- Medical Devices

- Wireless Fetal Monitoring Systems Market

Wireless Fetal Monitoring Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Wireless Fetal Monitoring Systems Market by Product Type (Instruments, Accessories, and Consumables), Application (Fetal Heart Rate Monitoring, Intrauterine Pressure Monitoring), End-user, and Regional Analysis from 2026 to 2033

Wireless Fetal Monitoring Systems Market Share and Trends Analysis

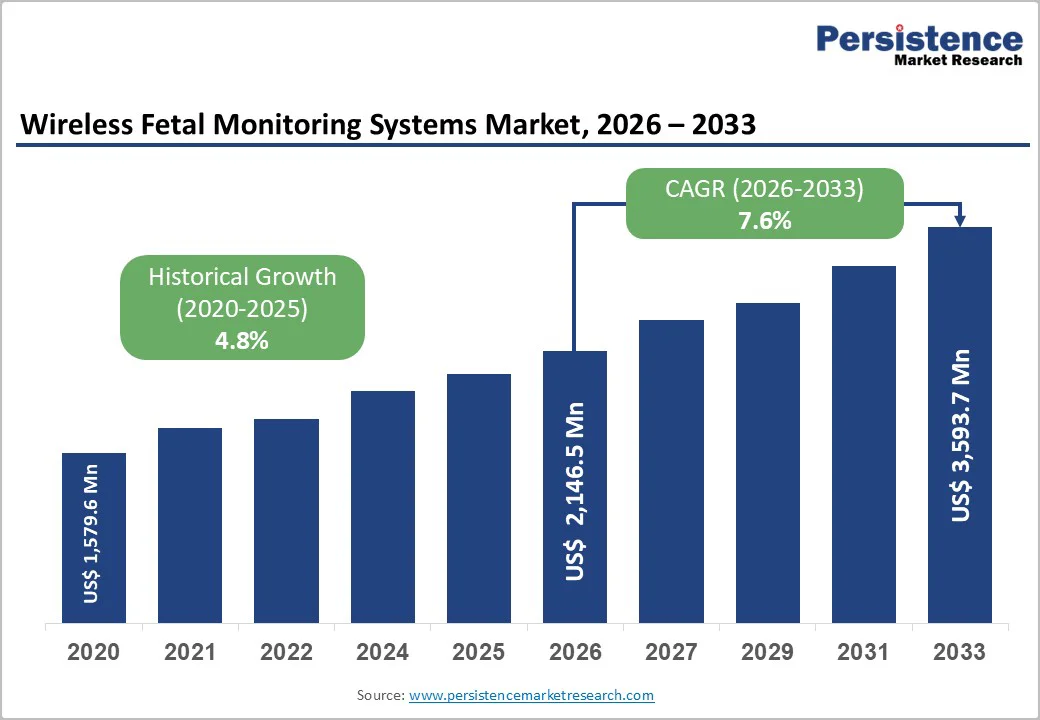

The global wireless fetal monitoring systems market size is estimated to grow from US$2,146.5 million in 2026 to US$3,593.7 million by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033. As healthcare providers increasingly shift toward mobility-enabled, patient-centric maternity care, it has triggered the need for wireless fetal monitoring systems.

These systems allow continuous or intermittent monitoring of fetal heart rate and uterine activity without restricting maternal movement, improving comfort and clinical efficiency. Growing adoption of telehealth, rising high-risk pregnancies, and the need to reduce hospital visits are accelerating demand for wireless solutions.

Hospitals and home-care settings are embracing these technologies for both intrapartum and remote monitoring. Advancements in wearable sensors, cloud connectivity, and real-time data analytics are further enhancing accuracy, early risk detection, and overall maternal-fetal outcomes globally.

Key Industry Highlights:

- Modern wireless monitors feature wearable sensors, Bluetooth/Wi-Fi connectivity, cloud-based data storage, and real-time analytics, improving monitoring accuracy, usability, and clinician decision-making efficiency.

- Rising preference for home-based maternal care is driving demand for portable wireless devices to support remote fetal monitoring and reduce dependence on hospital infrastructure.

- Advanced analytics provide early detection of fetal distress, uterine abnormalities, and labor progression trends, improving clinical interventions and neonatal outcomes.

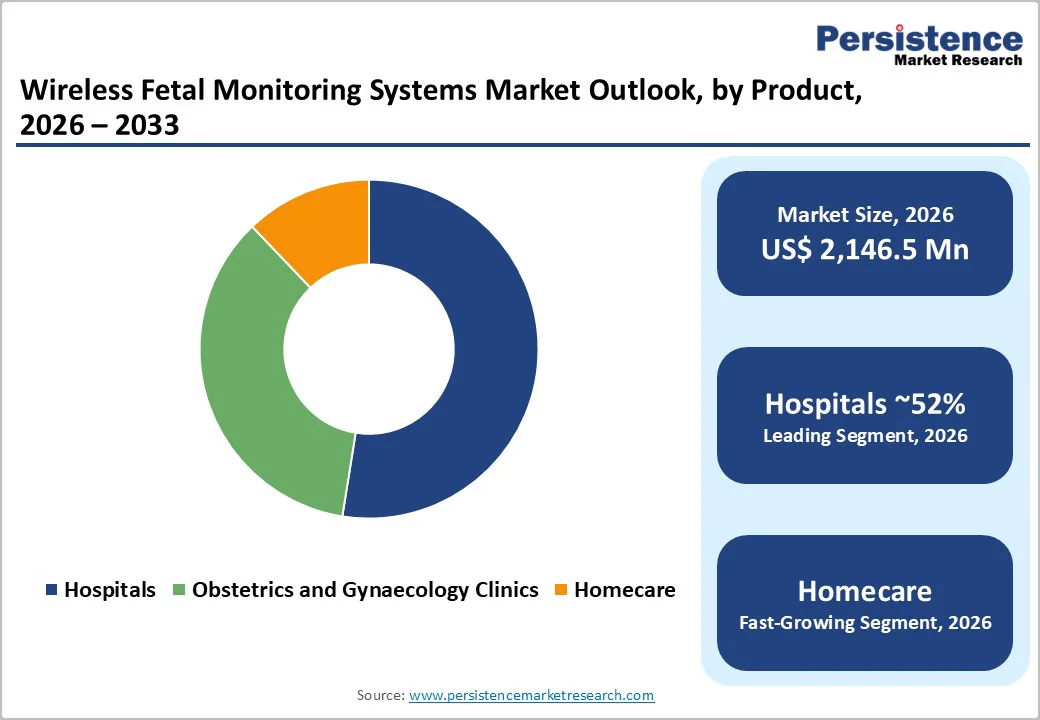

- Instruments are the core product that hospitals, clinics, and home-care providers purchase, making them the main contributor to overall market value.

- The North American population prioritizes prenatal care, early risk detection, and high-risk pregnancy management, driving demand for advanced monitoring systems.

| Key Insights | Details |

|---|---|

| Wireless Fetal Monitoring Systems Market Size (2026E) | US$2,146.5 Mn |

| Market Value Forecast (2033F) | US$ 3,593.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.8% |

Market Dynamics

Driver - Shift Toward Ambulatory & Home-Based Care

The shift toward ambulatory and home-based care is transforming maternal-fetal monitoring, creating a strong growth avenue for wireless fetal monitoring systems. Increasingly, expectant mothers are seeking care models that allow them to remain comfortable at home while still receiving professional medical oversight.

Traditional hospital-based monitoring, often involving wired CTG machines and long inpatient stays, can be inconvenient, stressful, and restrictive, particularly for those in high-risk pregnancies or with mobility challenges. Wireless fetal monitoring devices, including wearable belts, patches, and portable Dopplers, empower mothers to move freely during daily activities while continuously tracking fetal heart rate and uterine contractions.

These devices transmit real-time data to clinicians via secure cloud platforms or smartphone applications, allowing obstetricians to monitor fetal well-being remotely and intervene promptly if any abnormalities are detected.

The convenience of at-home monitoring not only reduces the frequency of hospital visits but also alleviates the psychological stress associated with frequent check-ups, particularly in rural areas where access to tertiary care centers may be limited.

Moreover, home-based monitoring supports personalized care, enabling clinicians to tailor monitoring frequency and interventions according to the patient’s risk profile.

Combined with rising adoption of telemedicine and digital health platforms, and patient preference for non-invasive, comfortable solutions, this trend is driving significant growth in wireless fetal monitoring systems globally, positioning home-based care as a cornerstone of modern maternal health management.

Restraints - Short Device Lifespan of Accessories

One significant challenge restraining the growth of the wireless fetal monitoring market is the short lifespan of device accessories, including electrodes, wearable patches, belts, and sensor pads. These consumables are critical for the accurate detection of fetal heart rate and uterine activity. Still, they are designed for limited use, often single-patient or short-duration applications, to ensure hygiene, signal fidelity, and clinical accuracy.

As a result, healthcare providers face frequent replacement cycles, which not only increase recurring operational costs but also require careful inventory management to avoid interruptions in patient monitoring. For hospitals and maternity centers with high patient volumes, the logistical burden of consistently stocking these consumables can be substantial, particularly when dealing with multiple device types or varying sizes for maternal comfort.

Moreover, in emerging markets or smaller clinics, inconsistent supply chains and delayed shipments may disrupt monitoring schedules, potentially compromising maternal-fetal care. The recurring expense of consumables can also impact overall affordability, discouraging adoption in cost-sensitive settings.

Even though the primary devices, wireless CTG monitors or wearable fetal sensors, have longer lifespans, the dependency on short-lived accessories emphasizes a hidden operational challenge, highlighting the need for innovative solutions such as reusable or longer-lasting electrodes and enhanced supply management systems to improve efficiency, reduce costs, and support wider adoption globally.

Opportunity - Wearable Sensor Miniaturization

Wearable Sensor Miniaturization in Wireless Fetal Monitoring represents a transformative opportunity in maternal healthcare, addressing both clinical effectiveness and patient comfort. Traditional fetal monitoring systems, while accurate, often involve bulky belts, wires, or patches that can restrict maternal movement, cause discomfort, and limit long-term use.

Miniaturization of sensors enables the development of ultra-thin, flexible, and lightweight devices that can be discreetly worn on the abdomen to monitor continuous fetal heart rate, uterine contractions, and movement without interfering with daily activities.

These next-generation wearables leverage flexible electronics, soft biocompatible materials, and low-power connectivity to ensure long-term adherence and reliable signal capture. Their design reduces skin irritation and pressure points, making them ideal for extended monitoring during high-risk pregnancies or remote home-based care.

Furthermore, miniaturized sensors enable integration with smartphones, cloud platforms, and AI-driven analytics, allowing clinicians to receive real-time alerts, track trends, and make proactive interventions.

By combining mobility, comfort, and advanced data capabilities, wearable sensor miniaturization not only enhances the maternal experience but also improves clinical outcomes by enabling timely detection of fetal distress or abnormal contraction patterns.

This innovation opens significant market potential in both developed regions, where patient-centered care is a priority, and emerging markets, where remote monitoring can bridge gaps in maternal-fetal healthcare access.

Category-wise Analysis

By Product Type Insights

In the wireless fetal monitoring systems market, instruments dominate the market share because they represent the core technology required for maternal-fetal monitoring. These devices-including wireless CTG monitors, wearable fetal belts, and handheld Dopplers-are high-value, capital-intensive products purchased primarily by hospitals, maternity centers, and clinics.

Their high price points, often several times greater than individual consumables, make them the largest revenue contributor. Clinically, instruments are indispensable; without them, monitoring cannot occur, whereas accessories and consumables are supportive.

Accessories and consumables, such as electrodes, disposable patches, and belts, are essential for device functionality but are relatively inexpensive and purchased in recurring cycles. While they contribute to steady, long-term revenue, their individual cost is minimal compared to instruments. Additionally, the replacement cycle for consumables is predictable, whereas instruments require significant upfront investment, which influences procurement budgets and market valuation.

Furthermore, instruments often integrate advanced features, such as Bluetooth, cloud connectivity, and AI analytics that add to their value and differentiation, reinforcing their dominance. In contrast, consumables are largely standardized with limited scope for technological differentiation, keeping their share smaller despite consistent demand.

By End-user Insights

In the wireless fetal monitoring systems market, hospitals are the leading end-user segment due to their central role in maternal and neonatal care. Hospitals, particularly maternity wards and tertiary care centers, manage a high volume of pregnancies, including both low-risk and high-risk cases, necessitating continuous, reliable, and advanced fetal monitoring solutions.

They require sophisticated instruments such as wireless CTG monitors, wearable fetal belts, and handheld Dopplers to ensure accurate real-time tracking of fetal heart rate, uterine contractions, and maternal health parameters.

Hospitals also benefit from robust budgets and reimbursement support, enabling investment in high-cost monitoring instruments, integration with electronic health records (EHR), and adoption of telehealth-enabled solutions. Their scale of operations, handling multiple deliveries and high-riskcases simultaneously, further drives demand for various devices, increasing total market share.

In contrast, Obstetrics & Gynecology clinics and home care settings have smaller shares because they serve fewer patients and often rely on intermittent monitoring. Clinics may purchase devices for periodic checks, and homecare monitoring is still emerging, limited by patient awareness, affordability, and infrastructure.

Overall, hospitals dominate due to volume of patients, investment capacity, clinical necessity, and integration with advanced healthcare systems, making them the backbone of market demand while other segments grow more gradually.

By End-user Insights

In the Wireless Fetal Monitoring Systems market, hospitals are the leading end-user segment due to their central role in maternal and neonatal care. Hospitals, particularly maternity wards and tertiary care centers, manage a high volume of pregnancies, including both low-risk and high-risk cases, necessitating continuous, reliable, and advanced fetal monitoring solutions.

They require sophisticated instruments such as wireless CTG monitors, wearable fetal belts, and handheld Dopplers to ensure accurate real-time tracking of fetal heart rate, uterine contractions, and maternal health parameters.

Hospitals also benefit from robust budgets and reimbursement support, enabling investment in high-cost monitoring instruments, integration with electronic health records (EHR), and adoption of telehealth-enabled solutions. Their scale of operations, handling multiple deliveries and high-riskcases simultaneously, further drives demand for various devices, increasing total market share.

In contrast, Obstetrics & Gynecology clinics and home care settings have smaller shares because they serve fewer patients and often rely on intermittent monitoring. Clinics may purchase devices for periodic checks, and homecare monitoring is still emerging, limited by patient awareness, affordability, and infrastructure.

Overall, hospitals dominate due to volume of patients, investment capacity, clinical necessity, and integration with advanced healthcare systems, making them the backbone of market demand while other segments grow more gradually.

Regional Insights

North America Wireless Fetal Monitoring Systems Trends

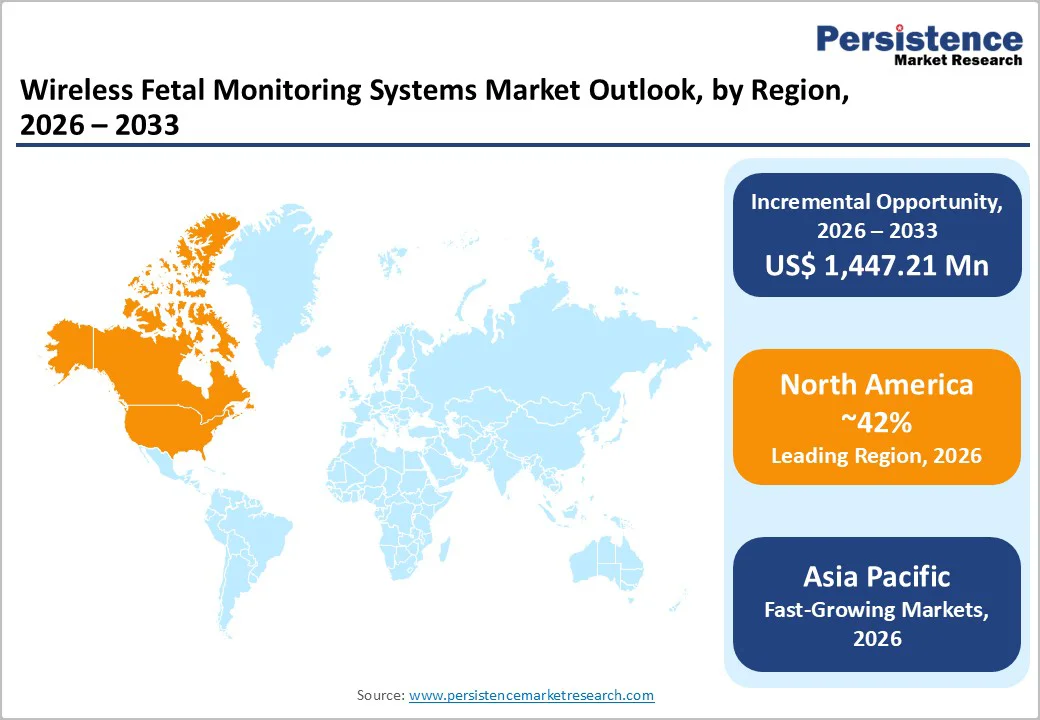

North America leads the Wireless Fetal Monitoring Systems market, driven by advanced healthcare infrastructure, high maternal health awareness, and rapid adoption of digital health technologies. Hospitals and maternity centers in the U.S. and Canada are increasingly deploying wireless CTG monitors, wearable fetal belts, and handheld Dopplers to enhance prenatal and intrapartum care.

In the U.S., the rising number of high-risk pregnancies, coupled with strong insurance reimbursement for maternal-fetal monitoring, has accelerated demand for continuous and remote monitoring solutions. Telehealth integration and remote patient monitoring (RPM) programs are expanding, allowing clinicians to track fetal health in real time, reduce hospital stays, and improve patient comfort.

Technological innovation is another key trend, with U.S. manufacturers incorporating cloud connectivity, AI-driven analytics, and flexible wearable sensors that enable continuous, mobility-friendly monitoring. Regulatory support from the FDA ensures device safety and encourages faster adoption in clinical settings.

Additionally, hospitals are investing in data-driven platforms that integrate fetal monitoring with electronic health records (EHR), streamlining workflows and enhancing early detection of complications. As patient-centric care and digital health adoption grow, North America, led by the U.S., continues to dominate the market while setting benchmarks for global wireless fetal monitoring innovation.

Asia Pacific Wireless Fetal Monitoring Systems Market Trends

Asia Pacific is emerging as the fastest-growing market for wireless fetal monitoring systems, driven by rising maternal health awareness, expanding healthcare infrastructure, and increasing high-risk pregnancies.

Countries such as China, India, Japan, and Australia are witnessing significant investments in modern maternity care facilities, enabling the adoption of wireless CTG monitors, wearable fetal belts, and handheld Dopplers in both urban hospitals and regional clinics.

Rapid urbanization, higher disposable incomes, and growing telemedicine initiatives are driving demand for home-based and remote fetal monitoring solutions, particularly in countries with limited access to specialized maternal care.

Technological advancements, such as portable wearable sensors, cloud-based analytics, and smartphone connectivity, are enhancing monitoring accuracy and maternal comfort, making wireless systems more appealing to both providers and patients. Government health programs and initiatives targeting maternal and neonatal health, especially in India and Southeast Asia, are further encouraging adoption.

Additionally, collaborations between local distributors and global device manufacturers are increasing market penetration. Overall, the Asia Pacific market is poised for accelerated growth, driven by infrastructure development, rising health awareness, technological innovation, and supportive policies that promote maternal-fetal healthcare.

Competitive Landscape

The Wireless Fetal Monitoring Systems market is highly competitive, featuring a mix of established medical device manufacturers and innovative digital health startups.

Market players compete through hospital-grade wireless CTG monitors, wearable fetal belts, and portable Dopplers integrated with telehealth and cloud-based analytics. Key strategies include technological innovation, regulatory approvals, and strategic partnerships with hospitals, clinics, and remote monitoring providers. Companies are increasingly investing in R&D to enhance device accuracy, maternal comfort, and real-time data insights.

Key Industry Developments:

- In February 2025, GE HealthCare received 510(k) clearance from the United States Food and Drug Administration (FDA) for the Novii™+ Wireless Patch Solution. The antepartum and intrapartum maternal and fetal monitor noninvasively measured and displayed fetal heart rate, maternal heart rate, and uterine activity, allowing care teams to have a real-time view of patient data.

Companies Covered in Wireless Fetal Monitoring Systems Market

- General Electric Company

- Koninklijke Philips N.V.

- OBMedical Company

- Huntleigh Healthcare Limited (ARJO Family)

- Sunray Medical Apparatus Co., Ltd

- Dixion Vertrieb der Medizingeräte GmbH

- Shenzhen Unicare Electronic Co., Ltd.

- Shenzhen Jumper Medical Equipment Co.,Ltd.

- Shenzhen Aeon Technology Co., Ltd.

- Shenzhen Lai Kang Ning Medical Technology Co., Ltd.

- Mediana Co.,Ltd

- Others

Frequently Asked Questions

The global market is projected to be valued at US$2,146.5 Mn in 2026.

Increasing cases of gestational diabetes, preeclampsia, and advanced maternal age are driving demand for continuous fetal monitoring.

The global wireless fetal monitoring systems market is poised to witness a CAGR of 7.6% between 2026 and 2033.

Developing ultra-thin, flexible, and comfortable sensors for long-term maternal use without restricting movement.

General Electric Company, Koninklijke Philips N.V., OBMedical Company, Huntleigh Healthcare Limited (ARJO Family), and others.