- Healthcare IT

- Wireless Medical Technologies Market

Wireless Medical Technologies Market Size, Share, and Growth Forecast, 2026 - 2033

Wireless Medical Technologies Market By Technology (Wireless Wide Area Network (WWAN), Others), Component Type (Software, Hardware, Services), Application (Patient-specific, Provider-specific), End-user, and Regional Analysis for 2026 - 2033

Wireless Medical Technologies Market Size and Trends Analysis

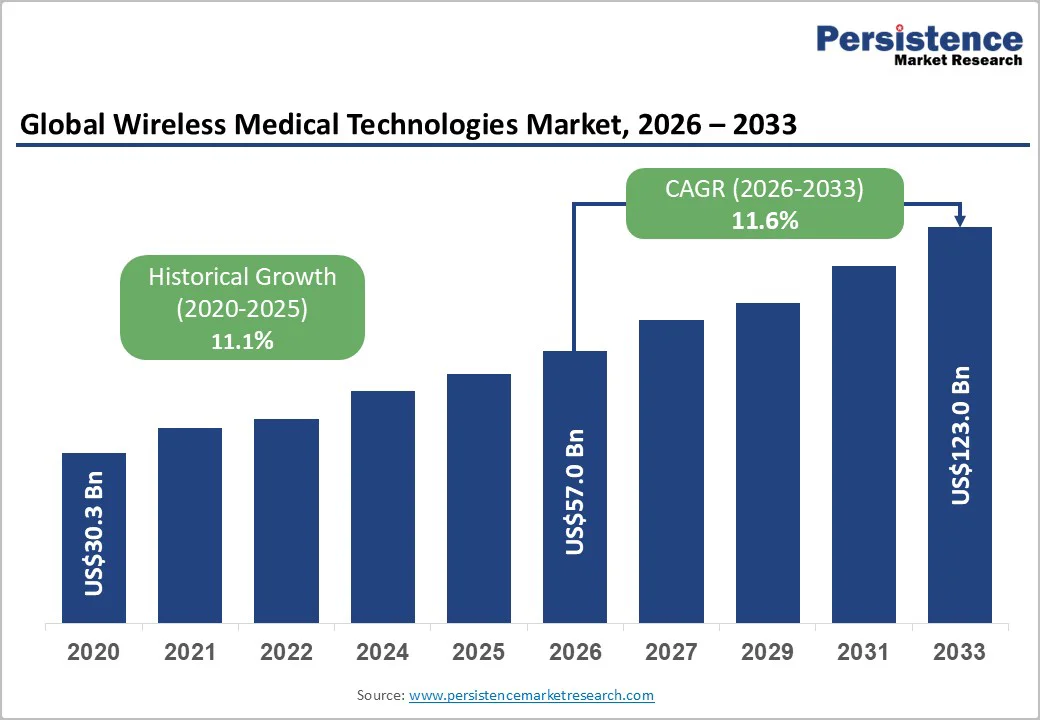

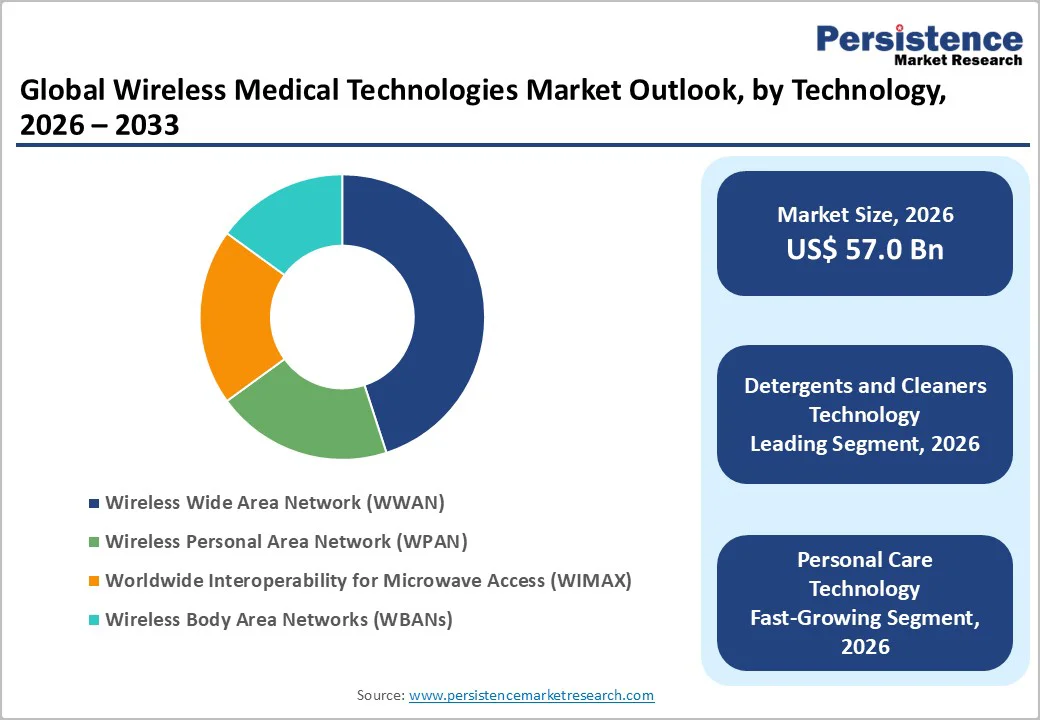

The global wireless medical technologies market size is likely to be valued at US$57.0 billion in 2026. It is expected to reach US$123.0 billion by 2033, growing at a CAGR of 11.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of telemedicine adoption, rising demand for remote patient monitoring, and advancements in low-power wireless networks.

Demand for seamless connectivity in wearables and hospital IoT is driving strong adoption of wireless medical technologies across diverse user groups. Advancements in WBANs and WPANs are further accelerating uptake by offering secure and efficient solutions. Growing reliance on wireless systems for chronic disease management, especially among healthcare providers, continues to fuel market growth.

Key Industry Highlights:

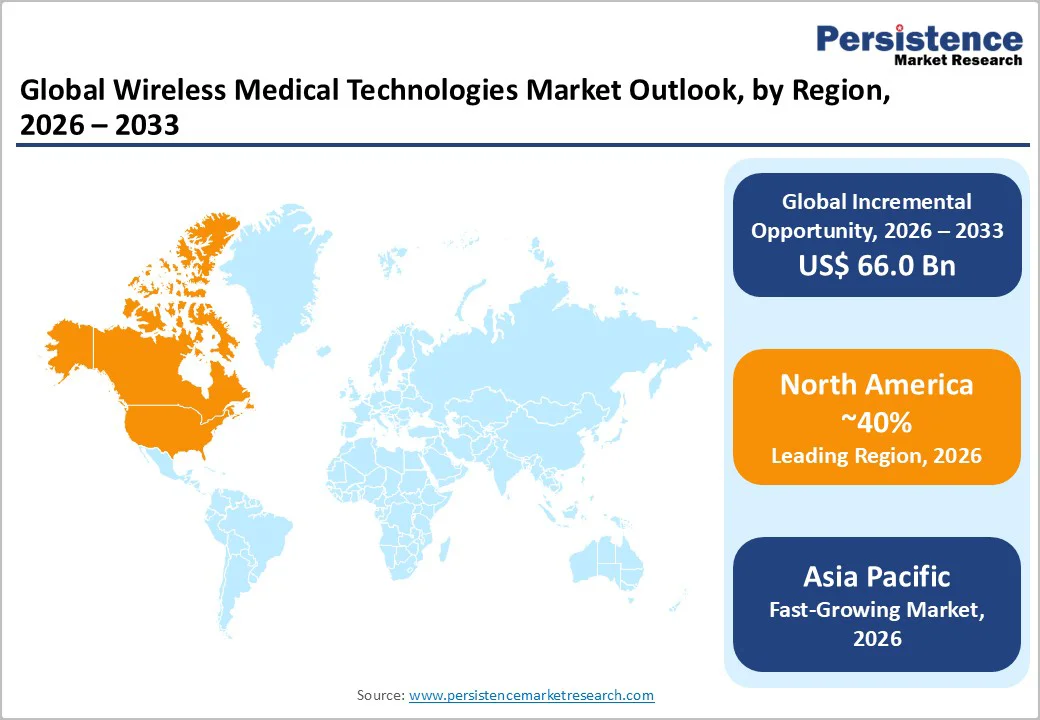

- Leading Region: North America is expected to account for approximately 40% of the market share in 2026, driven by advanced healthcare IT infrastructure, high prevalence of remote monitoring, and strong R&D activities in the U.S.

- Fastest-growing Region: Asia Pacific is anticipated to be the fastest-growing, fueled by increasing smartphone penetration, rising awareness of mHealth, and growing investments in digital health in China and India.

- Dominant Technology: Wireless Body Area Networks (WBANs) are projected to hold approximately 35% of the market share, due to wearable integration.

- Leading Component Type: Hardware, to account for over 45% of market revenue in 2026, driven by device demands.

- Leading Application: Patient-specific, to contribute nearly 50% of market revenue in 2026, due to personalized care.

- Leading End-user: Providers, to account for approximately 55% market share in 2026, driven by hospital networks.

- Key Market Driver: Explosive growth in telemedicine and IoT-enabled wearables is accelerating the adoption of wireless medical technologies for remote patient care.

- Market Opportunity: Expansion in 5G-enabled mHealth and AI-driven diagnostics creates strong opportunities for secure wireless solutions.

| Key Insights | Details |

|---|---|

|

Wireless Medical Technologies Market Size (2026E) |

US$57.0 Bn |

|

Market Value Forecast (2033F) |

US$123.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

11.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

11.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Telemedicine Adoption and Demand for Remote Patient Monitoring

The rising prevalence of telemedicine adoption globally is a primary driver of the wireless medical technologies market. Telemedicine has gained widespread acceptance as healthcare providers seek to expand access, improve patient engagement, and reduce the burden on traditional clinical settings. The COVID-19 pandemic accelerated this trend, demonstrating the value of virtual consultations, remote diagnostics, and continuous patient monitoring, especially for chronic disease management, post-operative care, and elderly populations.

Remote patient monitoring (RPM) leverages wireless devices, wearables, and connected health platforms to track vital signs, glucose levels, cardiac metrics, and other health parameters in real time. This capability allows clinicians to detect early warning signs, adjust treatments promptly, and reduce unnecessary hospital visits. The growing emphasis on preventive and value-based care has made RPM a critical tool for improving outcomes and optimizing healthcare costs. Advancements in mobile health apps, cloud computing, and IoT-enabled devices have made remote monitoring more accurate, scalable, and user-friendly. Patients benefit from convenience and personalized care, while providers gain actionable data to make informed decisions.

High Development and Interoperability Costs

The high costs associated with development and ensuring interoperability of wireless medical technologies pose a significant restraint on market growth. Developing advanced wireless medical devices and platforms requires substantial investments in research, design, and testing to ensure accuracy, reliability, and compliance with stringent regulatory standards. Manufacturers must integrate multiple technologies, including sensors, wireless protocols, cloud computing, and cybersecurity measures, all of which add to development complexity and costs. The high cost of prototyping, clinical validation, and obtaining approvals from agencies such as the FDA or EMA further increases the financial burden.

Interoperability poses another critical cost factor. Wireless medical systems must seamlessly integrate with existing hospital infrastructure, electronic health records (EHRs), and other medical devices to provide cohesive patient data management. Achieving this requires extensive software customization, rigorous testing, and continuous updates to maintain compatibility across diverse platforms and vendor products. Legacy systems in healthcare facilities often complicate integration, necessitating additional resources for system upgrades or middleware solutions.

Advancements in 5G-enabled mHealth and AI-driven Diagnostics

Advancements in 5G-enabled mHealth and AI-driven diagnostics present significant growth opportunities for the wireless medical technologies market. The integration of 5G significantly enhances mobile health capabilities through ultra-low latency, high bandwidth, and reliable data transmission, allowing clinicians to access real-time patient information with unprecedented accuracy. This supports advanced applications such as remote surgeries, continuous monitoring through wearables, and high-quality teleconsultations, improving accessibility and outcomes across both urban and rural settings.

AI-driven diagnostics are transforming the way medical data is analyzed and interpreted. Sophisticated algorithms can process large volumes of imaging, sensor, and clinical data to detect abnormalities, predict disease progression, and support decision-making far more rapidly than traditional methods. When paired with 5G connectivity, these AI tools can instantly relay insights to healthcare providers, enabling timely interventions and personalized treatment plans. The convergence of 5G and AI also accelerates the deployment of smart hospital systems, automated triage solutions, and predictive maintenance of medical devices.

Category-wise Analysis

Technology Insights

Wireless Body Area Networks (WBANs) are anticipated to dominate the market, accounting for approximately 35% of the market share in 2026. Its dominance is driven by wearables, low energy, and proximity, making it preferred for monitoring. WBANs, such as those from Dexcom, provide continuous glucose, ensuring accuracy. Its scalability and security make it preferred for developers.

Wireless Personal Area Network (WPAN) is the fastest-growing segment, propelled by rising Bluetooth-enabled devices and expanding home-care applications. The simple pairing and low-power connectivity make it ideal for wearables and remote monitoring tools. Ongoing innovations in Zigbee and similar protocols are further boosting adoption, particularly across Asia Pacific and North America’s rapidly evolving digital-health ecosystems.

Component Type Insights

Hardware is expected to lead the market, holding approximately 45% of the market share in 2026, driven by strong demand for sensors, wearables, and connected medical devices. Its essential role in real-time data transmission and device interoperability drives widespread adoption. As wireless monitoring and diagnostics expand, hardware remains the core component enabling reliable, continuous healthcare connectivity.

Services are likely to represent the fastest-growing segment, driven by the rising demand for system integration, configuration, and consulting support in wireless healthcare deployments. Healthcare providers rely on these services for smooth implementation, interoperability, and continuous optimization. The convenience of expert guidance, maintenance, and scalable support accelerates adoption, making services essential to the expansion of connected medical ecosystems.

Application Insights

Patient-specific is likely to dominate the market, contributing nearly 50% of market revenue in 2026, driven by strong adoption of wearables and personalized health tools. These technologies enable continuous monitoring, making them highly preferred for chronic disease management. Rising demand for individualized care, real-time insights, and user-friendly devices further reinforces the prominence of patient-specific wireless medical applications.

Provider-specific is projected to be the fastest-growing segment, driven by rapid IoT adoption in hospitals and the expansion of clinical network infrastructure. Scalable wireless platforms enable seamless integration of devices, enhancing workflow efficiency. Advanced analytics and real-time data insights further strengthen decision-making, pushing healthcare institutions to accelerate adoption of connected, provider-focused wireless technologies.

End-user Insights

Providers are anticipated to dominate the market, with approximately 55% share in 2026, due to strong adoption across hospitals, clinics, and care facilities. Their need for efficient, real-time monitoring and integrated health systems drives widespread use. Growing patient volumes, demand for streamlined workflows, and focus on connected care further strengthen provider reliance on wireless solutions.

Payers are likely to be the fastest-growing, driven by insurers’ increasing focus on cost savings and preventive care. Data-driven monitoring tools help reduce hospitalizations, improve risk assessment, and support value-based reimbursement models. As insurers adopt connected health platforms to track patient outcomes, efficiency and care coordination improve, accelerating growth in the segment.

Regional Insights

North America Wireless Medical Technologies Market Trends

North America is projected to account for 40% of the share in 2026. The market is progressing rapidly as healthcare systems shift toward more connected, predictive, and patient-centric care models. The region’s strong digital infrastructure, widespread use of electronic health records, and early adoption of innovative medical devices provide a solid foundation for wireless integration. Hospitals and clinics are increasingly deploying wireless monitoring tools, wearable sensors, and mobile health platforms to improve chronic disease management, enhance care coordination, and support home-based treatment.

Advancements in AI, cloud computing, and 5G connectivity are enabling faster data transmission, real-time analytics, and seamless device interoperability across different clinical settings. This is helping providers move toward continuous monitoring and proactive intervention rather than traditional episodic care. The region also benefits from supportive policies that encourage telehealth expansion, remote patient monitoring reimbursement, and cybersecurity improvements.

Consumers in the U.S. and Canada are showing growing acceptance of digital health tools, driven by rising healthcare costs and a preference for convenient, personalized care options. This trend is fueling the adoption of wireless wearables, smart therapeutics, and connected diagnostic devices.

Europe Wireless Medical Technologies Market Trends

Europe is projected to account for 20% of the market share in 2026, as healthcare systems prioritize digitization, interoperability, and patient-centric care. The region is witnessing strong adoption of remote monitoring devices, telehealth platforms, and wireless diagnostic tools as hospitals seek to reduce clinical workloads and improve care efficiency. Aging populations, high chronic disease prevalence, and rising demand for home-based care are driving the shift toward continuous, real-time health tracking, supported by wireless connectivity.

European governments and regulatory bodies are accelerating digital health innovation through favorable frameworks, funding programs, and standards promoting data security, device integration, and cross-border health information exchange. These initiatives will enable seamless communication between medical devices, electronic health records, and cloud platforms.

Advancements in 5G networks, AI-powered analytics, and IoT-enabled sensors are enhancing the performance of connected medical systems across cardiology, neurology, diabetes care, and emergency response. Healthcare providers across Western and Northern Europe are leading early adoption, while Central and Eastern Europe are catching up with increasing investments in telemedicine infrastructure.

Asia Pacific Wireless Medical Technologies Market Trends

Asia Pacific is likely to be the fastest-growing market for wireless medical technologies, driven by rapid digital transformation, expanding healthcare infrastructure, and the rising adoption of connected medical devices. Countries such as China, India, Japan, and South Korea are accelerating investments in smart hospitals, telemedicine platforms, and remote patient monitoring systems, fueled by increasing chronic disease cases and a growing elderly population.

The region’s widespread smartphone penetration and improved 4G–5G connectivity are enabling seamless integration of wireless solutions across clinical and home-care settings. Governments are actively promoting digital health through initiatives supporting electronic health records, AI-enabled diagnostics, and IoT-based care models, which further strengthen market growth.

Local manufacturers are increasingly developing cost-effective wireless devices tailored for regional needs, improving accessibility in both urban and rural areas. The rise of medical wearables, such as continuous glucose monitors and wireless cardiac trackers, is enhancing patient engagement and preventive care adoption.

Competitive Landscape

The global wireless medical technologies market is highly competitive, driven by medtech leaders, telecom firms, and digital health innovators. In North America and Europe, companies such as Medtronic and GE Healthcare hold strong positions through advanced R&D, broad product portfolios, and established clinical partnerships. In Asia Pacific, players such as Huawei are accelerating growth with cost-effective connectivity solutions and 5G-enabled healthcare technologies. Rising adoption of smart devices, real-time monitoring, and AI-driven platforms is intensifying competition as companies pursue strategic partnerships and cross-industry collaborations.

Key Industry Developments

- In May 2025, Medtronic announced it had received the 2025 MedTech Breakthrough Award for ‘Best Overall Medical Device Solution’ for its HealthCast™ intelligent patient monitoring system, recognizing its commitment to advancing clinician support and patient care.

- In April 2024, GE HealthCare launched its Caption AI software on the Vscan Air SL wireless handheld ultrasound system. This technology provides AI-driven guidance and automated ejection fraction calculation to help clinicians capture diagnostic-quality cardiac images more easily.

Companies Covered in Wireless Medical Technologies Market

- Medtronic

- GE Healthcare

- Koninklijke Philips N.V.

- Siemens Healthineers

- Johnson & Johnson MedTech

- Dexcom

- Fitbit Health Solutions

- Samsung Electronics

- Baxter

- Oracle

Frequently Asked Questions

The global wireless medical technologies market is projected to reach US$57.0 billion in 2026.

The rising prevalence of telemedicine adoption and demand for remote patient monitoring are the key drivers.

The wireless medical technologies market is poised to witness a CAGR of 11.6% from 2026 to 2033.

Advancements in 5G-enabled mHealth and AI-driven diagnostics are the key opportunities.

Medtronic, GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers, and Johnson & Johnson MedTech are the key players.