- Animal Health

- Veterinary Anti-Infectives Market

Veterinary Anti-Infectives Market Size, Share, Growth, and Regional Forecast, 2025 to 2033

Veterinary Anti-Infectives Market by Animal Type (Livestock Animals, Companion Animals), by Drug Class (Antimicrobial, Antiviral, Antifungal, Antiparasitic, Others), by Route of Administration (Oral, Parenteral, Topical), by Regional Analysis, from 2026 to 2033

Veterinary Anti-infectives Market Share and Trends Analysis

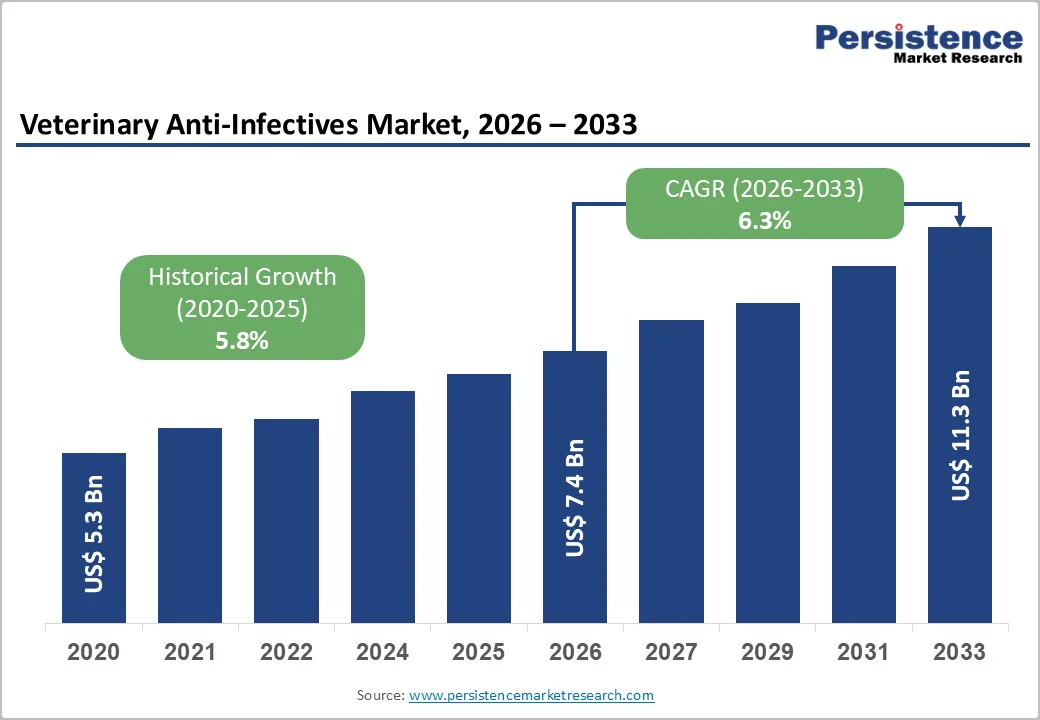

The global veterinary anti-infectives market size is estimated to grow from US$ 7.4 billion in 2026 to US$ 11.3 billion by 2033. The market is projected to record a CAGR of 6.3% during the forecast period from 2026 to 2033.

The market is expanding due to increasing antimicrobial use in food-producing animals, rising pet ownership, and heightened disease awareness. Usage reached nearly 99,500 tonnes in 2020 and is forecast to rise further by 2030. Global initiatives from WOAH, FAO, and WHO are shaping stewardship-aligned therapies and improving compliance. Major players such as Zoetis, Boehringer Ingelheim, Merck Animal Health, and Ceva are investing in targeted antimicrobials, vaccines, and diagnostic-supported treatment approaches, reinforcing the market’s transition toward safer, more responsible anti-infective utilization.

Key Industry Highlights:

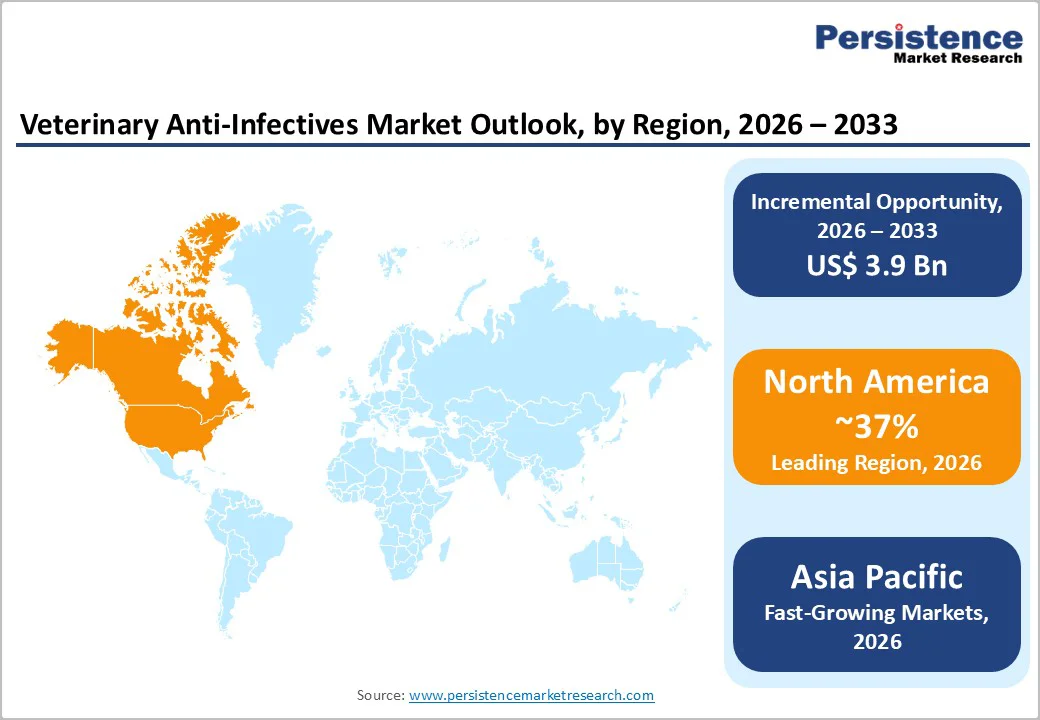

- Leading Region: North America leads the global market with approximately 37% share in 2025, supported by advanced veterinary infrastructure, high livestock and pet populations, and strong regulatory frameworks.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by expanding livestock production, rising meat and dairy consumption, increasing pet ownership, and growing adoption of veterinary healthcare services.

- Dominant Segment: Antimicrobials remain the dominant segment, accounting for the largest market share due to widespread use in livestock and companion animals to treat bacterial infections.

- Fastest Growing Segment: Antivirals are the fastest-growing segment, fueled by rising viral disease incidence, advances in veterinary antiviral therapies, and growing awareness of viral threats in livestock and pets.

| Key Insighst | Details |

|---|---|

| Veterinary Anti-Infectives Market Size (2026E) | US$ 7.4 Bn |

| Market Value Forecast (2033F) | US$ 11.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Dynamics

Driver - High Infectious Disease Burden in Livestock Production Systems

A key growth driver for the veterinary anti-infectives market is the substantial burden of infectious diseases in intensively managed livestock, including poultry, swine, and cattle. Global veterinary antimicrobial usage in food-producing animals was estimated at approximately 99,502 tonnes in 2020, with tetracyclines alone accounting for around 33,300 tonnes. This highlights the scale of bacterial disease pressure in intensive farming systems. Livestock diseases such as bovine respiratory disease, enteric infections, mastitis, and other systemic bacterial infections create persistent demand for antimicrobials like penicillins, cephalosporins, macrolides, quinolones, and tetracyclines. High-output protein production and export-oriented livestock operations further amplify the need for reliable anti-infective interventions to prevent economic losses and ensure animal health.

Projections indicate that antimicrobial usage in cattle, sheep, poultry, and pigs could grow by roughly 8% by 2030, with cattle alone contributing over 50% of total antimicrobial tonnage in some regions. This continued reliance on veterinary anti-infectives reflects both clinical necessity and economic incentives for maintaining herd health and productivity. As a result, the high disease burden in livestock production systems remains a fundamental driver sustaining robust market growth and revenue generation across global veterinary anti-infective segments.

Restraints - Shift Toward Alternatives and Preventive Health Approaches

Another restraining factor is the accelerated shift toward non-antibiotic alternatives and preventive measures such as vaccination, improved biosecurity, and management practices. Leading companies including Zoetis, Inc. have removed growth promotion indications for medically important antibiotics and have increased investment in vaccines and immune modulators that reduce the need for traditional anti-infectives. Global initiatives like the Health for Animals Roadmap to Reducing the Need for Antibiotics set sector-wide commitments to introduce alternatives and improve stewardship by 2025, encouraging producers to adopt integrated health programs rather than relying solely on anti-infective therapies. Over time, these shifts may moderate demand growth for some broad-spectrum antimicrobials, especially in high-compliance regions.

Opportunity - Expansion of Targeted Therapies and Stewardship-Aligned Solutions

A significant opportunity in the global veterinary anti-infectives market lies in the development and commercialization of targeted antimicrobial therapies and stewardship-aligned products. Growing concerns over antimicrobial resistance (AMR) are prompting regulators, producers, and veterinarians to prioritize precision use of anti-infectives over broad-spectrum, non-specific treatments. Innovations such as species-specific formulations, long-acting injectables, and combination therapies enable more effective disease management while minimizing drug resistance. Additionally, advancements in diagnostics, including rapid point-of-care testing and molecular pathogen identification, support timely and accurate treatment decisions, further enhancing market potential. Companies investing in such technologies can capture increasing demand from livestock operations focused on sustainable production practices and responsible antimicrobial use.

The expansion of companion animal ownership worldwide also presents a robust growth avenue, with pet owners seeking specialized anti-infective therapies and preventive solutions for common bacterial, viral, and parasitic infections. Alongside rising awareness of animal welfare and preventive care, veterinary hospitals and clinics are increasingly adopting innovative anti-infective products integrated with digital health tools and herd management solutions. These trends create opportunities for both multinational and regional players to introduce value-added products, expand their market presence, and strengthen the adoption of responsible, outcome-driven anti-infective therapies globally.

Category-wise Analysis

By Animal Type Insights

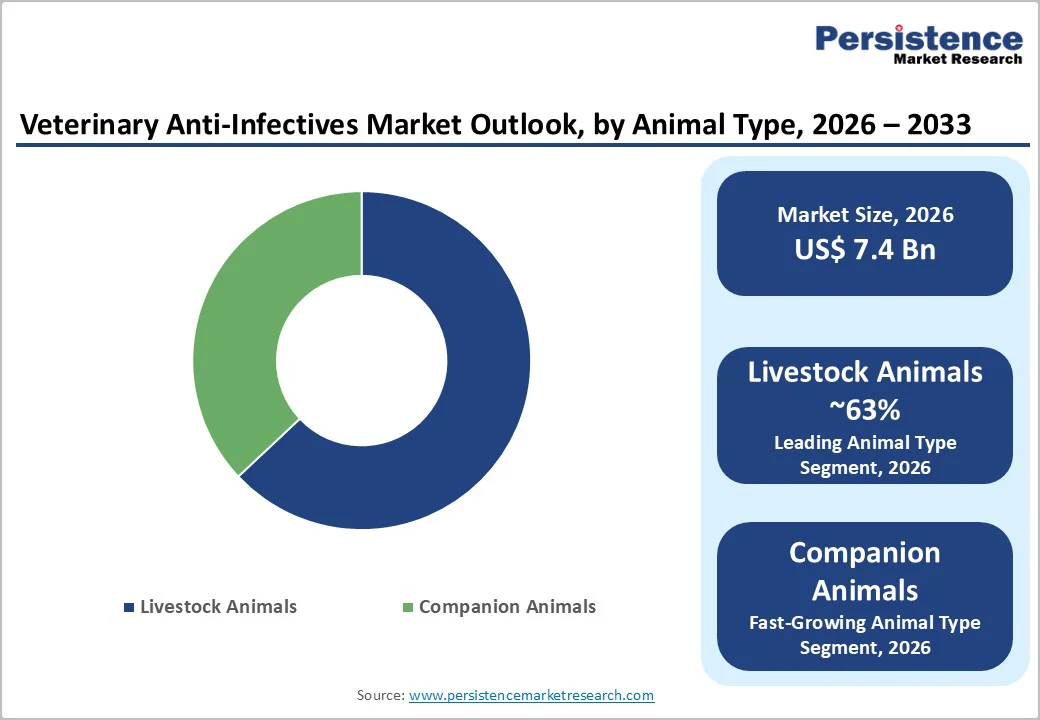

The livestock segment dominated the veterinary anti-infectives market in 2025, accounting for approximately 63% of total revenue. Key subcategories include cattle, sheep, goats, swine, poultry, and fish. High disease prevalence in these animals and routine use of anti-infective treatments for prevention and therapy underpin this dominance. Rising global demand for animal protein further intensifies the need for effective interventions. For example, India’s meat production reached 10.25 million metric tons (MMT) in 2023-24, a 4.95% increase from the previous year, with poultry contributing over 5 MMT and buffalo meat 4.57 MMT, making India the fifth-largest meat producer globally. Growing emphasis on food safety, productivity, and sustainable farming practices also supports continued anti-infective adoption across livestock operations.

The companion animal segment is projected to record the fastest growth due to increasing pet ownership and rising awareness of preventive veterinary care. Owners are investing in specialized anti-infective products to maintain pet health, driven by emotional bonding and the recognition of pets’ benefits for mental and cardiovascular well-being.

By Drug Class Insights

The antimicrobials segment holds the largest share of the veterinary anti-infectives market, accounting for close to half of total demand in 2025. Its position is supported by widespread use in livestock and companion animals to manage respiratory infections, enteric diseases, and systemic bacterial conditions. Cephalosporins, penicillins, tetracyclines, and macrolides remain essential therapeutic classes prescribed in both farm and clinical settings. Rising focus on herd health programs, food safety regulations, and consistent disease surveillance keeps antimicrobial usage high across poultry, cattle, and swine operations. Regulatory frameworks that promote judicious antibiotic administration have not reduced necessity but redirected demand toward monitored usage and improved formulations.

The antiviral segment is projected to expand at the fastest rate, driven by escalating prevalence of economically damaging viral diseases such as lumpy skin disease in cattle, porcine reproductive-respiratory syndrome, and avian viral infections. Growing research investments, disease outbreaks affecting trade, and increased veterinary vaccination coverage further accelerate product development and commercialization of targeted antiviral therapies.

Region-wise Insights

North America Veterinary Anti-Infectives Market Trends

North America, led by the U.S., accounts for approximately 37% of the global veterinary anti-infectives market in 2025, driven by high livestock and companion animal populations and advanced veterinary infrastructure. The region hosts leading animal health companies such as Zoetis, Merck Animal Health, Elanco Animal Health, and Phibro Animal Health Corporation, generating substantial revenues from diverse product portfolios. Regulatory oversight by the U.S. FDA and Health Canada has restricted the use of medically important antibiotics for growth promotion, promoting their application for therapeutic and preventive purposes under veterinary supervision. This regulatory environment, combined with stewardship initiatives including antimicrobial resistance (AMR) surveillance, vaccine development to reduce antibiotic dependency, and proper disposal campaigns, fosters responsible product use.

High pet ownership, robust companion animal healthcare, and strong poultry, beef, and dairy industries maintain consistent demand for anti-infectives. Integration of diagnostics, digital herd management systems, and precision dosing technologies is accelerating, supported by research collaborations and investments. Mature distribution networks across veterinary hospitals, clinics, and pharmacies ensure efficient product availability. These factors collectively position North America as the leading regional market while setting global standards for sustainable veterinary anti-infective practices and innovation.

Asia Pacific Veterinary Anti-Infectives Market Trends

Asia Pacific veterinary anti-infectives market is projected to be the fastest-growing globally, fueled by rapid livestock expansion and rising consumption of meat and dairy products in China, India, Southeast Asia, and East Asia. Intensive farming systems and large animal populations in cattle, swine, and poultry generate significant demand for anti-infective products, including antimicrobials, antivirals, antifungals, and antiparasitics. China and India alone account for more than 40% of the world’s cattle, highlighting the region’s substantial growth potential. Rising incomes and changing dietary preferences are prompting producers to invest in health interventions to prevent disease, improve productivity, and meet domestic and export quality standards.

Governments in China, India, and ASEAN countries are increasingly aligning with FAO and WOAH guidelines to monitor antimicrobial use and combat resistance, creating a more structured stewardship environment. Asia-Pacific is also a major manufacturing hub for veterinary medicines, with local and multinational companies producing formulations and active pharmaceutical ingredients for domestic and international markets. Companies such as Zoetis, Merck Animal Health, Ceva, Cipla, and Neogen are expanding through partnerships, localized formulations, and technical support, combining rising demand with evolving regulations to drive long-term market growth.

Competitive Landscape

The veterinary anti-infectives market is moderately consolidated, with a core group of global animal health leaders such as Zoetis, Inc., Boehringer Ingelheim GmbH, Merck & Co., Inc. (Merck Animal Health), Eli Lilly and Company (Elanco Animal Health), Bayer AG, Ceva Santé Animale, Vetoquinol S.A., Virbac S.A., and Phibro Animal Health Corporation controlling a significant share of revenues, complemented by regional generic manufacturers and niche specialists. These companies pursue strategies centered on portfolio diversification (combining antimicrobials with vaccines, parasiticides, and diagnostics), geographic expansion into high-growth emerging markets, and R&D investments targeting stewardship-aligned products and innovative delivery systems. Emerging business models emphasize integrated health solutions, including digital decision-support tools, AMR surveillance services, and value-based partnerships with producer groups and veterinary networks, which help differentiate market leaders beyond pure product supply.

Key Industry Developments:

- In January 2025, the Federation of Veterinarians of Europe launched the Alternatives to Veterinary Antibiotics (AVANT) initiative, aimed at minimizing antimicrobial use in livestock through the development and promotion of effective non-antibiotic solutions, enhancing animal health and welfare, and supporting sustainable farming practices.

- In July 2024, Boehringer Ingelheim GmbH revealed investment plans to launch up to 20 new animal health products by 2026, focusing largely on anti-infectives and respiratory disease management.

- In June 2024, Zoetis, Inc. reported ongoing advancements in its antibiotic stewardship program, featuring expanded AMR monitoring and new vaccines to reduce antibiotic use in cattle and poultry.

Companies Covered in Veterinary Anti-Infectives Market

- Bayer AG

- Cipla Limited

- Dechra Pharmaceuticals PLC

- Eli Lilly and Company (Elanco Animal Health)

- Heska Corp (Diamond Animal Health)

- Merck & Co., Inc. (Merck Animal Health)

- Neogen Corporation

- Phibro Animal Health Corporation

- Sanofi (Merial Animal Health)

- Vetoquinol S.A.

- Virbac S.A.

- Zoetis, Inc.

- Boehringer Ingelheim GmbH

- Ceva Santé Animale

- Others

Frequently Asked Questions

The global veterinary anti-infectives market is projected to be valued at US$ 7.4 Bn in 2026.

Rising companion animal ownership, zoonotic disease incidence, livestock productivity needs, antimicrobial resistance monitoring, and greater veterinary healthcare expenditure stimulate demand.

The global anti-infectives market is poised to witness a CAGR of 6.3% between 2026 and 2033.

Development of targeted antimicrobial therapies, broad-spectrum formulations, residue-free products, and precision dosing technologies, alongside expanding veterinary hospitals and livestock integration programs.

Major players include Bayer AG, Cipla Limited, Dechra Pharmaceuticals PLC, Eli Lilly and Company (Elanco Animal Health), Merck & Co., Inc. (Merck Animal Health), Zoetis, Inc., Boehringer Ingelheim GmbH, Ceva Santé Animale.