- Biotechnology

- Single-Use Bioprocess Systems Market

Single-Use Bioprocess Systems Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Single-Use Bioprocess Systems Market by Component (Bioreactors, Mixers, Bioprocess Containers, Transfer and Storage Bags, Sampling Systems, Others), by Application (Research & Development (R&D), GMP and Commercial Production), End-user, Regional Analysis, from 2026 to 2033

Singe-use Bioprocess Systems Market Share and Trends Analysis

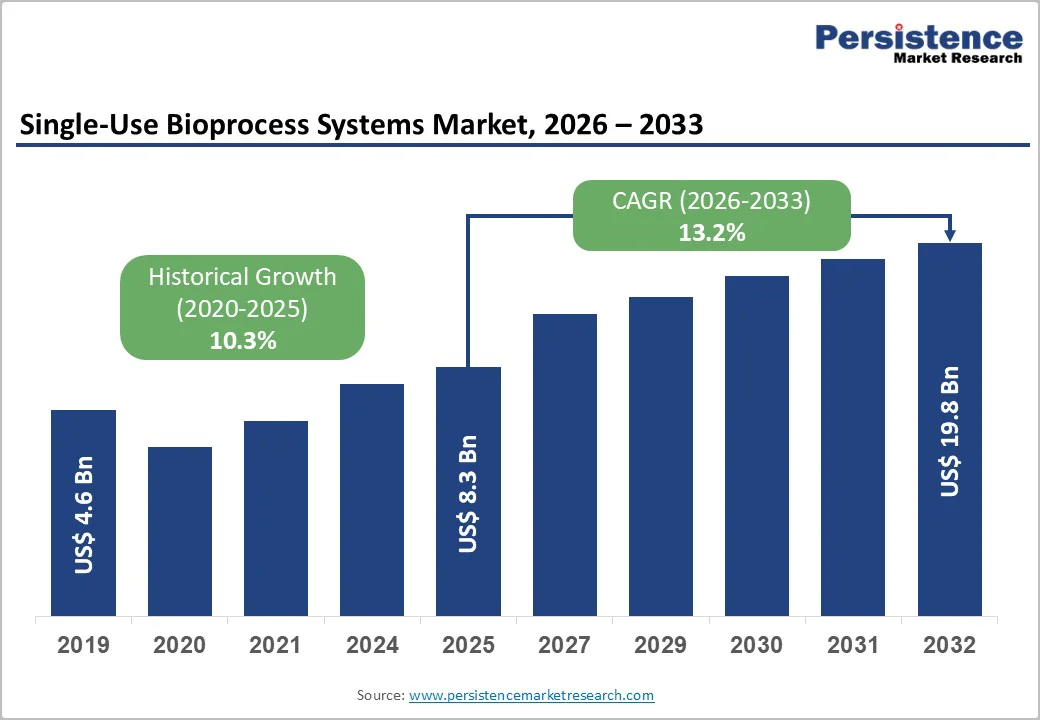

The global single-use bioprocess systems market size is likely to value at US$ 8.3 billion in 2026 and projected to reach US$ 22.4 billion by 2033, growing at a CAGR of 13.2% during the forecast period from 2026 to 2033.

Several end-users view single-use systems (SUS) as an economically viable strategy to attain the highest level of productivity and process efficiency. SUS equipment is therefore extensively used throughout the biomanufacturing phase, especially in the production of pre-commercial biopharmaceuticals.

The single-use bioprocess systems market is driven by vendors offering sustainable disposables, which overcome drawbacks of traditional stainless-steel bioreactors, including reduced cleaning, sterilization, and potential cost savings. Automation advancements, incorporating big data and machine learning for predictive analytics, are enhancing biomanufacturing efficiency and product yields.

Increasing investments in R&D for sustainable single-use solutions are expected to further accelerate market growth over the next decade.

Key Industry Highlights:

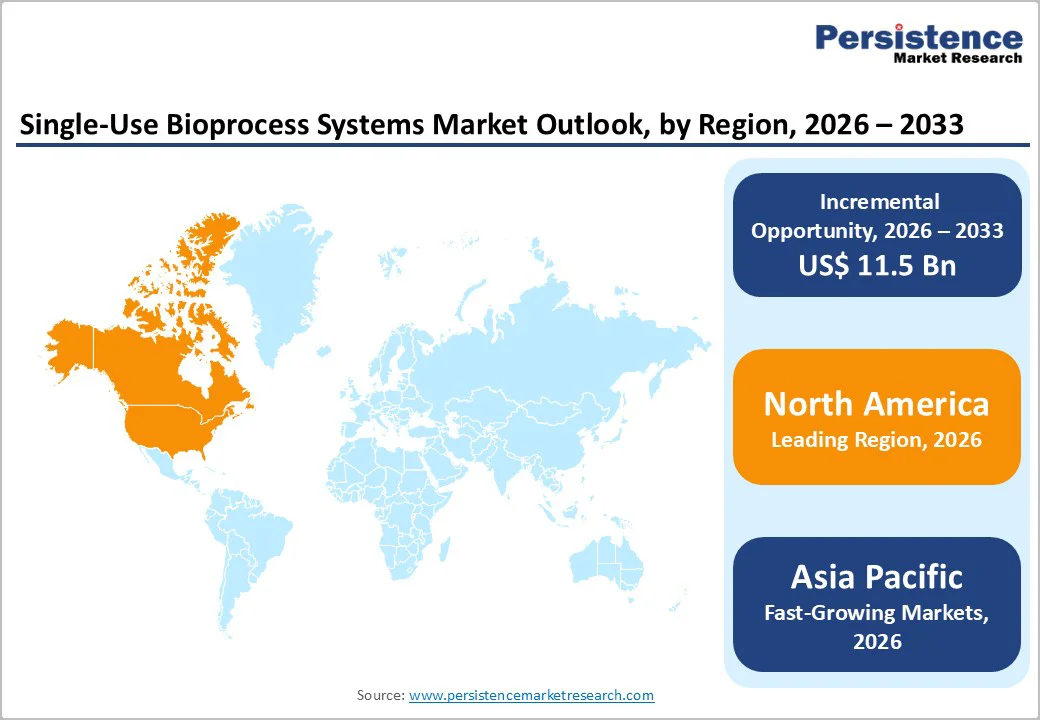

- Leading Region: North America holds the largest market share, supported by industry-leading infrastructure and robust regulatory support for single-use platforms.

- Fastest Growing Region: Asia Pacific is the fastest growing region, fueling adoption across vaccine and biosimilar production, thanks to scalable digital manufacturing.

- Dominant Segment: Bioreactors are the dominant component segment, leading single-use bioprocess systems in capacity expansion and GMP compliance.

- Fastest Growing Segment: R&D applications are emerging as the fastest growing segment, driven by biopharma investments and frequent process changeovers.

| Key Insights | Details |

|---|---|

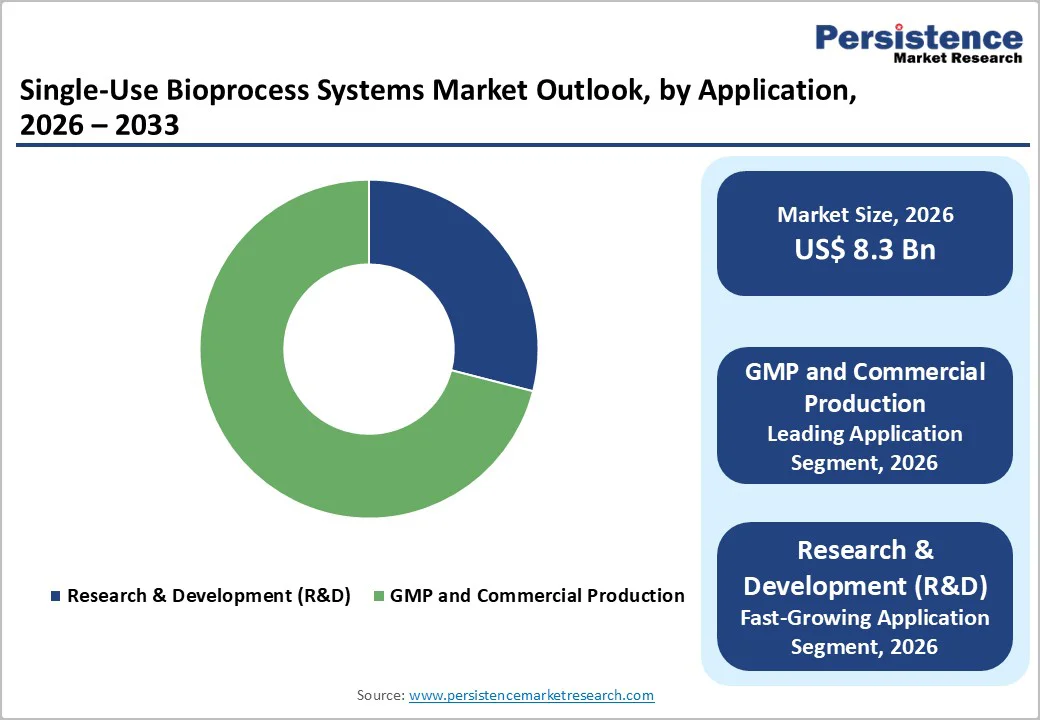

| Single-Use Bioprocess Systems Market Size (2026E) | US$ 8.3 Bn |

| Market Value Forecast (2033F) | US$ 19.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.3% |

Market Dynamics

Driver - Technological Adoption Transforming Single-use Bioprocessing Systems Sector

With ongoing technological upgradation and high investments by companies to make unique single-use bioprocess systems, the focus has shifted from conventional steel bioreactors to disposable single-use bioreactors that are easier and cheaper to use. Furthermore, they provide high energy efficiency and reduce the chances of cross-contamination.

For instance, companies such as ThermoFisher Scientific, Eppendorf AG, Merk KGaA, and Danaher Corporation, are developing single-use bioprocessing systems and components.

For instance, in September 2021, Merck released the ProCellics Raman Analyzer with Bio4C PAT Raman software for upstream monoclonal antibody and vaccine process development and manufacture, which provides a GMP-ready platform for in-line and real-time monitoring of cell culture crucial process parameters and critical quality attributes.

The introduction of new technologies is expected to result in higher adoption rates, which will, in turn, drive market growth during the forecast period.

Manufacturers are also investing a lot of time in research and development to produce single-use bags as they are easily disposable and provide efficient temperature resistance, strength of usage, and are also quite durable. The successful launch of disposable bags of various sizes will help market leads expand their businesses with a larger product portfolio and capture a share in untapped markets.

Furthermore, with increased demand for disposable sensors and probes in the biopharmaceutical industry, new market entrants are also trying to expand their businesses by offering a wide range of products.

Restraints - Increasing Cost of Consumables and Rising Industrial Pollution

The single-use bioprocess systems market is facing notable restraints linked to both cost pressures and environmental concerns. Consumables associated with single-use platforms such as bags, filters, tubing sets, and connectors continue to rise in price due to manufacturing complexity, strict regulatory requirements, and dependence on high-grade raw materials.

As operating budgets tighten, this cost burden limits wider adoption, particularly among small and mid-scale biopharmaceutical manufacturers. Alongside financial challenges, the growing scrutiny around industrial waste is another factor slowing down market momentum.

Although the bioprocessing sector represents only a small share of global plastic consumption, the accumulation of single-use components after each production cycle contributes to the industry’s environmental footprint.

The hesitation of smaller companies to invest in sustainable materials or recycling-focused product development further intensifies this issue. As a result, environmental pressure from regulatory bodies, sustainability initiatives, and public expectations are expected to weigh on the market over the coming years, creating a barrier to otherwise robust demand.

Opportunity - Rise in Opportunity in Smart, Sensor-Integrated Single-Use Bioprocessing Platforms

The growing shift toward automated, sensor-integrated single-use bioprocessing systems presents a significant opportunity for market expansion. Biopharmaceutical companies prefer platforms that offer real-time visibility into critical process parameters, ensuring tighter control, higher reproducibility, and reduced risks of batch failure.

The introduction of disposable sensors for pH, dissolved oxygen, temperature, pressure, and metabolites eliminates the need for manual measurement and reduces contamination risks, which is especially valuable in high-value production environments such as mAbs, vaccines, and cell and gene therapies.

As developers aim to shorten development timelines and streamline tech transfers across global sites, automation combined with closed-loop digital control greatly accelerates process scale-up from bench to commercial scale. Sensor-equipped systems also reduce labor dependency and enable continuous data-driven optimization, supporting regulatory expectations for process transparency and traceability.

With companies advancing smart platform portfolios tailored for GMP and multi-product facilities, demand for integrated single-use automation solutions is expected to surge across CDMOs, biopharma innovators, and emerging biotech firms, unlocking substantial growth potential for suppliers.

Category-wise Analysis

By Component Insights

Bioreactors represent the leading component in the single-use bioprocess systems market, accounting for an estimated 43% share of the global market in 2024. Their dominance is closely tied to the expanding landscape of biopharmaceutical production, where flexibility, faster turnaround, and reduced risk of cross-contamination have become essential.

Demand has surged particularly in developed regions such as North America and Europe, where the number of biopharmaceutical firms, CDMOs, and CMOs continues to rise. At the same time, increasing investments in biologics, including monoclonal antibodies, vaccines, cell therapies, and gene therapies, have accelerated the shift from traditional stainless-steel reactors to single-use platforms.

These systems minimize cleaning and sterilization requirements, shorten batch-to-batch changeover time, and improve operational efficiency, making them well-suited for high-mix, multiproduct manufacturing environments. As biologics pipelines grow worldwide and smaller players enter commercial-scale production, the adoption of single-use bioreactors is expected to remain a key driver of segment expansion.

By Application Insights

GMP and commercial production account for the largest share of the single-use bioprocess systems market, contributing about 71% in 2024. Their strong position reflects the industry’s shift toward large-scale biologics manufacturing, where efficiency, contamination control, and fast turnaround are crucial.

Single-use technologies eliminate the need for intensive cleaning and sterilization, enable swift batch changeovers, and support multi-product facilities, making them particularly valuable for contract manufacturers and pharmaceutical companies handling diverse product portfolios.

The increasing commercial availability of monoclonal antibodies, vaccines, cell therapies, and gene therapies further reinforces the preference for disposable systems during full-scale production.

At the same time, the Research & Development (R&D) segment is expanding at the fastest pace. R&D environments demand flexibility to conduct numerous experiments, change process parameters regularly, and move candidate molecules rapidly into clinical testing.

Single-use systems provide the adaptability required for pilot-scale operations, prototyping, and early clinical development without infrastructure constraints. As the global biologics pipeline broadens and innovation accelerates, R&D is expected to maintain its strong growth momentum over the coming years.

Region-wise Insights

North America Single-Use Bioprocess Systems Market Trends

North America remains the leading regional market for single-use bioprocess systems, accounting for roughly 35% of the global share in 2025.

The region benefits from a strong concentration of major biopharmaceutical companies, contract manufacturers, and technology suppliers, backed by well-established biomanufacturing infrastructure in the U.S. and Canada. A supportive regulatory framework encourages adoption of newer bioprocessing platforms, with U.S. FDA guidance allowing flexible validation pathways for single-use technologies in commercial production.

Substantial investment in R&D, particularly in advanced therapies such as monoclonal antibodies, cell therapies, and gene therapies, drives consistent technology upgrades across both clinical and commercial environments.

Collaboration is another major growth catalyst; strategic alliances between biotech innovators and CDMOs help accelerate process optimization, scale-up efficiency, and tech transfer. North American facilities are also at the forefront of incorporating automation, data analytics, and closed-system processing to meet high standards for sterility and productivity. Together, these elements firmly position the region as the innovation hub for single-use bioprocessing.

Asia Pacific Single-Use Bioprocess Systems Market Trends

Asia Pacific is gaining momentum as the fastest developing regional market for single-use bioprocess systems, driven by growing biopharmaceutical manufacturing capacity in China, Japan, India, South Korea, and Southeast Asian economies.

Governments and private investors are significantly expanding production capabilities for vaccines, biosimilars, and biologics, creating an environment where flexible and modular bioprocessing systems offer clear operational advantages. Lower labor costs, rising availability of skilled technical talent, and quick adoption of digital manufacturing tools support economically efficient scale-up of biologic production.

Regional facilities are increasingly integrated into global supply chains, supplying biosimilars, therapeutic proteins, and vaccine components to markets worldwide. Many pharmaceutical firms are shifting a portion of their commercial and clinical manufacturing to Asia Pacific due to favorable cost structures and accelerated facility commissioning.

Industrial parks and biotechnology clusters across China and India have further strengthened supply ecosystems for raw materials, consumables, and equipment. These combined factors continue to elevate Asia Pacific as a strategic growth engine for single-use bioprocessing worldwide.

Competitive Landscape

The market is moderately consolidated, with major companies like Thermo Fisher Scientific, Sartorius Stedim Biotech, Danaher Corporation, and Merck KGaA occupying significant shares.

Competitive differentiation centers on process integration, automation, and custom modular solutions for GMP and clinical production. Collaborative R&D projects and service bundling are key growth strategies, while niche innovators like Eppendorf AG and Avantor compete via specialized mixing and container technologies.

Key Industry Developments:

- In September 2023, Getinge introduced the AppliFlex ST GMP, a single-use bioreactor designed for commercial-scale applications. The system is offered in multiple capacity options and supports full cGMP compliance, making it suitable for mRNA manufacturing as well as cell and gene therapy production workflows.

- In September 2022, Thermo Fisher Scientific Inc. launched the Thermo Scientific DynaSpin single-use centrifuge system at the BioProcess International Annual Conference in Boston, Massachusetts, to provide the finest single-use option for mass cell culture harvesting.

Companies Covered in Single-Use Bioprocess Systems Market

- Thermo Fisher Scientific Inc.

- Sartorius Stedim Biotech

- Danaher Corporation

- Merck KGaA

- Corning

- Avantor

- CESCO Bioengineering Co. Ltd.

- PBS Biotech, Inc.

- Distek, Inc.

- Eppendorf AG

- Celltainer Biotech B.V.

- Getinge (Applikon Biotechnology)

- Cellexus Ltd.

- Parker Hannifin Corp

- Others

Frequently Asked Questions

The global singe use bioprocess systems market is projected to be valued at US$ 8.3 Bn in 2026.

Expansion in biologics manufacturing and operational efficiency boost demand for cost-effective, flexible production.

The global market is poised to witness a CAGR of 13.2% between 2026 and 2033.

Automated, sensor-integrated single-use platforms enable rapid, high-quality production for personalized medicines.

Thermo Fisher Scientific Inc., Sartorius Stedim Biotech, and Danaher Corporation are the top three producers of single-use bioprocess systems.