- Chipsets & Processors

- Wireless Chipsets Market

Wireless Chipsets Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Wireless Chipsets Market by Connectivity (Wi-Fi & Bluetooth Combo, 5G & IoT Wireless ICs, ZigBee Chipsets), Application (Consumer Electronic, Industrial Automation, Others), End-User (Residential, Enterprise, Industrial, Automotive), and Regional Analysis for 2025-2032

Wireless Chipsets Market Share and Trends Analysis

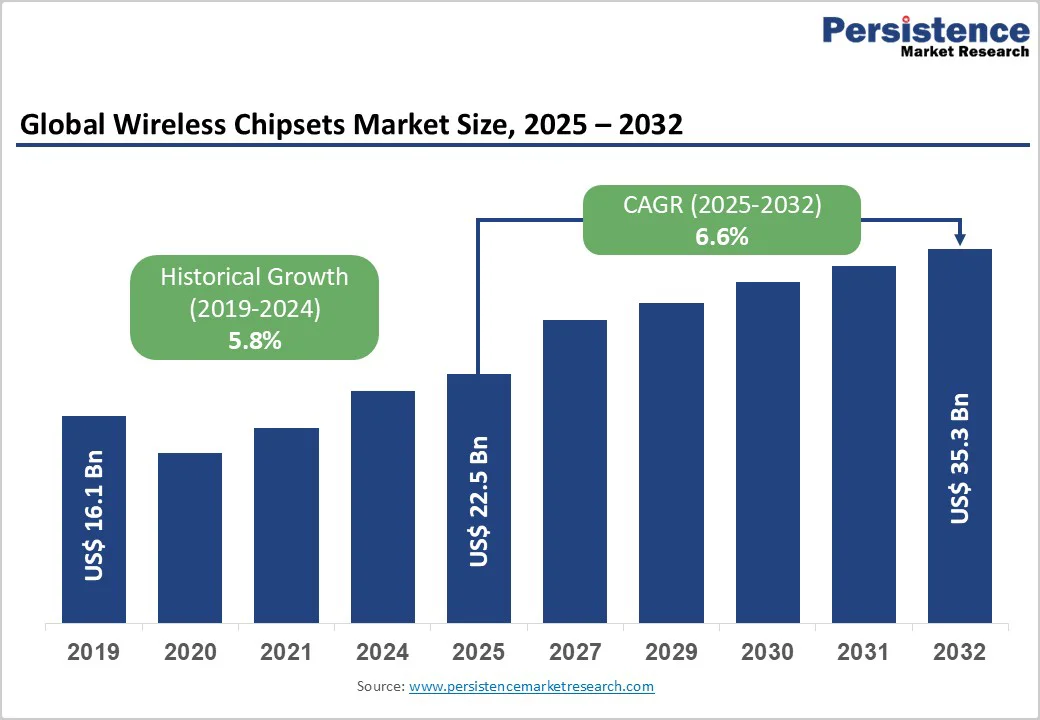

The global wireless chipsets market size is likely to be valued at US$ 22.5 billion in 2025 and is estimated to reach US$ 35.3 billion by 2032, growing at a CAGR of 6.6% during the forecast period 2025−2032. The market is expected to grow robustly on account of the surging demand for high-speed internet, proliferation of IoT-enabled devices, and expanding deployment of advanced wireless standards such as Wi-Fi 6 and 5G. The sector is experiencing renewed momentum from remote work trends, digital transformation initiatives across industries, and government-backed connectivity programs.?

Key Industry Highlights

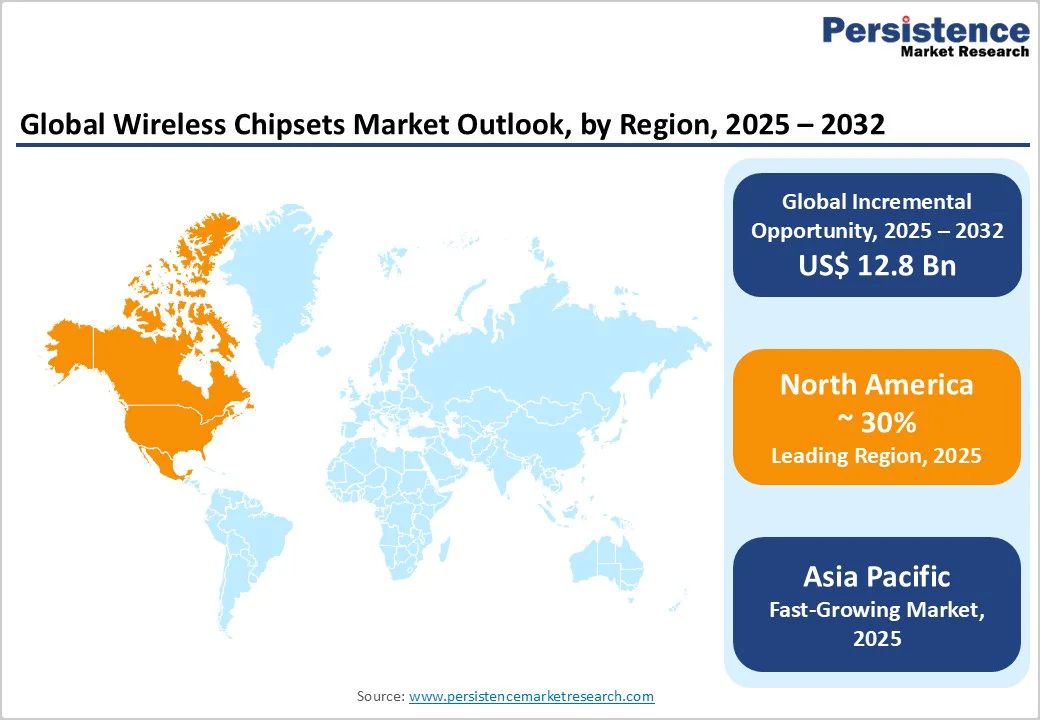

- Dominant Region: North America holds around 30% share in 2025, as regional stakeholders are integrating cutting-edge connectivity and rapid adoption of advanced Wi-Fi and 5G technologies.

- Fastest-growing Market: Asia Pacific is set to be the fastest-growing regional market from 2025 to 2032, fueled by the proliferation of digital infrastructure and expansive smart city projects in India and China.

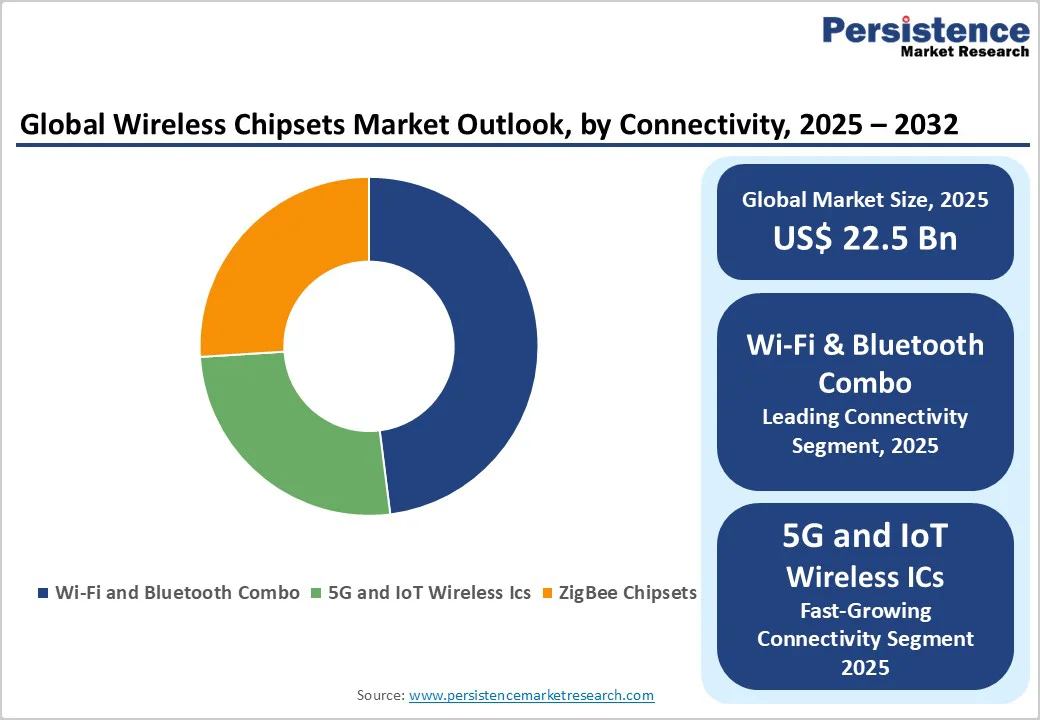

- Leading Connectivity: The Wi-Fi & Bluetooth segment commands around 48% in 2025 due to its ability to deliver multiple wireless functions within a single, integrated solution.

- Fastest-growing Connectivity: 5G & IoT wireless ICs are likely to be the fastest-growing segment through 2032, as they support the expansion of advanced, connected systems across multiple industries.

- Leading & Fastest-growing Application: Consumer electronics leads with an approximate 42% revenue share in 2025, while industrial automation and automotive are to grow the fastest boosted by rapid digital transformation and acceptance of smarter connected systems.

| Key Insights | Details |

|---|---|

|

Wireless Chipsets Market Size (2025E) |

US$ 22.5 Bn |

|

Market Value Forecast (2032F) |

US$ 35.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Widening Adoption of Mobile Phones and IoT Devices

Wireless chipsets serve as the backbone of modern connectivity, enabling seamless communication across an ever-expanding ecosystem of devices and industries. They provide the essential framework that allows smartphones, wearables, and smart home systems to interact effortlessly with one another and connect to cloud-based platforms. In consumer electronics, these chipsets deliver advanced functionalities such as real-time data access, remote operation, and uninterrupted multimedia streaming. By integrating these capabilities, manufacturers enhance user convenience, promote automation, and create more immersive and responsive digital experiences.

In industrial, healthcare, and automotive sectors, wireless chipsets drive innovation and operational efficiency. Within industrial environments, they enable reliable machine-to-machine communication that underpins predictive maintenance, data analytics, and continuous equipment monitoring, which are essential for Industry 4.0 transformation. In healthcare, connected medical devices equipped with wireless chipsets support remote patient monitoring and instantaneous data exchange between clinicians, improving care coordination and outcomes. Meanwhile, automotive applications leverage these technologies to enhance vehicle-to-vehicle and vehicle-to-infrastructure connectivity, power advanced driver assistance, and enrich in-car infotainment, advancing the evolution toward smarter, safer, and more autonomous mobility.

Regulatory Compliance and Security Risks

Wireless chipset manufacturers operate within an increasingly complex regulatory landscape shaped by evolving rules on spectrum allocation, device interoperability, and data security. Each geographic region enforces distinct standards governing frequency usage, wireless communication protocols, and electromagnetic emission limits, prompting manufacturers to customize designs to meet local compliance requirements. For instance, certification mandates such as the Conformité Européenne (CE) marking in Europe, Federal Communications Commission (FCC) approval in the United States, and Ministry of Internal Affairs and Communications (MIC) certification in Japan require rigorous documentation, device testing, and iterative product modifications. Managing these diverse obligations often extends development timelines, increases operational costs, and necessitates collaboration among engineering, legal, and compliance teams to ensure global market readiness.

As digital ecosystems expand, regulatory authorities are intensifying their focus on privacy protection and cybersecurity. This shift compels wireless chipset companies to strengthen data encryption frameworks, incorporate advanced device authentication mechanisms, and maintain secure over-the-air (OTA) update capabilities. The constant emergence of new cyber threats, including unauthorized network intrusions and data interception, drives ongoing investments in firmware resilience, intrusion detection systems, and real-time threat analytics. These efforts, while essential for safeguarding product integrity and consumer trust, add layers of complexity to product development and testing.

Growing Adoption of Consumer Electronics Devices

Wireless chipsets serve as vital enablers of connectivity across modern communication devices, particularly smartphones and tablets. These components support seamless integration with wireless standards such as Wi-Fi, cellular networks, and Bluetooth, empowering users to access the internet, make voice and video calls, send messages, and share data across multiple platforms. Their multifunctional capabilities enhance mobile device efficiency, enabling uninterrupted streaming, cloud synchronization, and location-based services that enrich the user experience. This level of performance and flexibility has made wireless chipsets indispensable in the design of next-generation smartphones and tablets, where high-speed connectivity and lower power consumption are critical differentiators in competitive markets.

In computing environments, wireless chipsets extend their utility to laptops and desktop systems, providing reliable Wi-Fi and Bluetooth connectivity for improved data access and device interoperability. These chipsets enable users to connect effortlessly with wireless peripherals such as keyboards, mice, printers, and headphones, reducing cable clutter while improving workplace ergonomics and convenience. The growing preference for wire-free computing and multimedia experiences has accelerated adoption among consumer electronics manufacturers. By supporting faster data transmission, secure network communication, and superior user mobility, wireless chipsets enhance both functionality and user satisfaction—positioning them as fundamental components in the continued evolution of connected consumer technologies.

Category-wise Analysis

Connectivity Insights

The Wi-Fi and Bluetooth combo segment is projected to hold the largest market share, approximately 48% in 2025, driven by its ability to integrate multiple wireless functions into a single, compact solution. This combination offers exceptional advantages for device manufacturers, including simplified design architecture, efficient power consumption, and lower overall bill of materials (BOM) costs. Such benefits make it the preferred option for high-volume consumer electronics such as smartphones, wearables, laptops, and smart home systems. By merging Wi-Fi for high-speed data transfer and Bluetooth for short-range communication, these combo chipsets enable seamless connectivity across diverse use cases, supporting the growing demand for stable, uninterrupted wireless interaction between devices.

The 5G and IoT wireless ICs segment is anticipated to exhibit the highest 2025-2032 CAGR, fueled by the proliferation of advanced, interconnected systems across industrial, healthcare, and urban infrastructures. These ICs provide ultra-reliable, low-latency communication capabilities that are essential for mission-critical applications such as real-time automation, predictive maintenance, and remote asset monitoring. Their energy-efficient design supports scalable deployment across battery-powered sensors, wearables, and IoT endpoints, enhancing cost efficiency and long-term sustainability. The integration of these ICs will accelerate digital transformation across sectors, enabling smarter factories, connected healthcare ecosystems, and intelligent city infrastructure characterized by high responsiveness and data-driven decision-making.

Application Insights

The consumer electronics segment dominates with an estimated 42% share in 2025, aided by the widespread use of connected personal devices such as smartphones, tablets, personal computers, and wearables. These devices rely on continuous and stable wireless connectivity to deliver essential functions such as real-time communication, high-definition multimedia streaming, and integration with smart home ecosystems. Manufacturers prioritize the integration of advanced wireless chipsets to enhance data transmission speed, improve user experience, and accommodate rapid feature upgrades aligned with evolving consumer needs. Growing global demand for connected devices, combined with the accelerated rollout of advanced Wi-Fi standards such as Wi-Fi 6 and Wi-Fi 6E, continues to strengthen this segment’s leadership position.

The industrial automation and automotive segment is emerging as the fastest-growing application, driven by rapid digital transformation and the increasing adoption of intelligent, connected infrastructure. In industrial environments, wireless chipsets play a pivotal role in enabling machine-to-machine communication, connecting IoT sensors, robotics, and monitoring systems that enhance production efficiency and operational flexibility. As factories evolve into fully integrated smart manufacturing spaces and vehicles become more autonomous and data-driven, the demand for high-performance, low-latency chipsets will continue to expand, fueling long-term growth across these technologically intensive sectors.

End-user Insights

The enterprise segment leads in 2025, holding an estimated 45% of the wireless chipset market revenue share. Enterprises across industries depend on wireless chipsets as the foundational enablers of their information technology (IT), telecommunications, and cloud infrastructure operations. These organizations require advanced connectivity solutions capable of supporting large-scale data transfer, managing complex network environments, and ensuring secure and reliable access across geographically distributed systems. Wireless chipsets enable high-performance communication between devices, servers, and applications, facilitating interoperability that is essential for cloud computing, unified communication systems, and digital collaboration platforms. As enterprises continue to invest in hybrid work models, edge computing, and advanced data analytics, the demand is likely to remain steady for chipsets that deliver low-latency performance, scalability, and robust network security.

The automotive sector represents the fastest-growing end-user, reflecting the industry’s rapid shift toward connected and intelligent mobility. Modern vehicles increasingly function as sophisticated digital platforms equipped with advanced wireless technologies for communication, entertainment, and safety. Automakers are integrating next-generation chipsets to enable vehicle-to-everything (V2X) communication, advanced driver assistance systems (ADAS), and immersive infotainment services. With electric and autonomous vehicle adoption accelerating, the integration of high-performance wireless solutions will be central to enabling OTA updates, fleet management, and system diagnostics, converting the automotive industry as a key driver of future market expansion.

Regional Insights

North America Wireless Chipsets Market Trends

North America is expected to account for approximately 30% of the wireless chipsets market share in 2025, bolstered by the region’s strong integration of advanced connectivity across industries. The United States, in particular, demonstrates rapid adoption of next-generation technologies such as 5G and advanced Wi-Fi standards, reinforcing North America’s leadership in global digital transformation. This dominance is underpinned by a well-established digital infrastructure, extensive use of smart devices, and the presence of leading semiconductor and networking technology companies. Ongoing investments in enterprise networking, industrial IoT systems, and cloud data centers, combined with high consumer demand for seamless, high-speed communication, continue to drive steady market expansion.

Early adoption of advanced chipset standards such as Wi-Fi 6, Wi-Fi 6E, and the emerging Wi-Fi 7 framework positions North American businesses and households at the forefront of connectivity innovation. Such advancements support a broad spectrum of applications, including high-resolution media streaming, smart home automation, industrial robotics, and connected vehicle platforms. The region’s market leadership is further reinforced by proactive government policies promoting spectrum availability, cybersecurity, and IoT innovation. Coupled with the strategic influence of global technology giants headquartered in the region, these initiatives ensure that North America remains the innovation benchmark for wireless chipset performance, deployment efficiency, and ecosystem maturity in the years ahead.

Europe Wireless Chipsets Market Trends

Europe continues to represent a strategic growth hub for wireless chipsets, with Germany, the U.K., France, and Spain serving as key centers of innovation, manufacturing, and deployment. The market here benefits from the European Union (EU)’s Digital Single Market framework, which supports regulatory harmonization and facilitates technology rollouts across member states. Germany and the U.K. lead technological advancement through significant research and development (R&D) investments and early industrial adoption of advanced wireless technologies, while France and Spain contribute to market expansion through rising digital infrastructure investments and smart connectivity initiatives.

The regional competitive landscape is marked by strong activity from leading semiconductor companies such as NXP Semiconductors N.V., Infineon Technologies AG, and STMicroelectronics N.V., complemented by ongoing mergers & acquisitions (M&A) and strategic collaborations aimed at expanding application focus and production capacity. Regulatory compliance and spectrum policy remain pivotal market drivers, influencing product certification, integration timelines, and regional market entry. Europe’s continued investment in industrial automation, 5G rollout, and smart home adoption reinforces long-term demand for high-performance chipsets.

Asia Pacific Wireless Chipsets Market Trends

Asia Pacific stands as the fastest-growing wireless chipsets market through 2032, propelled by a combination of demographic, technological, and policy-driven factors. China and India are spearheading demand through their large populations, accelerated urbanization, and rising disposable incomes, which in turn fuel high adoption rates of smartphones, IoT devices, and connected consumer electronics. The rapid expansion of digital infrastructure, coupled with the rollout of nationwide broadband and 5G networks, has transformed connectivity accessibility across both urban and rural areas. Extensive government-backed smart city initiatives are further strengthening the regional ecosystem by promoting real-time connectivity, intelligent transportation systems, and energy-efficient infrastructure—creating fertile ground for sustained wireless technology adoption.

The region’s robust manufacturing base and concentration of leading original equipment manufacturers (OEMs) such as MediaTek and Taiwan Semiconductor Manufacturing Company (TSMC) underpin its competitive advantage in cost-efficient chipset production. Proximity to these technology powerhouses enables faster innovation cycles and the swift deployment of next-generation wireless standards. Supportive government policies are encouraging intensified R&D investments and facilitating vertical-specific advancements in sectors such as automotive, industrial automation, and smart manufacturing.

Competitive Landscape

The global wireless chipsets market structure remains moderately consolidated, with Qualcomm, Intel, Broadcom, MediaTek, and Texas Instruments collectively commanding an estimated 58% share in 2025. These companies maintain their dominance through strong intellectual property (IP) portfolios, extensive R&D investments, and well-established partnerships across device manufacturers and network operators. Their ability to innovate consistently in areas such as 5G integration, Wi-Fi evolution, and energy-efficient design ensures sustained leadership in both consumer and industrial applications. This concentration of technological expertise and manufacturing capability provides these players with significant competitive and pricing advantages, setting a high performance benchmark within the global market.

The remaining market share is distributed among regional and niche vendors specializing in application-specific chipsets for sectors such as automotive, healthcare, and industrial automation. These companies often focus on customized design, low-power solutions, or mid-range connectivity standards to address specific performance requirements not fully covered by larger incumbents. As competition intensifies, differentiation through vertical integration, software-driven functionality, and strategic collaborations is expected to shape future market dynamics and open selective opportunities for specialized players operating within focused application domains.

Key Industry Developments

- In December 2025, Rohde & Schwarz deepened its collaboration with Broadcom to enable the testing and validation of next-generation Wi-Fi 8 chipsets using the CMP180 radio communication tester. The CMP180 has been validated by Broadcom as a comprehensive, future-proof solution that offers manufacturers accelerated time-to-market with pre-built test routines and ensures ultra-high reliability for demanding applications such as extended reality (XR) and AI.

- In August 2025, Silex Technology America launched the SX-SDMAX6E, a tri-band Wi-Fi 6E embedded module based on NXP Semiconductors’ IW623 chipset, targeting high-speed, low-power connectivity for medical, industrial, and factory automation applications. Featuring dual-stream support across 2.4/5/6 GHz bands, ultra-low-power SDIO 3.0 (Wi-Fi) and UART (Bluetooth) interfaces, and an industrial temperature range of -40°C to +85°C, it offers surface-mount and M.2 form factors with global regulatory compliance.

- In August 2025, LitePoint and Advantech partnered to develop next-generation industrial-grade Wi-Fi 7 modules, leveraging LitePoint’s advanced testing platform to ensure reliable, high-speed wireless connectivity for smart manufacturing, edge AI, and autonomous robotics applications. This collaboration aims to accelerate deployment of Wi-Fi 7 technology with enhanced performance, low latency, and robust validation for demanding industrial environments.

Companies Covered in Wireless Chipsets Market

- Qualcomm

- Intel Corporation

- Broadcom

- Texas Instruments

- MediaTek Inc.

- NVIDIA

- NXP Semiconductors

- Micron Technology, Inc

- TSMC

- Samsung Electronics

- Infineon Technologies

- STMicroelectronics

- Marvell Technology Group

- Realtek Semiconductor

- Apple Inc.

Frequently Asked Questions

The global wireless chipsets market is projected to reach US$ 137.2 billion in 2025.

The growing demand for Wi-Fi among SMEs and the rising demand for high-speed internet access and 5G networks are the major factors that are driving the market.

The market is poised to witness a CAGR of 6.6% from 2025 to 2032.

The rising adoption of cutting-edge technologies such as 5G and IoT is expected to generate multiple lucrative market opportunities.

Qualcomm, Intel Corporation, NVIDIA, and MediaTek Inc. are some of the key players in the market.