- Medical Devices

- Sleep Aid Devices Market

Sleep Aid Devices Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Sleep Aid Devices Market by Product (Wearables, Non-wearables, and Others), by Application (InsoBnia, Obstructive Sleep Apnea, Narcolepsy, and Others), by End User (Hospitals, Specialty Clinics, and Home Care Settings), and Regional Analysis from 2026 to 2033.

Sleep Aid Devices Market Share and Trends Analysis

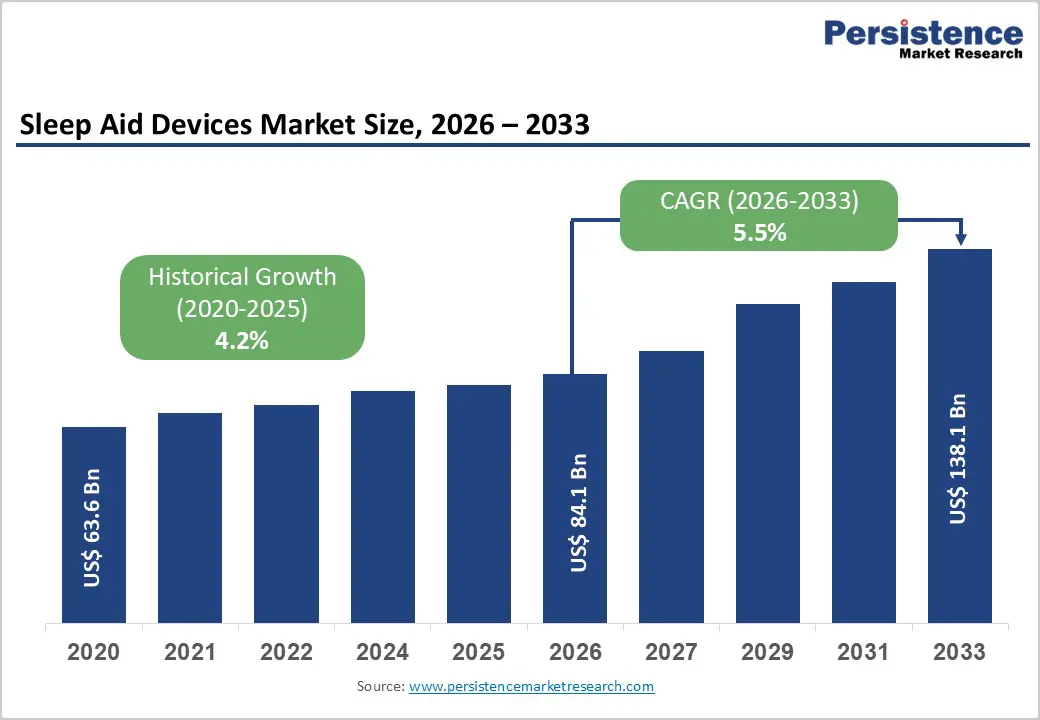

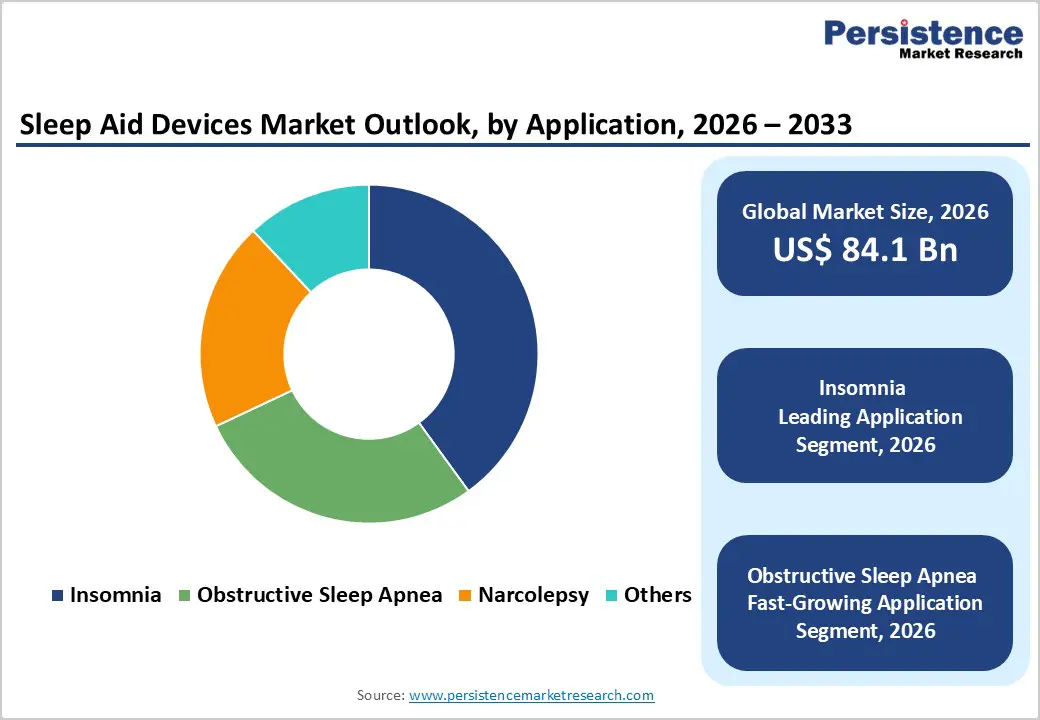

The global sleep aid devices market size is estimated to grow from US$ 84.1 billion in 2026 to US$ 138.1 billion by 2033, growing at a CAGR of 5.5% during the forecast period from 2026 to 2033.

Global demand for sleep aid devices is increasing steadily, driven by the rising prevalence of sleep disorders such as insomnia, obstructive sleep apnea, and circadian rhythm disturbances, along with growing awareness of sleep health as a core component of overall well-being. Lifestyle changes, increased screen exposure, stress, obesity, and aging population are contributing to poor sleep quality across both younger and older demographics, supporting sustained market growth. Increasing preference for non-pharmacological and home-based sleep management solutions is accelerating the adoption of wearable devices, sleep monitors, and smart beds.

Wider clinical acceptance of device-assisted sleep diagnosis and therapy, combined with the convenience of continuous monitoring and minimal intervention, is further strengthening demand. Rising disposable incomes, higher healthcare spending, and growing integration of digital health technologies are reinforcing market expansion. Continuous innovation in sensor technology, AI-driven sleep analytics, remote monitoring, and personalized therapy features is improving diagnostic accuracy, patient compliance, and long-term engagement. Additionally, the shift toward preventive healthcare, outpatient sleep management, and connected wellness ecosystems is further propelling the global sleep aid devices market.

Key Industry Highlights:

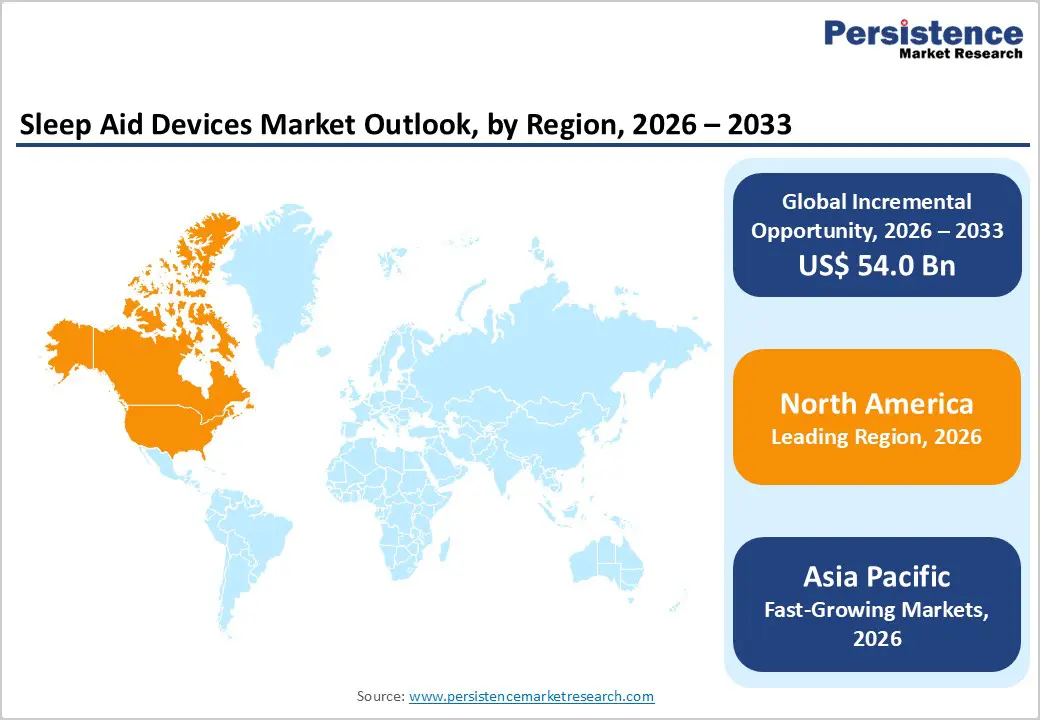

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high awareness of sleep disorders, strong adoption of wearable and connected sleep technologies, and widespread availability of sleep clinics and home-based diagnostic solutions.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large population base, rising incidence of sleep disorders, increasing disposable incomes, growing digital health adoption, and improving access to sleep diagnostics and home care solutions.

- Leading Application Segment: Insomnia dominates the market due to its high global prevalence, growing demand for non-drug sleep management, and widespread use of wearable and monitoring devices for long-term tracking and behavioral intervention.

- Fastest-Growing Application Segment: Obstructive sleep apnea is expanding rapidly as demand increases for advanced diagnostic, monitoring, and therapy-support devices that improve treatment adherence and clinical outcomes.

- Leading End User Segment: Hospitals remain the top segment, driven by high volumes of sleep disorder diagnosis, availability of specialized sleep labs, and use of advanced monitoring and therapeutic devices.

- Fastest-Growing End User Segment: Home care settings are scaling quickly as patients increasingly prefer convenient, non-invasive, and remotely monitored sleep solutions that support long-term disease management and comfort.

| Key Insights | Detailss |

|---|---|

| Sleep Aid Devices Market Size (2026E) | US$ 84.1 Bn |

| Market Value Forecast (2033F) | US$ 138.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Rising Burden of Sleep Disorders and Shift Toward Non-Pharmacological Sleep Management

Increasing prevalence of sleep disorders such as insomnia, obstructive sleep apnea, and circadian rhythm disruptions is a major factor supporting long-term market expansion. Modern lifestyles characterized by prolonged screen exposure, irregular work schedules, stress, and sedentary behavior have significantly worsened sleep quality across age groups. At the same time, growing awareness of the side effects and dependency risks associated with sleep medications has accelerated the shift toward non-pharmacological, device-based interventions. Consumers and healthcare providers increasingly prefer sleep aid devices that enable monitoring, behavioral modification, and therapy support without chemical intervention.

Technological advancements are further amplifying adoption. Innovations in wearable sensors, AI-driven sleep analytics, cloud connectivity, and remote monitoring platforms are improving diagnostic accuracy and treatment personalization. Devices now provide actionable insights into sleep stages, breathing patterns, and oxygen saturation, supporting early intervention and chronic condition management. Rising integration of sleep monitoring into preventive healthcare and chronic disease management programs is also expanding clinical use. Additionally, increasing acceptance of home-based sleep diagnostics and telemedicine-supported sleep care is reinforcing demand, making sleep aid devices an essential component of modern sleep health management.

Restraints – Data Privacy Concerns, Device Accuracy Limitations, and Cost Barriers

Market growth faces constraints related to data security concerns, variability in device accuracy, and affordability challenges. Sleep aid devices increasingly rely on continuous data collection, cloud storage, and mobile applications, raising concerns around patient privacy, cybersecurity, and compliance with data protection regulations. In regions with stringent digital health laws, manufacturers face higher compliance costs, which can slow product launches and limit market penetration.

Another key limitation is variability in clinical accuracy, particularly among consumer-grade wearables. Differences in sensor quality, algorithm validation, and calibration standards can lead to inconsistent sleep metrics, reducing confidence among clinicians and conservative patient groups. While advanced hospital-grade systems offer higher precision, their elevated costs restrict widespread adoption outside specialized settings. Affordability remains a challenge in price-sensitive markets, especially where sleep diagnostics and devices are not reimbursed. High upfront costs for smart beds, CPAP-integrated monitoring systems, and subscription-based analytics platforms may deter long-term use. Limited awareness in rural areas, lack of trained sleep specialists, and uneven healthcare infrastructure further constrain adoption in developing regions.

Opportunity – Growth of Home-Based Care, AI-Enabled Personalization, and Emerging Market Penetration

Expanding demand for home-based and self-managed healthcare solutions presents a strong opportunity for future growth. Consumers increasingly seek convenient, comfortable sleep monitoring and therapy options that can be used outside clinical settings. Advancements in connected wearables, contactless sleep monitors, and smart beds are enabling continuous at-home assessment while maintaining clinical relevance. Integration of artificial intelligence and machine learning allows for highly personalized sleep insights, predictive analytics, and adaptive therapy recommendations, enhancing long-term user engagement.

Emerging economies across Asia Pacific, Latin America, and the Middle East represent significant untapped potential. Rising disposable incomes, rapid urbanization, and growing awareness of sleep health are driving demand for affordable and scalable sleep solutions. Expansion of telehealth platforms and digital health ecosystems is further improving access in underserved regions. Manufacturers also have opportunities through product differentiation, including hybrid diagnostic-therapy devices, subscription-based sleep coaching services, and integration with broader wellness ecosystems. Strategic partnerships with hospitals, insurers, and digital health platforms, along with investments in clinical validation and localized manufacturing, are expected to unlock sustained growth opportunities over the forecast period.

Category-wise Insights

By Product, Wearables Lead Due to Continuous Monitoring, Personalization, and Consumer Adoption

Wearable devices are projected to dominate the global sleep aid devices market in 2026, accounting for a revenue share of 38.0%. This leadership is driven by their ability to provide continuous, real-time sleep tracking across multiple parameters such as sleep stages, heart rate variability, oxygen saturation, and movement. Smart watches and bands enable high treatment personalization through AI-driven analytics and mobile app integration, allowing users to modify sleep behavior and therapy based on individual patterns. High consumer acceptance, ease of use, and compatibility with remote monitoring platforms support widespread adoption. Wearables are increasingly preferred for insomnia, sleep quality assessment, and long-term sleep health management due to their non-invasive nature. Ongoing advancements in sensor accuracy, battery life, and data interpretation algorithms are further strengthening clinician and consumer confidence. Additionally, frequent device upgrades, subscription-based software features, and recurring engagement cycles significantly contribute to revenue concentration, reinforcing the dominance of the wearables segment globally.

By Application Insights

The insomnia segment is projected to dominate the global sleep aid devices market in 2026, capturing a revenue share of 40.0%. This dominance is primarily driven by the rising global prevalence of chronic and lifestyle-induced insomnia, particularly among working-age and elderly populations. Increasing awareness of the long-term side effects associated with sleep medications has accelerated demand for non-pharmacological solutions such as sleep tracking devices, smart wearables, and behavioral therapy-enabled platforms. Sleep aid devices offer real-time insights into sleep duration, latency, and disturbances, supporting early diagnosis and personalized management. Strong consumer demand for home-based, non-invasive sleep solutions, coupled with growing stress levels, screen exposure, and irregular sleep patterns, further fuels adoption. Healthcare providers increasingly recommend digital sleep solutions as adjuncts to cognitive behavioral therapy for insomnia (CBT-I). High recurrence rates, long-term monitoring needs, and growing preventive health awareness continue to position insomnia as the leading application segment.

By End-user Insights

Hospitals are expected to dominate the global sleep aid devices market in 2026, accounting for a revenue share of 45.0%. This leadership is attributed to the high volume of patients undergoing sleep disorder diagnosis and treatment in hospital-based sleep labs and specialized departments. Hospitals are primary centers for managing complex conditions such as obstructive sleep apnea, narcolepsy, and comorbid sleep disturbances linked to cardiovascular and metabolic disorders. Availability of advanced diagnostic infrastructure, including polysomnography systems and integrated monitoring devices, supports large-scale adoption of sleep aid technologies. Hospitals also benefit from trained sleep specialists, standardized clinical protocols, and higher patient trust, particularly for device-based therapies such as CPAP and smart sleep monitoring systems. Integration with electronic health records and reimbursement-backed diagnostic procedures further strengthens hospital adoption. As sleep disorders increasingly intersect with chronic disease management, hospitals continue to remain the leading end-user segment globally.

Regional Insights

North America Sleep Aid Devices Market Trends

North America is expected to dominate the global sleep aid devices market with a value share of 47.3% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare ecosystem, strong awareness of sleep health, and early adoption of digital health and connected medical devices. High prevalence of insomnia and obstructive sleep apnea, driven by obesity, stress, and sedentary lifestyles, significantly supports market demand. Consumers in North America show strong acceptance of wearable sleep trackers, smart beds, and CPAP-integrated monitoring systems, particularly for home-based care.

Favorable reimbursement frameworks for sleep diagnostics, widespread availability of sleep clinics, and strong physician recommendations enhance device adoption. The presence of leading global manufacturers and continuous innovation in AI-enabled sleep analytics further strengthen regional leadership. Additionally, increasing focus on preventive healthcare, personalized medicine, and remote patient monitoring continues to reinforce North America’s dominant position in the global sleep aid devices market.

Europe Sleep Aid Devices Market Trends

Europe sleep aid devices market is expected to grow steadily, supported by rising awareness of sleep disorders and an expanding aging population across countries such as Germany, the U.K., France, Italy, and Spain. Strong public and private healthcare systems enable broad access to sleep diagnostics and treatment services, including hospital-based sleep labs and home sleep testing solutions. European consumers demonstrate a growing preference for non-invasive, technology-driven health monitoring solutions, supporting adoption of wearable sleep trackers and smart monitoring devices. Regulatory frameworks emphasizing device safety, data protection, and clinical validation strengthen patient and physician confidence.

Growth is further supported by increasing diagnosis rates of sleep apnea, expanding geriatric care, and integration of sleep monitoring into chronic disease management programs. Rising healthcare digitalization, coupled with continuous innovation by regional and global players, supports sustained adoption. Overall, Europe is expected to maintain stable, long-term growth in the sleep aid devices market.

Asia Pacific Sleep Aid Devices Market Trends

Asia Pacific sleep aid devices market is expected to register a relatively higher CAGR of around 7.5% between 2026 and 2033, driven by rapid healthcare modernization and a large, increasingly health-conscious population. Countries such as China, India, Japan, South Korea, and Australia are witnessing rising incidence of sleep disorders due to urbanization, long working hours, and lifestyle changes. Growing awareness of sleep health, supported by digital health campaigns and increasing physician engagement, is accelerating adoption of wearable and home-based sleep monitoring devices.

Expansion of private hospitals, specialty sleep clinics, and telehealth platforms is improving access to sleep diagnostics and therapy. Government initiatives supporting digital health infrastructure, along with rising disposable incomes, further support market growth. Additionally, local manufacturing, competitive pricing, and strategic expansion by global players are improving affordability, positioning Asia Pacific as the fastest-growing regional market for sleep aid devices.

Competitive Landscape

The global sleep aid devices market is highly competitive, with strong participation from companies such as Koninklijke Philips N.V., DECKMOUNT, ResMed, Fitbit (Google LLC), Apple Inc., and Eight Sleep. These players leverage established global distribution networks, strong brand recognition, and diversified sleep technology and digital health product portfolios to address rising demand for non-pharmacological diagnosis, monitoring, and management of sleep disorders.

Their offerings emphasize advancements in sensor accuracy, AI-driven sleep analytics, device comfort, therapy effectiveness, patient safety, and ease of home use, supporting widespread adoption across hospitals, sleep clinics, and home care settings. Continuous product innovation, regulatory compliance, and adherence to international quality standards remain critical to sustaining competitive positioning in the global sleep aid devices market.

Key Industry Developments:

- In June 2025, Somnee, a leading sleep technology company specializing in AI-powered neurotechnology and software solutions, announced that it secured $10 million in a seed extension funding round. Founded in 2022 by renowned sleep scientist Dr. Matt Walker, PhD, along with a team of researchers from the University of California, Berkeley, the company focuses on advancing personalized, science-driven sleep optimization technologies.

- In September 2023, Beacon Biosignals announced that it received FDA 510(k) clearance for Dreem 3S, an advanced wearable headband that uses integrated machine learning algorithms to capture electroencephalogram (EEG) data for monitoring sleep architecture and supporting the diagnosis of sleep disturbances.

Companies Covered in Sleep Aid Devices Market

- Koninklijke Philips N.V.

- DECKMOUNT

- Resmed

- Fitbit (Google LLC)

- Apple Inc

- Eight Sleep

- Xiaomi

- Sleep Number

- Rest

- SleepScore Labs,

- Withings's

- Nox Medical Global

- ProSomnus Sleep Technologies.

Frequently Asked Questions

The global sleep aid devices market is projected to be valued at US$ 84.1 Bn in 2026.

Rising prevalence of sleep disorders, increasing health awareness, growing demand for non-drug AI/IoT-enabled sleep solutions, expanding healthcare access in emerging markets, and an aging population drive market growth.

The global sleep aid devices market is poised to witness a CAGR of 5.5% between 2026 and 2033.

Expansion into emerging markets with rising awareness and disposable incomes, combined with AI/IoT-enabled personalized and integrated smart sleep solutions, represents the most significant growth opportunity.

Koninklijke Philips N.V., DECKMOUNT, Resmed, Fitbit (Google LLC), Apple Inc., and Eight Sleep are some of the key players in the sleep aid devices market.