safety regulations such as U.S. FDA food-contact norms and Japan’s Plastic Recycling Promotion Act. This convergence of science and industry potentiates the rapid adoption of eco-conscious disposable systems.

Artificial intelligence and machine learning accelerator chips drive demand for specialised thermal interface materials and die attach adhesives capable of managing heat dissipation exceeding 500W per package. Advanced flip-chip technologies enabling high-performance computing applications require underfill materials with enhanced thermal conductivity and reliability under power cycling conditions.

The Flexible Packaging segment leads with 58% share in 2025, driven by heightened demand from delivery and takeaway services. Flexibles enable compact stacking, moisture resistance, and cost efficiency suited for dynamic foodservice operations. Their adaptability supports both hot and cold meal distribution, aligning with the expansion of digital food ordering platforms globally.

Government-endorsed food safety requirements and sustainable material technology have increased the structural relevance of flexible packaging within urban supply chains. Cross-sector data highlight that food packaging represents nearly half of U.S. flexible packaging shipments, confirming the segment’s application dominance across containers, wraps, and pouches.

The plastic segment, accounting for a 38% share in 2025, retains leadership due to entrenched infrastructure, low processing cost, and universal applicability in cups, trays, and cutlery.

Plastic’s resilience in moisture control and heat retention remains fundamental for hot beverages and food packaging sectors. Despite regulatory constraints, consumer preference for reliable performance sustains moderate continuity. Extensive usage across QSR chains and beverage services, especially within North America, substantiates the segment’s material versatility, emphasising its efficiency in food preservation during transit.

The fibre segment, encompassing bagasse, wheat straw, and bamboo derivatives, is the fastest-growing category, estimated at around 11% share in 2025. Fibre-based disposables gain traction from regulatory initiatives promoting organic waste recovery and compostability.

In response to global plastic bans, producers have diversified into cellulose-based replacements that fulfil hygiene, strength, and biodegradability standards. This segment holds strategic relevance in eco-design policy landscapes particularly in Europe and East Asia because of its compliance advantages and cost reduction potential through agricultural residue utilisation. Material life-cycle evaluation exhibits fiber’s low carbon intensity, reinforcing market alignment with international sustainability goals.

North America accounts for approximately 23% share, driven by high per-capita disposable usage and an established quick-service restaurant culture. The U.S. packaging domain supports widespread production capacity, employing 85,000 individuals and maintaining diverse converter networks across 10 leading states, housing 58% of industry facilities.

Foodservice disposables feature persistent integration across major QSR chains, coffee franchises, and catering outlets where reliability and branding are crucial operational factors. Regulatory action toward sustainable transformation remains incremental, as state-level environmental goals emphasise both recycling and gradual substitution.

Ongoing technological investments in flexible packaging and biodegradable film coatings strengthen domestic innovation output. Corporate geographic expansions across Canada and Mexico demonstrate regional integration in logistics and supply networks.

The combination of standardised production, moderate population growth, and consumer preference for convenience creates durable volumetric demand. Investments in digital traceability systems ensure product accountability as part of U.S. sustainability certification frameworks such as the Green Seal Program.

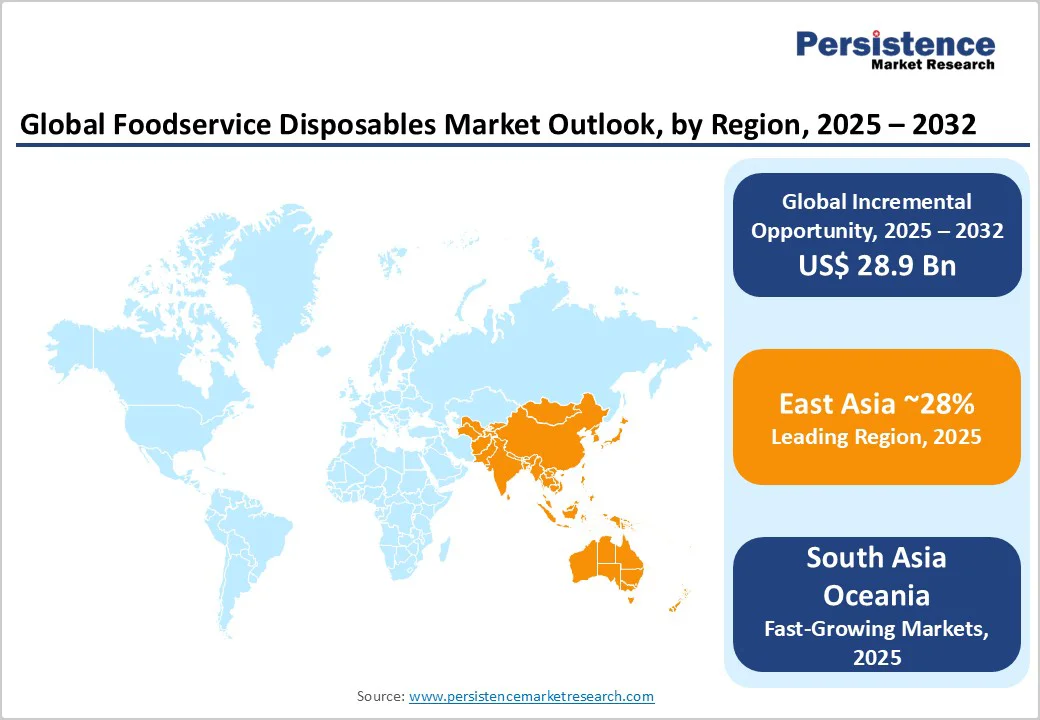

East Asia accounts for approximately 28% of the global foodservice disposables market. This region demonstrates large-scale production capability and strong domestic consumption, led by China, Japan, and South Korea. Packaging turnover rates remain among the highest globally due to elevated foodservice density and substantial catering industries.

China’s national plastic restriction guidelines under the 2023 Green Development Policy accelerated fibre-based substitution, while Japan’s continued progress on recycling promotion acts fortified waste recovery efficiency to above 85% for paper-based disposables.

South Korea’s advanced urban dining ecosystem further integrates compostable meal packaging, encouraged by local waste-reduction targets. Investment trends in automation and digital logistics bolster domestic supply chains, enabling functional expansion within export networks centred around high-volume flexible packaging.

Government-backed innovation grants, particularly those linked to clean production certification, anchor sustainable competitiveness across the regional industry framework.

Holding approximately 16% market share, South Asia and Oceania demonstrate high structural opportunity supported by regional demographic strength and evolving consumption patterns. India dominates disposable usage volumes, with rising online delivery penetration and comprehensive policy promotion under its National Mission on Sustainable Packaging.

Recent government data indicate continuous FDI inflows worth US$ 1.74 billion (2000 - 2024) into packaging-related manufacturing, enabling scalable production of both plastic and fiber-based foodservice disposables. In Australia, innovation transitions toward compostable packaging align with the 2025 National Packaging Targets focused on 100% recyclable or compostable material recovery.

With approximately 20% global participation, Europe represents a sustainability-centred market supported by institutional policy evolution. High foodservice density across Germany, France, Italy, and the UK maintains consumption volume despite a gradual per-unit reduction due to material shifts.

The EU Single-use plastics directive (2021) and continuing enforcement cause diversification into fiber and compostable categories at scale. Numerous initiatives under the Circular Economy Action Plan (CEAP) target packaging innovation and waste minimisation. Government-sponsored pilot projects in France (2023 - 2024) focus on large-scale substitution testing between moulded pulp and cellulose composites.

The regulatory intensity across Europe redefines supply chain design, compelling corporations to localise sourcing and optimise reverse logistics operations. Competitive dynamics reveal gradual industry consolidation, as manufacturers pursue technology partnerships to align products with recycling rate improvement targets for 2030. The emphasis on renewable input ensures the region’s leadership within ecological compliance and market structural stability.

The global foodservice disposables market demonstrates a fragmented structure, characterised by the presence of numerous international manufacturers and strong regional converters competing across material and packaging categories.

Market competition is driven by innovation in compostable materials, customisation, and supply chain efficiency. Leading players include Huhtamaki Food Service, Dart Container Corporation, Berry Global Inc., Sabert Corp., Pactiv LLC, Vegware Ltd., Genpak LLC, and Graphic Packaging International LLC, each maintaining diversified product portfolios. Additional strong participants, such as Anchor Packaging Inc. and Georgia-Pacific LLC, emphasise recyclable and fibre-based designs.

The global foodservice disposables market is projected to be valued at US$ 59.7 Bn in 2025.

The flexible packaging segment is expected to hold around 58% share in 2025. This is driven by strong demand from delivery and takeaway services, which utilize flexible packaging for its convenience and adaptability in foodservice disposables.

The foodservice disposables market is expected to witness a CAGR of 5.8% from 2025 to 2032.

The foodservice disposables market is driven by sustainability regulations, expansion of digital food delivery infrastructure, and strong industrial packaging ecosystem support.

Key market opportunities include the integration of circular economic practices, advancements in material engineering, and emerging market formalisation with increased institutional adoption.

The leading global players in the foodservice disposables market are Dart Container Corporation, Berry Global Inc., Georgia-Pacific LLC, Huhtamaki, Pactiv Evergreen Inc., and Anchor Packaging Inc.

| Report Attribute | Details |

|---|---|

| Forecast Period | 2025 to 2032 |

| Historical Data Available for | 2019 to 2024 |

| Market Analysis | USD Million for Value |

| Region Covered |

|

| Key Companies Covered |

|

| Report Coverage |

|

By Packaging Type

By Material Type

By Application

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author