- Consumer Goods

- Sleepwear Market

Sleepwear Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Sleepwear Market by Product Type (Top Wear, Night Dresses & Nightgowns, Robes & Lounge Shirts, Shorts & Tops, Others), Material (Cotton, Silk, Wool, Synthetic Blends), End-User (Women, Men, Children), and Regional Analysis for 2026 - 2033

Sleepwear Market Share and Trends Analysis

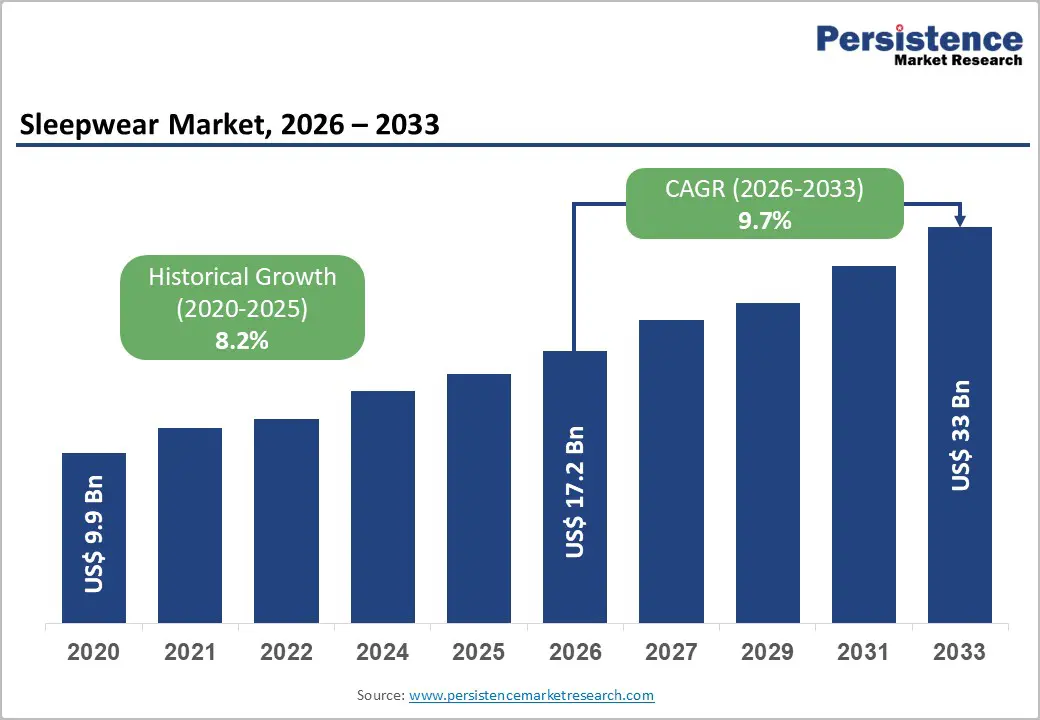

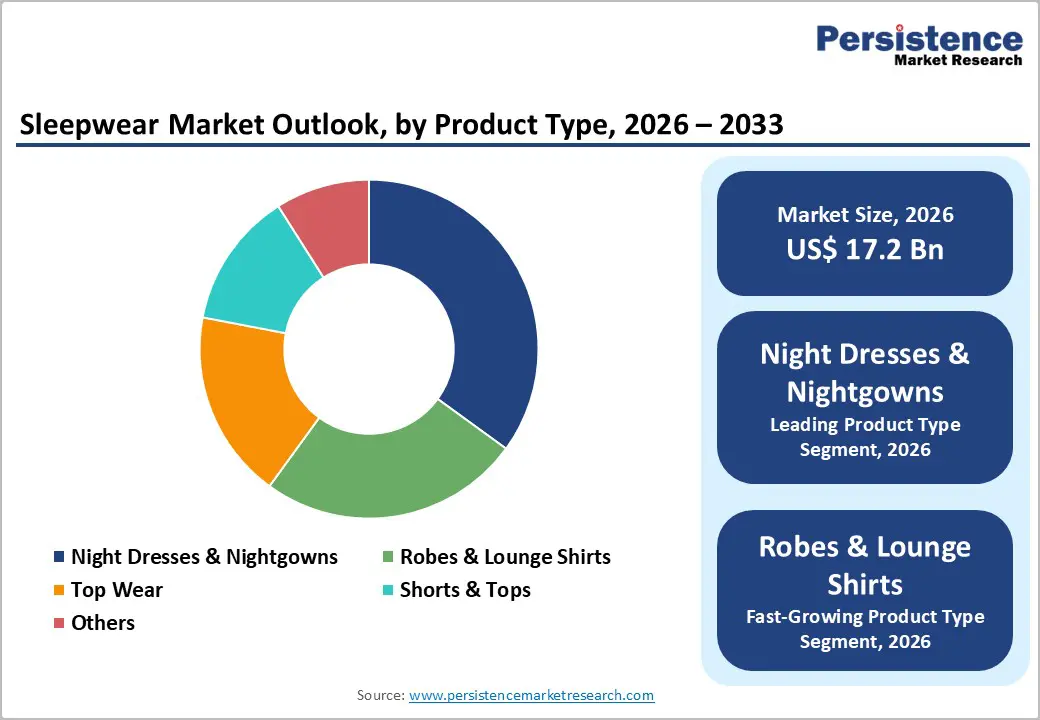

The global sleepwear market size is likely to be valued at US$ 17.2 billion in 2026, and is projected to reach US$ 33.0 billion by 2033, growing at a CAGR of 9.7% during the forecast period 2026 - 2033.

Sustained demand growth is driven by demographic expansion, rising awareness of sleep quality, and increasing adoption of functional sleepwear. Growing prevalence of sleep disorders and related health complications strengthens focus on preventive and therapeutic solutions, expanding the addressable market. Technological integration, including smart fabrics and wearable monitoring systems, improves functionality and supports targeted use.

Urbanization, lifestyle shifts, and income growth enhance accessibility and affordability, especially in emerging markets. Advancements in healthcare infrastructure, along with expanding retail and distribution networks, improve availability. Supportive regulatory frameworks for safety, hygiene, and environmental standards build consumer trust and reduce barriers to adoption.

Key Industry Highlights

- Leading Product Type: Night dresses & nightgowns are projected to lead the market with over 35% share in 2026, supported by ergonomic designs and widespread accessibility.

- Fastest-Growing Product Type: Robes & lounge shirts are projected to be the fastest-growing segment from 2026 to 2033 due to multifunctional usage and smart fabric adoption.

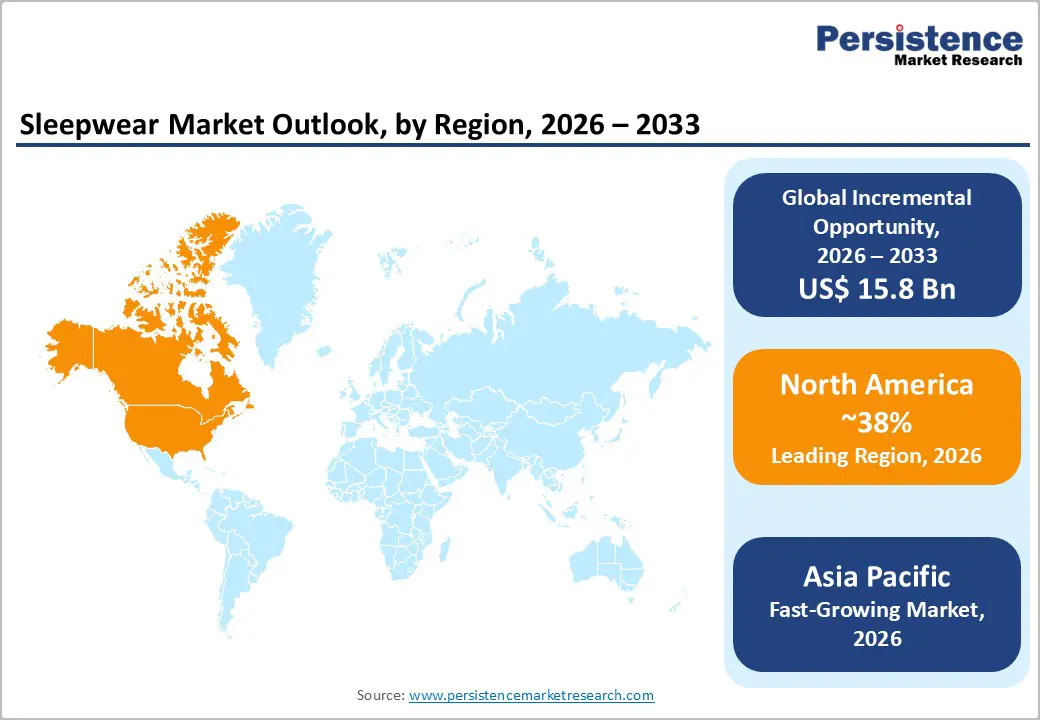

- Dominant Region: North America is projected to dominate with around 38% market share in 2026, supported by regulatory frameworks.

- Fastest-growing Regional Market: Asia Pacific is expected to be the fastest-growing market between 2026 and 2033, stimulated by urbanization and disposable income growth.

- Innovation Trends: Smart fabrics, wearable integration, and sustainable materials drive product differentiation, strengthen adoption rates, and support scalable market expansion.

- March 2026: Bebe launched a Betty Boop-inspired sleepwear collection, enhancing brand visibility through pop-culture licensing and targeting younger consumers.

| Key Insights | Details |

|---|---|

| Sleepwear Market Size (2026E) | US$ 17.2 Bn |

| Market Value Forecast (2033F) | US$ 33.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.2% |

DRO Analysis

Growing Comfort-wear Demand to Boost Sleepwear Sales

Rising preference for comfort-oriented apparel reshapes consumer purchasing patterns across the sleepwear market. Work-from-home models, flexible schedules, and increased time spent indoors elevate demand for garments designed for relaxation and extended wear. Consumers prioritize breathable fabrics, ergonomic fits, and skin-friendly materials, which directly increases product turnover. As per the U.S. Census Bureau, online apparel sales accounted for over 38% of total apparel retail in 2025, reflecting a structural shift toward casual and comfort categories. This shift strengthens sales velocity, supports premium product positioning, and expands average transaction values across digital and organized retail channels globally.

Evolving lifestyle patterns reinforce continuous demand across multiple consumer segments, including working professionals, millennials, and aging populations seeking enhanced comfort. Retailers respond through portfolio expansion, integrating loungewear-inspired sleepwear collections aligned with daily utility. This alignment improves inventory rotation and reduces demand uncertainty. Manufacturers benefit from streamlined production cycles focused on high-volume comfort fabrics such as cotton blends and modal. Strong alignment between consumer expectations and product design drives repeat purchases and brand loyalty. Rising exposure through digital platforms and targeted marketing further accelerates category penetration, strengthening revenue consistency and supporting long-term demand expansion across both developed and emerging economies.

Integration of Sleepwear into Daily Wear to Fuel Market Growth

Evolving fashion preferences position comfort-oriented apparel within everyday wardrobes, which elevates demand across the sleepwear market. Consumers seek versatile garments suitable for both indoor and casual outdoor use, which expands usage frequency and purchase intent. Retailers align product design with contemporary fashion aesthetics, which increases category relevance and pricing power. Digital channels strengthen visibility and accelerate trend diffusion across demographics. According to the U.S. Census Bureau, total U.S. retail e-commerce sales reached 1,233.7 billion in 2025, indicating strong digital retail infrastructure that supports rapid adoption of fashion-driven apparel categories.

Integration into daily wear strengthens demand elasticity and reduces dependence on traditional nightwear consumption patterns. Production strategies align with fast-cycle fashion models, which improves responsiveness to evolving consumer preferences. Brand portfolios expand into lifestyle positioning, which increases cross-category engagement and repeat purchases. Omnichannel distribution enhances product accessibility and conversion efficiency across physical and digital platforms. This structural shift increases addressable market size, strengthens inventory turnover, and supports margin expansion through higher-value product positioning aligned with everyday fashion consumption behavior.

Limited Awareness of Technical Fabrics to Reduce Uptake

Limited awareness of technical fabrics constrains demand formation within the market by weakening perceived value among end users. Consumers often associate sleepwear with basic comfort, leading to preference for conventional cotton products instead of advanced moisture-wicking or temperature-regulating materials. This perception gap reduces willingness to pay premium prices, limiting revenue expansion for manufacturers investing in innovation. Product differentiation remains unclear in the absence of consumer education, which reduces the effectiveness of branding and positioning strategies. As a result, innovation-led offerings struggle to achieve scale despite strong functional advantages.

Retail and distribution channels face challenges in communicating fabric performance, which reduces conversion rates and slows inventory turnover. Sales teams in mass retail environments often lack technical expertise, resulting in limited product explanation at the point of purchase. Marketing strategies shift toward price competition instead of value-driven messaging, compressing margins across the value chain. Limited understanding of durability and performance benefits restricts repeat purchases and weakens customer retention. This dynamic discourages investment in advanced materials and slows the transition toward higher-value product segments across the industry.

Low-cost Alternatives to Create Strong Competition

Price-sensitive consumers frequently shift toward inexpensive, mass-produced garments that meet basic utility expectations. This behavior weakens demand for branded and premium sleepwear, limiting revenue expansion across organized players. A large base of unorganized manufacturers sustains continuous supply of low-cost products, creating persistent pricing pressure. This structure lowers entry barriers and increases market saturation, leading to constrained margins and limited scope for differentiation. Established brands face difficulty in communicating value beyond price, which reduces conversion rates and restricts premium segment growth within both offline and online retail channels.

Operational advantages within low-cost segments further intensify competitive pressure. Simplified designs, lower-grade inputs, and minimal branding investment enable aggressive pricing across distribution networks. Consumers focused on affordability prioritize price over durability or fabric innovation, reducing demand for advanced features. Retailers respond by allocating more shelf space to high-turnover, low-priced products to sustain sales velocity. This dynamic limits visibility for premium offerings and slows adoption of innovation such as sustainable materials and enhanced comfort technologies, which affects long-term profitability and discourages investment in differentiated product development.

Designer Collaborations to Expand Premium Offerings

Designer collaborations elevate perceived value through brand equity transfer, enabling premium pricing across curated sleepwear collections. Established designers introduce distinct aesthetics, limited editions, and signature elements that differentiate offerings within a crowded apparel landscape. This differentiation strengthens consumer willingness to pay and supports margin expansion. Limited-run collections create urgency, accelerating purchase decisions and reducing inventory holding periods. Retailers benefit from higher sell-through rates and improved margin realization. Strategic alignment with well-known designers enhances brand credibility, attracting aspirational consumers and strengthening competitive positioning across premium apparel segments.

Collaborations streamline product innovation cycles by combining creative expertise with established production capabilities, improving speed to market. Brands leverage co-creation to introduce new fabrics, silhouettes, and thematic designs with controlled risk exposure. This approach expands product portfolios while maintaining operational efficiency. Consumer engagement strengthens through storytelling, influencer alignment, and cross-brand promotion, driving higher conversion rates. Premium segments expand as buyers seek differentiated and experience-driven apparel. Retailers gain higher average transaction values and stronger brand recall, supporting sustained revenue growth and reinforcing long-term market differentiation through structured partnership models.

Smart Textiles to Offer Innovation Potential

Integration of smart textiles into the sleepwear market introduces advanced functionality aligned with rising demand for health-oriented and performance-driven apparel. Embedded sensors enable tracking of sleep patterns, body temperature, and heart rate, creating a differentiated product category with clear value addition. This capability supports premium pricing and strengthens positioning in high-income consumer segments. Manufacturers gain scope for partnerships with technology firms, accelerating innovation cycles and enhancing product portfolios. Continuous development of conductive fibers and wearable components improves product reliability, encouraging consumer adoption and reinforcing brand competitiveness within an evolving apparel landscape.

Operational efficiency improves through fabrics that actively regulate temperature and moisture, reducing dependence on multiple product variants. This capability supports streamlined inventory structures and better resource utilization across supply chains. Demand expands as consumers engage with wellness ecosystems where connected garments integrate with digital health platforms and mobile applications. Retailers benefit from stronger engagement and higher repeat purchases driven by personalized data insights. Advancements in scalable production techniques reduce unit costs over time, enabling wider accessibility while maintaining margins. This convergence of textile engineering and digital functionality strengthens long-term growth potential and opens new revenue streams across premium and mid-tier segments.

Category-wise Analysis

Product Type Insights

Night dresses & nightgowns are anticipated to secure around 35% of the sleepwear market share in 2026, reflecting consistent consumer preference for comfort-oriented, versatile sleepwear. The segment benefits from preference for lightweight, breathable designs that support sleep quality across adult and older demographics. Retail visibility across offline and digital channels ensures wide accessibility. Fabric innovation, including temperature regulation and hypoallergenic properties, strengthens trust and differentiation. Brands emphasize design variety, functional features, and seasonal launches, supporting steady demand and repeat purchase patterns.

Robes & lounge shirts are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by rising adoption of multifunctional sleepwear that bridges relaxation, home leisure, and wellness applications. Demand rises with preference for versatile apparel supporting comfort and light activity. Smart fabrics improve thermal control and moisture management. E-commerce growth expands direct access and personalization. Urban lifestyles promote extended wear beyond bedtime. Sustainable materials and antimicrobial features strengthen acceptance and repeat usage.

Material Insights

Cotton extracts are poised to dominate with a forecasted market share of over 40% in 2026, powered by consumer trust, cultural acceptance, and broad retail penetration. Natural breathability, softness, and hypoallergenic properties support comfortable sleep conditions. Strong retail and e-commerce networks ensure wide accessibility. Rising awareness of skin-friendly textiles drives preference. Digital commerce supports branded product reach and repeat purchases. Reliable supply chains enable efficient scaling and consistent quality.

Synthetic blends are estimated to be the fastest-growing segment from 2026 to 2033, fueled by advancements in textile engineering and demand for multifunctional fabrics. Blends with polyester, modal, or bamboo deliver moisture control, thermal regulation, and durability. Online retail and direct-to-consumer models expand accessibility and awareness. Smart textiles enable integration with sleep monitoring features. Wellness-driven lifestyles increase demand for adaptable fabrics. Customization and digital marketing support adoption and scalable growth.

Regional Insights

North America Sleepwear Market Trends and Insights

North America is expected to lead with an estimated 38% of the sleepwear market share, fueled by high per capita apparel expenditure and strong alignment with premium lifestyle positioning across United States and Canada. Consumers prioritize comfort-driven clothing integrated with daily routines, supporting consistent demand for high-quality sleepwear. Established retail ecosystems, including department stores and digital marketplaces, enable rapid product visibility and efficient distribution. Brand concentration supports continuous product innovation and targeted marketing strategies. High penetration of private labels strengthens competitive pricing structures while maintaining margins. Demand stability benefits from frequent product refresh cycles and strong engagement with seasonal collections.

Market dominance is reinforced by advanced supply chain infrastructure and efficient inventory management systems across United States, Canada, and Mexico, supporting rapid replenishment and reduced stockouts. Strong adoption of digital commerce platforms enhances direct-to-consumer engagement and personalized product offerings. Consumer preference for sustainable and ethically sourced materials drives premium product positioning and higher average selling prices. Integration of data analytics in merchandising improves demand forecasting and assortment planning. Retailers emphasize curated collections and exclusive launches to sustain consumer interest. High brand loyalty and repeat purchase behavior contribute to stable revenue streams and sustained market control across multiple distribution channels.

Europe Sleepwear Market Trends and Insights

Europe demonstrates steady demand for comfort-oriented and sustainable sleepwear, driven by strong consumer preference for high-quality fabrics and design-focused apparel. Purchasing behavior reflects emphasis on durability, skin-friendly materials, and seasonal adaptability, supporting premium product positioning. Well-established retail networks and fashion chains ensure structured distribution and consistent brand visibility. Sustainability standards influence material selection, with rising demand for organic cotton and recycled fibers. Countries such as Germany and France contribute significantly through high purchasing power, refined fashion sensibilities, and increasing alignment with eco-conscious textile consumption patterns.

Market structure reflects strict regulatory frameworks governing textile safety, labeling, and environmental compliance, shaping sourcing and production decisions. Countries such as United Kingdom and Italy influence category evolution through innovation in fabric development and luxury-oriented designs. E-commerce penetration supports cross-border accessibility and enables emerging brands to gain visibility. Retail strategies focus on curated collections, limited editions, and transparency in material sourcing to attract informed consumers. Stable replacement cycles and preference for long-lasting garments sustain consistent demand across both premium and mid-range product segments.

Asia Pacific Sleepwear Market Trends and Insights

Asia Pacific is forecasted to be the fastest-growing market for sleepwear between 2026 and 2033, propelled by rapid income expansion and shifting consumption toward lifestyle-oriented apparel. Urban population growth supports higher demand for organized retail and branded products. Digital commerce penetration accelerates product discovery and purchase frequency. China drives volume growth through large-scale manufacturing ecosystems and strong domestic consumption. India supports expansion through rising middle-income households and increasing online retail adoption. Product affordability across varied price tiers enables wider consumer participation and faster market scaling across metropolitan and semi-urban clusters.

Growth momentum strengthens through evolving consumer preferences aligned with comfort, wellness, and multifunctional apparel usage. Japan and South Korea influence premium segment expansion through innovation in fabric technology and design aesthetics. Regional manufacturing advantages enable cost-efficient production and flexible supply chain operations. Local brands leverage digital marketing and influencer engagement to accelerate adoption among younger consumers. Expansion of direct-to-consumer models enhances brand visibility and margin control. Increasing focus on sustainable materials and climate-adaptive fabrics supports product differentiation and faster acceptance across diverse climatic conditions.

Competitive Landscape

The global sleepwear market reflects a moderately fragmented structure, where leading global apparel brands such as Hanesbrands, PVH, Lululemon Athletica, UNIQLO, and Fruit of the Loom maintain a strong presence alongside niche players focused on functional and smart sleepwear. These key participants collectively account for nearly 40-45% of total market share, while several regional manufacturers sustain competitive intensity through localized offerings and pricing strategies across diverse consumer segments.

Market concentration varies across regions, with North America and Europe exhibiting higher consolidation driven by established brands and technology-integrated products. Asia Pacific presents a more fragmented landscape supported by domestic manufacturers and new international entrants. Competitive positioning centers on product differentiation through innovation, sustainable materials, and technology-enabled features. Companies prioritize expansion of distribution networks, strengthening of brand credibility, and adoption of digital commerce platforms to enhance consumer reach.

Key Industry Developments

- In December 2025, Hanna Andersson partnered with Oeuf to launch a coordinated sleepwear capsule featuring family-oriented pajama sets and lifestyle accessories, strengthening premium sleepwear positioning through design-led collaboration and multi-generational appeal.

- In June 2025, Four Seasons Hotels and Resorts expanded its sleepwear portfolio with a new resort-inspired pajama collection featuring linen-cotton sets designed for summer comfort, reinforcing premium positioning and extending its signature sleep experience into home-based luxury lifestyle offerings.

- In May 2025, womenswear brand Ammarzo expanded its portfolio with the launch of a premium sleepwear collection crafted from natural fabrics, strengthening positioning in the evolving luxury sleepwear segment and addressing rising demand for comfort-driven and wellness-oriented apparel.

Companies Covered in Sleepwear Market

- HANESBRANDS LLC.

- PVH Corp.

- lululemon athletica

- UNIQLO Co., Ltd.

- Fruit of The Loom, Inc.

- Calvin Klein.

- Victoria's Secret.

- Jockey

- Marks & Spencer Group plc

- Gildan Activewear S.R.L.

- Chico's Distribution Services, LLC.

- Decathlon Sports India Pvt Ltd.

- H&M Group

Frequently Asked Questions

The global sleepwear market is projected to reach US$ 17.2 billion in 2026.

Rising consumer focus on comfort, wellness, and lifestyle-oriented apparel is driving the demand for sleepwear.

The market is poised to witness a CAGR of 9.7% from 2026 to 2033.

Expansion of sustainable fabrics, smart textiles, and direct-to-consumer digital channels is unlocking novel growth opportunities in the market.

Some of the key market players include Hanesbrands, PVH, Lululemon Athletica, UNIQLO, and Fruit of the Loom.